South Korea Electric Vehicle Battery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

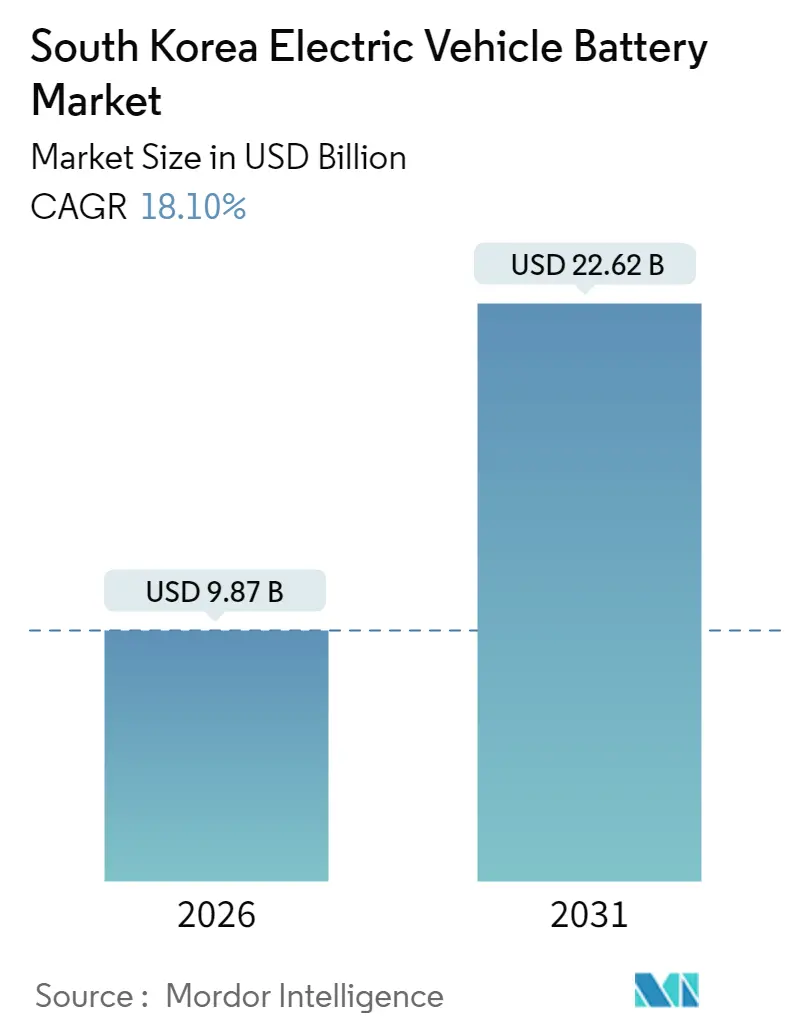

| Market Size (2026) | USD 9.87 Billion |

| Market Size (2031) | USD 22.62 Billion |

| Growth Rate (2026 - 2031) | 18.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Electric Vehicle Battery Market Analysis by Mordor Intelligence

The South Korea Electric Vehicle Battery Market is expected to grow from USD 8.36 billion in 2025 to USD 9.87 billion in 2026 and is forecast to reach USD 22.62 billion by 2031 at 18.1% CAGR over 2026-2031. The current South Korea electric vehicle battery market size demonstrates the nation’s ability to convert long-term industrial policy into immediate commercial scale, helped by rapid giga-factory build-outs and targeted consumer incentives. Demand surges as domestic automakers accelerate electrified model launches, while defense procurement and second-life initiatives open parallel revenue channels that lessen exposure to raw-material cost swings. Competitive intensity remains high. Yet, local firms sustain a technological edge in high-nickel and emerging LFP chemistries, allowing them to defend premium pricing in export markets. Grid-capacity constraints and commodity volatility weigh on near-term margins. Still, recycling frameworks and vertical integration efforts mitigate structural risks, underscoring the resilience of the South Korean electric vehicle battery market.

Key Report Takeaways

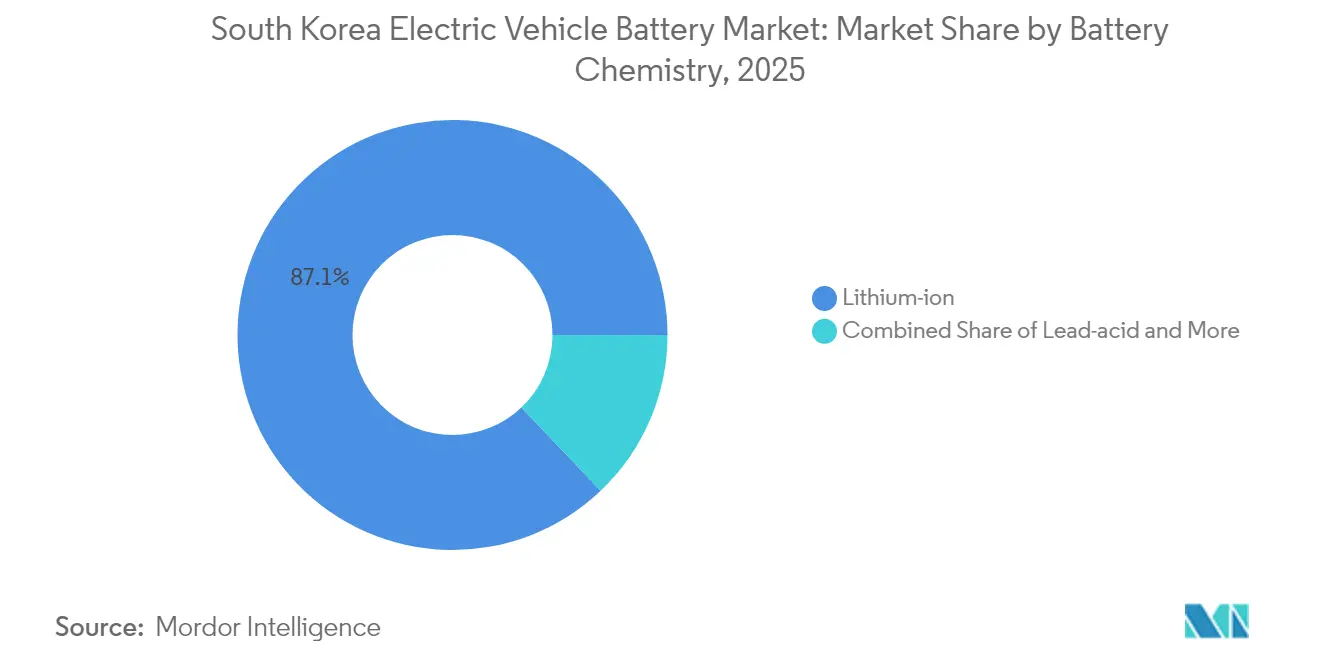

- By battery chemistry, lithium-ion led with 87.10% revenue share of the South Korean electric vehicle battery market in 2025, and it is also growing at a robust CAGR of 18.08% through 2031.

- By vehicle type, battery electric vehicles commanded 72.65% of South Korea's electric vehicle battery market share in 2025, while plug-in hybrid electric vehicles are projected to post an 18.22% CAGR through 2031.

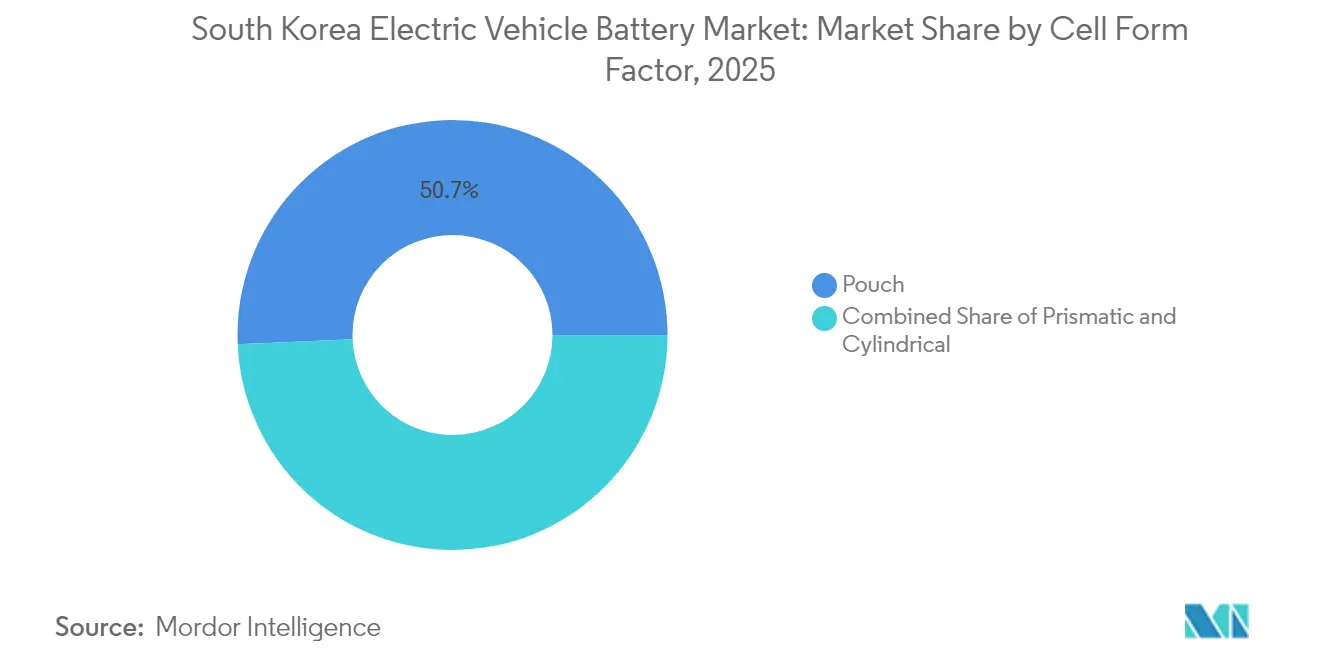

- By cell form factor, pouch cells accounted for 50.68% of the South Korean electric vehicle battery market size in 2025, and cylindrical cells are expected to expand at an 18.31% CAGR to 2031.

- By battery component, cathode active material captured 36.25% share of the South Korean electric vehicle battery market size in 2025, whereas separators are forecast to grow at 18.28% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Electric Vehicle Battery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM-Backed Giga-Factory Build-Outs | +4.1% | National core, with expansion to North America and Europe | Short term (≤ 2 years) |

| Escalating Government EV-Adoption | +3.2% | National, with spillover to ASEAN export markets | Medium term (2-4 years) |

| Rapid Growth In Domestic EV Exports | +2.8% | National production, global market reach | Medium term (2-4 years) |

| Rising ESS-To-EV Line Conversions | +1.9% | National, with technology transfer potential | Long term (≥ 4 years) |

| Second-Life Battery Repurposing Incentives | +1.1% | National, with regional demonstration effects | Medium term (2-4 years) |

| Military Electrification Programs | +0.7% | National defense applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OEM-Backed Giga-Factory Build-Outs

Between 2025 and 2028, Korean firms are executing a synchronized capacity surge exceeding 200 GWh, financed through rights issues, multilateral loans, and joint ventures. SK On completed its first solid-state pilot line in September 2025, giving the company a developmental lead in post-lithium chemistries [1]“Completion of Solid-State Pilot Line,” SK On, skon.com . Samsung SDI raised a vast amount in March 2025 to fund high-nickel and LFP modules. LG Energy Solution’s Michigan LFP project and a supply agreement with Tesla bind future cash flows to U.S. policy incentives [2]“Michigan LFP Investment Release,” LG Energy Solution, lges.com . The Blue Oval SK joint venture secured a massive amount in Department of Energy financing, confirming the strategic importance of Korean know-how to North American electrification. These announcements compress payback periods and position the South Korean electric vehicle battery market as the design hub supporting a dispersed manufacturing footprint.

Escalating Government EV-Adoption Mandates

Korea’s revised subsidy schedule eliminates many imported models from incentive eligibility, channeling household purchases toward Hyundai and Kia platforms that exclusively source domestic cells [3]“2025 Strategic Industries Tax Credit Scheme,” Ministry of Economy and Finance, moef.go.kr . The program also covers light-duty commercial fleets and military vehicles, further deepening captive demand for the South Korean electric vehicle battery market. A 2025 budget allocation of up to KRW 200 billion extends preferential tax credits to battery plants labeled “advanced strategic industries,” trimming effective capital costs by as much as three-fifths [4]“Advanced Battery Grant Guidelines,” Ministry of Trade, Industry and Energy, motie.go.kr. Southeast Asian partner states mirror these rules through bilateral memoranda, creating export demand for Korean-made packs. Korea’s volume-based waste charging system and extended producer responsibility laws, which have been in force since 2003, supply the regulatory backbone for closed-loop material recovery, reinforcing domestic value retention.

Rapid Growth in Domestic EV Exports

Hyundai Motor Group shipped a record nearly three lakh battery-electric cars in 2024, a one-fifth year-on-year jump that directly translates into higher cell pull-through for local suppliers. Planned investment in the Georgia assembly represents a template for co-located battery sourcing, lowering freight and inventory costs. Still, the Federation of Korean Industries estimates restrictive U.S. tax credits could trim outward sales by a considerable amount yearly, exposing the South Korean electric vehicle battery market to regulatory swings. Global installations grew exponentially in Q1 2025, and Korean brands retained one-fifth share despite greater Chinese penetration, demonstrating that volume growth can coexist with sliding share ratios.

Rising ESS-to-EV Line Conversions

Maturing stationary-storage demand has prompted LG Energy Solution, Samsung SDI, and SK On to retool idle ESS capacity for automotive cells, raising blended factory utilization above four-fifths in 2025. Conversion leverages existing dry-room, calendaring, and formation assets, cutting capital intensity by one-fourth versus greenfield builds. Convergence of ESS and EV performance specs around cycle life and thermal tolerance simplifies design transfer, while flexible scheduling allows firms to toggle between markets if either segment softens. The strategy broadens output options for the South Korean electric vehicle battery market and acts as a hedge against commodity price shocks that affect deployment economics differently across use cases.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nickel + Lithium Price Volatility | -2.4% | Global supply chains, concentrated impact on Korean refiners | Short term (≤ 2 years) |

| Grid-Capacity Bottlenecks | -1.8% | National infrastructure constraints | Medium term (2-4 years) |

| Heightened ESG Scrutiny | -1.1% | Global operations, supply chain transparency | Long term (≥ 4 years) |

| Domestic Skilled-Labor Shortages | -0.9% | National manufacturing base | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility

Due to their high-nickel cathode mix, Korean manufacturers carry added exposure to nickel swings. POSCO Future M’s diversification into non-Chinese graphite underscores the urgency of raw-material hedging. LG Chem’s March 2025 reveal of precursor-free LFP cathodes seeks to lessen dependence on volatile feedstocks. Meanwhile, domestic electricity tariffs climbed three-fifths from 2022 to 2024, amplifying input cost pass-through risks within the South Korean electric vehicle battery market.

Grid-Capacity Bottlenecks at New Cell Plants

Gigawatt-scale plants require up to 900 GWh of steady power annually, yet local substations often hit capacity ceilings during commissioning. Government commitments to expand high-voltage links lag implementation, forcing manufacturers to stagger ramp-ups or add on-site generation that raises capex. SK Nexilis cited power prices less than half Korean levels when justifying Malaysian expansion, reflecting how domestic grid limits dent cost competitiveness. Concentrated industrial parks intensify peak loads, disrupting process stability for cathode calcination and cell formation. These bottlenecks delay output, constrict the South Korean electric vehicle battery market, and compel firms to diversify buildouts overseas.

Segment Analysis

By Battery Chemistry: Lithium-ion Sustains Dominance While LFP Gains Ground

Lithium-ion technology accounted for 87.10% of the South Korean electric vehicle battery market in 2025, and the segment is forecast to grow at an 18.08% CAGR to 2031 as incremental improvements in high-nickel and silicon-rich anodes push performance benchmarks further. This chemistry continues to benefit from entrenched supply networks and advanced automation, allowing scale advantages that smaller alternatives struggle to match. Research initiatives such as LG Chem’s precursor-free cathodes cut energy use by 20% in coating stages, driving cost parity with entry-level chemistries. Conversely, lead-acid and nickel-metal hydride remain relegated to auxiliary and hybrid niches, reducing relevance as lithium-ion costs slide.

LFP capacity additions mark a strategic hedge against nickel volatility and emerging mass-market EV price points for Korean players. Next-generation R&D efforts at POSTECH explore fluoride-free systems to satisfy looming RoHS restrictions and enhance ion mobility. This widening chemistry portfolio allows the South Korean electric vehicle battery market to serve value-tier cars without sacrificing premium leadership in energy-dense segments.

Note: Segment shares of all individual segments available upon report purchase

By Vehicle Type: BEVs Anchor Revenue as PHEVs Accelerate

Battery electric vehicles held 72.65% of the South Korean electric vehicle battery market in 2025, leveraging greater range capability and expanding fast-charge networks to convert internal-combustion loyalists. Hyundai’s 300 Wh/kg LFP pack prototype cuts 7 minutes off two-fifths of the charging time, lifting consumer acceptance and strengthening local demand. Though smaller in volume, Plug-in hybrids are forecast to post an 18.22% CAGR through 2031 as automakers use them to meet tightening fleet-average requirements in cost-sensitive export regions.

Hybrid electric vehicles still fill a practicality gap in markets with sparse charging, giving Korean suppliers steady baseline orders that smooth factory utilization. Samsung SDI’s robot-platform battery deal illustrates how non-passenger segments diversify revenue streams, reinforcing the South Korean electric vehicle battery market against cyclical swings in personal vehicle sales.

By Cell Form Factor: Pouch Supremacy Faces Cylindrical Expansion

Pouch cells captured 50.68% of the South Korean electric vehicle battery market size in 2025, benefiting from design flexibility that lets automakers maximize cabin volume and manage thermal loads efficiently. However, cylindrical cells are projected to expand at an 18.31% CAGR through 2031 as automation advances drive down per-unit costs and Tesla’s 4680 standard gains broad OEM acceptance. LG Energy Solution’s new 46-series range bridges the structural advantages of prismatic formats with the cost profile of cylindrical, ensuring Korean manufacturers maintain a presence across architectures.

Prismatic formats retain specialized demand in commercial vehicles that value mechanical rigidity. Continuous form-factor diversification underpins the competitiveness of the South Korean electric vehicle battery market by matching varied OEM pack philosophies without compromising supply-chain economies of scale.

Note: Segment shares of all individual segments available upon report purchase

By Battery Component: Cathode Materials Drive Value Creation

Cathode active material claimed 36.25% share of the South Korean electric vehicle battery market in 2025, reinforcing its role as the principal cost and performance lever in cell economics. Korean specialists EcoPro BM and L&F chase high-nickel NCM and manganese-rich variations to raise energy density above 750 Wh/L. Meanwhile, separators lead growth at an 18.28% CAGR as ceramic-coated films extend safety envelopes to 180 °C operating thresholds, permitting faster-charging architectures.

Anode R&D focuses on gradient-structured silicon integrations that deliver 10% energy gains with negligible swelling. Electrolyte innovators pursue fluoro-ether blends to widen temperature windows and align with forthcoming PFAS restrictions, ensuring the South Korean electric vehicle battery market sustains compliance-driven differentiation opportunities.

Geography Analysis

Domestic installations remain the bedrock of the South Korean electric vehicle battery market, with local demand supported by protectionist subsidies and a four-fifths recycling rate achieved under long-standing EPR rules. Military procurement adds a strategic layer as Samsung SDI supplies submarine batteries, extending utilization beyond civilian cars. Stable home-market cash flows finance aggressive foreign expansion while cushioning margin compression from export headwinds.

North America has emerged as the fastest external growth node following the U.S. Inflation Reduction Act. LG Energy Solution’s Michigan line and Blue Origin SK’s triplet of plants commit a considerable amount, unlocking supply deals with Ford and Tesla that elevate Korean content in U.S. vehicle assemblies. However, Policy-linked eligibility caps could trim Korean vehicle exports, which grew exponentially yearly, a scenario that underscores the need for further localization.

Due to strict fleet-average CO₂ limits and pension-fund ESG mandates, Europe offers complementary demand, enticing Samsung SDI and SK On into Polish and Hungarian ventures. Yet logistics and energy-price volatility require hedging strategies such as building cathode precursor facilities inside the block. ASEAN markets provide volume upside and tariff relief owing to existing FTAs, allowing Korean firms to counter Chinese pricing through brand positioning around reliability and safety, thereby broadening the geographic diversification base of the South Korean electric vehicle battery market.

Competitive Landscape

Market concentration is high, with LG Energy Solution, Samsung SDI, and SK On collectively commanding most of domestic capacity and holding one-fifth of global installations in Q1 2025. LG Energy Solution emphasizes open-innovation alliances, signing a multi-year agreement with Tesla and co-developing silicon-rich anodes with startup Sila Nanotechnologies.

Samsung SDI prioritizes premium automotive niches, announcing a 10-layer stacked solid-state prototype promising 900 Wh/L by 2026. SK On advances vertical integration, merging upstream trading units to streamline nickel and graphite procurement.

White-space growth appears in circular-economy plays. Thoth Inc.’s AI robotic disassembly platform, winner of four CES 2025 awards, aims to trim recycling labor costs by two-fifths, offering collaborations with Korea’s legally mandated waste-recovery quotas. The national RoHS update, effective 2026, forces smaller foreign entrants to upgrade compliance systems, indirectly protecting incumbent share in the South Korean electric vehicle battery market. Intellectual-property barriers strengthen as POSTECH’s fluoride-free binder patents receive U.S. approvals, limiting imitation and sustaining premium margins.

South Korea Electric Vehicle Battery Industry Leaders

LG Energy Solution Ltd

Samsung SDI Co. Ltd

SK Innovation Co. Ltd

Hyundai Motor Group

POSCO Future M

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: SK On inaugurated its inaugural solid-state battery pilot plant, aiming to revolutionize battery technology with a commercial rollout planned by 2027. This move is expected to enhance energy density and safety in batteries, catering to the growing demand for advanced energy storage solutions.

- September 2025: L&F unveiled 'L&F Plus' following a hefty investment of KRW 338.2 billion, establishing a 60,000-tonne LFP cathode facility in Daegu. This expansion is set to strengthen L&F's position in the global cathode materials market, addressing the increasing need for lithium iron phosphate (LFP) batteries in electric vehicles and energy storage systems.

- September 2025: GEM initiated proceedings for a Hong Kong IPO, aiming to amplify its recycling and upstream material capabilities across China, Indonesia, and South Korea. The IPO is expected to provide GEM with the necessary capital to expand its operations and support the global push toward sustainable and circular economies.

South Korea Electric Vehicle Battery Market Report Scope

An electric vehicle battery refers to the rechargeable energy storage device used in electric vehicles. It stores electrical energy that powers the vehicle's electric motor, allowing it to operate without the need for combustion engines. Electric vehicle batteries typically utilize lithium-ion or other advanced battery chemistries for efficient and reliable performance.

The scope of the South Korea Electric Vehicle Battery Market is segmented by Battery Type and Vehicle Type. By Vehicle Type, the market is segmented into Battery Electric Vehicles, Hybrid Electric Vehicles, and Plug-in Hybrid Electric Vehicles. By Battery Type, the market is segmented into Lead-acid Batteries, Lithium-ion Battery, and Other Battery Types. Other Battery types segment include Nickel-Metal Hydride batteries, solid-state batteries, ultracapacitors, etc.

For each segment, market sizing and forecast have been done on the basis of value in USD.

| Lithium-ion |

| Lead-acid |

| Nickel-Metal Hydride |

| Others |

| Battery Electric Vehicles |

| Hybrid Electric Vehicles |

| Plug-in Hybrid Electric Vehicles |

| Pouch |

| Prismatic |

| Cylindrical |

| Cathode Active Material |

| Anode Active Material |

| Electrolyte |

| Separator |

| Others |

| By Battery Chemistry | Lithium-ion |

| Lead-acid | |

| Nickel-Metal Hydride | |

| Others | |

| By Vehicle Type | Battery Electric Vehicles |

| Hybrid Electric Vehicles | |

| Plug-in Hybrid Electric Vehicles | |

| By Cell Form Factor | Pouch |

| Prismatic | |

| Cylindrical | |

| By Battery Component | Cathode Active Material |

| Anode Active Material | |

| Electrolyte | |

| Separator | |

| Others |

Key Questions Answered in the Report

How large is the South Korean electric vehicle battery market in 2026?

The market is valued at USD 9.87 billion and is forecast to grow at an 18.1% CAGR to 2031.

Which chemistry dominates current production?

Lithium-ion holds 87.10% share, driven by high-nickel and emerging LFP product mixes.

What is the fastest-growing vehicle segment for Korean batteries?

Plug-in hybrid electric vehicles are projected to increase by 18.22% CAGR between 2026 and 2031.

Why are Korean firms converting ESS lines to EV battery output?

Higher automotive margins and converging performance specifications enable flexible capacity that raises overall plant utilization.

How are raw material price risks being mitigated?

Firms pursue vertical integration, secure alternative graphite and nickel sources, and develop precursor-free cathodes to reduce dependence on volatile inputs.