Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

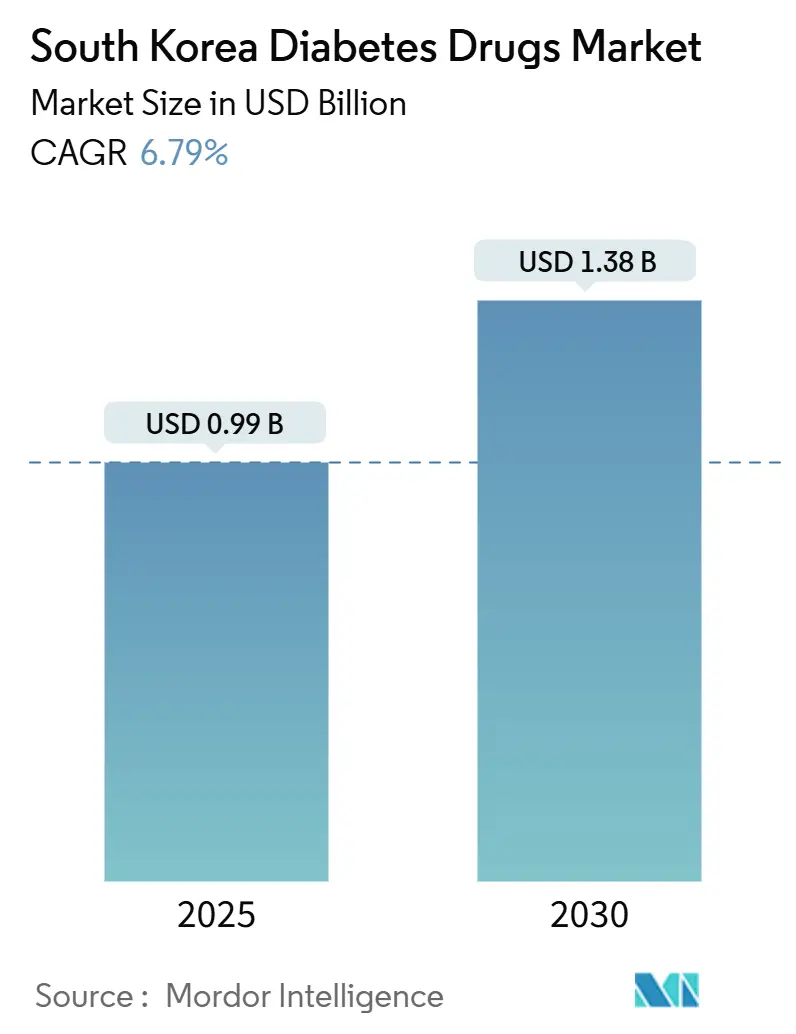

| Market Size (2025) | USD 0.99 Billion |

| Market Size (2030) | USD 1.38 Billion |

| Growth Rate (2025 - 2030) | 6.79% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Diabetes Drugs Market Analysis by Mordor Intelligence

The South Korea diabetes drugs market is valued at USD 995 million in 2025 and is anticipated to reach USD 1.38 billion by 2030, registering a 6.79% CAGR over the forecast period. Accelerating growth stems from a rapid rise in disease prevalence, an ageing population, and continuing urban lifestyle shifts. Novel agents that combine glycaemic control with cardio-renal and weight-management benefits are reshaping prescribing behaviour. Digital health solutions that link medication, monitoring, and coaching are embedding themselves in routine care and opening new distribution channels. Meanwhile, supply security for glucagon-like peptide-1 (GLP-1) agents, stricter reimbursement discussions, and an evolving biosimilar pipeline shape the competitive climate

Key Report Takeaways

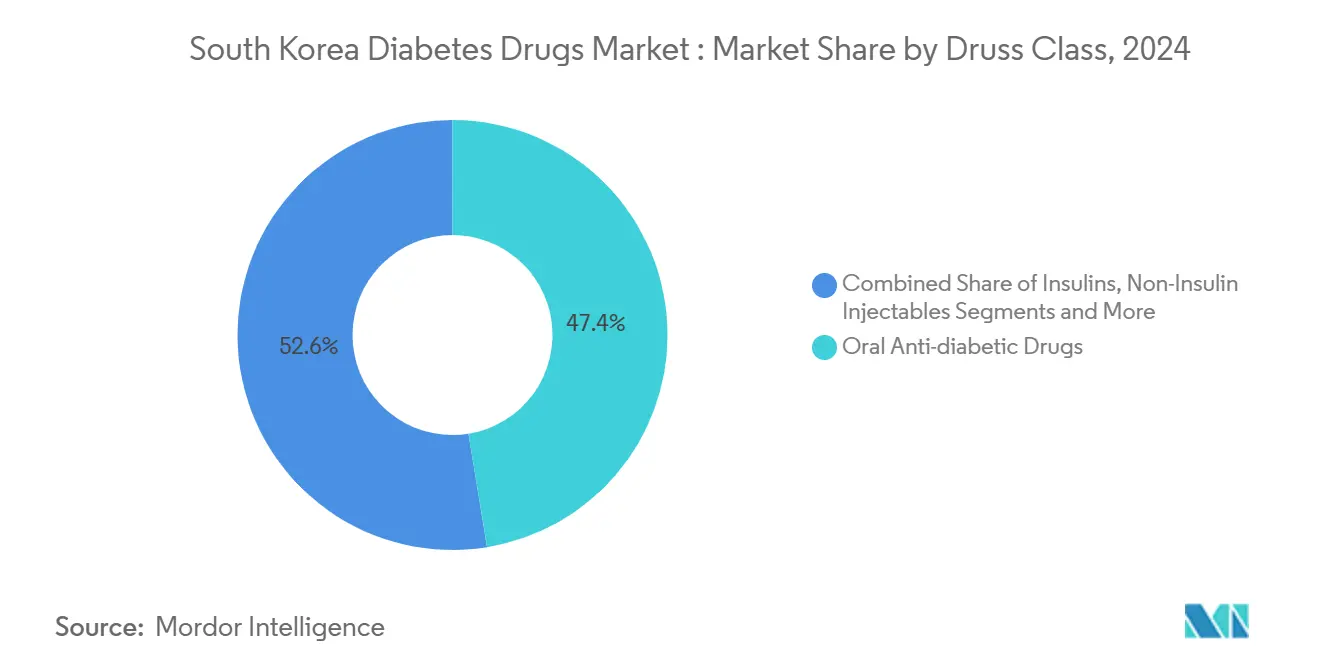

- By drug class, oral agents retained 47.43% revenue share in 2024, whereas non-insulin injectables are projected to rise at a 10.03% CAGR through 2030.

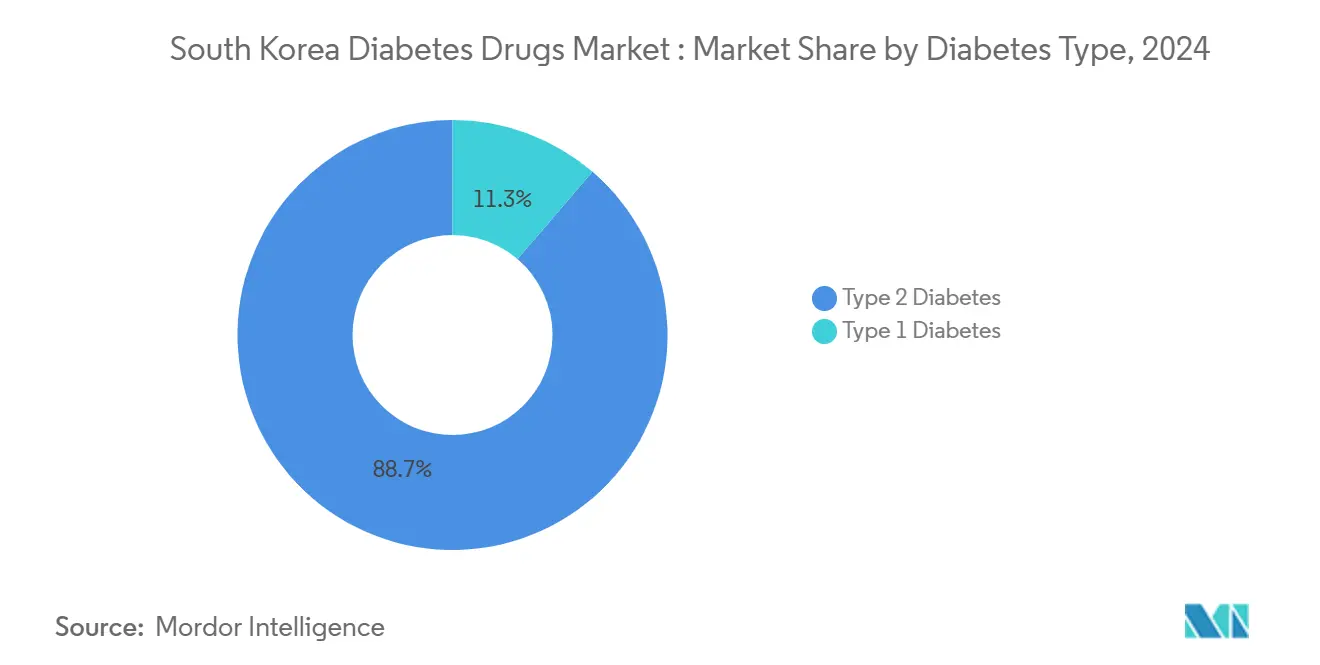

- By diabetes type, Type 2 cases accounted for 88.72% of the South Korea diabetes drugs market share in 2024 and are growing at a 7.56% CAGR to 2030.

- By drug origin, innovators held 64.82% of the South Korea diabetes drugs market size in 2024, yet biosimilars and generics are expanding at a 9.04% CAGR.

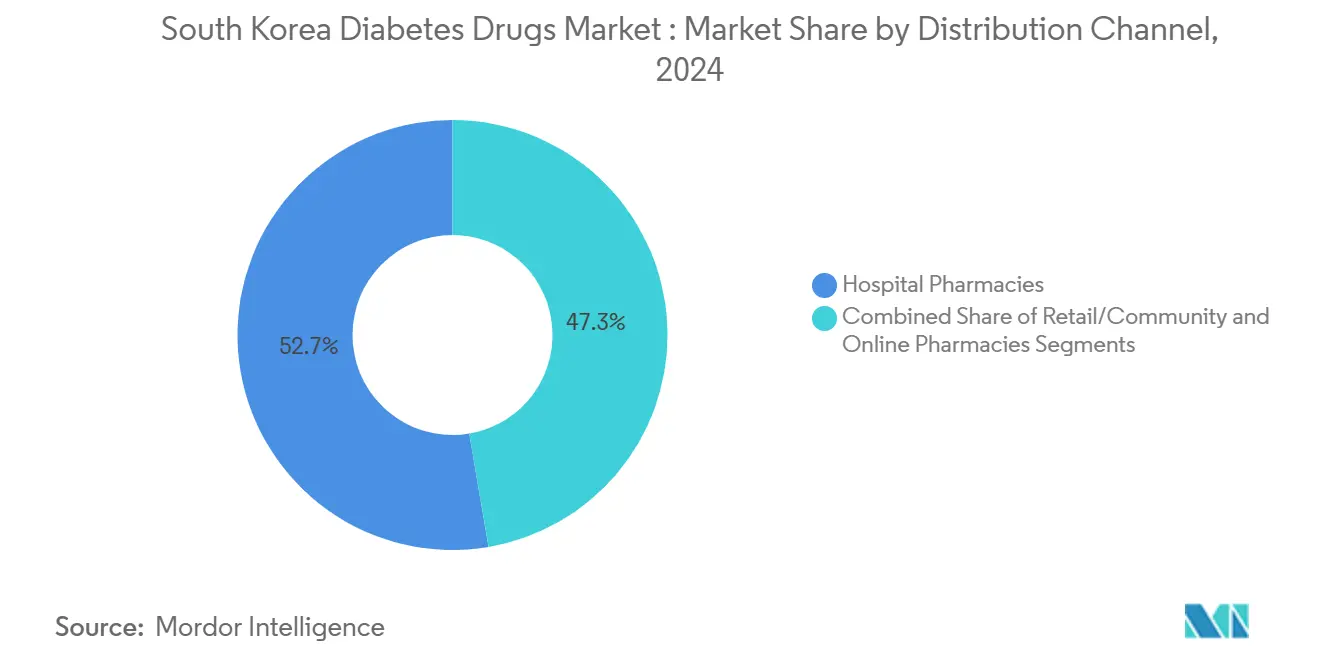

- By distribution channel, hospital pharmacies commanded 52.67% share in 2024, while online pharmacies show the fastest growth at 9.79% CAGR.

South Korea Diabetes Drugs Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diabetes prevalence and obesity burden | +1.8% | National; urban centres | Long term (≥ 4 years) |

| Preference for innovative and combination therapies | +1.2% | National; tertiary hospitals | Medium term (2-4 years) |

| Ageing population and urban lifestyles | +1.5% | Nationwide; Seoul-Incheon corridor | Long term (≥ 4 years) |

| Government reimbursement for novel agents | +0.9% | National | Medium term (2-4 years) |

| Digital health integration in diabetes management | +0.7% | Major cities | Short term (≤ 2 years) |

| Expanding R&D and global licensing collaborations | +0.6% | Nationwide with global partners | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes Prevalence and Obesity Burden

Diabetes prevalence among adults aged 30 and older stood at 16.7% in 2024, making the disease Korea’s largest contributor to disability-adjusted life years. Obesity remains the key co-morbidity, as 73% of patients are overweight or obese.[1]Sung-Hee Oh, “Prevalence and Socioeconomic Burden of Diabetes Mellitus in South Korean Adults,” BMC Public Health, bmcpublichealth.biomedcentral.com Sugar intake trends deepen the challenge, with one-fifth of children exceeding recommended levels.[2]Hyejin Yu and Sang-Jin Chung, “Total Sugar Intake and Its Contributed Foods by Age Groups in Koreans,” Korean Journal of Community Nutrition, kjcn.or.kr Combined, these factors keep demand for established oral agents high while encouraging adoption of GLP-1 and sodium–glucose cotransporter-2 (SGLT-2)–based therapies. Lean diabetes, affecting 8.8% of patients, adds clinical complexity and underpins the need for personalised regimens.

Preference for Innovative and Combination Therapies

Updated Korean Diabetes Association guidance directs clinicians toward multi-mechanism regimens that optimise glycaemic control, cardiovascular protection, and renal outcomes. Phase 3 data on a triple agonist (efpeglenatide) targeting GLP-1, glucose-dependent insulinotropic polypeptide, and glucagon receptors highlight the climate of clinically oriented innovation. Low-dose lobeglitazone studies demonstrate non-inferior efficacy with fewer side effects, supporting wider adoption.[3]Soree Ryang et al., “REFIND Study on Low-Dose Lobeglitazone,” National Center for Biotechnology Information, ncbi.nlm.nih.govMarket appetite for fixed-dose combinations is reinforced by the approval of the triple oral agent metformin-dapagliflozin-sitagliptin in 2025, offering simpler dosing and better adherence.

Ageing Population and Urban Lifestyles

Adults aged 65 and older form Korea’s fastest-growing demographic segment, and this group shows the highest diabetes incidence. Urban residents face amplified exposure to sedentary jobs and processed food intake, further raising risk. The Act on Integrated Support for Community Care mandates home-centric, digitally enabled chronic disease care from 2026. Pharmaceutical companies thus focus on elder-friendly formulations, remote monitoring devices, and adherence aids.

Government Reimbursement for Novel Agents

National Health Insurance has introduced value-based frameworks that reward clinical benefit while containing costs. Generic price indices, however, remain higher than those in many peer countries. Manufacturers, therefore, invest in real-world evidence dossiers to strengthen cost-effectiveness arguments. Risk-sharing agreements and conditional listings create opportunities for high-value products that deliver measurable outcomes.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent price cuts and reimbursement delays | -1.1% | National | Medium term (2-4 years) |

| Safety concerns, including ketoacidosis | -0.6% | Nationwide; elderly focus | Short term (≤ 2 years) |

| GLP-1 supply shortages and import caps | -0.8% | Nationwide; premium tier | Short term (≤ 2 years) |

| Clinical inertia despite guideline updates | -0.4% | Primary-care settings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Price Cuts and Reimbursement Delays

Aggressive cost-containment under the Drug Expenditure Rationalization Plan compresses margins for novel therapies. Generic price indices declined only marginally from 4.79 to 3.40 versus the United States benchmark between 2020 and 2022, signifying limited relief. Manufacturers face protracted negotiations, prompting strategic launches of evidence packages that document cardio-renal benefits and long-term cost offsets.

Safety Concerns, Including Ketoacidosis

Expanded use of SGLT-2 inhibitors and GLP-1 agents triggers vigilance over rare but serious adverse events such as ketoacidosis in elderly or renal-impaired patients. Post-marketing surveillance studies are therefore front-loaded to secure clinician confidence, sometimes delaying promotional momentum.

Segment Analysis

By Drug Class: Oral Agents Lead Despite Injectable Innovation

The South Korea diabetes drugs market size for oral agents stood at USD 472 million in 2024, accounting for 47.43% of total sales. SGLT-2 inhibitors and dipeptidyl peptidase-4 (DPP-4) inhibitors dominate prescribing volumes, supported by an 87.5% medication adherence rate among older adults. Nevertheless, non-insulin injectables are accelerating at a double-digit 10.03% CAGR as GLP-1 receptor agonists prove effective in weight control and cardio-renal protection. Cardiovascular-outcome trials continue to expand label indications, encouraging earlier initiation in high-risk patients. Low-dose lobeglitazone achieved non-inferior glucose reduction while lowering side-effect rates, exemplifying the quest for safer profiles. Fixed-dose triple combinations reduce pill burden and improve adherence, supporting treatment intensification without patient fatigue.

Within non-insulin injectables, patient acceptance is rising due to thinner needles, autoinjector devices, and once-weekly dosing. Biosimilar development and local fill-and-finish capacity are expected to moderate prices and alleviate shortages over the next five years. Oral GLP-1 development programmes, leveraging permeability enhancers and nanoparticle carriers, could blur class boundaries by 2030. Insulin remains indispensable for Type 1 and advanced Type 2 patients, and high-concentration formulations provide flexibility for dose-intensive regimens aimed at overcoming insulin resistance.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Diabetes Type: Type 2 Dominance Drives Growth

In 2024, Type 2 patients generated 88.72% of the South Korea diabetes drugs market. Rising obesity and ageing lift the Type 2 case load, pushing forecasts toward 29.2% prevalence in men and 19.7% in women by 2030. Early combination therapy adoption aims to counter comorbidity clusters of hypertension and dyslipidaemia, improving overall outcomes. Type 1 population remains smaller yet technologically sophisticated, relying on sensor-integrated pumps and rapid-acting analogues for tight control. Paediatric Type 2 options are still limited to metformin, insulin, and liraglutide, indicating a clinical gap that innovators may address with youth-specific dosing and devices.

Lean diabetes, defined by lower body-mass index yet impaired insulin secretion, commands research attention for its unique pathophysiology. Herbal adjuncts, including red ginseng extract, demonstrated modest fasting glucose reductions in prediabetic adults, hinting at culturally familiar complementary options.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Drug Origin: Biosimilars Gain Ground Against Innovators

Innovator brands commanded 64.82% of the South Korea diabetes drugs market share in 2024, but the biosimilar cohort is expanding at a 9.04% CAGR. Samsung Bioepis and GC Corp lead with diversified portfolios that encompass insulin, growth hormone, and monoclonal antibody biosimilars. Tiered pricing encourages early generic entry while rewarding innovation with temporary premium tiers. Domestic firms target complex injectables and high-volume oral agents, leveraging state incentives for biologics manufacturing. International alliances accelerate know-how transfer, as seen in HK inno.N’s GLP-1 collaboration.

Oramed’s oral insulin licence could erode innovators’ basal insulin share by offering needle-free convenience. Yet innovators retain differentiation through proprietary delivery systems, extended-release profiles, and continuous data connectivity.

By Distribution Channel: Digital Transformation Reshapes Access

Hospital pharmacies retained 52.67% of 2024 sales, reflecting the country’s specialist-led care model. The South Korea diabetes drugs market size handled by online pharmacies grew sharply after regulatory allowances for teleconsultations during the pandemic. Telemedicine platforms integrate e-prescriptions, point-of-care diagnostics, and doorstep delivery, giving chronic patients frictionless refills. Community pharmacies maintain patient education roles, particularly in suburban and rural locales where broadband constraints limit virtual care.

From 2026, community-care legislation will reimburse home-based monitoring devices and coaching apps. Continuous glucose monitors and sensor-augmented pumps require technical support, prompting certain chains to open specialist centres. Retail loyalty programmes that link drug refills with nutrition counselling and wearable data uploads differentiate offerings and build retention.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Regional diabetes patterns mirror demographic and lifestyle gradients. The Seoul-Incheon megalopolis exhibits the highest prevalence due to dense fast-food outlets, sedentary office work, and stress-related behaviours. Here, tertiary hospitals offer early access to GLP-1 and SGLT-2 therapies, accelerating urban uptake. Rural provinces, characterised by quicker population ageing and limited specialist supply, have less access to novel agents and rely more on generics and traditional oriental medicine. Government policy directs additional funding toward telemedicine and mobile clinics to equalise care standards.

Continuous-glucose-monitor penetration is highest in metropolitan school programmes aimed at early detection. Provincial centres adopt community-health-worker models that pair basic test strips with smartphone coaching, gradually bridging the technology gap. Manufacturing clusters in Gyeongbuk and Chungbuk provinces support local supply of metformin, gliclazide, and biosimilar insulin, reducing import dependence for essential medicines. National procurement frameworks adjust stock levels based on surge alerts for GLP-1 shortages broadcast by the World Health Organization.

Urban lifestyle campaigns that promote active commuting and sugar-content labelling are likely to slow incidence growth in affluent districts, but socio-economic disparities persist, with lower-income boroughs reporting higher complication rates. Pharmacies in Busan are trialling blockchain-based traceability for high-value injectables, signalling regional experimentation with advanced supply-chain safeguards.

Competitive Landscape

Competition is innovation-centred and moderately consolidated. Local champions such as Hanmi Pharmaceutical invest heavily in multi-agonist peptides, while multinationals protect franchise positions through lifecycle management that bundles drugs with digital services. Biosimilar entrants compress price points for mature insulins and DPP-4 inhibitors, pressuring innovators to pivot toward differentiated GLP-1 and dual-agonist pipelines. Strategic moves illustrate the dynamic such as Hanmi Pharmaceutical advanced efpeglenatide to Phase 3 for metabolic disease, HK inno.N licensed ecnoglutide, reinforcing the local GLP-1, GC Corp secured EU certification for a next-generation glucose monitor, expanding its value-chain footprint.

Digital partnerships between device manufacturers and pharmaceutical firms seek to embed prescription fills within remote-monitoring dashboards, thereby raising therapy stickiness and data-driven care optimisation. Real-world evidence repositories built on longitudinal insurance data help firms demonstrate economic value to payers, turning analytics into a critical competitive tool.

South Korea Diabetes Drugs Industry Leaders

Eli Lilly and Company

Novo Nordisk A/S

Sanofi

Merck & Co.

Hanmi Pharmaceutical

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: South Korea granted Diamyd Medical a patent covering insulin-based antigens for autoimmune diabetes in patients with the HLA DR4-DQ8 genetic marker.

- December 2024: Novo Nordisk Korea received MFDS approval for once-weekly basal insulin icodec (Awiqli) for adult diabetes treatment.

- August 2024: Yunovia secured MFDS investigational new drug clearance for Phase I trials of its small-molecule GLP-1 agonist ID110521156.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South Korea diabetes drugs market as the aggregate ex-factory sales value of prescription medicines, insulins, non-insulin injectables (for example, GLP-1 receptor agonists), and oral anti-hyperglycemics intended for chronic glycemic control in type 1 and type 2 adults and adolescents.

(Scope exclusion) Blood-glucose monitoring devices, nutraceuticals, and drugs used solely for diabetes complications (neuropathy, nephropathy, retinopathy) sit outside this boundary.

Segmentation Overview

- By Drug Class

- Insulins

- Oral Anti-diabetic Drugs

- Non-Insulin Injectables

- Combination Drugs

- By Diabetes Type

- Type 1 Diabetes

- Type 2 Diabetes

- By Drug Origin

- Innovator Brands

- Biosimilars / Generics

- By Distribution Channel

- Hospital Pharmacies

- Retail / Community Pharmacies

- Online Pharmacies

Detailed Research Methodology and Data Validation

Primary Research

Several semi-structured interviews and short surveys with endocrinologists, hospital pharmacists, payers, and domestic manufacturers across Seoul, Busan, and Daegu helped validate price corridors, formulary penetration rates, and biosimilar uptake. Follow-up calls clarified draft assumptions before numbers were locked.

Desk Research

Mordor analysts first mapped supply and demand using authoritative open datasets such as KOSIS pharmaceutical production statistics, Korean Diabetes Association prevalence surveys, National Health Insurance Service reimbursement dashboards, OECD Health at a Glance cost indices, and MFDS product-registration records.

Financial clues were then drawn from company 10-Ks, investor decks, and D&B Hoovers filings to approximate brand-level revenues.

News archives on Dow Jones Factiva and peer-reviewed journals supplied launch dates, patent expiries, and guideline changes that shift therapy mix.

These examples illustrate the tier 1 evidence pool; many other sources were referenced to cross-check figures and definitions.

Market-Sizing & Forecasting

The core model builds a top-down prevalence-to-treated cohort funnel, multiplying diagnosed patient counts by therapy adoption splits and average daily dose multiplied by average selling price.

Select bottom-up roll-ups of leading supplier revenues and channel checks temper aggregate totals.

Key variables tracked include adult diabetes prevalence, share of SGLT-2/GLP-1 prescriptions, NHIS reimbursement ceilings, generic erosion pace, and won-USD FX trends.

Multivariate regression, enriched with scenario analysis around obesity growth and pricing reform, projects values from 2025 to 2030.

Gaps in bottom-up inputs (for instance, private-clinic volumes) are bridged with calibrated substitution factors agreed during primary research.

Data Validation & Update Cycle

Outputs pass three tiers of review: automated anomaly flags, senior analyst variance checks versus external spend indicators, and final sign-off by the research lead.

Reports refresh yearly and are rereviewed on material events, such as drug recalls, guideline shifts, or price cuts, so clients receive the latest view.

Why Mordor's South Korea Diabetes Drugs Baseline Commands Confidence

Published estimates often diverge because firms pick different product sets, price bases, and refresh cadences. Recognizing this, we disclose scope and variables openly so buyers see exactly what is and is not included.

Key gap drivers arise when some publishers fold glucose-monitoring devices into 'drugs,' assume hospital list prices without rebate haircuts, or inflate near-term growth with global GLP-1 headlines that have limited local supply. Mordor reports, conversely, isolate pharmaceutical value, apply net-of-rebate ASPs, and refresh annually, which curbs overstatement.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.99 B (2025) | Mordor Intelligence | - |

| USD 1.70 B (2024) | Global Consultancy A | Includes OTC supplements and uses list prices |

| USD 1.05 B (2024) | Regional Analytics B | Relies on reimbursement spend, lacks price erosion adjustment |

| USD 1.13 B (2024) | Industry Data Service C | Bundles insulin pumps under antidiabetics |

In sum, by selecting a clear scope, mixing top-down epidemiology with grounded supplier read-outs, and stress-testing every assumption, Mordor delivers a dependable baseline that decision-makers can trace and replicate.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

1. What is the current value of the South Korea diabetes drugs market?

The market stands at USD 995 million in 2025 and is forecast to reach USD 1.38 billion by 2030.

2. Which therapeutic class leads sales in the South Korea diabetes drugs market?

Oral antidiabetic agents lead with 47.43% of 2024 revenue, though non-insulin injectables are growing fastest.

3. How dominant is Type 2 diabetes in South Korea?

Type 2 cases contribute 88.72% of total drug revenue and are projected to expand further at a 7.56% CAGR.

4. What role do biosimilars play in market dynamics?

Biosimilars and generics are growing at 9.04% CAGR, steadily eroding innovators’ share and lowering therapy costs.

5. How is digital health transforming distribution?

Online pharmacies and telemedicine platforms are expanding at 9.79% CAGR, offering integrated prescription, delivery, and monitoring services.

6. What are the main challenges facing manufacturers?

Stringent price negotiations, GLP-1 supply constraints, and the need for real-world evidence to secure reimbursement are key hurdles.