Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

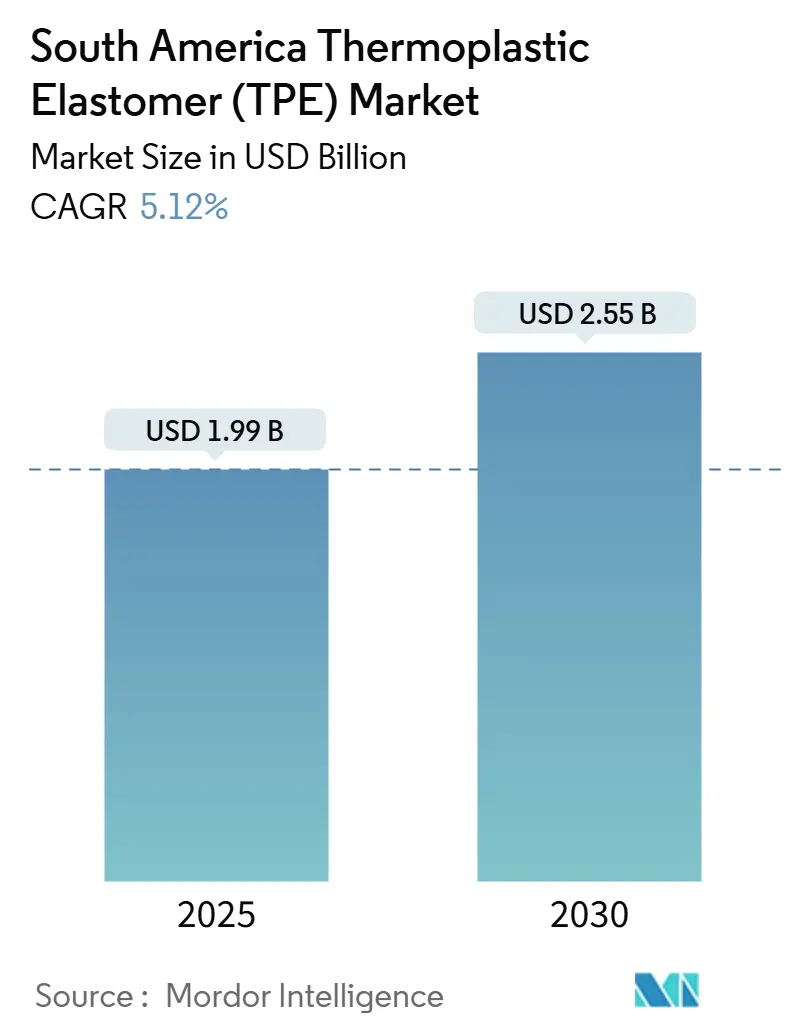

| Market Size (2025) | USD 1.99 Billion |

| Market Size (2030) | USD 2.55 Billion |

| Growth Rate (2025 - 2030) | 5.12% CAGR |

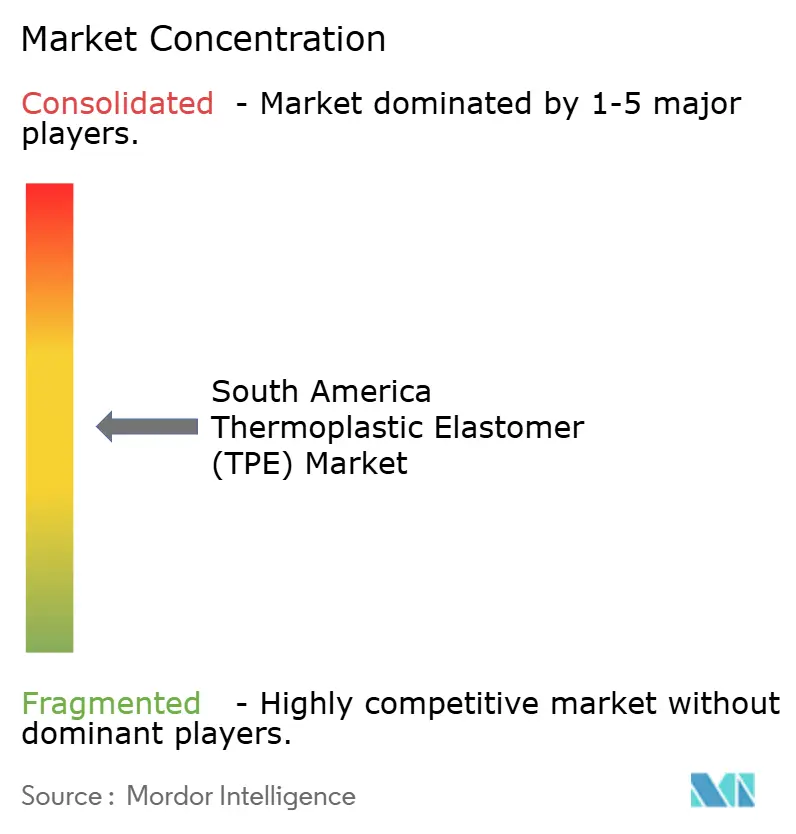

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Thermoplastic Elastomer (TPE) Market Analysis by Mordor Intelligence

The South America thermoplastic elastomer (TPE) market size is estimated at USD 1.99 billion in 2025, and is expected to reach USD 2.55 billion by 2030, at a CAGR of 5.12% during the forecast period (2025-2030). The rapid adoption of electric-vehicle platforms, multi-year infrastructure programs, and the reshoring of medical-device manufacturing are expanding demand for elastomers that combine rubber-like flexibility with thermoplastic recyclability. Brazil’s Mover incentive program is stimulating procurement of halogen-free wire jackets, lightweight door seals, and soft-touch interior parts, while Argentina’s USD 452 billion infrastructure pipeline is steering specifiers toward weather-resistant thermoplastic vulcanizates for bridge expansion joints and window gaskets. Accelerated data-center construction and 5G installations are amplifying pull for flame-retardant cable jacketing, and post-consumer-recycled content grades are gaining traction as brand owners pursue circularity targets. Competitive intensity remains moderate because global majors supply base resins and regional toll-compounders customize hardness, adhesion, and flame performance to OEM specifications.

Key Report Takeaways

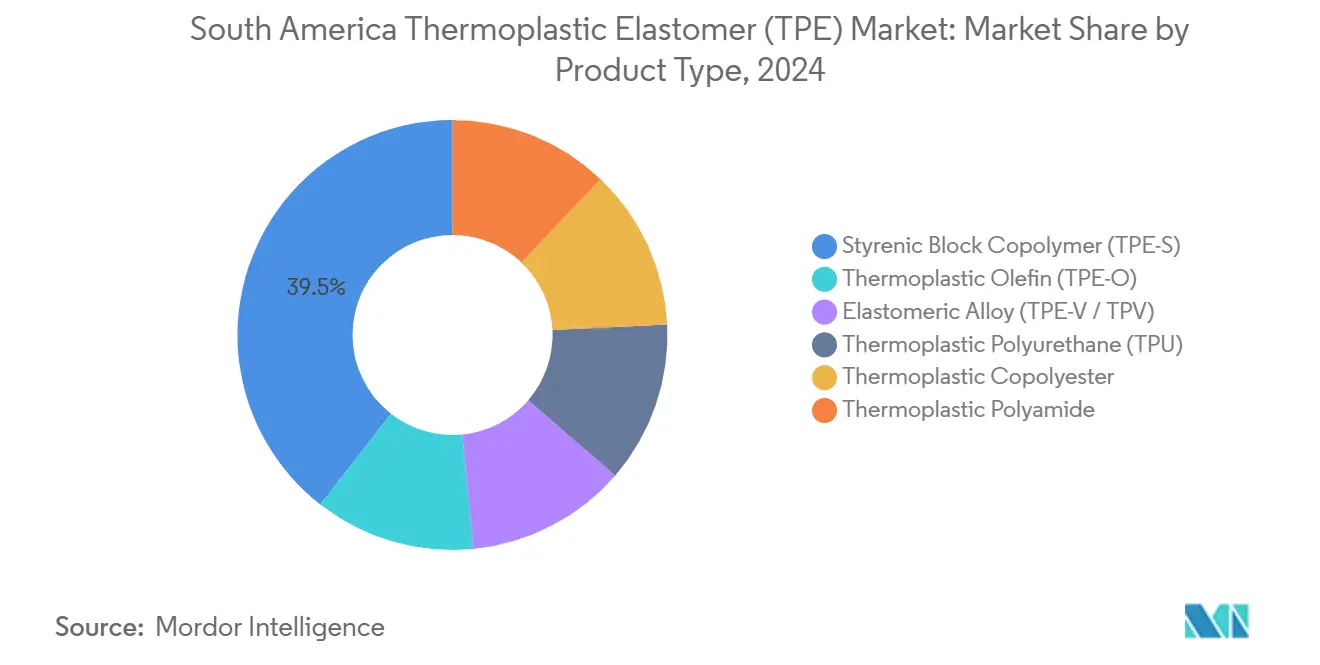

- By product type, styrenic block copolymers led the South American thermoplastic elastomer market with a 39.46% share in 2024, and thermoplastic polyurethane is forecast to expand at a 5.78% CAGR through 2030.

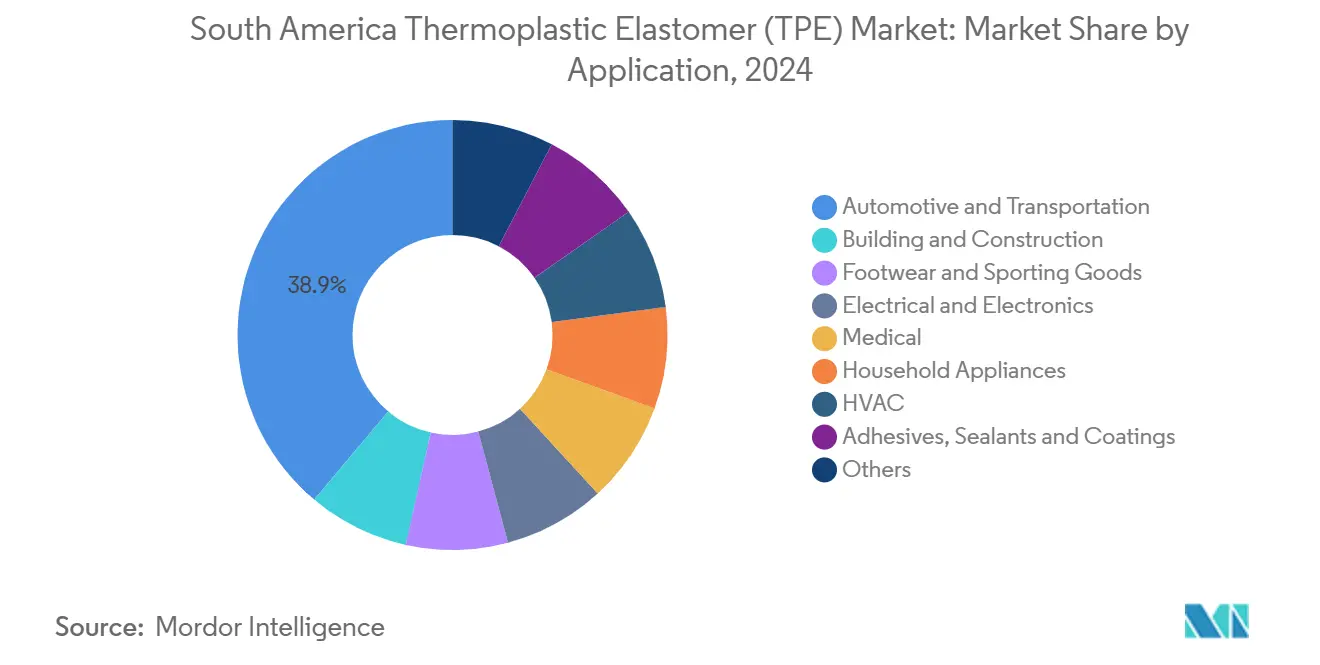

- By application, automotive and transportation accounted for 38.88% of the South America thermoplastic elastomer market size in 2024, while electrical and electronics is advancing at a 5.92% CAGR to 2030.

- By geography, Brazil captured 72.22% of 2024 revenue, while it is projected to post a 6.02% CAGR through 2030.

South America Thermoplastic Elastomer (TPE) Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive lightweighting and EV production surge | +1.3% | Brazil (São Paulo, Minas Gerais), Argentina (Córdoba) | Medium term (2–4 years) |

| Infrastructure rehabilitation and green public works spend | +0.9% | Brazil (national PAC program), Argentina (IDB-financed corridors), Chile (mining-region roads) | Long term (≥ 4 years) |

| Accelerated medical-device manufacturing and reshoring | +0.7% | Brazil (ANVISA-regulated hubs), Argentina (Buenos Aires pharma cluster) | Short term (≤ 2 years) |

| Footwear sector's pivot to bio-based TPE soles | +0.5% | Brazil (Rio Grande do Sul, Ceará footwear clusters) | Medium term (2–4 years) |

| Mining and energy uptake of abrasion-resistant TPE parts | +0.6% | Chile (copper belt), Brazil (iron-ore Minas Gerais), Peru (gold/copper regions) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Automotive Lightweighting and EV Production Surge

Stellantis, Volkswagen, and General Motors committed more than USD 22 billion in hybrid and battery-electric projects under Brazil’s Mover incentive scheme, prompting widespread substitution of EPDM with thermoplastic vulcanizates that deliver 30% weight savings and 40% faster cycle times. Halogen-free thermoplastic polyurethane now dominates high-voltage cable jackets because Lubrizol’s Estane grades meet IEC 62893 flammability and withstand continuous 125 °C exposure. Argentina’s EV registrations increased sharply between 2022 and 2023 as charging corridors expanded in Buenos Aires and Córdoba. Yet regional suppliers still lack in-line degassing and low-VOC compounding, forcing importation of pre-colored pellets and lengthening lead times to as much as 12 weeks.

Infrastructure Rehabilitation and Green Public Works Spend

Argentina secured USD 1 billion from the Inter-American Development Bank for the Paraná River bridge and USD 816 million from China Machinery Engineering Corporation for rail upgrades, anchoring a USD 452 billion public-works roadmap through 2040. Provincial tenders specify thermoplastic-olefin combinations that resist ozone cracking and remain elastic below –20 °C. Grades with 9–35% post-consumer recycled content now meet the ASTM C1401 adhesion standard and help contractors earn green-building credits. Long payback horizons mean specifiers favor premium copolyester and polyamide elastomers that resist hydrolysis in coastal humidity, even when acquisition costs are higher.

Accelerated Medical-Device Manufacturing and Reshoring

Brazil’s ANVISA traceability rules and MERCOSUR GMC 28-2024 positive lists push multinationals to source ISO 10993-compliant elastomers locally. KRAIBURG’s Thermolast M series has cleared cytotoxicity and irritation tests, enabling the production of syringe plungers and breathing-circuit connectors in São Paulo and Buenos Aires. Peru enacted limits for nitrosamines and bisphenol-A in baby articles in 2024, sparking reformulation with phthalate-free styrenic elastomers that already meet FDA indirect food-contact rules. Container rates on Asia-to-South America lanes surged 40% in early 2024, strengthening the case for domestic compounding of medium-volume runs.

Footwear Sector Pivot to Bio-Based TPE Soles

Brazilian shoe clusters in Rio Grande do Sul and Ceará manufacture more than 900 million pairs of shoes annually, and premium brands are transitioning to bio-attributed thermoplastic polyurethanes containing castor-oil polyols to reduce their carbon footprints by 20–30%. Huntsman’s Avalon Gecko line delivers Shore A 85–95 hardness without sacrificing rebound, while Braskem’s ethanol-to-ethylene route supplies bio-attributed EVA for lightweight midsoles. Certification under ISCC PLUS elevates auditing costs, which smaller manufacturers struggle to absorb, so conventional SBS still dominates value-tier footwear where 10–15% cost premiums for renewables are prohibitive.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile styrene and petro-feedstock pricing | -0.8% | Brazil (São Paulo petrochemical corridor), Argentina (Bahía Blanca complex) | Short term (≤ 2 years) |

| Limited regional compounding/masterbatch capacity | -0.5% | Argentina, Chile, Colombia, Peru (reliance on imports) | Medium term (2–4 years) |

| Tightening Phthalate and VOC regulations | -0.3% | Brazil (ANVISA jurisdiction), MERCOSUR member states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Styrene and Petro-Feedstock Pricing

Brazilian crackers ran at 60% utilization in 2024, and natural-gas prices near USD 15 per million Btu inflated ethylene and propylene costs, pushing styrene spot quotes between USD 1,100 and USD 1,450 per ton during unplanned outages at Braskem’s Triunfo complex. Argentina’s Bahía Blanca hub suffered storm damage in 2023, and although feedstock output rebounded 37.1% in December 2024, downstream plastics demand fell 5.1%[1]INDEC, “Industrial Production Index December 2024,” indec.gob.ar. Compounders now carry up to 90 days of inventory, and quarterly surcharges erode the cost advantage that thermoplastic elastomers hold over thermoset rubber. Brazil’s Presiq program, valued at R$4.0 billion per year starting in 2027, aims to stabilize raw material prices, but its execution hinges on congressional budget approvals.

Limited Regional Compounding and Masterbatch Capacity

Cromex operates the region’s largest masterbatch network; however, its specialty thermoplastic-elastomer compounding capacity remains below 150 kilotons per year, equivalent to less than 8% of consumption. Argentina, Chile, Colombia, and Peru lack twin-screw lines that can disperse flame retardants or conductive fillers above 15%. Consequently, OEMs import pre-compounded pellets from Asia or North America, which have a 10–14-week delivery time. Minimum order quantities of 20 tons deter small buyers. Braskem polymerizes polyethylene and polypropylene but not styrenic block copolymers or thermoplastic polyurethane, leaving these base resins almost entirely imported.

Segment Analysis

By Product Type: Styrenic Dominance Meets Polyurethane Momentum

Styrenic block copolymers generated 39.46% of 2024 revenue, delivering transparency, a soft-touch feel, and adhesion to polypropylene for footwear soles and consumer overmolding applications. Their density below 1.0 g/cm³ supports automakers’ mass-reduction strategies, while the segment also underpins the use of hot-melt adhesives by packaging converters. Thermoplastic olefins are used in exterior trim and under-hood air-duct applications because they resist chemicals and ultraviolet exposure. Elastomeric alloys, such as thermoplastic vulcanizates, are displacing EPDM door seals, reducing vehicle weight by 30% and compressing assembly cycles. Copolyester and polyamide elastomers withstand continuous service at 130 °C in exhaust hangers and transmission mounts, justifying premium pricing in powertrain components.

Thermoplastic polyurethane will post the fastest 5.78% CAGR through 2030, fueled by mining conversions where TPU replaces cast polyurethane in slurry pumps, raising service life by 20–50% and cutting downtime. Halogen-free polyether-based TPU also anchors high-voltage EV cable jackets that must withstand continuous duty at 125 °C and cold starts at –40°C. Bio-attributed TPU derived from castor oil polyols enables footwear brands to claim up to 30% renewable content without compromising Shore A hardness or rebound[2]Technical brochure, “Avalon Gecko Bio-TPU,” Huntsman, huntsman.com . Raw-material pressure remains a concern because Middle Eastern polyol suppliers diverted capacity to specialty chemicals, lifting polyol prices 12–18% in 2024.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Automotive Leads, Electronics Accelerates

Automotive and transportation accounted for 38.88% of 2024 revenue, following the assembly of nearly 2.8 million vehicles in Brazil and Argentina. This was achieved through the use of rubber-replacement thermoplastic elastomers in door seals, instrument panel skin, and wire harnesses. OEM sustainability goals align with recyclable elastomers, and single-step injection molding reduces takt time on high-volume assembly lines. Building and construction ranks second, supported by Argentina’s USD 452 billion pipeline, which specifies thermoplastic-olefin bridge bearings that stay elastic below –20 °C. Footwear clusters produce more than 900 million pairs a year, integrating styrenic soles with bio-attributed EVA midsoles. Medical uptake is accelerating as KRAIBURG’s Thermolast M clears ISO 10993 testing for syringe plungers and insulin-pen grips.

The electrical and electronics sector is projected to grow at a 5.92% CAGR, making it the fastest-expanding end-use. Data centers and 5G base stations require low-smoke, zero-halogen cable jackets that utilize polyether TPU and thermoplastic polyamide elastomers, capable of continuous service at 125 °C. Connector boots require a Shore A hardness of 60–80, plus adhesion to polycarbonate, which can be satisfied without primers by thermoplastic polyamide elastomers. Household appliances adopt grades with 35–48% post-consumer recycled content to meet corporate circularity metrics. HVAC ducting specifies low-VOC thermoplastic vulcanizates that maintain compression set below 25% after 1,000-hour aging.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Brazil accounted for 72.22% share of the South America TPE market i 2024 revenue and is forecast to advance at 6.02% CAGR through 2030, buoyed by Braskem’s 9.3-million-ton resin capacity and the USD 800 million Mover automotive program. Construction spending reached USD 128 billion in 2024, and federal tenders are increasingly mandating recycled-content materials. Braskem’s 86-kiloton PCR line enables thermoplastic elastomer grades with 35–48% recycled content, validated for ANVISA food-contact applications. Iron-ore mines in Minas Gerais and offshore oil platforms consume abrasion-resistant TPU for pumps and gaskets. However, natural-gas prices, which are four times the U.S. benchmarks, constrain cracker utilization and margin expansion.

Argentina ranks second, boasting a USD 632.6 billion economy that is heavily integrated into petrochemicals, automotive, and pharmaceutical sectors. The government secured USD 1 billion in IDB financing for the Paraná River bridge and USD 816 million in Chinese funding for rail improvements, part of a USD 452 billion public works plan. Less than 35% of highways are paved, boosting demand for thermoplastic-olefin expansion joints. EV registrations climbed 66% from 2022 to 2023 as Buenos Aires and Córdoba built charging corridors ILO.ORG. The Vaca Muerta pipeline improved ethane supply to Bahía Blanca, but downstream plastics output shrank 5.1% in late 2024 due to fragile construction demand.

The rest of South America—Chile, Colombia, Peru, and smaller economies—makes up the balance. Chilean copper projects specify hydrolysis-resistant polyester TPU seals exposed to acidic process water, while Peru’s mining investment surpasses USD 3.3 billion and drives demand for injection-molded elastomer parts in slurry pipelines. Colombian consumer-goods plants adopt styrenic elastomers in soft-touch grips, yet all three nations depend on imported compounded pellets with lead times up to 14 weeks. Divergent regulatory frameworks complicate multi-country product launches even though MERCOSUR and Pacific Alliance agreements waive most tariffs.

Competitive Landscape

The South America thermoplastic elastomer market is moderately fragmented. Global producers such as BASF supply base resins, while regional toll-compounders customize flame retardancy, adhesion, and hardness profiles. Sustainability dominates strategies. White-space opportunities cluster around advanced recycling. Process automation is another lever: injection cells with real-time rheology sensors and automated hardness testers reduce scrap rates below 2%, a critical gain for high-value medical grades. ISO 13485 and ISO 10993 certifications remain concentrated in São Paulo and Buenos Aires, raising entry barriers.

South America Thermoplastic Elastomer (TPE) Industry Leaders

-

KRATON CORPORATION

-

BASF

-

Dynasol Group

-

LG Chem

-

Avient Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Braskem chartered a gas transporter to secure ethane from Bolivia’s Vaca Muerta pipeline, lowering feedstock costs for its Triunfo cracker and supporting EVA and thermoplastic-olefin production.

- June 2024: Teknor Apex introduced Monprene S3 CP-15170 BLK, a 35% sustainable-content thermoplastic elastomer for injection-molded electronics grips.

South America Thermoplastic Elastomer (TPE) Market Report Scope

Thermoplastic elastomers (TPEs) are elastic materials that exhibit elasticity similar to cross-linked rubber, and they find their major applications in end-user industries, such as construction, automotive, and electronics. It is mainly produced from mechanical blending and dynamically vulcanized blending.

The South America thermoplastic elastomer (TPE) market is segmented by product type, application, and geography. By product type, the market is segmented into styrenic block copolymer, thermoplastic olefin, elastomeric alloy, thermoplastic polyurethane, thermoplastic copolyester, and thermoplastic polyamide. By application, the market is segmented into automotive and transportation, building and construction, footwear and sporting goods, electrical and electronics, medical, household appliances, HVAC, adhesives, sealants, and coatings, and other applications. By geography, the market is segmented into Brazil, Argentina, and the Rest of South America. For each segment, market sizing and forecasts have been conducted based on revenue (USD billion).

By Product Type

| Styrenic Block Copolymer (TPE-S) |

| Thermoplastic Olefin (TPE-O) |

| Elastomeric Alloy (TPE-V / TPV) |

| Thermoplastic Polyurethane (TPU) |

| Thermoplastic Copolyester |

| Thermoplastic Polyamide |

By Application

| Automotive and Transportation |

| Building and Construction |

| Footwear and Sporting Goods |

| Electrical and Electronics |

| Medical |

| Household Appliances |

| HVAC |

| Adhesives, Sealants and Coatings |

| Others |

By Geography

| Brazil |

| Argentina |

| Rest of South America |

| By Product Type | Styrenic Block Copolymer (TPE-S) |

| Thermoplastic Olefin (TPE-O) | |

| Elastomeric Alloy (TPE-V / TPV) | |

| Thermoplastic Polyurethane (TPU) | |

| Thermoplastic Copolyester | |

| Thermoplastic Polyamide | |

| By Application | Automotive and Transportation |

| Building and Construction | |

| Footwear and Sporting Goods | |

| Electrical and Electronics | |

| Medical | |

| Household Appliances | |

| HVAC | |

| Adhesives, Sealants and Coatings | |

| Others | |

| By Geography | Brazil |

| Argentina | |

| Rest of South America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What revenue level are South America’s thermoplastic-elastomer suppliers expected to reach by 2030?

Sales are projected to climb to USD 2.55 billion, reflecting a 5.12% CAGR over 2025-2030.

Which product family is set to register the fastest expansion in the region?

Thermoplastic polyurethane is forecast to post the quickest pace, advancing at a 5.78% CAGR through 2030.

How dominant is Brazil within regional demand?

Brazil generated 72.22% of 2024 revenue and is on track for a 6.02% CAGR, helped by automotive incentives and local resin capacity.

Which end-use is adding volume the most rapidly?

Electrical and electronics applications are expected to log a 5.92% CAGR thanks to data-center and 5G build-outs.

What sustainability factor is shaping procurement choices?

Grades formulated with 35–48% post-consumer recycled content are winning share as brand owners pursue circularity goals.

How are feedstock price swings influencing local processors?

Producers are carrying up to 90 days of styrene-based inventory and applying quarterly surcharges to offset raw-material volatility.

Page last updated on: