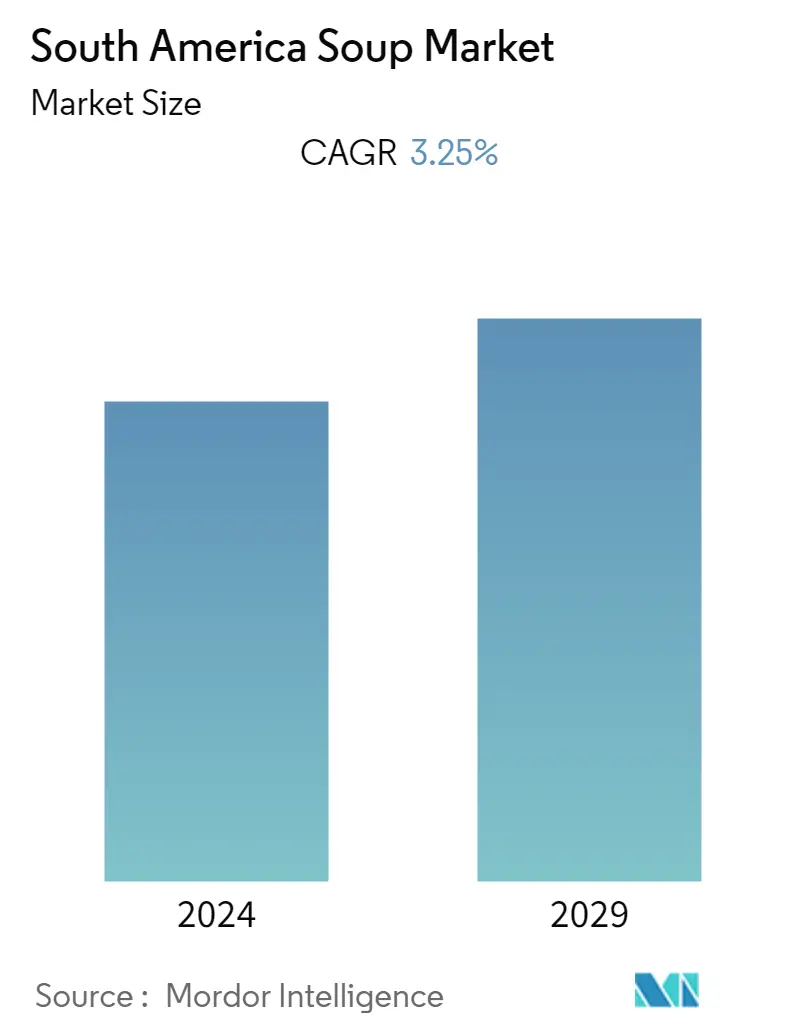

Market Size of South America Soup Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2019 - 2022 |

| CAGR | 3.25 % |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

South America Soup Market Analysis

The South America soup market is forecasted to witness a CAGR of 3.25% during the forecast period (2020 - 2025).

- Several factors are contributing to the rise in demand for soup in South America, including rapid urbanization, busy lifestyles, and a substantial rise in the demand for packaged and ready-to-eat food products.

- Moroever, factors such as minimal effort for the preparation and consumption of packaged soups, the increase in awareness of the health benefits in soup consumption to the overall health and new product launches is ensuring that sales of the soup is increasing in the market studied.

- One of the restraints, which is exptected to hamper the sales of South America soup market is that these South Amerian countries have an ineffecient supply chain management, as chilled soups require an efficient cold chain supply and timely delivery. This increases the cost and reduces demand.

- One of the other factor, which is hindering the growth of the market is that in light of the economic crisis in the region, for an instance, Argentinians are opting to create homemade soup rather than buying packaged soup in independent small grocers and hypermarkets. The reason for this is financial crises, and homemade soups are significantly cheaper.

South America Soup Industry Segmentation

The South America market study of soup is available by category as vegetarian and non-vegetarian soups, by prouct type as canned/preserved, chilled, dehydrated, frozen, instant, and UHT. By packaging, the market is segmented into canned, pouched and other packaging. By distribution channel, the market is segmented as supermarkets/hypermarkets, convenience stores, online, and other distribution channels.

| By Category | |

| Vegetarian Soup | |

| Non-Vegetarian Soup |

| By Type | |

| Canned/Preserved soup | |

| Chilled soup | |

| Dehydrated soup | |

| Frozen soup | |

| Instant soup | |

| UHT soup |

| By Packaging | |

| Canned | |

| Pouched | |

| Other Packagin |

| By Distribution Channel | |

| Supermarkets/Hypermarkets | |

| Convenience Stores | |

| Online Retail | |

| Others |

| By Geography | |

| Brazil | |

| Argentina | |

| Colombia | |

| Rest of South America |

South America Soup Market Size Summary

The South America soup market is experiencing a steady growth trajectory, driven by factors such as rapid urbanization and the increasing demand for convenient, ready-to-eat food products. The market is characterized by a growing awareness of the health benefits associated with soup consumption, which is further bolstered by new product launches. However, challenges such as inefficient supply chain management, particularly for chilled soups, and economic constraints in the region are hindering market expansion. These issues have led to a preference for homemade soups over packaged options in some areas, as consumers seek more cost-effective solutions during economic downturns.

Despite these challenges, the market remains competitive, with major players like Nestle SA, Unilever, and CSC BRANDS, L.P. actively innovating to capture consumer interest. The trend towards health and wellness has prompted companies to introduce products with natural ingredients and no preservatives, catering to the demand for 'free from' packaged foods. The introduction of shelf-stable soups and a diverse range of flavors, including reduced salt and fat options, reflects the industry's response to changing consumer preferences. As urban lifestyles continue to evolve, ready-to-cook and instant soups are becoming essential in South American kitchens, offering convenience and taste that appeal to a broad audience.

South America Soup Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Drivers

-

1.2 Market Restraints

-

1.3 Porter's Five Forces Analysis

-

1.3.1 Threat of New Entrants

-

1.3.2 Bargaining Power of Buyers/Consumers

-

1.3.3 Bargaining Power of Suppliers

-

1.3.4 Threat of Substitute Products

-

1.3.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 By Category

-

2.1.1 Vegetarian Soup

-

2.1.2 Non-Vegetarian Soup

-

-

2.2 By Type

-

2.2.1 Canned/Preserved soup

-

2.2.2 Chilled soup

-

2.2.3 Dehydrated soup

-

2.2.4 Frozen soup

-

2.2.5 Instant soup

-

2.2.6 UHT soup

-

-

2.3 By Packaging

-

2.3.1 Canned

-

2.3.2 Pouched

-

2.3.3 Other Packagin

-

-

2.4 By Distribution Channel

-

2.4.1 Supermarkets/Hypermarkets

-

2.4.2 Convenience Stores

-

2.4.3 Online Retail

-

2.4.4 Others

-

-

2.5 By Geography

-

2.5.1 Brazil

-

2.5.2 Argentina

-

2.5.3 Colombia

-

2.5.4 Rest of South America

-

-

South America Soup Market Size FAQs

What is the current South America Soup Market size?

The South America Soup Market is projected to register a CAGR of 3.25% during the forecast period (2024-2029)

Who are the key players in South America Soup Market?

Nestle SA, Unilever, AJINOMOTO CO., INC., Quala and CSC BRANDS, L.P. are the major companies operating in the South America Soup Market.