| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 4.88 Billion |

| Market Size (2030) | USD 7.64 Billion |

| CAGR (2025 - 2030) | 9.38 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

South Korea Aerospace and Defense Market Analysis

The South Korea Aerospace And Defense Market size is estimated at USD 4.88 billion in 2025, and is expected to reach USD 7.64 billion by 2030, at a CAGR of 9.38% during the forecast period (2025-2030).

South Korea's aerospace & defense industry is undergoing significant transformation driven by increased regional security concerns and technological advancement. The government has demonstrated a strong commitment to defense modernization, with the 2023 defense budget reaching approximately USD 47.9 billion, marking a 1.1% increase from the previous year. This substantial investment is part of a broader strategic initiative outlined in the 2022-2026 mid-term defense plan, which allocates USD 271.5 billion for comprehensive military modernization. The focus on indigenous development capabilities has become increasingly prominent, with domestic companies taking leading roles in major defense systems programs and establishing strategic partnerships with international defense contractors.

The country's space systems and satellite sector has emerged as a crucial focus area for technological advancement and strategic capability development. In August 2021, the Defense Acquisition Program Administration (DAPA) unveiled an ambitious roadmap involving an investment of USD 13.6 billion by 2031 to strengthen the nation's defense infrastructure capabilities in outer space. This strategic initiative encompasses the development of military reconnaissance satellites, space-based surveillance systems, and advanced communication networks. The commitment to space systems technology development is further evidenced by the increasing collaboration between government agencies and private sector companies in developing sophisticated satellite systems and launch vehicles.

South Korea's naval modernization program represents a significant component of its aerospace & defense industry development, with major shipbuilding companies leading various high-profile projects. The country's shipbuilding industry has demonstrated remarkable capabilities in producing advanced naval vessels, from sophisticated submarines to state-of-the-art destroyers. The emphasis on naval capability enhancement has led to increased investment in research and development of advanced naval technologies, including autonomous systems, advanced sonar capabilities, and integrated combat management systems.

The aerospace sector has witnessed substantial progress in indigenous aircraft development and manufacturing capabilities. A notable achievement is the increasing localization of components in major aerospace programs, with domestic manufacturers now producing approximately 65% of components for key projects like the KF-21 fighter aircraft program. This growing self-reliance in aerospace engineering has been accompanied by significant investments in research and development of advanced technologies, including unmanned aerial systems, artificial intelligence integration, and sophisticated avionics systems. The industry has also seen enhanced collaboration between domestic manufacturers and international partners, facilitating technology transfer and expertise sharing in critical aerospace technologies.

South Korea Aerospace and Defense Market Trends

Growing Air Traffic and Fleet Modernization

The robust growth in South Korea's aviation sector is evidenced by the significant increase in flight operations, with 539,788 flights recorded in FY 2023, marking a substantial rise from 465,469 flights in 2021. This surge in civil aviation has prompted major airlines to undertake extensive fleet modernization initiatives, as demonstrated by Korean Air's landmark decision in March 2024 to procure 33 A350 wide-body jets in a deal valued at USD 13.7 billion. This strategic investment reflects the airline's commitment to strengthening its long-haul capabilities while systematically retiring older aircraft to maintain operational efficiency and meet growing passenger demands.

The modernization drive is further exemplified by the adoption of advanced propulsion technologies, as evidenced by Korean Air's induction of its first GTF engine in November 2023. This technological advancement represents a significant step forward in the airline's efforts to enhance fuel efficiency and reduce operational costs. The increasing presence of low-cost carriers (LCCs) in the market has also catalyzed the modernization efforts of full-service carriers, compelling them to invest in newer, more efficient aircraft to maintain their competitive edge and meet evolving passenger preferences.

Understand The Key Trends Shaping This Market

Download PDF

Military Modernization and Defense Investments

South Korea's commitment to military modernization is demonstrated through substantial investments in upgrading its aerospace and defense capabilities. A prime example is the comprehensive F-15K fighter military aircraft fleet modernization program announced in November 2023, with an allocated budget of KRW 3.46 trillion (USD 2.72 billion) spanning from 2024 to 2034. This extensive program aims to enhance the mission capability and survivability of the force's 59 F-15K aircraft, reflecting the country's dedication to maintaining a technologically advanced air force. The program's scope encompasses various aspects of aircraft enhancement, from avionics upgrades to weapons systems improvements.

The country's robust military foundation, comprising thousands of military aircraft, generates an annual Maintenance, Repair, and Overhaul (MRO) demand exceeding USD 1 billion. This substantial demand has led to strategic partnerships, as evidenced by the collaboration between the Defense Acquisition Program Administration (DAPA) and Boeing announced in November 2023, focusing on enhancing South Korea's aviation maintenance capabilities. These initiatives encompass not only maintenance and repair activities but also significant upgrade work, demonstrating the country's holistic approach to military aviation advancement and sustainment.

Space Industry Development

South Korea's aerospace sector is experiencing significant growth through substantial investments in space industry technology and satellite manufacturing capabilities. The government's commitment is reflected in its allocation of USD 674 million for space programs in FY 2023, demonstrating a strong focus on developing indigenous space capabilities. This investment is channeled through the Korea Aerospace Research Institute (KARI), the country's primary government agency responsible for satellite research, development, and production, which has established itself as a crucial driver of technological advancement in the space sector.

The country's progress in space technology is exemplified by successful missions such as the Danuri lunar orbiter launch in August 2022, designed to survey valuable lunar resources including water ice, uranium, helium-3, silicon, and aluminum. This mission also aims to produce detailed topographic maps for future lunar landing sites, showcasing South Korea's growing capabilities in advanced space exploration. The emphasis on research and development has led to significant advancements in high-resolution imaging, remote sensing, and satellite systems, positioning South Korea as an emerging leader in satellite manufacturing and space industry applications.

Segment Analysis: Industry

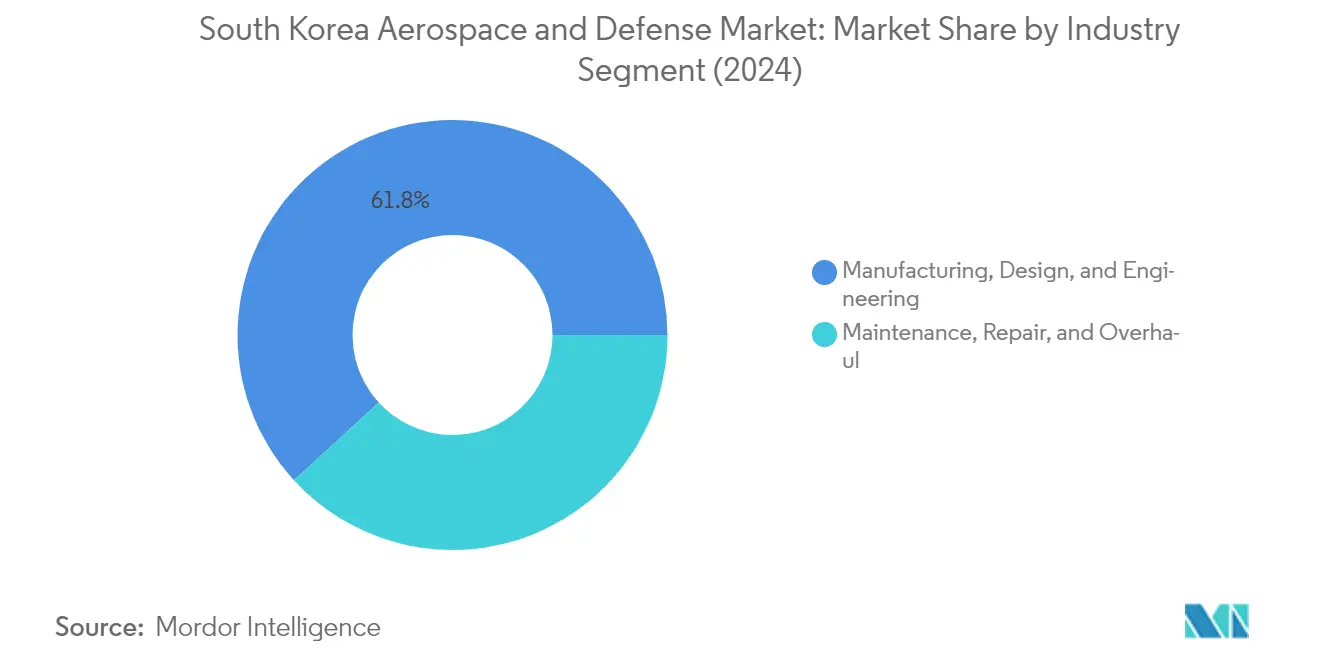

Manufacturing, Design, and Engineering Segment in South Korea Aerospace and Defense Market

The Manufacturing, Design, and Engineering segment dominates the South Korea aerospace & defense market, accounting for approximately 62% of the market share in 2024, while also being the fastest-growing segment. This segment is driven by major players like Korea Aerospace Industries (KAI) and Korean Air, who are actively involved in developing indigenous aircraft, including UAVs, rotor-wings, and fixed wings. The Korean Aerospace Valley, a cluster of small and medium-sized aerospace companies in the Gyeongnam area, further strengthens this segment by supplying aircraft parts and aerospace components to KAI and Korean Air while also focusing on exports. The segment's growth is bolstered by significant investments in space capabilities, with South Korea planning to invest approximately USD 13.6 billion over the next decade in advancing its defense capabilities in outer space. Additionally, the country's focus on unmanned systems development, led by KAI's successful deployment of reconnaissance UAVs and ongoing research in VTOL UAVs, strike-type UAVs, and UCAVs, continues to drive innovation in this segment.

Maintenance, Repair, and Overhaul Segment in South Korea Aerospace and Defense Market

The Maintenance, Repair, and Overhaul (MRO) segment plays a crucial role in supporting South Korea's aerospace & defense capabilities, representing about 38% of the market in 2024. This segment encompasses a wide range of aerospace services, including aircraft engine maintenance, naval vessel maintenance, and land vehicle support systems. The segment benefits from strategic facilities like KAEMS' new aircraft MRO center in Sacheon, which aims to become an aviation MRO hub in Asia. The presence of major players like Korean Air, which maintains its own MRO division with specialized facilities in Gimpo, Incheon, Gimhae, and Bucheon, further strengthens this segment. Additionally, the segment is supported by companies like Hanwha Aerospace, which has established strong partnerships with international firms like Rolls-Royce for military engine maintenance, demonstrating the segment's growing capabilities in servicing both domestic and international clients.

Segment Analysis: Type

Defense Segment in South Korea Aerospace and Defense Market

The defense systems segment continues to dominate the South Korea aerospace & defense market, holding approximately 83% of the market share in 2024. This significant market position is driven by South Korea's ongoing military modernization initiatives and increased defense spending amid regional security challenges. The country's focus on developing indigenous defense capabilities through programs like the KF-21 fighter jet development, naval vessel construction programs, and advanced missile defense systems has strengthened this segment's position. The defense segment encompasses various subsectors, including army, navy, and military aviation, with naval systems showing particularly strong growth due to significant investments in submarine development and surface vessel modernization programs. The government's emphasis on achieving greater self-reliance in defense manufacturing and the active participation of major domestic defense contractors like Hanwha Defense, LIG Nex1, and Korea Aerospace Industries have further consolidated this segment's market leadership.

Aerospace Segment in South Korea Aerospace and Defense Market

The commercial aerospace segment is emerging as the most dynamic sector in the South Korean aerospace & defense market, projected to grow at approximately 15% during the forecast period 2024-2029. This robust growth is primarily driven by South Korea's ambitious space program initiatives and expanding civil aviation sector. The country's increased focus on satellite development, space launch capabilities, and the establishment of indigenous space technology has created significant growth opportunities. The development of the Nuri rocket program, investments in satellite manufacturing capabilities, and plans to launch multiple satellites for various applications, including communication and earth observation, are key growth drivers. Additionally, the expansion of maintenance, repair, and overhaul (MRO) facilities and the government's support for developing the domestic aerospace industry through initiatives like the aerospace cluster in Sacheon are contributing to this segment's rapid growth trajectory.

South Korea Aerospace and Defense Industry Overview

Top Companies in South Korea Aerospace and Defense Market

The South Korean aerospace and defense market features a mix of established domestic players and international companies, with key participants including Korea Aerospace Industries, Hanwha Group, Korean Air Lines, Daewoo Shipbuilding & Marine Engineering, and Lockheed Martin Corporation. Companies are increasingly focusing on indigenous development capabilities, particularly in areas like fighter aircraft, naval vessels, and military systems. The industry demonstrates strong innovation trends in autonomous systems, AI-powered platforms, and space technologies, with significant investments in research and development. Strategic partnerships and technology transfer agreements between domestic and international players are becoming more prevalent, enabling local manufacturers to enhance their capabilities. Companies are expanding their manufacturing footprint while simultaneously developing advanced maintenance, repair, and overhaul (MRO) capabilities to support both military and commercial sectors.

Domestic Champions Lead Market Transformation Efforts

The South Korean aerospace and defense market is characterized by strong domestic conglomerates that have diversified their operations across multiple defense segments. These large industrial groups, or chaebols, have established themselves as primary contractors for major defense programs, while maintaining strategic partnerships with global defense companies. The market structure shows increasing consolidation, particularly evident in the aviation sector where Korean Air's acquisition of Asiana Airlines demonstrates the trend toward operational efficiency and market optimization.

The industry exhibits a balanced mix of specialized defense manufacturers and diversified industrial groups, with companies like Hanwha Group and Hyundai Heavy Industries maintaining significant defense divisions alongside their commercial operations. Market entry barriers remain high due to substantial technological requirements and strong government involvement in the defense procurement process. The emphasis on indigenous development capabilities has led to increased collaboration between domestic players, forming strategic alliances to compete more effectively in both local and international markets.

Innovation and Localization Drive Future Success

Success in the South Korean aerospace and defense market increasingly depends on companies' ability to develop indigenous technologies and participate in the government's defense modernization initiatives. Market incumbents are strengthening their positions through investments in next-generation technologies, particularly in areas like unmanned systems, artificial intelligence, and space capabilities. The ability to offer comprehensive solutions that align with the Defense Reform 2.0 initiative, while maintaining cost competitiveness and technological advancement, has become crucial for market success.

Companies seeking to gain market share must focus on developing specialized capabilities in emerging technology areas while fostering partnerships with established players. The regulatory environment strongly favors domestic production and technology transfer arrangements, making local manufacturing capabilities essential for long-term success. End-user concentration remains high with the government as the primary customer, necessitating strong relationships with defense procurement agencies and an understanding of national security priorities. The industry's future trajectory will be shaped by the ability to balance technological innovation with cost-effective solutions, while meeting increasingly stringent requirements for indigenous development and production.

South Korea Aerospace and Defense Market Leaders

-

Lockheed Martin Corporation

-

Korea Aerospace Industries, Ltd.

-

HD Hyundai Heavy Industries Co., Ltd.

-

Hanwha Corporation

-

The Boeing Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

South Korea Aerospace and Defense Market News

- April 2023: The Defense Acquisition Program Administration (DAPA) greenlit a program to construct a new air-to-air electronic warfare platform (AEWP). This initiative, slated to run from 2024 to 2032, is estimated to cost USD 1.41 billion.

- September 2022: KT SAT Corporation Ltd (KT SAT), a prominent player in South Korea's satellite services, partnered with Thales Alenia Space to deliver the KOREASAT 6A communications satellite. KOREASAT 6A, set to replace its predecessor, KOREASAT 6, will cater to both Fixed Satellite Service (FSS) and Broadcast Satellite Service (BSS) needs nationwide.

South Korea Aerospace and Defense Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Industry

- 5.1.1 Manufacturing, Design, and Engineering

- 5.1.2 Maintenance, Repair, and Overhaul

-

5.2 Type

- 5.2.1 Aerospace

- 5.2.1.1 Space

- 5.2.1.2 Civil Aviation

- 5.2.2 Defense

- 5.2.2.1 Army

- 5.2.2.2 Navy

- 5.2.2.3 Air Force

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Hanwha Corporation

- 6.1.2 DSME Co. Ltd

- 6.1.3 Korean Air Lines Co. Ltd

- 6.1.4 Korea Aerospace Research Institute (KARI)

- 6.1.5 Lockheed Martin Corporation

- 6.1.6 The Boeing Company

- 6.1.7 Korea Aerospace Industries Ltd

- 6.1.8 Victek Co. Ltd.

- 6.1.9 DXK Co. Ltd

- 6.1.10 Hyundai Motor Group

- 6.1.11 HD Hyundai Heavy Industries Co. Ltd

- 6.1.12 LIG Nex1 Co. Ltd

- 6.1.13 SNT Holdings Co. Ltd

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

South Korea Aerospace and Defense Industry Segmentation

The South Korean aerospace and defense market mainly comprises companies that manufacture products for military use. International collaborations, partnerships, weapon and defense asset developments, space programs, and other important factors impact the South Korean defense and aerospace market.

The South Korean aerospace and defense market is segmented by industry and type. By industry, it is segmented into manufacturing, design, and engineering and maintenance, repair, and overhaul. By type, it is segmented into aerospace and defense. For each segment, the market sizing and forecasts have been provided based on value (USD).

| Industry | Manufacturing, Design, and Engineering | ||

| Maintenance, Repair, and Overhaul | |||

| Type | Aerospace | Space | |

| Civil Aviation | |||

| Defense | Army | ||

| Navy | |||

| Air Force | |||

Need A Different Region or Segment?

Customize Now

South Korea Aerospace and Defense Market Research FAQs

How big is the South Korea Aerospace And Defense Market?

The South Korea Aerospace And Defense Market size is expected to reach USD 4.88 billion in 2025 and grow at a CAGR of 9.38% to reach USD 7.64 billion by 2030.

What is the current South Korea Aerospace And Defense Market size?

In 2025, the South Korea Aerospace And Defense Market size is expected to reach USD 4.88 billion.

Who are the key players in South Korea Aerospace And Defense Market?

Lockheed Martin Corporation, Korea Aerospace Industries, Ltd., HD Hyundai Heavy Industries Co., Ltd., Hanwha Corporation and The Boeing Company are the major companies operating in the South Korea Aerospace And Defense Market.

What years does this South Korea Aerospace And Defense Market cover, and what was the market size in 2024?

In 2024, the South Korea Aerospace And Defense Market size was estimated at USD 4.42 billion. The report covers the South Korea Aerospace And Defense Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the South Korea Aerospace And Defense Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

South Korea Aerospace And Defense Market Research

Mordor Intelligence provides comprehensive insights into the aerospace & defense sector. We leverage extensive expertise in aerospace engineering and aviation research. Our analysis covers the complete spectrum of aerospace manufacturing, including segments such as civil aviation, military aircraft, and commercial aircraft. The report examines crucial developments in defense technology, aerospace components, and aircraft systems. Additionally, it analyzes trends in aviation maintenance and aerospace services.

Stakeholders gain valuable insights through our detailed examination of military equipment, defense systems, and space industry developments. The report, available as an easy-to-download PDF, provides an in-depth analysis of satellite systems, missile systems, and defense electronics. Our research encompasses military aviation, commercial aerospace, and space systems, offering strategic insights into aircraft parts manufacturing and defense infrastructure. The comprehensive coverage extends to military aerospace operations, defense equipment, and emerging trends in aerospace technology. This makes it an essential resource for industry decision-makers.