Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

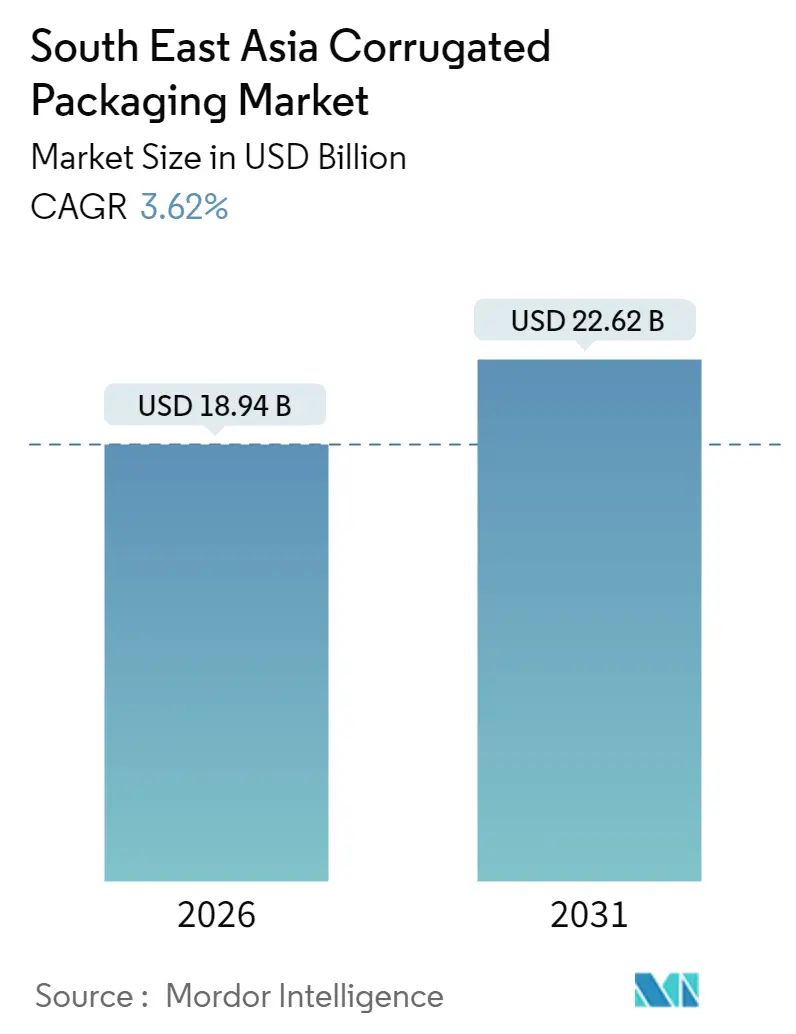

| Market Size (2026) | USD 18.94 Billion |

| Market Size (2031) | USD 22.62 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South East Asia Corrugated Packaging Market Analysis by Mordor Intelligence

The South-East Asia corrugated packaging market is expected to grow from USD 18.28 billion in 2025 to USD 18.94 billion in 2026 and is forecast to reach USD 22.62 billion by 2031 at 3.62% CAGR over 2026-2031. Escalating parcel volumes from e-commerce platforms, the rise of food-delivery ecosystems, and regulatory pressure on single-use plastics continue to steer procurement budgets toward fiber-based formats. Indonesia’s integrated supply chains, Vietnam’s export-oriented manufacturing base, and Thailand’s food-processing clusters drive geographic momentum, while investments in high-speed digital flexo lines compress lead times that once hampered regional converters. Material cost volatility linked to kraft liner and recycled OCC supplies remains the primary margin headwind, yet plantation-based fast-growing fiber grades and AI-enabled design software offset part of the squeeze through lower input costs and higher yield efficiencies. Competition centers on technology adoption rather than price warfare as converters chase long-term contracts with food-delivery platforms and 3PL operators.

Key Report Takeaways

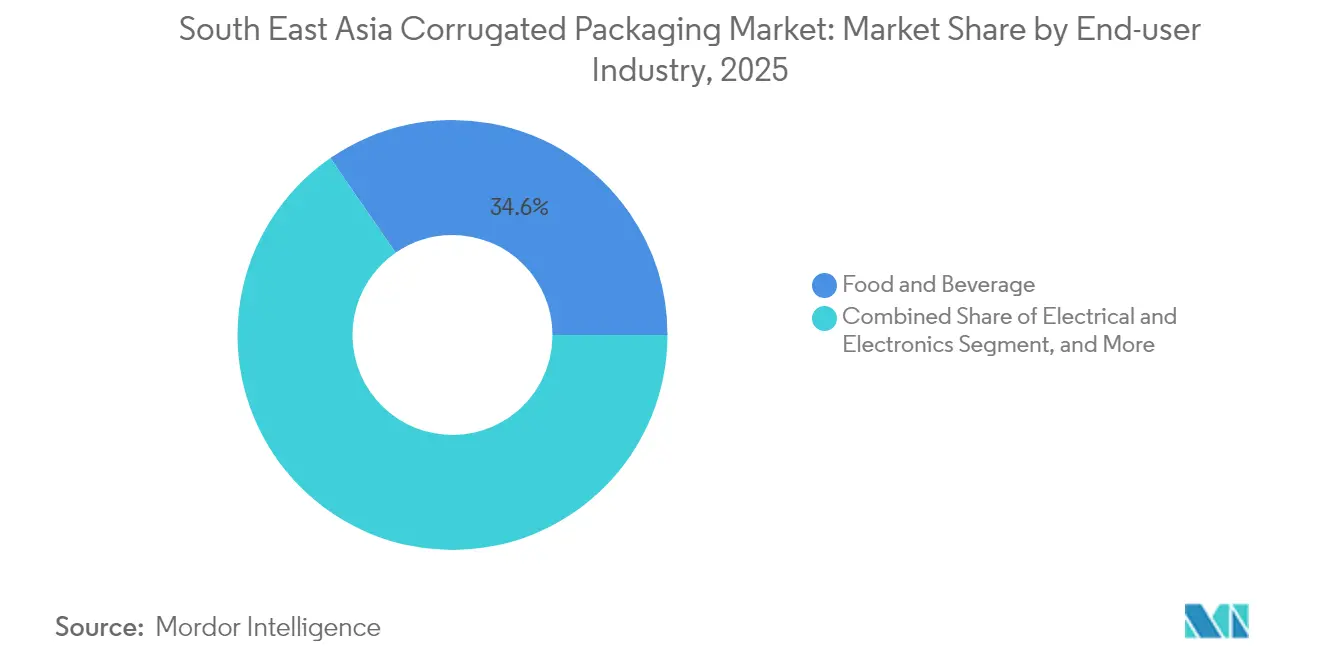

- By end-user industry, food and beverage led with 34.62% revenue share of the South-East Asia corrugated packaging market in 2025; e-commerce packaging is projected to advance at a 5.17% CAGR through 2031.

- By board type, single wall accounted for 38.64% share of the South-East Asia corrugated packaging market size in 2025, while triple wall is set to grow at 4.36% CAGR to 2031.

- By flute type, C-flute held 32.31% of the South-East Asia corrugated packaging market share in 2025; F-flute and microflute variants are forecast to expand at 4.83% CAGR through 2031.

- By printing technology, flexographic printing captured 28.34% share of the South-East Asia corrugated packaging market size in 2025; digital printing is expected to post a 5.75% CAGR between 2026-2031.

- By Indonesia, the largest country market, commanded 21.55% of the South-East Asia corrugated packaging market share in 2025, whereas Vietnam is projected to log the fastest 5.42% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South East Asia Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive B2C e-commerce parcel volumes | +1.2% | Indonesia, Vietnam, Thailand | Medium term (2-4 years) |

| Food-delivery boom | +0.8% | Vietnam, Indonesia | Short term (≤ 2 years) |

| Single-use-plastic phase-outs | +0.6% | Indonesia, Vietnam, Thailand | Long term (≥ 4 years) |

| High-speed digital flexo lines | +0.4% | Malaysia, Thailand | Medium term (2-4 years) |

| AI-enabled box-design software | +0.3% | Regional technology centers | Long term (≥ 4 years) |

| Plantation-based fast-growing fiber grades | +0.5% | Indonesia, Malaysia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive B2C E-commerce Parcel Volumes Demanding Right-Sized Shipping Boxes

E-commerce logistics transformation drives corrugated demand through dimensional weight optimization and standardized packaging requirements. PT Pos Indonesia processed over 2.8 billion parcels in 2024, representing 15% year-over-year growth, with corrugated packaging comprising approximately 65% of total parcel volume. The state postal service has invested in automated sorting facilities across Jakarta, Surabaya, and Medan, creating standardized packaging specifications that favor corrugated solutions. Cross-border e-commerce through platforms like Shopee and Lazada generates varied packaging requirements, with 3PLs standardizing box sizes to optimize warehouse space and shipping costs. Regional infrastructure challenges including rural delivery networks, tropical climate conditions, and extended transit times increase preference for robust corrugated grades and moisture-resistant treatments that maintain structural integrity during logistics cycles.

Shopee Indonesia implemented a packaging standardization program in 2024, reducing box size variations from 47 to 12 standard dimensions across its fulfillment network. This initiative resulted in 23% reduction in packaging material usage and 18% improvement in truck loading efficiency, demonstrating how e-commerce platforms drive corrugated demand through operational optimization rather than pure volume growth.

Food-Delivery Boom Accelerating Need for Leak-Resistant Corrugated Meal Boxes

Vietnam's food delivery market expansion to USD 1.8 billion in 2024 with 26% growth exemplifies regional demand acceleration for specialized food packaging solutions, with corrugated meal boxes representing approximately 40% of packaging volume by weight. Grab Holdings reported 2.4 billion food delivery orders across Southeast Asia in 2024, with Vietnam and Indonesia accounting for 67% of total volume, creating massive demand for standardized corrugated meal containers. The shift from heavy discounting to sustainable growth models among major platforms emphasizes operational efficiency initiatives, creating opportunities for corrugated suppliers offering moisture-resistant treatments, grease-proof coatings, and stackable designs that maintain food safety during extended delivery cycles.

Gojek partnered with Indonesian corrugated manufacturer PT Fajar Surya Wisesa in 2024 to develop biodegradable meal boxes with enhanced grease resistance. The collaboration resulted in 30% reduction in packaging-related customer complaints and 15% improvement in food temperature retention during delivery, while reducing material costs by 8% through optimized box design and local sourcing

Mandated Phase-Out of Single-Use Plastics in Indonesia, Vietnam and Thailand

Thailand's Ministry of Natural Resources and Environment implemented comprehensive plastic waste import restrictions in January 2025, banning 432 categories of plastic waste imports and creating immediate substitution demand for paper-based packaging alternatives. Vietnam's Ministry of Natural Resources and Environment announced the complete phase-out of plastic scrap imports by December 2025, with interim restrictions reducing import volumes by 78% in 2024 compared to 2023 levels. Indonesia's Ministry of Environment and Forestry delayed stricter recovered paper import restrictions until 2026, providing temporary supply chain stability while domestic recycling infrastructure develops capacity to process 2.3 million tonnes annually by 2030.

Asia Pulp and Paper Group invested SGD 450 million (USD 333 million) in 2024 to expand its Foopak Bio Natura product line, developing corrugated packaging solutions specifically designed to replace single-use plastic containers in food service applications. The investment includes new coating technologies that provide moisture and grease resistance comparable to plastic alternatives while maintaining recyclability standards required by regional environmental regulations

Installation of High-Speed Digital Flexo Lines Slashing Lead-Times for SMEs

WestRock Company completed installation of three high-speed digital flexographic lines across its Southeast Asian facilities in 2024, including new equipment at its Malaysian and Thai operations capable of producing 350 meters per minute with CMYK+spot color capabilities. The digital preprint technology eliminates plate requirements and supports minimum runs of 500 linear meters, enabling fast turnaround for small and medium enterprises that previously faced 2-3 week lead times with conventional flexographic processes. Bobst Group SA reported 40% increase in digital corrugated equipment sales across ASEAN markets in 2024, with installations concentrated in Thailand, Malaysia, and Vietnam where SME manufacturers seek competitive advantages through shorter lead times.

Thai Containers Group invested THB 280 million (USD 7.8 million) in 2024 to install Bobst's MASTER DM5 digital corrugated line at its Rayong facility. The investment reduced average order lead times from 14 days to 3 days for runs under 10,000 square meters, enabling the company to capture 35% more orders from SME customers in food and beverage sectors who require rapid prototyping and short-run customization

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Kraft liner and recycled OCC price volatility | -0.9% | Regional manufacturing centers | Short term (≤ 2 years) |

| Inferior humidity resistance during monsoons | -0.5% | Tropical climate zones across SEA | Medium term (2-4 years) |

| Fragmented panel-board logistics | -0.4% | Indonesia, Philippines archipelago | Medium term (2-4 years) |

| Skilled-operator shortage | -0.3% | Technology adoption centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Kraft Liner and Recycled OCC Price Volatility Squeezing Converter Margins

Raw material cost pressures intensified in early 2025 with kraft paper mills experiencing production disruptions and price volatility affecting regional supply chains. The Indonesian Pulp and Paper Association reported average kraft liner prices increased 18% in Q4 2024 compared to Q3, while recycled OCC prices fluctuated between USD 180-240 per tonne, creating margin compression for downstream converters. PT Fajar Surya Wisesa reported EBITDA margin compression of 2.3 percentage points in 2024 due to raw material cost volatility, despite implementing dynamic pricing mechanisms for major customers.

The volatility stems from supply-demand imbalances as regional demand growth of 4.2% annually outpaces capacity additions of 2.8%, creating structural tightness that amplifies price swings during supply disruptions. Converter profitability faces additional pressure from limited pricing power with major food delivery platforms and e-commerce operators who maintain annual contracts with fixed pricing terms.

Inferior Humidity Resistance During Monsoon Logistics Cycles

Tropical climate conditions across Southeast Asia create moisture-related challenges for corrugated packaging during extended container transit and storage periods, with relative humidity levels frequently exceeding 85% during monsoon seasons from May through October. The ASEAN Logistics Association reported 12% increase in packaging-related damage claims during 2024 monsoon season, with corrugated packaging failures accounting for 34% of total claims by value. Container shipments experience critical moisture exposure during three phases: inland transport to ports, sea voyage temperature fluctuations, and destination port storage, with recorded humidity spikes reaching 96% during land transport phases.

Samsung Electronics Vietnam reported 15% increase in packaging-related product damage during 2024 monsoon season, primarily affecting corrugated packaging used for consumer electronics exports. The company implemented enhanced moisture barrier treatments and modified box designs, reducing damage rates to 3.2% while increasing packaging costs by 8% through specialized coatings and desiccant integration.

Segment Analysis

By End-User Industry: Food Delivery Drives Digital Innovation

Food and beverage applications commanded 34.62% of the South-East Asia corrugated packaging market share in 2025, benefiting from the region's expanding food service sector and cold chain infrastructure development. The South-East Asia corrugated packaging market size for food and beverage applications reached USD 6.33 billion in 2025, with growth accelerating in Vietnam and Indonesia where food delivery platforms generate consistent demand for specialized packaging solutions. E-commerce packaging emerges as the fastest-growing segment with 5.17% CAGR through 2031, driven by platform consolidation and standardization requirements from major operators including Shopee, Lazada, and regional postal services.

Nestlé Indonesia implemented new corrugated packaging specifications in 2024 for its instant noodle products, reducing packaging material usage by 12% while improving shelf stability through enhanced moisture barrier properties. The optimization resulted in annual cost savings of USD 3.2 million while maintaining product protection standards across Indonesia's diverse climate zones. Electrical and electronics packaging serves regional manufacturing hubs, particularly in Malaysia and Thailand, where export-oriented production requires robust corrugated solutions for component protection during international shipping.

Healthcare and pharmaceutical applications gain momentum from regulatory compliance requirements and cold chain integrity demands, with specialized corrugated designs incorporating antimicrobial coatings and temperature-resistant properties. Cosmetics and personal care packaging reflects rising disposable incomes and urbanization trends across the region, while automotive and industrial segments benefit from manufacturing diversification and supply chain regionalization initiatives. The convergence of food delivery growth and e-commerce expansion creates cross-segment opportunities for converters offering multi-application solutions, with digital printing technologies enabling rapid customization across diverse end-user requirements.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Board Type: Triple Wall Gains Heavy-Duty Traction

Single wall corrugated boards maintained 38.64% of the South-East Asia corrugated packaging market share in 2025, reflecting cost-effectiveness for medium-duty shipping applications and food delivery packaging where weight optimization remains critical for last-mile logistics efficiency. The South-East Asia corrugated packaging market size for single wall applications reached USD 7.06 billion in 2025, with food delivery and e-commerce segments driving consistent demand. Triple wall configurations experience the fastest growth at 4.36% CAGR, driven by heavy-duty industrial applications and export packaging requirements where enhanced crush resistance and stackability provide competitive advantages.

Double wall boards serve intermediate applications including electronics packaging and retail displays, while single face corrugated finds niche applications in protective wrapping and void fill solutions. Advanced corrugator installations enable regional converters to produce consistent triple wall products with precise flute formation and adhesive application. Thai Containers Group's investment in high-speed corrugating equipment demonstrates how manufacturers upgrade capabilities to serve demanding export markets requiring superior packaging performance.

Mitsubishi Motors Vietnam upgraded its export packaging specifications in 2024, transitioning from double wall to triple wall corrugated containers for automotive parts shipments to reduce damage rates during ocean transport. The change increased packaging costs by 23% but reduced product damage claims by 67%, resulting in net savings of USD 1.8 million annually. The trend toward triple wall adoption reflects increasing quality requirements from multinational manufacturers establishing regional production facilities, creating opportunities for converters with advanced manufacturing capabilities.

By Flute Type: Microflutes Enable Premium Applications

C-flute configurations held 32.31% of the South-East Asia corrugated packaging market share in 2025, providing optimal balance between strength and cushioning properties for general packaging applications across food delivery and e-commerce segments. The South-East Asia corrugated packaging market size for C-flute applications reached USD 5.91 billion in 2025, with broad adoption across multiple end-user industries. F-flute and microflute variants achieve the highest growth rate at 4.83% CAGR, driven by premium packaging requirements and print quality demands from consumer goods manufacturers seeking enhanced graphics capabilities.

A-flute maintains strong performance in heavy-duty applications where maximum cushioning properties are required, while B-flute serves space-constrained applications including retail displays and compact shipping boxes. The microflute trend reflects regional manufacturing evolution toward higher value-added applications, with converters investing in precision corrugating equipment capable of producing consistent fine flute profiles. Digital printing compatibility becomes increasingly important for microflute applications, as enhanced print quality capabilities enable converters to compete for premium packaging contracts with multinational consumer goods companies.

Unilever Indonesia transitioned 40% of its personal care product packaging to E-flute corrugated containers in 2024, achieving 25% improvement in print quality while reducing packaging thickness by 15%. The change enabled better shelf presentation and reduced shipping volumes, resulting in 8% reduction in total packaging costs despite 12% higher material costs per unit. The microflute adoption trend demonstrates how consumer goods manufacturers balance performance requirements with sustainability objectives, creating opportunities for converters with specialized manufacturing capabilities.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Printing Technology: Digital Disrupts Traditional Flexo

Flexographic printing maintained 28.34% of the South-East Asia corrugated packaging market share in 2025, leveraging established infrastructure and cost advantages for high-volume production runs across food and beverage packaging applications. The South-East Asia corrugated packaging market size for flexographic printing reached USD 5.18 billion in 2025, with major converters maintaining substantial flexographic capacity for high-volume contracts. Digital printing technologies achieve the fastest growth at 5.75% CAGR, driven by demand for shorter runs, rapid turnaround times, and late-stage customization capabilities that traditional flexographic processes cannot economically support.

Litho-lamination serves premium applications requiring superior graphics quality, while offset printing maintains niche applications in specialized packaging segments. The digital transformation accelerates as converters seek competitive differentiation through customization capabilities and reduced lead times for small and medium enterprise customers. Water-based ink adoption across all printing technologies aligns with regional sustainability initiatives and regulatory compliance requirements, while UV-curable inks gain traction for applications requiring enhanced durability and chemical resistance.

Harta Packaging Industries invested MYR 15 million (USD 3.4 million) in 2024 to install digital printing capabilities at its Selangor facility, enabling minimum run sizes of 500 units compared to 5,000 units for conventional flexographic processes. The investment captured 28% more orders from SME customers requiring customized packaging solutions, increasing revenue per customer by 35%. The digital printing adoption trend demonstrates how technology investments create competitive differentiation in a market traditionally dominated by scale economies and established customer relationships.

Geography Analysis

Indonesia commanded 21.55% of the South-East Asia corrugated packaging market share in 2025, leveraging its position as Southeast Asia's largest economy and consumer market, with established manufacturing infrastructure supporting both domestic consumption and export-oriented production. The South-East Asia corrugated packaging market size in Indonesia reached USD 3.94 billion in 2025, with integrated pulp and paper operations providing competitive advantages through vertical integration and supply chain proximity. Vietnam emerges as the fastest-growing market with 5.42% CAGR through 2031, driven by rapid food delivery expansion, manufacturing diversification, and foreign direct investment in packaging infrastructure.

Thailand maintains strong performance through its established food processing industry and strategic location for regional distribution, while Malaysia benefits from integrated pulp and paper operations and advanced manufacturing capabilities. Vietnam's exceptional growth trajectory stems from its food delivery market leadership with 26% growth in 2024, manufacturing diversification initiatives, and strategic positioning for regional supply chain integration. The Vietnam Paper Association reported total corrugated packaging production of 1.8 million tonnes in 2024, representing 15% increase from 2023 levels, with exports accounting for 35% of total production.

Vina Kraft Paper Company expanded its containerboard capacity by 400,000 tonnes in 2024 through a USD 180 million investment at its Dong Nai facility, targeting growing demand from food delivery and e-commerce sectors. The expansion includes advanced water treatment systems and energy recovery capabilities, reducing production costs by 12% while meeting international environmental standards. Philippines demonstrates steady growth supported by rising consumer spending and e-commerce adoption, though infrastructure constraints limit acceleration compared to regional peers. Singapore serves as a regional hub for premium packaging applications and technology adoption, with regulatory leadership in sustainability initiatives influencing broader regional trends.

Indonesia's dominant position with 21.55% market share in 2025 reflects its massive consumer base of over 270 million people and established manufacturing infrastructure, though growth moderates as the market matures and competition intensifies from regional peers. The country benefits from integrated pulp and paper operations including major investments by domestic players, with PT Indah Kiat reporting 2.1 million tonnes annual packaging capacity serving both domestic and export markets. The Indonesian Corrugated Packaging Association reported 8.2% growth in domestic consumption during 2024, driven primarily by food delivery and e-commerce applications in major urban centers including Jakarta, Surabaya, and Medan.

Thailand and Malaysia maintain steady performance through established food processing industries and advanced manufacturing capabilities, with Thailand's packaging market benefiting from tourism recovery and domestic consumption growth. The Thai Packaging Association reported 6.8% growth in corrugated packaging consumption during 2024, driven by food service recovery and expanding e-commerce applications. Malaysia's integrated pulp and paper sector provides competitive advantages through vertical integration, with major producers like Harta Packaging Industries achieving cost efficiencies through captive fiber supply and advanced manufacturing technologies.

The Rest of South-East Asia category includes emerging markets such as Cambodia and Laos, where infrastructure development and manufacturing investment create long-term growth opportunities. These markets typically lag regional leaders in technology adoption and manufacturing sophistication, though foreign direct investment creates pockets of advanced packaging capabilities serving export-oriented industries. Regional integration through ASEAN trade agreements facilitates cross-border supply chains, creating opportunities for converters with multinational operations and logistics capabilities.

Competitive Landscape

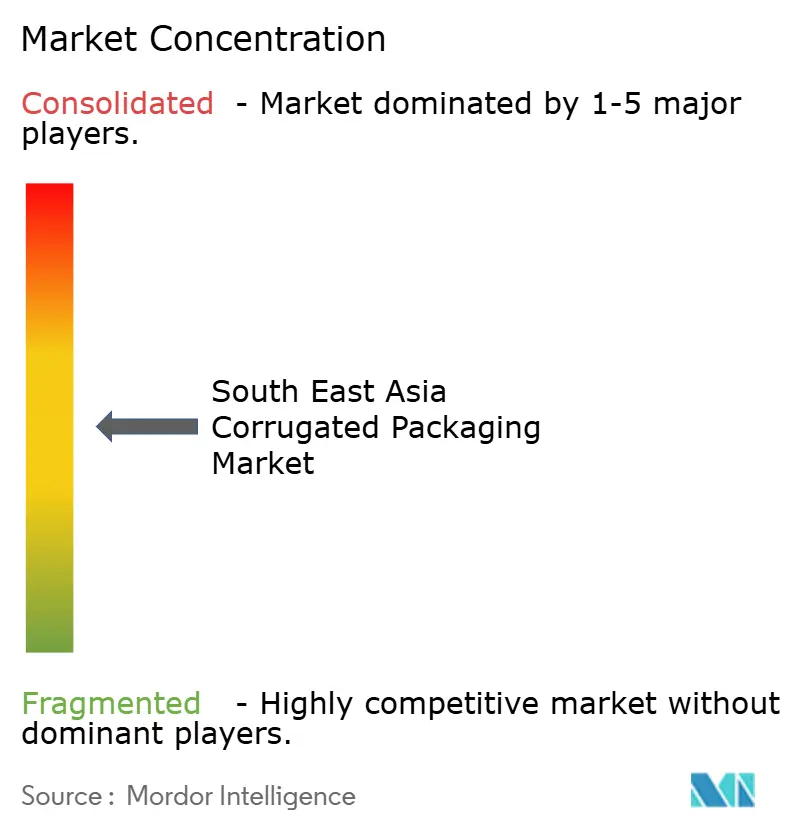

The South-East Asia corrugated packaging market exhibits moderate concentration with established regional players pursuing vertical integration and technology adoption strategies to defend market positions against global entrants. SCG Packaging's acquisition of 99.72% stake in PT Fajar Surya Wisesa for approximately IDR 9.98 trillion (USD 6.6 billion) exemplifies consolidation trends, creating integrated supply chains from pulp production through corrugated converting across Thailand, Vietnam, and Indonesia.[1]"Annual Report 2023," SCG Packaging Public Company Limited, scgpackaging.com The transaction strengthens SCG Packaging's vertical integration across Indonesia's packaging paper supply chain, adding 1.2 million tonnes annual containerboard capacity to serve growing regional demand.

International players including Rengo, Oji Holdings, and emerging global consolidators create competitive pressure through advanced technology and global customer relationships, though regional players maintain advantages through local market knowledge and supply chain proximity. Rengo Co., Ltd. announced plans to construct a new containerboard manufacturing facility in Vietnam with initial capacity of 600,000 tonnes annually, representing USD 450 million investment to serve growing Southeast Asian demand for corrugated packaging materials. The investment demonstrates how Japanese packaging manufacturers expand regional presence to serve multinational customers and capture growth opportunities in emerging markets.

Technology adoption becomes the primary competitive differentiator, with digital printing capabilities, AI-enabled design software, and Industry 4.0 automation creating sustainable advantages for forward-investing converters. WestRock Company installed three high-speed digital flexographic printing lines across Southeast Asian facilities, including new equipment at Malaysian and Thai operations capable of 350 meters per minute production speeds with enhanced color management capabilities.[2]"Q4 2024 Earnings Call Transcript," WestRock Company, westrock.com The investment demonstrates how global players leverage technology transfer to strengthen regional market positions and serve multinational customers with consistent quality standards.

White-space opportunities emerge in specialized applications including cold chain packaging, pharmaceutical compliance solutions, and premium consumer goods packaging where technical expertise and certification requirements create barriers to entry. Nine Dragons Paper Holdings Limited commenced operations at its new recycled containerboard mill in East Java, Indonesia, with 1.8 million tonnes annual capacity and USD 1.2 billion total investment, utilizing advanced deinking technology for recovered paper processing.[3]"Annual Report 2024," Nine Dragons Paper Holdings Limited, ndpaper.com The investment demonstrates how Chinese manufacturers expand regional presence to secure raw material supply and serve growing packaging demand across Southeast Asia.

The competitive landscape increasingly rewards scale, technology integration, and sustainability credentials as key success factors for long-term market leadership, with ISO 9001 and FSC certifications becoming standard requirements for major customer contracts. Oji Holdings Corporation completed acquisition of 65% stake in Malaysian corrugated packaging manufacturer for MYR 280 million (USD 63 million), expanding regional presence and adding 180,000 tonnes annual converting capacity across Peninsula Malaysia. The transaction demonstrates how Japanese packaging manufacturers pursue inorganic growth strategies to expand regional footprint and serve multinational customers across Southeast Asia.

South East Asia Corrugated Packaging Industry Leaders

-

SCG Packaging Public Company Limited

-

Oji Holdings Corporation

-

Rengo Co., Ltd.

-

Toppan Inc.

-

Smurfit WestRock

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2024: PT Pura Barutama implemented Esko Cape Pack optimization software across corrugated production lines, achieving 8.5% reduction in raw material usage while improving box strength by 15% through optimized flute orientation and cutting patterns.

- November 2024: Sarnti Packaging Co., Ltd. deployed machine learning algorithms for corrugated box design optimization, resulting in 11% average material usage reduction and THB 45 million (USD 1.25 million) annual cost savings.

- October 2024: Harta Packaging Industries installed digital printing capabilities at Selangor facility with MYR 15 million (USD 3.4 million) investment, enabling minimum run sizes of 500 units and capturing 28% more SME customer orders.

- September 2024: Vina Kraft Paper Co., Ltd. expanded containerboard capacity by 400,000 tonnes through USD 180 million investment at Dong Nai facility, including advanced water treatment systems and energy recovery capabilities.

South East Asia Corrugated Packaging Market Report Scope

- Corrugated board packaging is a versatile and cost-efficient method to protect, preserve, and transport a wide range of products. Attributes, such as light-weight, biodegradability, and recyclability, are the advantages of this packaging that make it an essential component in modern life.

- The market has been segmented by the end-user industry (Food and Beverage, Cosmetics and Household Care, Manufacturing and Automotive, Healthcare and Pharmaceutical, Other End-User Industry (Electrical and Electronics, Others)

- The study also covers the impact of COVID-19 on the market.

By End-User Industry

| Food and Beverage |

| Electrical and Electronics |

| Cosmetics and Personal Care |

| Healthcare and Pharmaceutical |

| Automotive and Industrial |

| Other End-User Industries |

By Board Type

| Single Face |

| Single Wall |

| Double Wall |

| Triple Wall |

By Flute Type

| A-Flute |

| B-Flute |

| C-Flute |

| E-Flute |

| F-Flute and Micro-Flutes |

By Printing Technology

| Flexographic |

| Digital (Inkjet) |

| Litho-lamination |

| Other Printing Technologies |

By Country

| Indonesia |

| Thailand |

| Malaysia |

| Vietnam |

| Philippines |

| Singapore |

| Rest of South-East Asia |

| By End-User Industry | Food and Beverage |

| Electrical and Electronics | |

| Cosmetics and Personal Care | |

| Healthcare and Pharmaceutical | |

| Automotive and Industrial | |

| Other End-User Industries | |

| By Board Type | Single Face |

| Single Wall | |

| Double Wall | |

| Triple Wall | |

| By Flute Type | A-Flute |

| B-Flute | |

| C-Flute | |

| E-Flute | |

| F-Flute and Micro-Flutes | |

| By Printing Technology | Flexographic |

| Digital (Inkjet) | |

| Litho-lamination | |

| Other Printing Technologies | |

| By Country | Indonesia |

| Thailand | |

| Malaysia | |

| Vietnam | |

| Philippines | |

| Singapore | |

| Rest of South-East Asia |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How are digital technologies transforming corrugated packaging in South-East Asia?

Digital flexographic printing reduces lead times from 14 days to 3 days for short runs, while AI-enabled design software cuts material usage by 5-12%. Companies like Thai Containers Group invested THB 280 million in Bobst's digital lines, while Sarnti Packaging's AI implementation saved THB 45 million annually through optimized box designs.

What is driving growth in the South-East Asia corrugated packaging market?

The market is primarily driven by e-commerce parcel volumes (+1.2% CAGR impact), food delivery expansion (+0.8%), single-use plastic regulations (+0.6%), and plantation-based fiber advantages (+0.5%). Vietnam's food delivery market grew 26% in 2024, while Indonesia's massive consumer base commands 21.55% regional market share.

Which country leads the South-East Asia corrugated packaging industry?

Indonesia commands the largest share at 21.55% of the South-East Asia corrugated packaging market, leveraging its 270 million population and integrated manufacturing infrastructure. Vietnam shows the fastest growth trajectory with 5.42% CAGR through 2031, driven by food delivery expansion and manufacturing diversification.

What challenges affect the South-East Asia corrugated packaging supply chain?

Key challenges include kraft liner price volatility (-0.9% CAGR impact), inferior humidity resistance during monsoons (-0.5%), fragmented logistics across archipelago regions (-0.4%), and skilled operator shortages for advanced equipment (-0.3%). Material costs fluctuated 18% in Q4 2024, creating margin pressure for converters.

Which end-user industries dominate corrugated packaging demand in South-East Asia?

Food and beverage applications lead with 34.62% market share, while e-commerce packaging shows highest growth at 5.17% CAGR through 2031. Single wall boards maintain 38.64% market share, though triple wall configurations grow fastest at 4.36% CAGR for heavy-duty applications.

How is sustainability influencing corrugated packaging development in the region?

Sustainability drives adoption through plastic phase-out regulations across Indonesia, Vietnam, and Thailand, plantation-based fiber with 5-7 year harvest cycles (versus 25-30 years for temperate regions), and AI-optimized designs reducing material usage by 11% while improving strength by 18%.