South America Two-Wheeler Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

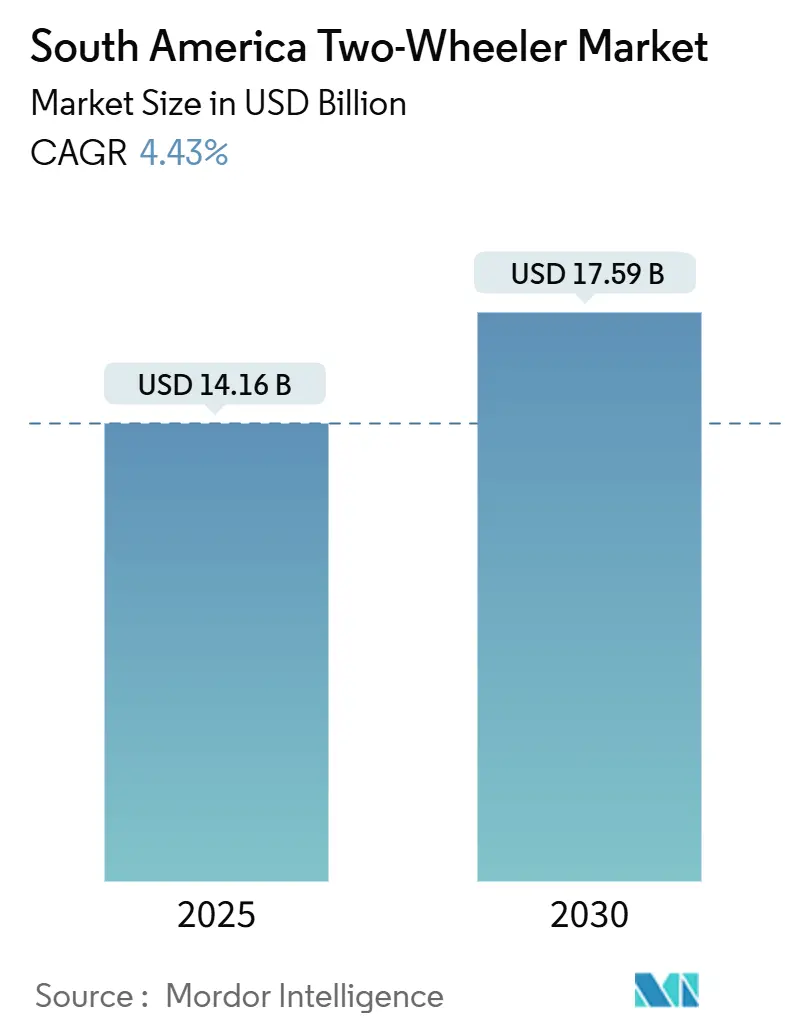

| Market Size (2025) | USD 14.16 Billion |

| Market Size (2030) | USD 17.59 Billion |

| Growth Rate (2025 - 2030) | 4.43% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Two-Wheeler Market Analysis by Mordor Intelligence

The South America two-wheeler market size is valued at USD 14.16 billion in 2025 and is forecast to reach USD 17.59 billion by 2030, registering a 4.43% CAGR during the forecast period. A structural shift toward commercial fleets, especially last-mile delivery operators, is expanding the addressable market for the South American two-wheeler market as gig-economy platforms proliferate. Rising localization by global OEMs is compressing landed costs and anchoring competitive price points, while steady smartphone-enabled micro-financing expands first-time ownership. Regulatory nudges—from Brazil’s flex-fuel incentives to tariff relief on Li-ion packs—add momentum, yet fragmented emission rules and currency volatility temper the velocity of substitution. Within this setting, manufacturers are racing to balance conventional ICE demand with a measured push into entry-level electrification and connected-vehicle features that open up new revenue streams.

Key Report Takeaways

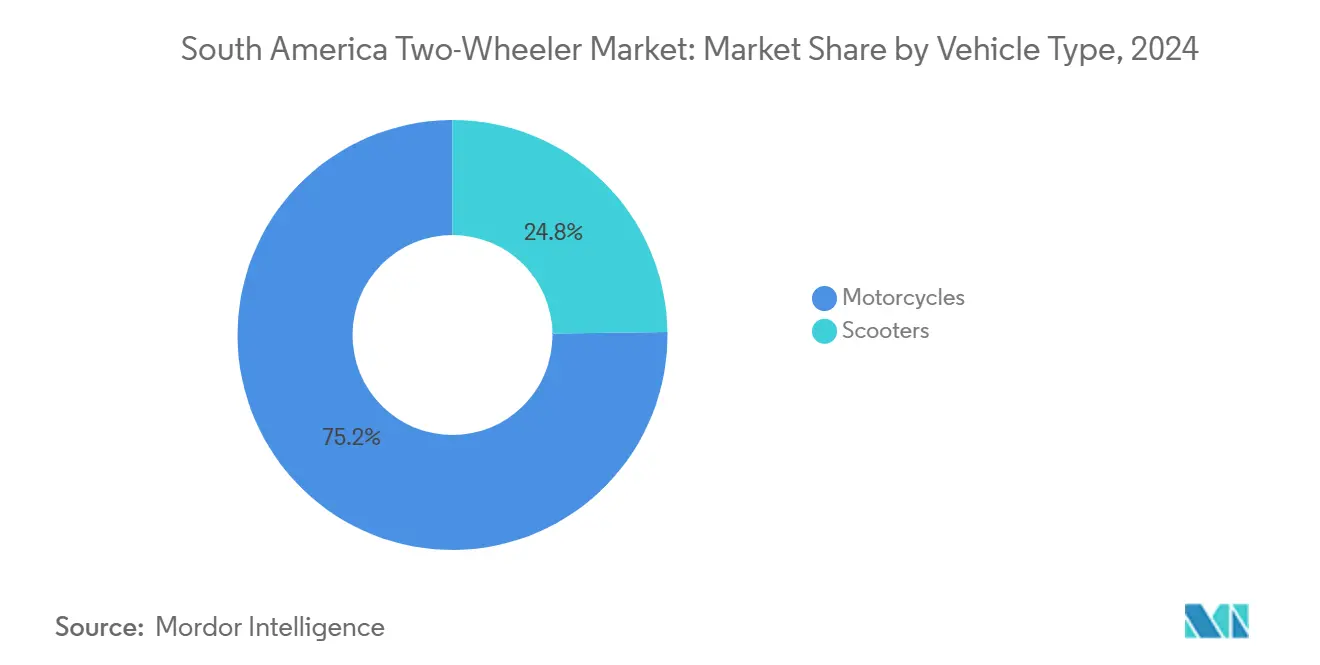

- By vehicle type, motorcycles led with a 75.22% share of South America's two-wheeler market in 2024; scooters are expected to advance at a 5.16% CAGR through 2030.

- By propulsion, internal combustion engine models accounted for 97.26% of the South America two-wheeler market size in 2024, while electric variants are projected to grow at a 9.52% CAGR to 2030.

- By engine capacity/motor power, two-wheelers with a capacity of up to 110 cc commanded a 42.31% share of the South American two-wheeler market in 2024, and the 1.1-3.0 kW electric band is expected to expand at a 7.43% CAGR through 2030.

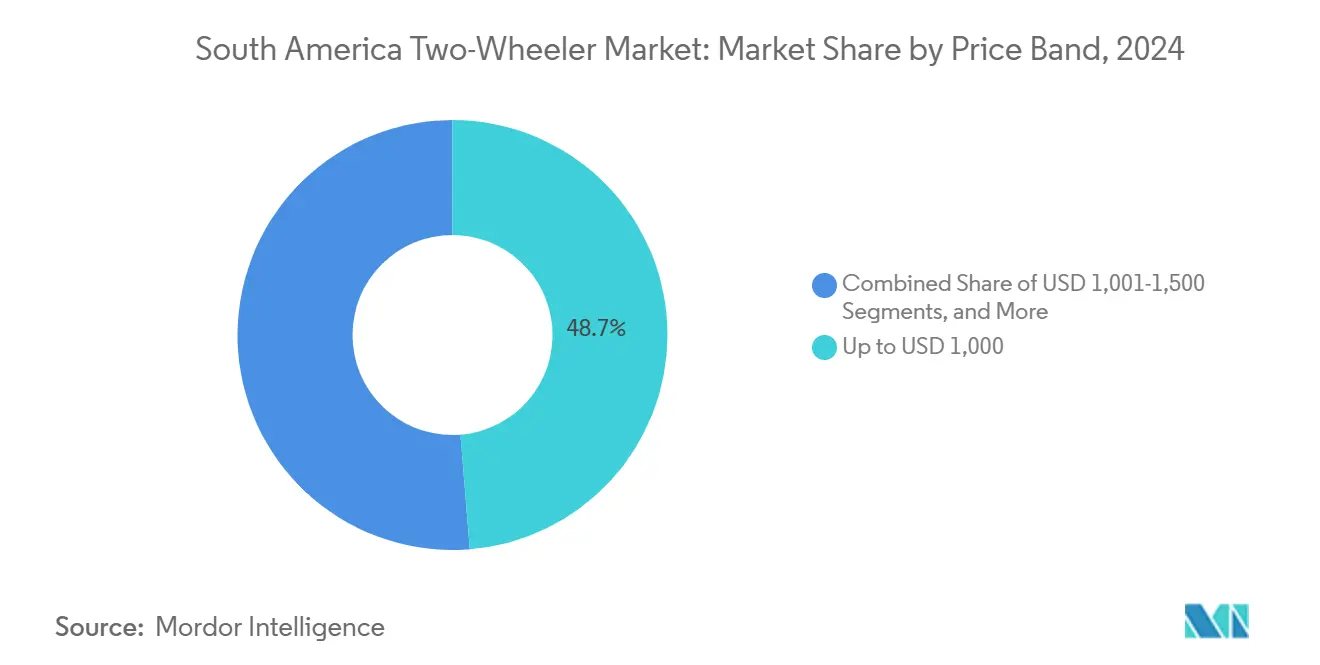

- By price band, sub-USD 1,000 motorcycles captured 48.72% share of the South American two-wheeler market in 2024; the USD 1,501-2,000 bracket is forecast to post a 6.22% CAGR by 2030.

- By end user, B2C will account for 69.61% of the South American two-wheeler market in 2024, while delivery and logistics are expected to grow at a 6.29% CAGR through 2030.

- By sales channel, offline outlets held a 92.17% share of the South American two-wheeler market in 2024, while online channels are projected to accelerate at a 7.28% CAGR through 2030.

- By country, Brazil dominated the South American two-wheeler market with a 64.31% share in 2024, and Colombia is projected to expand at a 5.28% CAGR through 2030.

South America Two-Wheeler Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Boom in Last-Mile and Gig Fleet Demand | +0.8% | Brazil core, spill-over to Colombia and Argentina | Short term (≤ 2 years) |

| Launch of Flex-Fuel and Ethanol Bikes for Brazil | +0.7% | Brazil national, limited regional spillover | Medium term (2-4 years) |

| OEM Localization (CKD/Plants in Manaus, Bogotá, Córdoba) Cutting Costs | +0.6% | Brazil, Colombia, Argentina with cross-border benefits | Long term (≥ 4 years) |

| Smartphone Micro-Financing Driving First-Time Buyers | +0.5% | Brazil, Colombia, Peru with urban concentration | Medium term (2-4 years) |

| Government Tariff Cuts on Li-Ion Imports for Two-Wheelers | +0.4% | Brazil national, potential MERCOSUR extension | Long term (≥ 4 years) |

| Connected Two-Wheelers (Telematics, OTA) Unlocking After-Sales Revenue | +0.3% | Brazil, Colombia tier-1 cities, gradual regional expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Last-Mile Delivery and Gig-Economy Fleet Demand

Brazil's delivery workforce has surged recently, reshaping consumer habits and leaving a significant impact on South America's two-wheeler market[1]“Pesquisa Nacional por Amostra de Domicílios Contínua,”, Brazilian Institute of Geography and Statistics, ibge.gov.br. In São Paulo, delivery riders predominantly opt to own their vehicles rather than lease them. This trend underscores how the rise of delivery platforms directly bolstered demand in the retail motorcycle sector. Due to intense daily usage, these vehicles experience accelerated wear and tear, resulting in more frequent replacements and increased sales of spare parts.

Colombia's urbanization trends suggest a parallel path, although the regulatory framework for gig workers remains uneven. Across the region, fleet managers clearly prefer motorcycles over scooters, valuing their enhanced load capacity and mechanical dependability. This choice ensures a consistent demand for robust vehicles.

Consequently, fleet compositions lean towards younger models, focusing on fuel-efficient, entry-level options. This trend establishes a feedback loop: heightened usage amplifies the demand for affordable, reliable two-wheelers, solidifying motorcycles' role in the urban logistics framework.

Introduction of Flex-Fuel and Ethanol-Ready Motorcycle Models Tailored to Brazil

Brazil’s ethanol infrastructure forecasts project total ethanol production to reach 32.5 billion liters in CY 2024, positions flex-fuel motorcycles as a near-term decarbonization bridge [2]“Ethanol-Ready Motorcycle Technologies,”, Society of Automotive Engineers, sae.org. Bajaj’s E27.5-compliant platforms exemplify adaptations that exploit ethanol’s 60-70% price advantage over gasoline, keeping running costs low for fleet operators. Ethanol compatibility also helps OEMs stay ahead of tightening emission caps without steep battery investments. Developing its biofuel sector, Argentina could replicate this template; however, most other South American markets lack fuel-pump coverage for wide roll-outs. Accordingly, the South America two-wheeler market gains an intermediate propulsion pathway that fits local feedstock economics and extends ICE relevance while regulators set the stage for full electrification.

OEM Localization Waves Lowering Price Points

Major motorcycle manufacturers are increasingly moving from importing vehicles to assembling them locally in Brazil. Honda's long-term investment plans and Hero MotoCorp's recent opening of a new production facility highlight this strategic shift. By operating within the Manaus Free-Trade Zone, these companies can sidestep import tariffs and cut logistics costs, keeping entry-level model prices competitive, even amid currency fluctuations.

Following suit, brands like Royal Enfield and Bajaj have initiated local assembly operations. Meanwhile, Honda's facility in Argentina has started exporting components to its neighbors. These actions indicate a broader trend of regional supply chain integration. Trade provisions within the MERCOSUR bloc bolster this transition, permitting a significant portion of components to be sourced externally. This not only streamlines intra-bloc trade but also promotes joint sourcing strategies.

These collective moves are transforming the cost dynamics of the South American two-wheeler market. Models assembled locally now boast a distinct pricing edge, enhancing their accessibility to consumers and underscoring the benefits of domestic production.

Smart-Connected Two-Wheelers Creating New After-Sales Revenue Pools

Connected hardware is creeping into mainstream price points as insurers roll out usage-based policies and fleet owners demand live tracking to curb theft. Brazil’s data-protection law (LGPD) prompts OEMs to invest in cybersecurity processes that smaller assemblers may struggle to match, possibly widening technology gaps. Over-the-air firmware unlocks are emerging, opening up micro-transaction revenue streams; yet, the average South American rider remains price-sensitive and carefully weighs connectivity fees. Nonetheless, early commercial uptake suggests a progressive revenue mix shift for the South America two-wheeler market as telematics move from novelty to necessity.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emission Standard Mismatch Limiting Regional Exports | -0.6% | MERCOSUR core, Andean Community fragmentation | Medium term (2-4 years) |

| Limited 2W Charging/Swapping Infrastructure Beyond Tier-1 Cities | -0.5% | Regional, acute in secondary cities | Long term (≥ 4 years) |

| Currency Volatility Affecting Import Component Prices | -0.4% | Regional with Argentina, Brazil exposure | Short term (≤ 2 years) |

| Rising Accident/Theft Rates Driving Up Insurance Costs | -0.3% | Brazil, Colombia urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mismatch of Emission Standards Curbing Intra-Regional Exports

Brazil enforced PROCONVE L8 in January 2025, aligning with Euro VI norms and creating the region’s strictest motorcycle emissions bar [3]“PROCONVE L8 Resolution,”, Brazilian National Environment Council, conama.gov.br. Argentina, Peru, and Chile each follow distinct protocols; hence, OEMs must juggle multiple calibrations, which increases compliance spend and truncates economies of scale. Smaller assemblers lacking multi-region homologation budgets risk retreating to domestic niches, thereby tightening the South America two-wheeler market around heavyweight players capable of absorbing certification overheads. Non-tariff barriers thus slice potential intra-bloc trade gains that would otherwise stem from Mercosur tariff relief.

Currency-Driven Price Volatility for Imported Components

Real and peso gyrations add instant sticker-shock when component invoices arrive in USD, the predominant trade currency for engines, EFI systems, and ABS modules. OEMs hedge with forward contracts and source plastics and frames locally, yet core electronics stay dollar-linked. Entry-level segments bear the brunt because price ceilings are rigid. Consumer budgets shift toward used bikes during spikes, offsetting volume growth in the South American two-wheeler market.

Segment Analysis

By Vehicle Type: Motorcycles Retain Scale While Scooters Accelerate

Motorcycles accounted for a 75.22% share of the South America two-wheeler market in 2024, as buyers favored versatile frames suited to rural tracks and gig-delivery payloads. The segment’s installed service network and favorable residuals enhance purchase confidence, particularly among commercial riders who clock high mileage. As OEMs add cargo racks, reinforced sub-frames, and flexible financing, motorcycles remain the workhorse across Brazil’s interior and Colombia’s inter-city routes.

However, urban congestion and parking constraints are pushing city commuters toward scooters, which are expected to log a 5.16% CAGR through 2030. Continuous-variable transmissions, flat floors, and lower seat heights are designed to accommodate female and senior riders. Scooter penetration relies on expanding BRT lanes, where lighter-footprint scooters dodge access bans on higher-displacement bikes. Over the next five years, the South American two-wheeler market is likely to converge on a dual-track profile: motorcycles for revenue-generating fleets and scooters for convenience-oriented urbanites.

Momentum for scooters is strongest in Bogotá, Medellín, and Santiago, where fuel savings and maneuverability trump cargo capacity. OEMs tune variants like Honda PCX and Yamaha NMAX with LED lighting, ABS, and smartphone-linked dashboards to justify mid-tier prices. Financing platforms now offer a tenor of up to 48 months, reducing monthly outlays and broadening their appeal. Retailers report a rising share of first-time female buyers, a demographic once underrepresented, despite cultural inertia favoring motorcycles. Sustained infrastructure adaptation and environmental curbs position scooters to chip gradually at the South American two-wheeler market over the forecast horizon.

By Propulsion: ICE Dominance Holds as Electric Gains Foothold

Internal-combustion engines held a 97.26% share of the South American two-wheeler market in 2024, underscoring entrenched fueling logistics and low entry costs. Flex-fuel compatibility provides extra resilience, as ethanol retains a 30-40% retail discount compared to gasoline in Brazil, thereby cushioning operating expenses. Parts inventories, roadside mechanics, and secondary markets are ICE-centric, reinforcing perceived reliability. Electric sales are projected to grow at a 9.52% CAGR through 2030, driven by import-duty relief for battery packs, city centers implementing zero-emission delivery mandates, and declining lithium-ion cell prices.

Fleet trials by Rappi in São Paulo revealed a 30% reduction in energy running costs compared to similarly sized petrol bikes, a data point that sparked interest among logistics contractors. Challenges persist: charging grids thin outside capital corridors, and up-front prices still carry a 25-30% premium. Yet, parity edges closer with battery vendors targeting USD 70/kWh. OEMs hedge by offering swappable modules in the 2.5 kWh class to minimize downtime, aligning with the 1.1-3.0 kW power segment scaling fastest. Across the timeline, electrification may rise to a mid-single-digit share, sustaining dual powertrain development within the South American two-wheeler market.

By Engine Capacity: Entry-Level Displacements Drive Volume

Up to 110 cc engines represented 42.31% share of the South American two-wheeler market in 2024, anchoring affordability benchmarks and satisfying urban range needs. Models such as the Honda CG 160 and Bajaj CT cater to gig-worker economics by pairing frugal fuel consumption with accessible maintenance. Financing plans typically peg monthly installments at below 8% of the minimum wage, widening the funnel for first-time homebuyers. Mid-tier 150-200 cc bikes retain popularity in Colombia’s hilly terrain, but volume dominance remains squarely with sub-125 cc capacities.

On the electric side, the South American two-wheeler market finds its sweet spot in 1.1-3.0 kW outputs, forecasted to rise at a 7.43% CAGR through 2030. The band aligns with metropolitan duty cycles of 60-90 kilometers per shift and fits within the 3-kWh battery sweet-spot that balances cost and curb weight. Battery-swap ecosystem pilots target this class for standardization, enabling fleet operators to reduce energy costs while maximizing asset utilization predictably.

By Price Band: Value Remains King but Mid-Tier Upgrades Quicken

Sub-USD 1,000 tags captured 48.72% share of the South American two-wheeler market in 2024, as informal-economy incomes pin buyer budgets. Local assembly and SKD strategies help keep prices down, even as foreign exchange fluctuations inflate imported content. Yet, rising expectations for ABS, digital clusters, and smartphone connectivity push many repeat buyers into the USD 1,501-2,000 tranche, the fastest-growing segment at a 6.22% CAGR through 2030. Micro-loan startups clear credit bottlenecks, and longer tenors dilute the monthly burden.

Premium tiers above USD 3,000 remain niche, populated by enthusiasts of BMW Motorrad and KTM. Steep import tariffs and volatile exchange rates limit reach beyond affluent cores in São Paulo, Buenos Aires, and Santiago. Nonetheless, the visibility of aspirational models serves a halo effect, nudging mass buyers toward mid-range trims with partial premium features, thus reshaping specification norms within the South American two-wheeler market.

Note: Segment shares of all individual segments available upon report purchase

By End User: B2C Retains Majority, B2B Delivery Leads Growth

Personal ownership accounted for a 69.61% share of the South American two-wheeler market in 2024, mirroring the motorcycle’s daily commuter and family hauler role. Rural dependability of two-wheelers in regions with patchy public transport sustains the B2C backbone. Rising insurance coverage and dealer loyalty programs deepen stickiness. Conversely, delivery and logistics riders now anchor the growth vector, expanding at a 6.29% CAGR through 2030, as platform work becomes an income mainstay.

Corporates adopting green-mile strategies are embracing electric two-wheelers for parcel runs under 50 kilometers, while municipal bodies are adding patrol fleets to navigate congested downtowns. Insurance firms, seeing lower accident speeds in scooter fleets, price group policies attractively, reinforcing B2B traction. These shifts diversify revenue sources and stabilize cyclicality in the South America two-wheeler market.

By Sales Channel: Dealers Still Rule, Digital Complements

Offline outlets accounted for a 92.17% share of the South American two-wheeler market in 2024. Many buyers find test rides, paperwork assistance, and proximity to a workshop non-negotiable. OEMs invest in express-service bays and spare-parts kiosks in peri-urban zones, preserving channel relevance. Online paths, however, post a 7.28% CAGR through 2030, catalyzed by pandemic-era digital comfort.

Platforms enable specification comparison and pre-approved financing, reducing showroom dwell time. Manufacturers pilot click-and-collect models where final registration and delivery still occur at partner dealers. The blend mitigates channel conflict and gradually migrates specific segments toward hybrid fulfillment across the South America two-wheeler market.

Geography Analysis

Brazil controlled a 64.31% share of the South America two-wheeler market in 2024. South America's two-wheeler market is transforming due to increasing urban delivery demand, regional manufacturing shifts, and evolving regulations. Brazil leads this change, driven by delivery riders, frequent vehicle replacements, and strong retail demand. Manufacturers are shifting to local assembly in areas like Manaus to reduce costs and remain competitive. Flex-fuel technology, domestic sourcing, and a vast dealer network support this ecosystem, while environmental standards drive engine innovation. Mercosur integration and strategic component sourcing enhance supply chain efficiency, giving locally produced models a competitive edge in terms of affordability and responsiveness.

Colombia charts the steepest slope, with a 5.28% CAGR, through 2030. Rapid urban migration is driving commuters toward two-wheel mobility as metro expansions lag. Bogotá’s CKD agendas attract vendor supply chains, trimming final prices. CrediOrbe and kindred fintechs alleviate credit friction, nudging penetration from informal toward formal financing. Swappable-battery pilots, with Copec as the seed, lay the groundwork for accelerated electrification.

Secondary markets—Argentina, Peru, Chile, Ecuador, Bolivia, and Paraguay—offer buffer growth and risk diversification. Argentina’s Decree 1069/2024 overhauls local content thresholds, prompting OEM re-costing. Peru’s RFID plate rule lengthens registration lead-times yet enhances security, potentially lowering theft-linked insurance premiums. Chile leads in charge-point density, attracting early electric adopters despite its modest population base. Therefore, the ensemble of smaller economies constitutes a fragmented yet opportunity-laden flank of the South America two-wheeler market.

Competitive Landscape

Market structure is moderately concentrated. Honda produces a substantial number of vehicles annually in Manaus, leveraging vertical integration to manage costs effectively. Bajaj and Hero MotoCorp import CKD kits from India, capturing entry-level price bands through scale in steel frames and common-platform engines. Royal Enfield taps lifestyle leanings with mid-displacement classics, while BMW Motorrad plays the prestige lane through Motorrad Days events.

Electric upstarts like Voltz Motors court fleet buyers with fixed-lease packs and telematics dashboards. Gogoro’s partnership model aligns hardware, software, and energy, delivering a holistic value proposition attractive to logistics companies. Dealer network reach and service parts availability remain decisive; therefore, incumbents invest significant capital expenditures (capex) into service training and parts logistics.

Strategic differentiators are shifting from mere engine displacement toward total cost of ownership and digital experience. OEM-fintech tie-ins reduce acquisition barriers, and connectivity suites promise subscription revenue. Firms that master multichannel retail and after-sales analytics are likely to expand their market share, particularly as fleet managers increasingly mandate uptime metrics and predictive maintenance.

South America Two-Wheeler Industry Leaders

-

Bajaj Auto Ltd.

-

Honda Motor Co. Ltd.

-

Suzuki Motor Corporation

-

Hero MotoCorp Ltd.

-

Yamaha Motor Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Honda's Brazilian subsidiary, Moto Honda da Amazonia Ltda. (HDA), is set to invest around 1.6 billion reais (approximately USD 296 million) in its Manaus plant in Amazonas State from 2026 to 2029. This investment aims to cater to the surging demand in Brazil's motorcycle market.

- October 2025: Bajaj officially launched the 2026 Dominar NS400Z motorcycle in Brazil. Manufactured in Manaus, Amazonas, this model stands as the most powerful offering from the national brand. With an output of 40 horsepower, it claims the title of Bajaj's most potent motorcycle in its domestic range. The company has integrated four riding modes: Road, Rain, Sport, and Off-Road, allowing riders to tailor the bike's performance to varying conditions, thereby enhancing its versatility.

South America Two-Wheeler Market Report Scope

The South America Two-Wheeler Market Report is Segmented by Vehicle Type (Motorcycles and Scooters), Propulsion (ICE and Electric), Engine Capacity/Motor Power (Up To 110cc, and More), Price Band (Up To USD 1, 000, and More), End User (B2C and B2B), Sales Channel (Online and Offline), and by Country. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Motorcycles |

| Scooters |

| Internal Combustion Engine (ICE) |

| Electric |

| Internal Combustion Engine (ICE) | Up to110 cc |

| 111-125 cc | |

| 126-150 cc | |

| 151-200 cc | |

| 201-250 cc | |

| 250-350 cc | |

| 350-500 cc | |

| Above 500 cc | |

| Electric | Up to 1.0 kW |

| 1.1-3.0 kW | |

| 3.1-5.0 kW | |

| Above 5.0 kW |

| Up to USD 1,000 |

| USD 1,000-1,500 |

| USD 1,501-2,000 |

| USD 2,001-3,000 |

| USD 3,001-5,000 |

| Above USD 5,000 |

| Business-to-consumer (B2C) | |

| Business-to-business (B2B) | Ride-hail / Bike-Taxi / Rental / Tourism |

| Delivery and Logistics | |

| Corporate and SME Fleets | |

| Others (Government and Institutional, NGO / Development) |

| Online |

| Offline |

| Brazil |

| Argentina |

| Colombia |

| Peru |

| Chile |

| Ecuador |

| Bolivia |

| Paraguay |

| Rest of South America |

| By Vehicle Type | Motorcycles | |

| Scooters | ||

| By Propulsion | Internal Combustion Engine (ICE) | |

| Electric | ||

| By Engine Capacity / Motor Power | Internal Combustion Engine (ICE) | Up to110 cc |

| 111-125 cc | ||

| 126-150 cc | ||

| 151-200 cc | ||

| 201-250 cc | ||

| 250-350 cc | ||

| 350-500 cc | ||

| Above 500 cc | ||

| Electric | Up to 1.0 kW | |

| 1.1-3.0 kW | ||

| 3.1-5.0 kW | ||

| Above 5.0 kW | ||

| By Price Band | Up to USD 1,000 | |

| USD 1,000-1,500 | ||

| USD 1,501-2,000 | ||

| USD 2,001-3,000 | ||

| USD 3,001-5,000 | ||

| Above USD 5,000 | ||

| By End User | Business-to-consumer (B2C) | |

| Business-to-business (B2B) | Ride-hail / Bike-Taxi / Rental / Tourism | |

| Delivery and Logistics | ||

| Corporate and SME Fleets | ||

| Others (Government and Institutional, NGO / Development) | ||

| Sales Channel | Online | |

| Offline | ||

| By Country | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Ecuador | ||

| Bolivia | ||

| Paraguay | ||

| Rest of South America | ||

Market Definition

- Vehicle Type - The category covers motorized two-wheelers.

- Vehicle Body Type - This includes Scooters and Motorcycles, while Kick-scooters and Bicycles are excluded.

- Fuel Category - Coverage extends to vehicles powered by Internal Combustion Engines (ICE) and electric propulsion systems.

| Keyword | Definition |

|---|---|

| Electric Vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| BEV | A BEV relies completely on a battery and a motor for propulsion. The battery in the vehicle must be charged by plugging it into an outlet or public charging station. BEVs do not have an ICE and hence are pollution-free. They have a low cost of operation and reduced engine noise as compared to conventional fuel engines. However, they have a shorter range and higher prices than their equivalent gasoline models. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all-electric vehicles as well as plug-in hybrids. |

| Plug-in Hybrid EV | A vehicle that can be powered either by an ICE or an electric motor. In contrast to normal hybrid EVs, they can be charged externally. |

| Internal combustion engine | An engine in which the burning of fuels occurs in a confined space called a combustion chamber. Usually run with gasoline/petrol or diesel. |

| Hybrid EV | A vehicle powered by an ICE in combination with one or more electric motors that use energy stored in batteries. These are continually recharged with power from the ICE and regenerative braking. |

| Commercial Vehicles | Commercial vehicles are motorized road vehicles designed for transporting people or goods. The category includes light commercial vehicles (LCVs) and medium and heavy-duty vehicles (M&HCV). |

| Passenger Vehicles | Passenger cars are electric motor– or engine-driven vehicles with at least four wheels. These vehicles are used for the transport of passengers and comprise no more than eight seats in addition to the driver’s seat. |

| Light Commercial Vehicles | Commercial vehicles that weigh less than 6,000 lb (Class 1) and in the range of 6,001–10,000 lb (Class 2) are covered under this category. |

| M&HDT | Commercial vehicles that weigh in the range of 10,001–14,000 lb (Class 3), 14,001–16,000 lb (Class 4), 16,001–19,500 lb (Class 5), 19,501–26,000 lb (Class 6), 26,001–33,000 lb (Class 7) and above 33,001 lb (Class 8) are covered under this category. |

| Bus | A mode of transportation that typically refers to a large vehicle designed to carry passengers over long distances. This includes transit bus, school bus, shuttle bus, and trolleybuses. |

| Diesel | It includes vehicles that use diesel as their primary fuel. A diesel engine vehicle have a compression-ignited injection system rather than the spark-ignited system used by most gasoline vehicles. In such vehicles, fuel is injected into the combustion chamber and ignited by the high temperature achieved when gas is greatly compressed. |

| Gasoline | It includes vehicles that use gas/petrol as their primary fuel. A gasoline car typically uses a spark-ignited internal combustion engine. In such vehicles, fuel is injected into either the intake manifold or the combustion chamber, where it is combined with air, and the air/fuel mixture is ignited by the spark from a spark plug. |

| LPG | It includes vehicles that use LPG as their primary fuel. Both dedicated and bi-fuel LPG vehicles are considered under the scope of the study. |

| CNG | It includes vehicles that use CNG as their primary fuel. These are vehicles that operate like gasoline-powered vehicles with spark-ignited internal combustion engines. |

| HEV | All the electric vehicles that use batteries and an internal combustion engine (ICE) as their primary source for propulsion are considered under this category. HEVs generally use a diesel-electric powertrain and are also known as hybrid diesel-electric vehicles. An HEV converts the vehicle momentum (kinetic energy) into electricity that recharges the battery when the vehicle slows down or stops. The battery of HEV cannot be charged using plug-in devices. |

| PHEV | PHEVs are powered by a battery as well as an ICE. The battery can be charged through either regenerative breaking using the ICE or by plugging into some external charging source. PHEVs have a better range than BEVs but are comparatively less eco-friendly. |

| Hatchback | These are compact-sized cars with a hatch-type door provided at the rear end. |

| Sedan | These are usually two- or four-door passenger cars, with a separate area provided at the rear end for luggage. |

| SUV | Popularly known as SUVs, these cars come with four-wheel drive, and usually have high ground clearance. These cars can also be used as off-road vehicles. |

| MPV | These are multi-purpose vehicles (also called minivans) designed to carry a larger number of passengers. They carry between five and seven people and have room for luggage too. They are usually taller than the average family saloon car, to provide greater headroom and ease of access, and they are usually front-wheel drive. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the sales volume with their respective average selling price (ASP). While estimating ASP factors like average inflation, market demand shift, manufacturing cost, technological advancement, and varying consumer preference, among others have been taken into account.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.