Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 12 Million |

| Market Size (2030) | USD 16.36 Million |

| Growth Rate (2025 - 2030) | 6.40% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Fertilizer Market Analysis by Mordor Intelligence

The Southeast Asia fertilizer market size is estimated at USD 12 million in 2025 and is projected to reach USD 16.36 million by 2030, growing at a 6.4% CAGR from 2025 to 2030. The region’s growth is anchored in public subsidy programs that lower input costs, a rising shift toward precision farming, and continuing investment in specialty nutrient technologies. Subsidized allocations totaling IDR 33.78 trillion (approximately USD 2.19 billion) in Indonesia alone demonstrate the government's commitment to fertilizer affordability, specifically designated for the 2024 budget year. Capacity expansions by domestic producers, coupled with field trials demonstrating double-digit efficiency gains from controlled-release formulations, are further widening adoption among rice, palm oil, and high-value horticulture growers. Meanwhile, digital agriculture tools that match nutrient dosing to real-time soil data are improving returns on investment and encouraging demand for premium blends compatible with sensor-guided application systems. Thailand's implementation of Variable Rate Technology for oil palm fertilization and Indonesia's development of the world's first hybrid green ammonia project, scheduled for 2024, signal a shift in the market toward sustainable, technology-driven solutions.

Key Report Takeaways

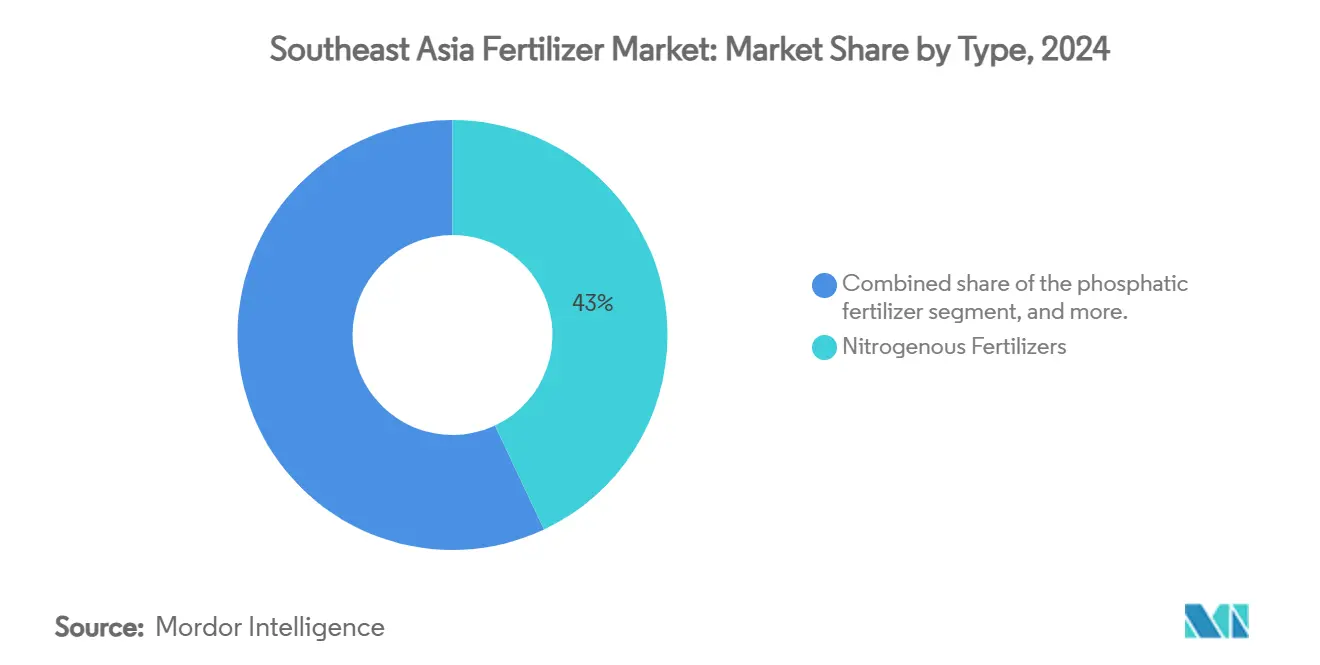

- By type, nitrogenous fertilizers captured 43% of the Southeast Asia fertilizer market share in 2024. Micronutrients are projected to post a 9.2% CAGR between 2025 and 2030, the fastest among all product categories.

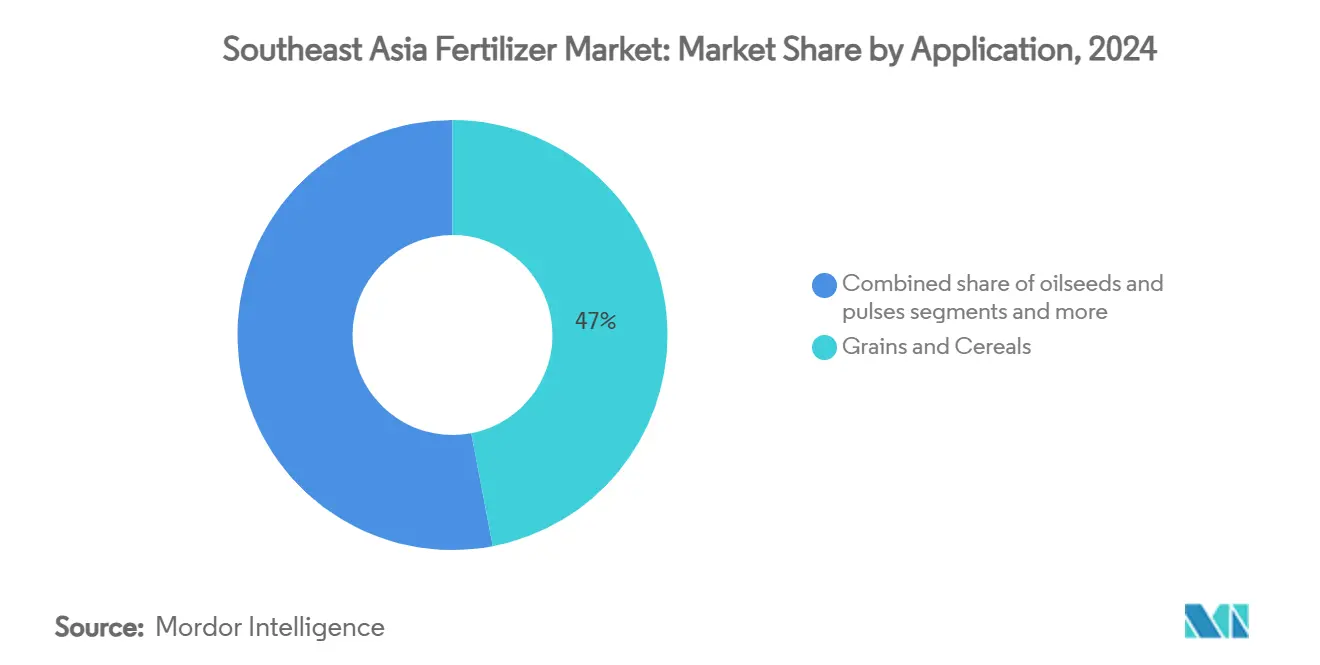

- By application, grains and cereals commanded 47% of the Southeast Asia fertilizer market size in 2024. Fruits and vegetables are forecast to expand at an 8.4% CAGR through 2030, outpacing every other crop segment.

- By geography, Indonesia captured 48.7% revenue share of the market in 2024, and Vietnam is projected to expand at an 8.4% CAGR to 2030.

Southeast Asia Fertilizer Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread adoption of precision-farming tools | +1.2% | Indonesia, Thailand, and Malaysia | Medium term (2-4 years) |

| Surging demand for enhanced-efficiency fertilizers | +0.9% | Global, with concentration in Vietnam and Philippines | Short term (≤ 2 years) |

| Government nutrient-management subsidy programs | +1.5% | Indonesia, Thailand, Malaysia, and Philippines | Short term (≤ 2 years) |

| Expansion of controlled-release and specialty blends | +0.8% | Malaysia, Indonesia, and Thailand | Medium term (2-4 years) |

| Digital twin modeling for field-specific fertilizer dosing | +0.6% | Thailand, Malaysia, and Vietnam | Long term (≥ 4 years) |

| Carbon-credit incentives for low-emission fertilizers | +0.4% | Indonesia, Malaysia, and Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Widespread Adoption of Precision-Farming Tools

Satellite imagery, soil sensors, and variable-rate applicators are transforming nutrient management across the Southeast Asia fertilizer market. Thailand’s Agriculture and Cooperatives Strategy offers tax relief for smart farming hardware, accelerating uptake of GPS-guided spreaders that cut nitrogen losses by up to 15%[1]Source: German-Thai Chamber of Commerce, “The Transition: Composing a Smart Farm,” gtcc.or.th. Malaysian oil-palm estates now run trials with drone-based mapping that tailors potassium inputs to canopy vigor, while Indonesian cooperatives deploy AI soil diagnostics that recommend field-specific urea rates. As growers verify savings in both cost and labor, demand for granular formulations compatible with precision machinery is rising. This technological shift drives demand for specialized fertilizer formulations compatible with precision application equipment, creating opportunities for enhanced-efficiency products.

Surging Demand for Enhanced-Efficiency Fertilizers

Controlled-release urea use in Vietnam expanded 25% in 2024, reflecting a regional pivot toward products that curb volatilization losses in monsoon climates. Indonesian universities report rice-husk-biochar coatings that extend nitrogen release over 60 days, lifting uptake efficiency by 20%. Malaysia's palm oil sector increasingly adopts slow-release formulations to address labor shortages and reduce application frequency. Palm growers in Malaysia favor polymer-coated blends that slash application frequency, easing labor constraints. Rising fertilizer costs, with urea prices reaching USD 430 per metric ton in February 2025, further accelerate the adoption of efficiency-enhancing products that deliver superior nutrient utilization rates.

Government Nutrient-Management Subsidy Programs

Public funding remains the strongest growth lever for the Southeast Asia fertilizer market. Indonesian state-owned PT Pupuk Indonesia distributed 7.25 million metric tons of subsidized fertilizer in 2024, surpassing targets. Thailand continues to reimburse smallholders for nutrient costs, and Vietnam exempts import tariffs on phosphate-based products under ASEAN-Korea agreements. However, subsidy coverage gaps persist, with South Sulawesi studies indicating government allocations meet only 37% of actual farmer requirements in 2024, creating market opportunities for private sector solutions.

Expansion of Controlled-Release and Specialty Blends

Specialty formulations that align macro- and micronutrients to crop phenology are gaining share. Malaysian producers market oil-palm blends with tailored boron and magnesium ratios, while Indonesian research institutes validate biochar-coated NPK pellets that outperform conventional inputs on acidic soils. Thailand’s sugar cane growers begin adopting sulfur-coated urea to manage nitrogen leaching amid erratic rainfall. These advances create a premium segment with higher margins and sustained throughput for domestic manufacturers. Vietnam's export-oriented agriculture sector adopts specialty blends tailored for high-value crops, supporting the country's agricultural diversification strategy. The Philippines promotes organic-inorganic fertilizer combinations through the National Organic Agriculture Program, creating demand for hybrid formulations that balance productivity with sustainability objectives.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited rural credit access | -0.8% | The Philippines, Vietnam, and Indonesia rural areas | Short term (≤ 2 years) |

| Climate-induced application uncertainties | -0.6% | Vietnam, Thailand, and the Philippines | Medium term (2-4 years) |

| Volatility in ammonia and potash feedstock prices | -1.1% | Global, particularly import-dependent countries | Short term (≤ 2 years) |

| Lagging logistics infrastructure in secondary cities | -0.5% | Indonesia, the Philippines, and Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Rural Credit Access

Smallholders in the Philippines pay annual interest rates topping 20% to informal lenders, constraining timely fertilizer purchases. Vietnamese rice farmers often lack collateral to meet banking requirements, while many Indonesian districts remain underserved by micro-finance branches. Smallholders in Malaysia's palm oil industry encounter comparable challenges, especially regarding investments in specialty fertilizers that demand higher initial expenditures. The International Fertilizer Development Center notes that credit access improvements could increase fertilizer consumption by 16% annually, as demonstrated in Indonesia's targeted subsidy programs

Climate-Induced Application Uncertainty

El Niño events and erratic monsoons complicate nutrient scheduling across the Southeast Asia fertilizer market. Thai growers witnessed rainfall shifts that forced mid-season changes in urea plans during 2024[2]Source: Asian Development Bank, “The Russian Invasion of Ukraine, Fertilizer Prices, and Food Security,” adb.org. Vietnamese deltas alternate between floods and droughts that wash away or lock up applied nutrients, while typhoon damage in the Philippines often wipes out recently fertilized acreage. These uncertainties shave returns on input investment and delay adopter confidence in premium products. Malaysia's palm oil sector adapts to changing precipitation patterns that influence fertilizer leaching rates and effectiveness. Climate change impacts are projected to reduce rice yields by 0.45% to 1.33% when combined with fertilizer price volatility, according to Asian Development Bank analysis.

Segment Analysis

By Type: Nitrogenous Fertilizers Lead Market Share

Nitrogenous products, anchored by urea and ammonium sulfate, held a 43% share of the Southeast Asia fertilizer market in 2024. Domestic champion PT Pupuk Indonesia alone maintains an annual urea capacity of 9.4 million metric tons, ensuring a reliable supply for national rice targets[3]Source: Pupuk Indonesia, “Company Profile and Production Capacity,” pupuk-indonesia.com. Imports still supplement Vietnamese and Thai demand, especially during peak paddy seasons. Potash fertilizers are subject to sourcing risks, however, the planned 1.2 million metric tons MOP facility in Thailand is expected to reduce dependency by 2028. Controlled-release coatings across each nutrient class are projected to gain market share because they match the incremental dosing preferred in precision platforms, thereby boosting nutrient-use efficiency under heavy rainfall regimes.

The Southeast Asia fertilizer market size attributed to micronutrient formulations is set to increase rapidly, with a 9.2% CAGR to 2030, reflecting growers’ push to correct widespread zinc and boron deficiencies. Specialty suppliers are responding with chelated blends that resist tropical soil fixation and are compatible with precision spreader formats. Secondary macronutrients, particularly sulfur and magnesium, rise in relevance as palm oil estates pursue higher oil-to-bunch ratios.

Note: Segment shares of all individual segments available upon report purchase

By Application: Grains and Cereals Dominate Usage

Grains and cereals accounted for 47% of the Southeast Asia fertilizer market size in 2024, reflecting rice’s strategic role in national food security. Indonesia’s plan to develop an additional 3 million hectares of rice land will require an extra 500,000 metric tons of urea and NPK blends each year once full planting begins. Thai rice cooperatives adopt site-specific nitrogen management to stabilize yields amid climate swings, reinforcing baseline demand.

Fruits and vegetables post the fastest trajectory at 8.4% CAGR through 2030 as export chains expand. Capsicum, durian, and dragon-fruit orchards demand soluble nutrient programs that support high-density planting. Commercial crops such as palm oil sustain steady bulk NPK uptake, while oilseeds and pulses usage gains momentum under crop-rotation policies aimed at soil health. Urban vertical farms in Kuala Lumpur and Bangkok anchor a niche segment for high-purity soluble fertilizers, adding diversified revenue to the Southeast Asia fertilizer market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Indonesia is the largest consuming nation, capturing 48.7% revenue share of the market in 2024, energized by subsidized distribution channels and strong domestic production. Government spending of IDR 33.78 trillion (USD 2.19 billion) in 2024 financed 9.55 million metric tons of discounted fertilizer that reached 17 million farmers. The upcoming hybrid green-ammonia plant positions Indonesia as an early mover in low-carbon nitrogen manufacturing, aligning supply resilience with environmental targets.

Vietnam is projected to expand at an 8.4% CAGR to 2030. It sits at the center of regional trade flows. Export volumes topped 1.29 million metric tons in the first nine months of 2024, even after the government introduced a 5% export tax on nitrogen products to safeguard local supply. Domestic fertilizer plants feed national rice priorities, while import terminals secure phosphate and potash from diverse origins. Malaysia’s palm-oil-fueled demand, the Philippines’ 66% import dependency, and emerging adoption in Myanmar and Cambodia add depth and opportunity across the Southeast Asia fertilizer market.

Thailand follows with roughly 4 million metric tons of fertilizer use annually. Policies embedded in its twenty-year agricultural strategy incentivize precision agriculture through machinery grants and training programs. A planned potash mine in Chaiyaphum province should cut import reliance once operational in 2028, smoothing potash price swings and supporting balanced fertilization for sugar cane and cassava.

Competitive Landscape

State ownership and multinational reach shape a moderately concentrated playing field. PPT Pupuk Indonesia (Persero) controls integrated production from ammonia to NPK and leverages proprietary distribution kiosks for last-mile delivery. Mitsui & Co., Ltd. (Thai Central Chemical PCL) and Vietnam’s Song Gianh Corporation offer localized blends that cater to various soil types and staple crops. Yara International ASA, Nutrien Ltd., and ICL Group Ltd. (Israel Corporation) compete through specialty grades and agronomic advisory services that mesh with precision platforms, even as they source bulk nutrients from global hubs.

Strategic partnerships focus on securing raw materials and achieving decarbonization. Pupuk Indonesia’s alliance with Itochu on green ammonia and Thai developers’ stake in domestic potash mining illustrate vertical integration moves designed to lock in cost advantages. Digital agronomy solutions packaged with fertilizer sales are proliferating. Yara’s crop-nutrition platforms and ICL Group Ltd.'s (Israel Corporation) soil-analysis apps help growers maximize returns and demonstrate environmental compliance. Specialty micronutrient firms target high-value horticulture markets where smaller volumes carry attractive margins, prompting potential consolidation as demand scales.

Regional players also explore carbon-credit monetization. Pilot projects in Malaysia’s palm sector test certified low-emission nitrogen blends that could generate future revenue streams under voluntary offset schemes. As governments refine sustainability frameworks, suppliers with proven emissions reductions, traceable sourcing, and digital advisory capabilities are poised to capture share within the Southeast Asia fertilizer market.

Southeast Asia Fertilizer Industry Leaders

Song Gianh Corporation

Mitsui & Co., Ltd. (Thai Central Chemical PCL)

PT Petrokimia Gresik

Yara International ASA

PT Pupuk Indonesia (Persero)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: ASEAN Potash Mining Public Company Limited confirmed construction of a 1.2 million metric tons MOP plant in Chaiyaphum, Thailand, with start-up slated for 2028.

- November 2024: Petrokimia Gresik, an agroindustry solutions company, outlined a 2024-2030 energy transition roadmap at COP29, pledging lower-carbon production pathways. This helps towards sustainable fertilizer manufacturing, aligning with environmental goals.

- August 2024: PT Pupuk Indonesia, Itochu, and Toyo Engineering signed a joint development agreement for the world’s first hybrid green ammonia project in Aceh, with commercial launch targeted for 2027.

Southeast Asia Fertilizer Market Report Scope

Fertilizer is any solid, liquid, or gaseous substance containing one or more plant nutrients in a known amount, which is applied to soil, directly on plants, or added aqueous solutions (as in fertigation) to maintain soil fertility, improve crop development, yield, and/or crop quality. The Southeast Asia Fertilizer Market has been segmented by Type (Nitrogenous Fertilizers, Phosphatic Fertilizers, Potassic Fertilizers, Secondary Macronutrients, and Micronutrients), Application (Grains and Cereals, Oilseeds and Pulses, Commercial Crops, Fruits and Vegetables, and Other Applications), and Geography (Malaysia, Thailand, Vietnam, Philippines, Indonesia, and Rest of Southeast Asia). The Report Offers the Market Sizes and Forecasts in Value (USD) for all the Above Segments.

By Type

| Nitrogenous Fertilizers | Urea |

| Calcium Ammonium Nitrate | |

| Ammonia | |

| Ammonium Nitrate | |

| Ammonium Sulfate | |

| Other Nitrogenous Fertilizers | |

| Phosphatic Fertilizers | Mono-ammonium Phosphate |

| Di-ammonium Phosphate | |

| Triple Superphosphate | |

| Other Phosphatic Fertilizers | |

| Potash Fertilizers | Muriate of Potash |

| Other Potash Fertilizers | |

| Secondary Macronutrients | |

| Micronutrients |

By Application

| Grains and Cereals |

| Oilseeds and Pulses |

| Commercial Crops |

| Fruits and Vegetables |

| Other Applications |

By Geography

| Malaysia |

| Thailand |

| Vietnam |

| Philippines |

| Indonesia |

| Rest of Southeast Asia |

| By Type | Nitrogenous Fertilizers | Urea |

| Calcium Ammonium Nitrate | ||

| Ammonia | ||

| Ammonium Nitrate | ||

| Ammonium Sulfate | ||

| Other Nitrogenous Fertilizers | ||

| Phosphatic Fertilizers | Mono-ammonium Phosphate | |

| Di-ammonium Phosphate | ||

| Triple Superphosphate | ||

| Other Phosphatic Fertilizers | ||

| Potash Fertilizers | Muriate of Potash | |

| Other Potash Fertilizers | ||

| Secondary Macronutrients | ||

| Micronutrients | ||

| By Application | Grains and Cereals | |

| Oilseeds and Pulses | ||

| Commercial Crops | ||

| Fruits and Vegetables | ||

| Other Applications | ||

| By Geography | Malaysia | |

| Thailand | ||

| Vietnam | ||

| Philippines | ||

| Indonesia | ||

| Rest of Southeast Asia | ||

Key Questions Answered in the Report

How large is the Southeast Asia fertilizers market in 2025?

The market is valued at USD 12 million in 2025 and is projected to reach USD 16.36 million by 2030.

Which nutrient type leads regional demand?

Nitrogenous fertilizers hold 43% of the 2024 market, reflecting rice-driven nitrogen requirements.

What segment is growing fastest by application?

Fruits and vegetables are anticipated to post an 8.4% CAGR during 2025-2030 due to export-oriented horticulture.

How will Thailand reduce potash import dependence?

A 1.2 million-ton MOP facility scheduled for 2028 will supply domestic and regional users.

What technology trend is reshaping fertilizer application?

Digital twin modeling allows real-time nutrient dosing simulations that can cut input costs by double digits.

Why are carbon credits relevant to fertilizer suppliers?

Indonesia and Malaysia are developing schemes that reward low-emission fertilizers, opening new revenue streams.

Page last updated on: