Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

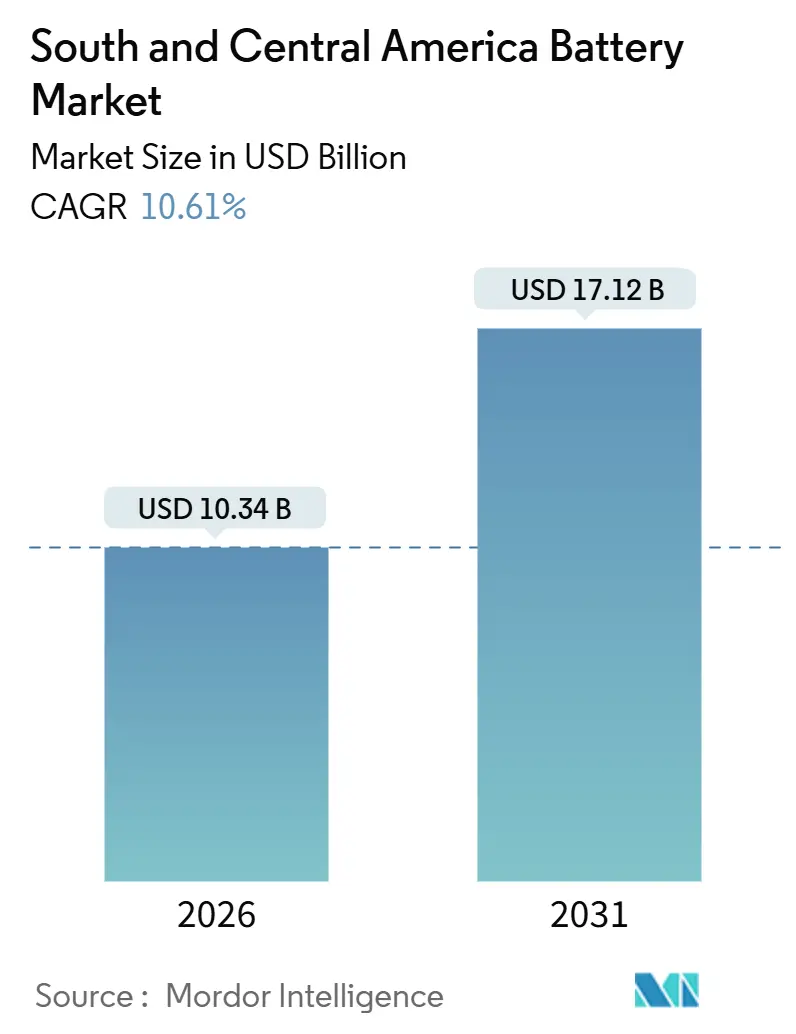

| Market Size (2026) | USD 10.34 Billion |

| Market Size (2031) | USD 17.12 Billion |

| Growth Rate (2026 - 2031) | 10.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South And Central America Battery Market Analysis by Mordor Intelligence

The South And Central America Battery Market size is estimated at USD 10.34 billion in 2026, and is expected to reach USD 17.12 billion by 2031, at a CAGR of 10.61% during the forecast period (2026-2031).

This expansion reflects synchronized policy support, local lithium refining that trims logistics costs, and rising electrification across transportation, grid storage, and telecom infrastructure. Incentives under Brazil’s MOVER program and Chile’s National Electromobility Strategy are narrowing the electric-vehicle price premium to 15% or less, which is accelerating demand for automotive packs. Simultaneously, lithium-triangle projects in Argentina, Chile, and Bolivia are shortening supply-chain lead times by up to two-thirds, improving cost competitiveness versus Asian imports. Stationary storage is gaining momentum as renewable penetration in key grids moves above 35%, while telecom operators transition from lead-acid to lithium-ion backup to cut cooling energy and site visits. These factors, coupled with accelerating spending on portable electronics in Colombia and Peru, underpin a durable growth runway for the South & Central America battery market.[1]Staff Report, “Chile’s National Electromobility Strategy Mandates 100% Zero-Emission Public Transport by 2035,” Bloomberg, bloomberg.com

Key Report Takeaways

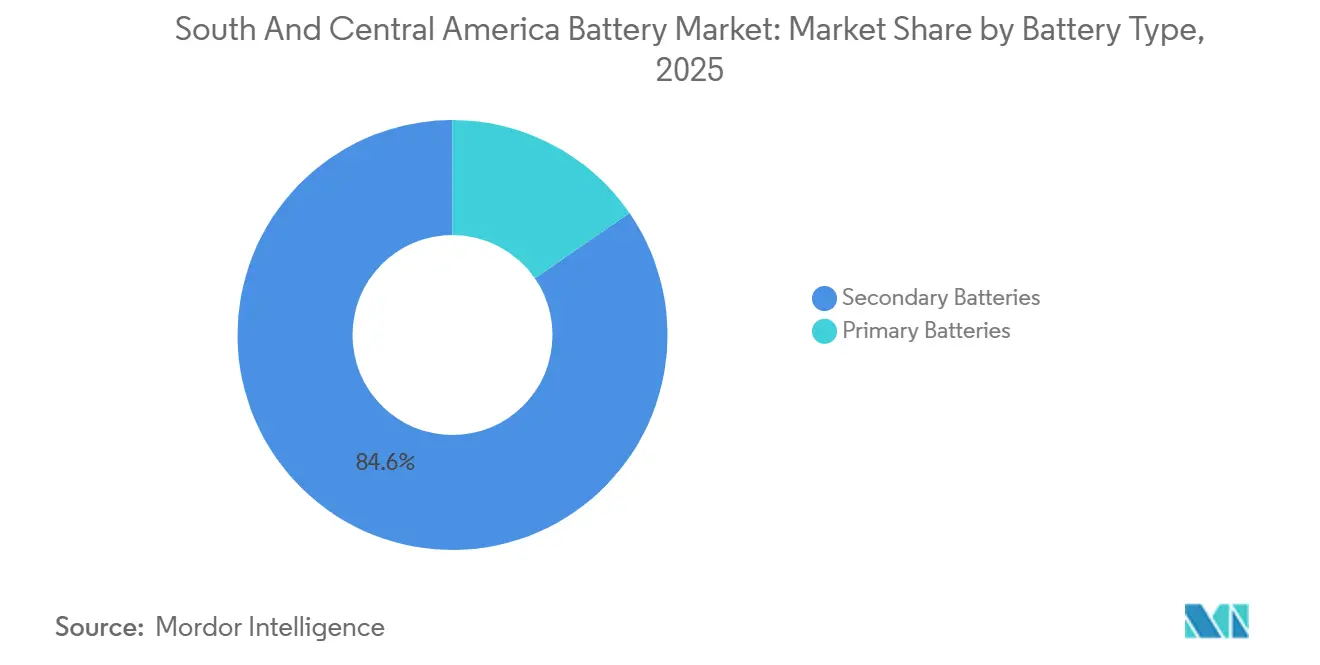

- By battery type, secondary batteries captured 84.6% of the South & Central America battery market share in 2025, while solid-state chemistries are forecast to post the highest 28.7% CAGR through 2031.

- By technology, lithium-ion commanded 47.9% of revenue in 2025; solid-state is projected to deliver the fastest expansion, lifting its share from 0.3% in 2025 to 3.2% in 2031.

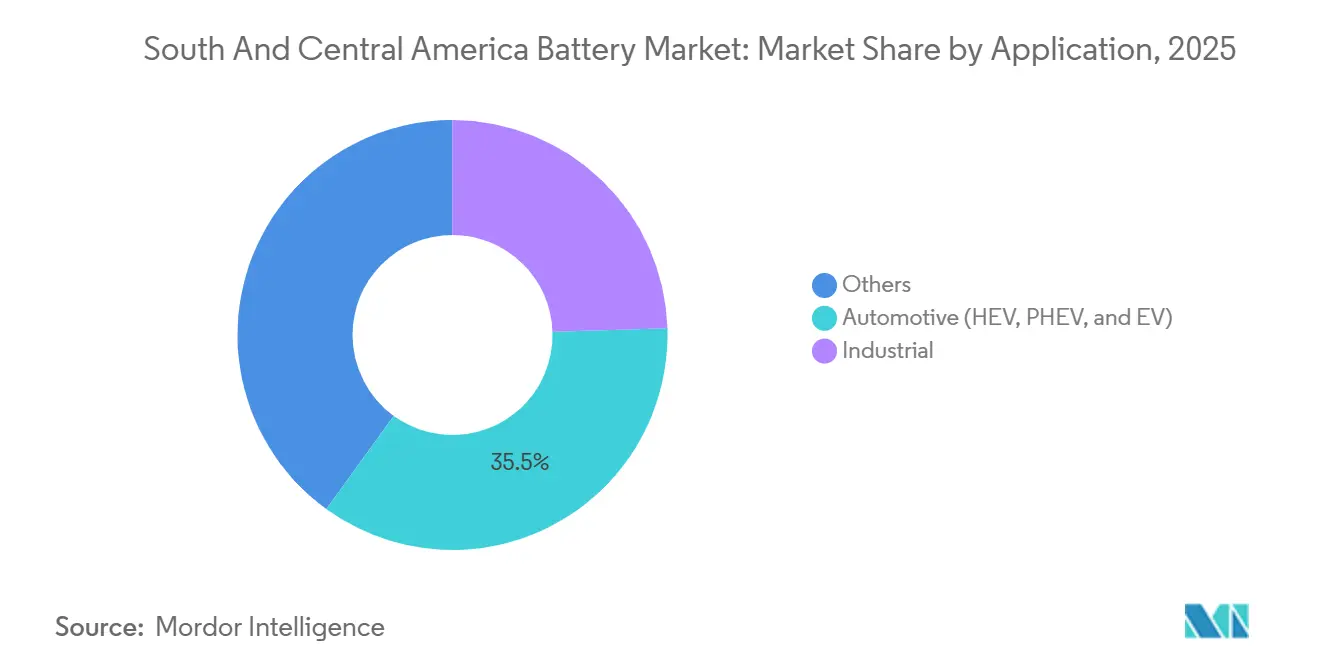

- By application, portable batteries represented 18.3% of demand in 2025 and are advancing at a 16.8% CAGR on the back of smartphone and remote-work uptake.

- By geography, Brazil held a 41.1% share in 2025, whereas Chile is the fastest-growing country with a 15.3% CAGR projected through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South And Central America Battery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV purchase incentives in Brazil & Chile | +2.3% | Brazil, Chile | Medium term (2-4 years) |

| Renewable-powered micro-grids driving ESS demand | +1.8% | Chile, Brazil, Argentina | Long term (≥4 years) |

| Telecom-data-center backup upgrades | +1.1% | Brazil, Chile, Colombia | Short term (≤2 years) |

| Lithium-triangle mining investments enabling local supply | +2.9% | Argentina, Chile, Bolivia | Long term (≥4 years) |

| Urban e-scooter fleet proliferation | +0.7% | Brazil, Chile, Colombia, Peru | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

EV Purchase Incentives in Brazil & Chile Compress Total Cost of Ownership

Tax credits granted under Brazil’s MOVER program and Chile’s import-duty waivers for sub-USD 50,000 electric cars have lowered upfront prices by 15%-25% relative to comparable internal-combustion models.[2]Staff Report, “Brazil’s MOVER Program Allocates BRL 19.6 Billion in EV Tax Credits Through 2028,” Reuters, reuters.com As a result, fleet operators in São Paulo and Santiago placed combined orders exceeding 1,500 electric buses in 2025, each requiring a 324 kWh lithium-ion pack. Leasing companies are rebalancing portfolios toward battery-electric vehicles to capture lower maintenance outlays and stronger residual values. The policy signal has also prompted domestic pack assembly expansions by BYD and Stellantis, which cuts logistics costs tied to imported modules. Fiscal durability diverges, however: Brazil faces a widening deficit and potential post-2026 revisions, whereas Chile funds its incentives via a carbon-tax mechanism that generated USD 400 million in 2025 and enjoys broad legislative support.

Renewable-Powered Micro-Grids Driving ESS Demand in Off-Grid Mining and Agriculture

High solar irradiation in the Atacama Desert and robust wind resources in Brazil’s Northeast are enabling large-scale solar-plus-storage projects that displace diesel gensets. Grenergy’s 11 GWh Oasis de Atacama system, paired with a 632 MW solar array, is designed to supply SQM’s lithium operations entirely off grid. Similar initiatives from AES Andes and YPF Luz illustrate a wider push to match renewable peaks with battery discharge, thereby avoiding costly grid upgrades. Diesel price spikes—Argentine diesel rose 120% in 2024—reinforce the business case for batteries, while Scope 3 emission targets among European metal off-takers add further pressure. Analysts expect off-grid mining and remote agribusiness projects to add over 4 GWh of new storage between 2026 and 2031, lifting the South & Central America battery market.

Telecom-Data-Center Backup Upgrades Favor Lithium-Ion Over Lead-Acid

Brazilian mobile network operators have begun replacing valve-regulated lead-acid batteries with lithium-ion modules across 5G sites, securing 10,000-cycle life and a 60% reduction in air-conditioning loads. Saft’s 2025 contract covering 2,500 Telefónica towers is emblematic of a broader shift driven by Uptime Institute availability standards and ANATEL guidelines that recommend lithium-ion for unreliable-grid locations. Data centers in Santiago and Bogotá echo this transition, installing multi-MWh UPS banks that unlock insurance discounts tied to higher uptime. Lead-acid retains relevance in legacy nodes and budget-constrained environments, yet lithium-ion’s total cost of ownership advantage is widening as import tariffs on lithium-ion cells fall under regional trade accords.

Lithium-Triangle Mining Investments Enable Local Supply and Vertical Integration

Projects such as Rio Tinto’s USD 2.5 billion Rincon mine and Bolivia’s planned USD 1 billion hydroxide plant are ushering in a new era of regional cathode supply. By refining lithium near the brine assets, exporters can shrink logistics cycles from up to 120 days to under 45 days. Early estimates indicate delivered-cost reductions of 12%-15% versus shipping unrefined material to Asia, a differential large enough to entice BYD and LG Energy Solution to expand local pack lines. Geographic bottlenecks persist, notably Salta’s limited rail infrastructure and water-scarcity constraints near Uyuni, but policy makers are accelerating rail and desalination investments to sustain momentum. Provided timelines hold, South America could supply cathode precursor to regional gigawatt-scale pack plants by 2027, a development that would further reinforce the South & Central America battery market.

Urban E-Scooter Fleet Proliferation Broadens Peak-Demand Profile

Shared-mobility operators ran 45,000 e-scooters across five major metropolitan areas in 2025, each powered by 460 Wh swappable packs. Daily battery exchanges exceed 1.5 million cycles per month and are creating a nascent secondary-life market for packs retired after 700 cycles. Municipal congestion charges and low-speed-zone expansions are pushing commuters toward micro-mobility, while ride-hailing platforms bundle e-scooter options to raise utilization. Battery assemblers have responded by building compact swap stations that package charging, data analytics, and recycling drop-off in a single unit. Although the energy throughput is modest relative to automotive demand, the high-cycle nature of micro-mobility adds steady volume growth to the South & Central America battery market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material cost volatility | -1.4% | Brazil, Colombia, Peru | Short term (≤2 years) |

| Limited fast-charging infrastructure | -1.2% | Argentina, Colombia, Peru, rural Brazil | Medium term (2-4 years) |

| Currency-driven import price swings | -0.9% | Argentina, Brazil, Chile | Short term (≤2 years) |

| Environmental licensing delays for recycling plants | -0.5% | Brazil, Chile | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Cost Volatility Erodes Manufacturer Margins and Delays Capacity Commitments

Lithium carbonate prices fell 80% between early 2023 and mid-2024, squeezing manufacturers that secured high-priced offtake contracts during the upswing. Margin compression of 8-12 percentage points forced CATL, LG Energy Solution, and Samsung SDI to defer certain South American assembly investments. Cobalt and nickel price swings compounded budgeting uncertainty, making it harder for pack integrators to lock in fixed-price agreements with automakers. The resulting hesitation slowed capital deployment for local cell lines and contributed to under-investment in ancillary supply-chain assets. Relief is expected once European and North American gigafactories absorb excess raw material around 2027, but near-term volatility continues to temper the growth trajectory of the South & Central America battery market.

Limited Fast-Charging Infrastructure Constrains Long-Distance EV Adoption

The region hosted fewer than 2,000 DC fast chargers in 2025, with density concentrated in three capital cities. Long-haul corridors such as Rio-Manaus and Santiago-Arica remain underserved, forcing EV owners to rely on slower AC alternatives or abandon trips altogether. Regulatory uncertainty compounds the problem: Brazil’s ANEEL has yet to publish final tariff structures for public charging, while Chile requires environmental permits for chargers above 350 kW, adding 12-18 months to rollout schedules. The resulting range anxiety caps EV uptake outside major metros and, by extension, moderates near-term battery demand. Stakeholders anticipate a step change only after policy makers finalize clear tariffs, offer grid-connection subsidies, and streamline permitting, milestones that are unlikely before 2028.

Currency-Driven Import Price Swings Distort Project Economics

A 54% peso depreciation in 2023 and a 10% Brazilian real slide in 2024 inflated the dollar cost of imported separators, electrolytes, and formation equipment. Such volatility complicates cash-flow projections for assemblers that set local-currency selling prices months in advance. Hedging instruments remain shallow, particularly for small and mid-size pack integrators. The resulting cost pass-through to end users can blunt the uptake benefits created by policy incentives, adding another layer of uncertainty that tempers South & Central America battery market growth.

Environmental Licensing Delays for Recycling Plants Slow Circular-Economy Build-Out

Battery-recycling proposals in Brazil and Chile must navigate multi-year impact assessments, partly because hydrometallurgical facilities involve handling hazardous reagents. Project developers report 24-30-month processing times at Brazil’s IBAMA, a window that discourages rapid scale-up of local recycling. The absence of sufficient domestic recycling capacity forces end-of-life packs to be shipped abroad, adding logistics costs and complicating compliance with extended-producer-responsibility rules. Until streamlined permitting accelerates plant approvals, the recycling gap will constrain supply of locally sourced nickel, cobalt, and lithium, adding dependency on imported materials and restraining the South & Central America battery market.

Segment Analysis

By Battery Type: Secondary Cells Extend Dominance Amid EV and Storage Tailwinds

Secondary batteries commanded 84.6% of revenue in 2025 and are projected to post an 11.1% CAGR through 2031, outpacing the overall South & Central America battery market size over the same horizon.[3]Staff Report, “Chile’s National Electromobility Strategy Mandates 100% Zero-Emission Public Transport by 2035,” Bloomberg, bloomberg.com Within the segment, lithium-ion chemistry contributed 92% of value, reflecting its entrenched role in electric vehicles, grid storage, and telecom backup. Lead-acid retains a sizable 28% sub-segment share for industrial motive equipment and SLI replacements, sustained by cost-sensitive buyers that prioritize upfront price over energy density.

The growth engine remains a policy-led surge in renewable generation that requires oscillation management. Chile alone targets 8 GWh of utility-scale storage by 2028, reinforcing demand for high-cycle lithium-ion modules. At the same time, Brazil’s net-metering scheme under Normative Resolution 1,000/2021 is spurring residential and commercial adoption, with behind-the-meter batteries reaching 450 MWh in 2025.[4]Staff Report, “Saft Wins Contract to Replace Lead-Acid Batteries at Telefónica Towers,” Reuters, reuters.com Environmental rules mandating reverse logistics for alkaline and zinc-carbon products are accelerating substitution away from primary cells. Nonetheless, niche demand for primary lithium batteries persists in medical and industrial sensing scenarios, making the secondary-primary split a nuanced dynamic within the South & Central America battery market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Technology: Solid-State Set to Accelerate From 2027 Pilot Lines

Lithium-ion held a 47.9% share in 2025, reflecting its cost-performance sweet spot across multiple use cases. Lead-acid followed at 38.2%, while nickel-metal hydride and nickel-cadmium trailed as legacy chemistries. Solid-state batteries represented only 0.3% in 2025 but are on course for a 28.7% CAGR, positioning them as the fastest-growing technology in the South & Central America battery market share landscape.

Pilot production by Toyota-Idemitsu and QuantumScape in 2027-2028 will introduce 1,000-kilometer EV range and sub-10-minute charging capabilities. OEMs with local assembly—Stellantis, General Motors—have signaled intent to migrate to solid-state packs once cost falls to USD 100/kWh at pack level, a milestone expected near 2029. Sodium-ion is another emerging contender; CATL’s 160 Wh/kg cells are earmarked for entry-level EVs targeting an USD 18,000 sticker price, but energy-density constraints limit use to city cars and stationary storage. Flow batteries and sodium-sulfur configurations remain niche but are carving out long-duration storage roles in desert micro-grids, adding chemistries that diversify, but do not yet redefine, the South & Central America battery market size equation.

By Application: Portable Segment Becomes Fastest-Expanding Use Case

Automotive packs accounted for 35.5% of demand in 2025, mirroring EV volume gains in Brazil and Chile. Industrial batteries, including forklifts and telecom standby, held 28.7%. The portable segment, covering consumer electronics, power banks, and wearables, represented 18.3% and is forecast to grow at a 16.8% CAGR, making it the quickest-rising slice of the South & Central America battery market.

Smartphone penetration in Colombia and Peru has climbed to 82%, and remote-work trends are sustaining laptop and tablet demand. Rising power-tool adoption and the electrification of two-wheeler fleets provide additional lift. Meanwhile, SLI replacement cycles are lengthening as micro-hybrid technology reduces discharge depth, trimming the share of conventional lead-acid units. Collectively, application diversification underpins resilient growth even as automotive policies remain the dominant swing factor for the South & Central America battery market share outlook.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Brazil owned 41.1% of South & Central America battery market size in 2025, supported by its population scale, automotive base, and telecom modernizations. The MOVER program’s USD-indexed tax credits have attracted BYD’s USD 150 million expansion that adds 10 GWh of pack capacity by 2026. Nevertheless, currency volatility and sparse fast-charging coverage outside coastal corridors temper upside.

Chile, though smaller in absolute terms, is expanding at a 15.3% CAGR, the fastest in the region. Its energy mix—dominated by solar and wind—and lithium endowment underpin both supply and demand pull for batteries. Grenergy’s 11 GWh project and Santiago’s growing fast-charger network illustrate a policy ecosystem that rewards storage deployment.

Argentina captured 16.8% share in 2025 but faces an 8.9% CAGR ceiling as peso instability and policy uncertainty cool investor appetite. Colombia and Peru together hold 13.2% share; both benefit from renewable mandates and mining electrification but need streamlined permitting to realize full potential. The balance of countries, including Bolivia and Uruguay, rely mostly on off-grid solar-plus-storage and pilot e-mobility schemes, which collectively contribute incremental volume to the broader South & Central America battery market.

Competitive Landscape

Moderate concentration defines the competitive field. The top five lithium-ion suppliers—BYD, CATL, LG Energy Solution, Samsung SDI, and Panasonic—controlled roughly 38% of segment revenue in 2025, while lead-acid leaders Clarios, Exide, and EnerSys held 52% of industrial and SLI sales. Global Tier-1 players favor asset-light supply agreements instead of regional gigafactories, mitigating currency risk and demand uncertainty.

Strategic moves in 2025-2026 include CATL’s tolling arrangement with BYD’s Campinas plant and LG Energy Solution’s module supply to Stellantis’s Betim facility. Panasonic and Honda are exploring export channels from new U.S. plants to serve South American assembly lines post-2027. White-space opportunities persist in stationary storage, where lithium-ion penetration remains below 15%, particularly among telecom and data-center operators seeking higher uptime.

Technology road maps suggest an inflection toward solid-state and sodium-ion, with Toyota’s 2027 pilot lines and CATL’s sodium-ion tests in Brazilian e-scooters providing key milestones. Regulatory compliance around reverse logistics is emerging as a competitive differentiator; Clarios operates 1,200 Brazilian recycling points, giving it a head start as extended-producer-responsibility rules tighten. These dynamics indicate a trajectory toward diversified chemistries and service-oriented revenue streams within the South & Central America battery market.

South And Central America Battery Industry Leaders

BYD Company Ltd.

Panasonic Corporation

EnerSys

EnerSys

Saft (TotalEnergies)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: BYD committed USD 150 million to expand its Campinas pack facility by 10 GWh, creating 800 jobs and targeting electric bus supply across the region.

- September 2025: Grenergy broke ground on the 11 GWh Oasis de Atacama storage project paired with 632 MW of solar in Chile, scheduled for late 2026 commissioning.

- December 2025: Rio Tinto’s Salta-based Rincon mine produced first lithium carbonate, initiating a ramp to 60,000 tons per year by 2028.

- December 2025: CATL partnered with Stellantis to deliver sodium-ion cells aimed at sub-USD 18,000 compact EVs assembled in Brazil from 2027.

South And Central America Battery Market Report Scope

An electric battery is a source of electric power consisting of one or more electrochemical cells with external connections for powering electrical devices.

The South and Central American battery market is segmented by type, technology, applications, and geography. By type, the market is segmented by primary battery and secondary battery. By technology, the market is segmented by lead-acid battery, lithium-ion battery, and other technologies. By application the market is segmented by automotive, industrial batteries (motive, stationary (telecom, UPS, energy storage systems (ESS), etc.)), consumer electronics, and other applications. The report also covers the market size and forecasts for the market across the major countries. For each segment, the market size and forecasts have been in USD billion.

By Battery Type

| Primary Batteries |

| Secondary Batteries |

By Technology

| Lead-acid |

| Li-ion |

| Nickel-metal hydride |

| Nickel-cadmium |

| Sodium-sulfur |

| Solid-state |

| Flow Battery |

| Emerging chemistries |

By Application

| Automotive (HEV, PHEV, and EV) | |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) | |

| Portable (Consumer Electronics, etc.) | |

| Power Tools | |

| SLI | |

| Other Applications | Light EVs |

By Geography

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South and Central America |

| By Battery Type | Primary Batteries | |

| Secondary Batteries | ||

| By Technology | Lead-acid | |

| Li-ion | ||

| Nickel-metal hydride | ||

| Nickel-cadmium | ||

| Sodium-sulfur | ||

| Solid-state | ||

| Flow Battery | ||

| Emerging chemistries | ||

| By Application | Automotive (HEV, PHEV, and EV) | |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) | ||

| Portable (Consumer Electronics, etc.) | ||

| Power Tools | ||

| SLI | ||

| Other Applications | Light EVs | |

| By Geography | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South and Central America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the South & Central America battery market in 2026?

The South & Central America battery market is estimated at about USD 10.4 billion in 2026, continuing its path toward USD 17.12 billion by 2031 on a 10.61% CAGR.

Which country leads regional battery demand?

Brazil leads with 41.1% revenue share in 2025, driven by auto production scale, telecom upgrades, and generous tax incentives.

What is the fastest-growing battery technology?

Solid-state batteries are projected to expand at a 28.7% CAGR through 2031 as automakers plan 2027-2028 commercial launches.

Why is portable-battery demand rising so fast?

Higher smartphone penetration and remote-work adoption in Colombia, Peru, Brazil, and Chile are pushing power-bank and laptop-battery sales, producing a 16.8% CAGR in the portable segment.

What impedes faster EV adoption in the region?

Sparse fast-charging networks outside major cities and currency volatility that inflates imported component costs are the primary hurdles.

Are local lithium reserves reshaping the supply chain?

Yes, mining and refining projects in Argentina, Chile, and Bolivia are cutting lead times and logistics costs, enabling competitive regional cathode and pack assembly by 2027.