Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

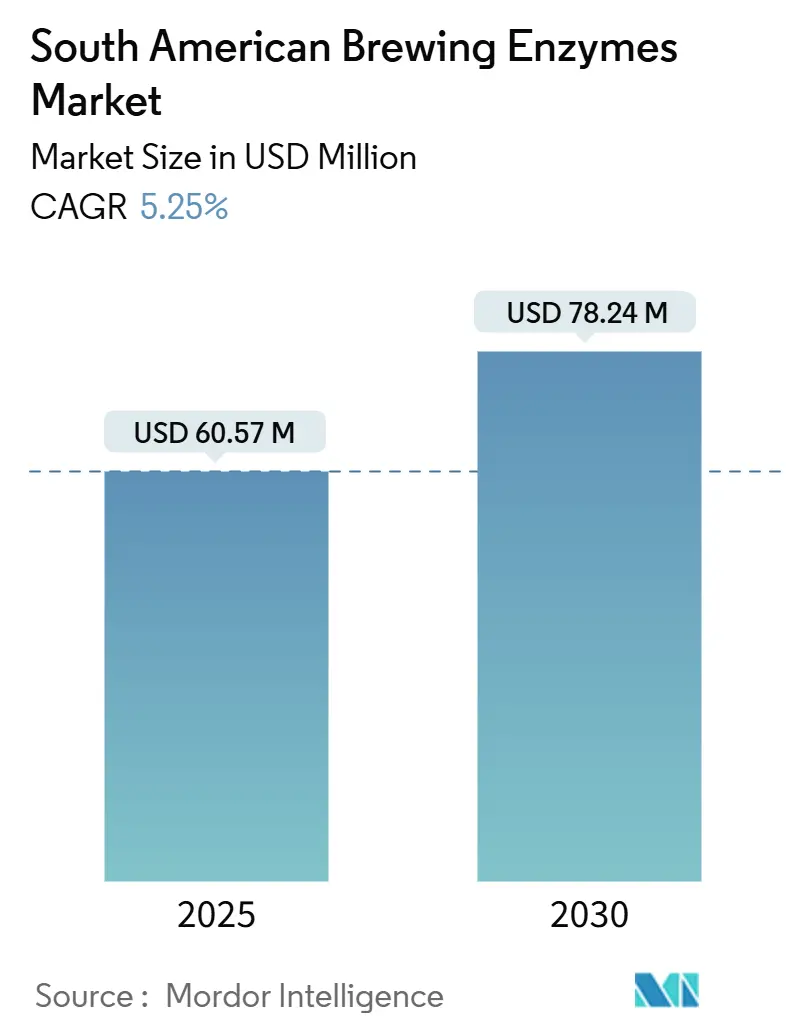

| Market Size (2025) | USD 60.57 Million |

| Market Size (2030) | USD 78.24 Million |

| Growth Rate (2025 - 2030) | 5.25% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South American Brewing Enzymes Market Analysis by Mordor Intelligence

The South American brewing enzyme market size stood at USD 60.57 million in 2025 and is projected to reach USD 78.24 million by 2030 at a 5.25% CAGR during 2025-2030. The continuous growth of craft breweries, increasing demand for low- and no-alcohol beers, and the adoption of high-gravity brewing protocols are driving enzyme consumption, even amid raw material cost fluctuations. Microbial enzymes dominate the market due to their consistent performance and cost efficiency, while plant-based alternatives are gaining traction in premium and clean-label segments that avoid GMO labeling. Breweries, particularly in Brazil and Colombia, where cold-chain challenges are significant, are increasingly opting for dry enzymes. This preference helps them mitigate the complexities of fragmented cold-chain logistics and the high energy demands of refrigerated storage. In response, suppliers are focusing on localized production, portfolio diversification, and technical service offerings to secure multiyear contracts with both craft and major brewers aiming for process efficiency and flavor innovation.

Key Report Takeaways

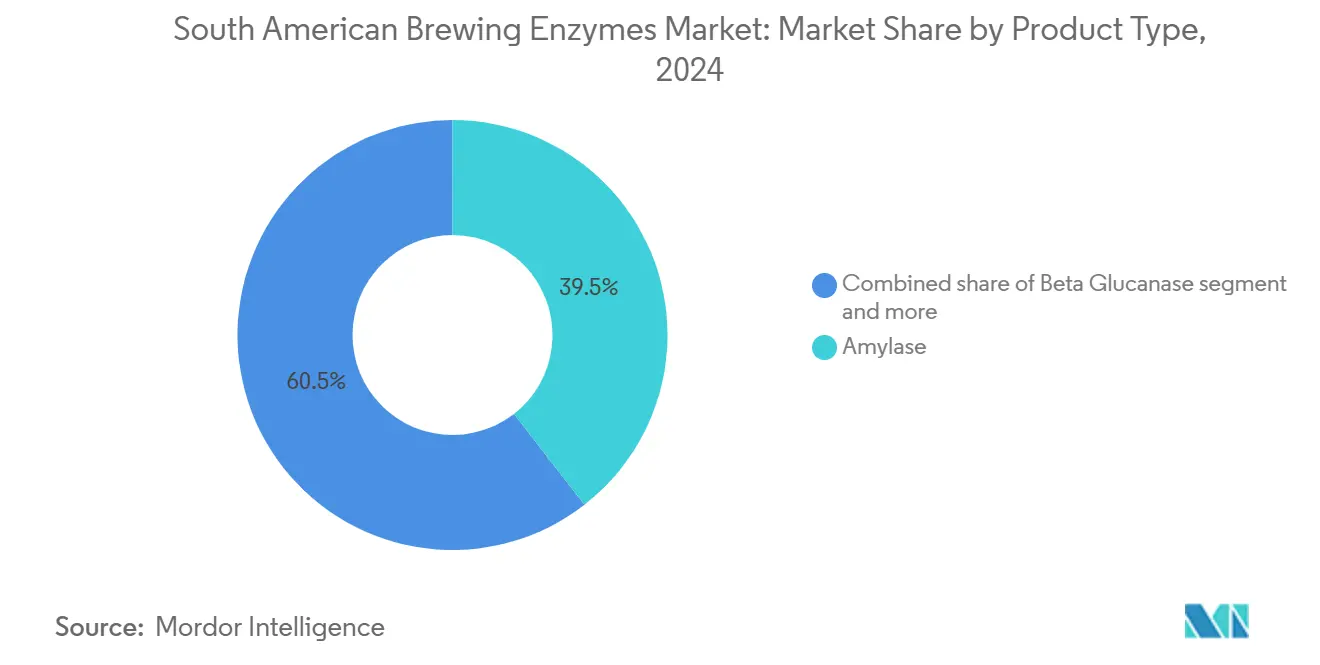

- By product type, amylase led with 39.47% of the South American brewing enzyme market share in 2024; beta-glucanase is forecast to expand at a 5.89% CAGR through 2030.

- By source, microbial enzymes accounted for 81.98% of the South American brewing enzyme market size in 2024, while plant-based alternatives are advancing at a 6.02% CAGR to 2030.

- By form, liquid formulations captured 65.27% revenue in 2024; dry enzymes are the fastest mover at 5.95% CAGR through 2030.

- By application, beer dominated with 90.17% volume in 2024, and wine enzymes are rising at a 6.35% CAGR during the forecast period.

- By geography, Brazil commanded 41.74% revenue share in 2024, and Colombia records the highest projected CAGR of 7.17% to 2030.

South American Brewing Enzymes Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising craft-beer production | +1.2% | Brazil, Chile, Argentina; nascent in Colombia | Medium term (2-4 years) |

| Expanding microbrewery and home brewing culture | +0.9% | Brazil, Colombia, Chile; regulatory easing in Argentina | Medium term (2-4 years) |

| Growing demand for low-/no-alcohol beer styles | +1.4% | Brazil (primary), Chile, Argentina | Short term (≤ 2 years) |

| Increasing adoption of enzymes in high gravity brewing | +0.8% | Global, with early gains in Brazil, Argentina | Long term (≥ 4 years) |

| Flavor innovation through controlled enzymatic conversion | +0.6% | Brazil, Chile, Argentina; premium segments | Medium term (2-4 years) |

| Cost-out pressure favouring enzyme-enabled malt-savings | +1.1% | Brazil, Colombia with currency volatility | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising craft-beer production

By 2023, Brazil's craft-beer segment included 1,847 registered breweries, as stated by the Ministry of Agriculture and Livestock [1]Source: Ministry of Agriculture and Livestock, "Anuário da Cerveja 2024", gov.br. At the same time, Chile's premium and craft categories are steadily increasing their market share. The growth of small-batch producers has driven up the demand for specific enzymes in specialty styles, such as saisons, sour ales, and hazy IPAs. These styles require precise beta-glucanase and protease dosing to manage viscosity and protein haze, eliminating the need for the expensive filtration systems used by larger breweries. In Colombia, the craft beer market accounts for less than 2 percent of the total market share but is attracting investments from regional private-equity funds. These investors view enzymatic process control as a competitive advantage, particularly in a market where Bavaria dominates with 98 percent of the mainstream volume. In Argentina, brewers are taking advantage of increased domestic barley production, spurred by European buyers seeking alternatives to Russian and Ukrainian supplies, to explore single-origin malt profiles. They are using amylase blends to extract fermentable sugars from grains with lower diastatic power. The growing craft-beer movement is driving demand for liquid enzyme formats, which dissolve quickly and enable easier dosing in batches ranging from 500 to 5,000 liters. However, dry enzymes are also gaining popularity among larger regional players looking to reduce their dependence on cold-chain logistics.

Growing demand for low-/no-alcohol beer styles

In Brazil, non-alcoholic beer consumption has risen significantly, driven by growing health awareness and stricter drunk-driving regulations. According to Banco do Nordeste, Brazil's annual consumption of non-alcoholic beverages reached 21.63 billion liters in 2024 [2]Source: Banco do Nordeste, "Caderno Setorial ETENE", bnb.gov.br. Brewers are increasingly using enzymatic production methods, particularly controlled applications of amylase and glucoamylase. This approach halts fermentation at or below 0.5% alcohol by volume, preserving malt sweetness and body, attributes often diminished by thermal dealcoholization or reverse-osmosis techniques. Similarly, Chile's premium beer segment is implementing these enzyme-based methods to introduce low-alcohol product lines that appeal to female consumers and younger audiences seeking moderation without compromising flavor. However, balancing residual maltose and dextrin profiles presents a technical challenge. Excessive amylase activity can result in a thin, watery mouthfeel, while insufficient conversion leaves an overly sweet taste. To address this, enzyme suppliers are developing time-temperature-optimized blends that achieve a final gravity of 4 to 6 Plato. In Argentina, brewers are incorporating proteases to improve foam stability in low-alcohol variants, offsetting the reduced role of ethanol in bubble formation and head retention. These advancements are driving the adoption of plant-based enzymes like papain, valued for their broader pH tolerance and compatibility with clean-label trends, which resonate strongly in health-focused retail markets.

Increasing adoption of enzymes in high gravity brewing

Brewers in Brazil and Argentina are adopting high-gravity brewing to address rising electricity costs and capacity challenges. This technique, which ferments wort at 18 to 22 degrees Plato before dilution, reduces energy consumption per hectoliter by 20 to 25 percent and enhances fermenter throughput. Enzymes are essential in this process, converting non-fermentable dextrins into fermentable sugars, enabling yeast to achieve desired alcohol levels without excessive malt usage. Typically, 15 to 20 percent of base malt is replaced with enzymatically treated adjuncts like corn or rice in high-gravity recipes, resulting in notable raw material savings. Colombia's Bavaria has implemented high-gravity brewing at its Bogotá and Barranquilla facilities, utilizing thermostable alpha-amylase to maintain enzyme activity during extended mash holds at 72 to 75 degrees Celsius. In Chile, brewers are integrating high-gravity fermentation with beta-glucanase to prevent viscosity issues that can disrupt filtration, particularly when using oat or wheat adjuncts that increase beta-glucan levels above 200 milligrams per liter.

Flavor innovation through controlled enzymatic conversion

Craft and premium brewers across South America are leveraging enzyme cocktails to create unique flavor profiles that stand out in competitive retail markets. Protease additions not only reduce chill-haze precursors but also release amino acids, enhancing the production of yeast-derived esters and phenols. This process results in fruit-forward or spice-accented notes, particularly in Belgian-style ales and wheat beers. Additionally, beta-glucanase improves wort filterability and speeds up lautering, cutting brew-day cycles by 15 to 20 minutes. This efficiency allows brewers to produce more batches per week without investing in larger mash tuns. In Argentina, brewers are experimenting with Malbec-inspired beer by infusing grape must into wort. They use pectinase and cellulase to clarify the blend and prevent pectin-haze, a technique influenced by the country’s wine-grape vineyards. Brazilian microbreweries are adopting acetaldehyde-reducing enzyme blends to eliminate green-apple off-flavors in fast-turnaround lagers. This approach reduces conditioning time from 21 days to 14 days, improving cash flow for operators with limited capital. Regulatory frameworks, such as Brazil's ANVISA Resolution RDC 272/2019, require enzyme suppliers to document purity and safety. This has driven demand for non-GMO, plant-based enzymes, which bypass CTNBio labeling requirements and appeal to organic-certified breweries.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Potential allergen concern in genetically engineered enzymes | -0.4% | Brazil, Argentina; regulatory oversight by CTNBio, CONABIA | Medium term (2-4 years) |

| Volatile malt and barley price correlation | -0.5% | Argentina, Brazil with currency exposure | Short term (≤ 2 years) |

| Fragmented cold-chain logistics for liquids | -0.7% | Brazil, Colombia, Peru; infrastructure deficits | Long term (≥ 4 years) |

| Currency-linked import duties on specialty enzymes | -0.6% | Colombia, Argentina; peso volatility, MERCOSUR CET variability | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented cold-chain logistics for liquids

Brazil's refrigerated-storage infrastructure fails to meet growing demand. Consequently, liquid-enzyme distributors depend on third-party cold-chain providers, whose energy expenses account for 75 percent of operating budgets. Liquid enzymes must be stored at temperatures between 2 to 8 degrees Celsius to preserve their activity over a six-to-twelve-month shelf life. However, temperature fluctuations during inland transport, particularly to breweries in Brazil's Northeast or Colombia's Andean regions, can reduce enzyme potency by 10 to 15 percent. This loss forces brewers to over-order by 20 percent to mitigate activity degradation. In Colombia, logistics costs are inflated by inadequate road infrastructure and complex regulatory checkpoints. INVIMA, the regulatory authority, requires Good Manufacturing Practice certification and Spanish-language labeling. Furthermore, customs clearance at Bogotá and Cartagena ports can extend lead times by two to three weeks. This fragmented system is driving brewers to adopt dry enzyme formats, which can be stored at ambient temperatures and have a shelf life of two to three years. However, these formats come with drawbacks, such as longer dissolution times and dust-handling challenges in manual-dosing environments. This issue is particularly severe for small craft breweries without on-site refrigeration. They must either accept a shorter enzyme shelf life or pay a 15 to 20 percent premium for dry formulations.

Currency-linked import duties on specialty enzymes

MERCOSUR's Common External Tariff framework facilitates duty-free trade of enzymes classified under HS code 3507 among its member states. However, Argentina's peso devaluation, exceeding 50 percent against the U.S. dollar in 2023, and Colombia's currency volatility have driven a quarterly increase of 8 to 12 percent in landed costs for imported specialty enzymes. Brazil applies a 14 percent import duty on enzymes sourced from outside the MERCOSUR bloc, but bilateral agreements with the European Union and ongoing trade negotiations with China could lower tariffs on microbial enzymes by 2026. Argentine brewers benefit from record domestic barley production, driven by European buyers diversifying supply chains, but they remain dependent on imports for specialty enzymes like beta-glucanase and xylanase. This reliance exposes them to currency risks during periods of devaluation. To address these challenges, enzyme suppliers are pursuing local manufacturing partnerships. For example, Apexzymes, a Campinas-based startup, is developing an enzyme platform leveraging Brazilian biodiversity. Supported by FAPESP and Argentina's GridExponential venture fund, the company targets a 2026 commercial launch, which could reduce supply-chain lead times and protect brewers from currency fluctuations.

Segment Analysis

By Product Type: Amylase Anchors Revenue, Beta-Glucanase Gains on Clarity Mandates

In 2024, amylase contributes 39.47 percent of product-type revenue, highlighting its essential role in starch liquefaction and saccharification across brewing processes, including lagers, ales, and adjunct-heavy protocols. Beta-glucanase, growing at a 5.89 percent CAGR through 2030, is driven by craft brewers increasingly incorporating oat, wheat, and barley. These grains elevate wort beta-glucan content beyond 200 milligrams per liter, necessitating enzymatic solutions to prevent filtration blockages and haze formation. Protease, which holds a notable share, helps brewers reduce chill-haze precursors and accelerate conditioning cycles. This is particularly important for fast-turnaround lagers, with Brazilian and Colombian breweries now adopting 14-day fermentation windows as a standard.

Additionally, enzymes such as xylanase, cellulase, and acetolactate decarboxylase serve niche purposes in gluten-reduced beer production and diacetyl management. Their adoption is primarily seen in premium and craft segments, where consumers are willing to pay a 10 to 15 percent premium for distinctive flavor profiles. This product-type segmentation reflects a maturing market: foundational enzymes like amylase and protease continue to sustain volume, while specialty enzymes such as beta-glucanase and xylanase drive margin growth and enable brewers to achieve premium retail pricing.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Source: Microbial Dominance Faces Clean-Label Pressure

In 2024, microbial enzymes account for 81.98 percent of source-based revenue. This dominance is driven by the consistent activity and scalable fermentation economics of Aspergillus and Bacillus strains, which have also gained regulatory approvals from Brazil's ANVISA, Argentina's ANMAT, and Colombia's INVIMA. Meanwhile, plant-based enzymes are projected to grow at a 6.02 percent CAGR through 2030. This growth is supported by increasing consumer demand for clean-label products and craft brewers' efforts to avoid Brazil's CTNBio labeling requirements for genetically modified organisms. Enzymes such as papain, bromelain, and ficin, extracted from papaya, pineapple, and fig, offer a broader pH tolerance (3.5 to 8.0) compared to microbial amylase (pH 5.0 to 6.5). Their non-GMO positioning appeals to organic-certified and export-oriented brewing segments. While Argentina's CONABIA regulates GMO enzyme approvals and provides a clear pathway, some microbreweries prefer plant-derived enzymes to mitigate consumer concerns in Buenos Aires and Córdoba, where allergen-related narratives are gaining traction.

The cost difference remains significant, as plant-based enzymes are priced higher than microbial alternatives due to lower fermentation yields and the seasonal availability of raw materials. However, premium and craft brewers are willing to absorb these costs to enhance their marketing claims around natural ingredients and biodiversity sourcing. In Chile, the adoption of plant-based enzymes is accelerating in wine production. Pectinase and cellulase, derived from fungal or plant sources, are used to clarify grape must without introducing microbial off-flavors, preserving the varietal character of Malbec or Carmenere blends. On the innovation front, Brazil's CNPEM has discovered the CelOCE enzyme from the country's biodiversity. With patenting in progress and licensing discussions expected to conclude within one to four years, this development could reduce plant-based enzyme costs by 10 to 12 percent if scaled for commercial fermentation. This source segmentation highlights a strategic contrast: microbial enzymes lead in cost-performance, while plant-based enzymes are gaining traction due to their alignment with sustainability and clean-label trends that are reshaping purchasing decisions in the premium segment.

By Form: Liquid Convenience Versus Dry Stability

In 2024, large breweries prefer liquid enzymes, which account for 65.27 percent of the form-based revenue. These enzymes are chosen for their rapid dissolution, precise automated dosing, and compatibility with continuous-process systems that reduce batch-to-batch variability. Meanwhile, dry enzymes are experiencing growth, expanding at a 5.95 percent CAGR through 2030. This growth is primarily driven by brewers in tropical and subtropical regions addressing cold-chain challenges. For example, Brazil faces a significant 38.5 million cubic meter shortfall in refrigerated storage. Additionally, with 75 percent of cold-chain energy costs being a burden, brewers are incentivized to shift toward ambient-stable dry formats, which offer a shelf life of two to three years. Dry enzymes also provide logistical benefits due to their higher concentration and lighter weight, resulting in lower freight costs. This is particularly advantageous for Colombian brewers, who contend with poor road infrastructure and multi-agency customs checkpoints that extend inland transport times by two to three weeks. However, there is a trade-off: dry enzymes require 10 to 15 minutes of agitation in pre-mash water for full dispersion, while liquid formats achieve this in just 2 to 3 minutes. This efficiency makes liquid enzymes the preferred option for breweries with tight production schedules and limited buffer time between batches.

In Argentina, craft brewers are increasingly adopting dry enzymes to simplify inventory management and reduce reliance on third-party cold-chain logistics. While they accept the longer dissolution times, they gain operational flexibility and lower spoilage risks. In Chile, premium brewers continue to favor liquid enzymes to support automated dosing systems that ensure batch consistency. However, export-oriented breweries are gradually shifting to dry formats, prioritizing shelf-stable inputs to minimize supply-chain disruptions during long-haul shipments to Asian and North American markets. This form segmentation highlights a broader trend: operational infrastructure, such as cold-chain capacity, automation levels, and batch size, plays a more significant role in format selection than the intrinsic performance of the enzymes.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Beer Volume Sustains Market, Wine Margin Expands

In 2024, beer applications lead the market, representing 90.17 percent of the volume, fueled by strong beer production. Enzyme usage is primarily concentrated in lagers, ales, and adjunct-heavy styles, which dominate mainstream retail. The growth in beer production, along with increasing exports from the region, supports the beer application. For example, Chile's beer exports, valued at USD 3.33 million in 2023, surged to USD 16.04 million in 2024, according to UN Comtrade [3]Source: UN Comtrade, " UN Comtrade data", comtradeplus.un.org. On the other hand, wine applications are experiencing steady growth, with a 6.35 percent CAGR projected through 2030. This growth reflects the outputs of Chile and Argentina, both of which are increasingly adopting enzymatic methods for clarification, color extraction, and filtration. These processes not only maintain the wine's varietal character but also reduce processing times. In red-wine maceration, enzymes such as pectinase, glucanase, and cellulase are used to enhance anthocyanin extraction and soften tannins. This reduces the skin-contact time from 14 days to 10 days while improving fermenter throughput by 25 to 30 percent. Additionally, Malbec producers in Argentina are leveraging enzyme blends to optimize phenolic extraction in high-altitude vineyards. In these regions, grape skins thicken due to increased UV exposure, requiring controlled enzymatic breakdown to prevent astringency.

Chile's harvest has declined due to drought, increasing the demand for enzymes per hectoliter as winemakers aim to maximize juice yield and color intensity from reduced grape volumes. The wine segment's faster growth is driven by premiumization trends and a focus on exports. Chilean wines are exported to Latin America, Asia, and the U.S., where retail buyers prioritize consistent clarity and color stability, attributes that enzymatic processing delivers more reliably than traditional fining agents like bentonite or isinglass. In the beer sector, enzyme applications are expanding beyond traditional amylase and protease. Craft brewers are now utilizing specialty enzymes such as beta-glucanase for clarifying hazy IPAs and acetolactate decarboxylase for diacetyl management. These innovations enable craft brewers to shorten conditioning cycles, improving cash flow. The segmentation of applications highlights beer's dominance in volume and wine's contribution to margins. Both sectors are increasingly adopting enzyme-driven process optimizations to address challenges like raw-material volatility and the demand for premiumization.

Geography Analysis

In 2024, Brazil holds a significant 41.74 percent share of regional revenue, driven by its active breweries. Colombia, fueled by a growing craft beer industry and rising disposable income among the middle class, is projected to grow at a robust 7.17 percent CAGR through 2030, the fastest in the region. However, INVIMA's multi-agency registration process, which includes Spanish-language labeling, Good Manufacturing Practice certification, and customs clearance, extends lead times by two to three weeks. This process reduces distributor margins and delays enzyme-SKU launches. Argentina secures a mid-tier market share by capitalizing on increased domestic barley production. This growth stems from European buyers diversifying their supply chains away from Russia and Ukraine, enabling brewers to explore single-origin malt profiles and enzyme-assisted adjunct substitutions that reduce raw material costs.

Economic challenges continue to limit enzyme adoption in Peru. The rest of South America, including Uruguay, Paraguay, and smaller markets, demonstrates limited enzyme penetration. Growth in these markets is tied to MERCOSUR's Common External Tariff framework, which allows duty-free intra-bloc trade for enzymes classified under HS code 3507. However, currency volatility in Argentina and Colombia has increased landed costs.

Brazil's ANVISA Resolution RDC 272/2019 enforces safety assessments and purity standards for food enzymes, driving demand for non-GMO, plant-based options. These alternatives bypass CTNBio's labeling requirements and appeal to organic-certified breweries. In Argentina, CONABIA regulates GMO enzyme approvals through an established pathway. Nevertheless, some microbreweries prefer plant-derived alternatives to avoid potential consumer resistance in retail markets like Buenos Aires and Córdoba. The geographic segmentation highlights Brazil's scale advantages, Colombia's rapid growth tempered by regulatory challenges, and the dual enzyme demand for beer and wine in Chile and Argentina. Meanwhile, Peru and smaller markets face constraints due to economic fluctuations and infrastructure limitations.

Competitive Landscape

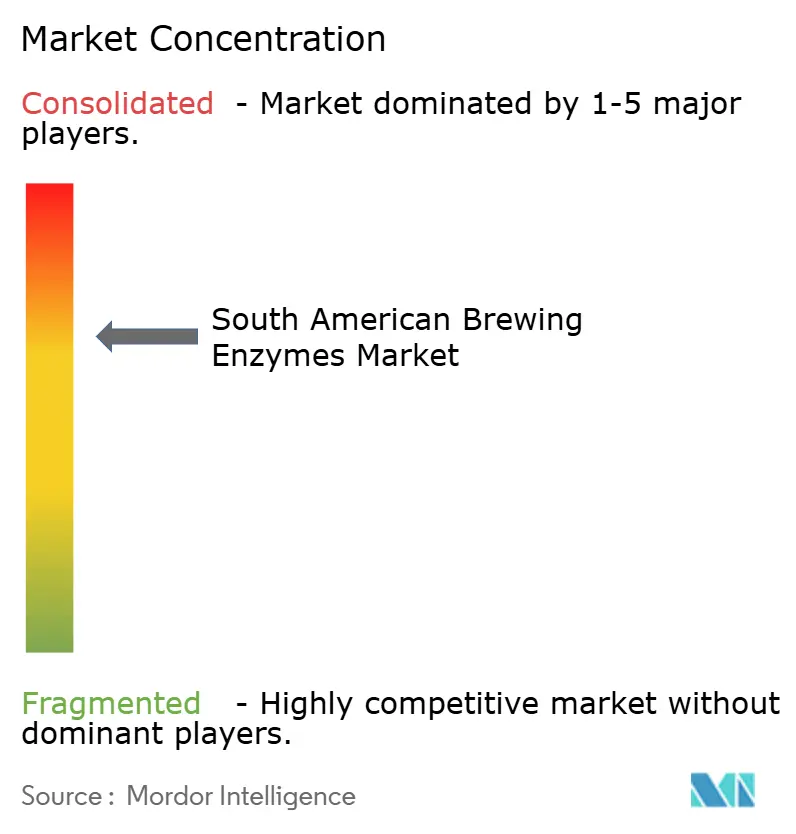

South American brewing enzymes market concentration remains moderately consolidated, with Novonesis, Kerry Group Plc, DuPont de Nemours, Inc., BASF SE, and DSM-Firmenich NV collectively holding an estimated significant share of regional revenue. However, no single player commands a dominant share due to fragmented brewery ownership and the pivotal role of regional distributors in last-mile delivery. This dynamic is evident across Brazil's Northeast, Colombia's Andean regions, and Argentina's interior provinces. Strategic positioning is bifurcating: global suppliers are offering broad enzyme portfolios with technical-service support, like Novonesis's SmartBev NEER for acetaldehyde reduction and DSM-Firmenich's Brewers Clarex for gluten management. In contrast, regional specialists such as Brazil's Prozyn and emerging ventures like Apexzymes are carving their niche. Apexzymes, for instance, is developing a Brazilian-biodiversity enzyme platform, backed by FAPESP and Argentina's GridExponential venture fund. Targeting a 2026 commercial launch, they aim to compress supply-chain lead times and shield brewers from currency-linked import-duty fluctuations.

White-space opportunities are emerging in enzyme solutions tailored for low-alcohol and alcohol-free beer styles. Controlled enzymatic hydrolysis allows brewers to halt fermentation at 0.5 percent alcohol by volume or below, all while preserving mouthfeel and flavor complexity. This capability, however, eludes traditional thermal or membrane processes, which often introduce off-notes. In a strategic move, BASF divested its bioenergy enzymes business to Lallemand in June 2024, retaining only feed and detergent enzymes. This divestiture signals a retreat from low-margin commodity segments, potentially paving the way for smaller enzyme suppliers to penetrate distribution channels, especially those targeting craft and premium breweries.

Technology adoption is on the rise among major players. For instance, Colombia's Bavaria, holding a commanding 98 percent of the national market, has trialed high-gravity brewing protocols at its Bogotá and Barranquilla plants. They've deployed thermostable alpha-amylase to sustain activity during extended mash holds at 72 to 75 degrees Celsius. This approach not only slashes per-hectoliter energy costs by 20 to 25 percent but also boosts fermenter throughput by 30 to 40 percent. Local innovation is gaining momentum, highlighted by CNPEM's discovery of the CelOCE enzyme from Brazilian biodiversity. Now patented, licensing discussions are expected to wrap up within one to four years. This development could pave the way for domestic enzyme production, curbing import reliance and alleviating currency-risk exposure. The competitive landscape is evolving, favoring enzyme suppliers that bundle technical-service support, like mash-protocol optimization and quality-control troubleshooting, with product sales. This approach resonates particularly with craft breweries that may lack in-house brewing scientists. These breweries are often willing to pay a 5 to 8 percent premium for consultative partnerships, which not only derisk recipe development but also expedite the time-to-market for seasonal and limited-edition releases.

South American Brewing Enzymes Industry Leaders

-

DuPont de Nemours, Inc.

-

Kerry Group Plc

-

DSM-Firmenich NV

-

BASF SE

-

Novonesis

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Novonesis has agreed to acquire DSM-Firmenich's Feed Enzyme Alliance for EUR 1.5 billion. This acquisition expands Novonesis's enzyme portfolio from brewing and food applications to include animal nutrition.

- May 2023: Kerry Group has acquired Proexcar, a Colombian company specializing in functional systems for meat and protein applications. This acquisition enhances Kerry's position in Colombia's food-processing sector and establishes a regional hub for distributing enzymes and ingredients across the Andean markets.

South American Brewing Enzymes Market Report Scope

By Product Type

| Amylase |

| Alphalase |

| Beta Glucanase |

| Protease |

| Other Types |

By Source

| Microbial |

| Plant |

By Form

| Dry |

| Liquid |

By Application

| Beer |

| Wine |

By Country

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Product Type | Amylase |

| Alphalase | |

| Beta Glucanase | |

| Protease | |

| Other Types | |

| By Source | Microbial |

| Plant | |

| By Form | Dry |

| Liquid | |

| By Application | Beer |

| Wine | |

| By Country | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the expected value of the South America brewing enzyme market in 2030?

The market is projected to reach USD 78.24 million by 2030 on a 5.25% CAGR.

Which enzyme type currently leads sales in South America?

Amylase holds the top position with 39.47% revenue share in 2024.

Why are dry enzyme formats gaining popularity?

Dry enzymes sidestep cold-chain gaps and offer two-year shelf life, cutting logistics costs in Brazil and Colombia.

Which country shows the fastest growth for brewing enzymes?

Colombia leads with a forecast 7.17% CAGR through 2030.

Page last updated on: