South America Polyvinyl Chloride (PVC) Market Size

| Study Period | 2019 - 2029 |

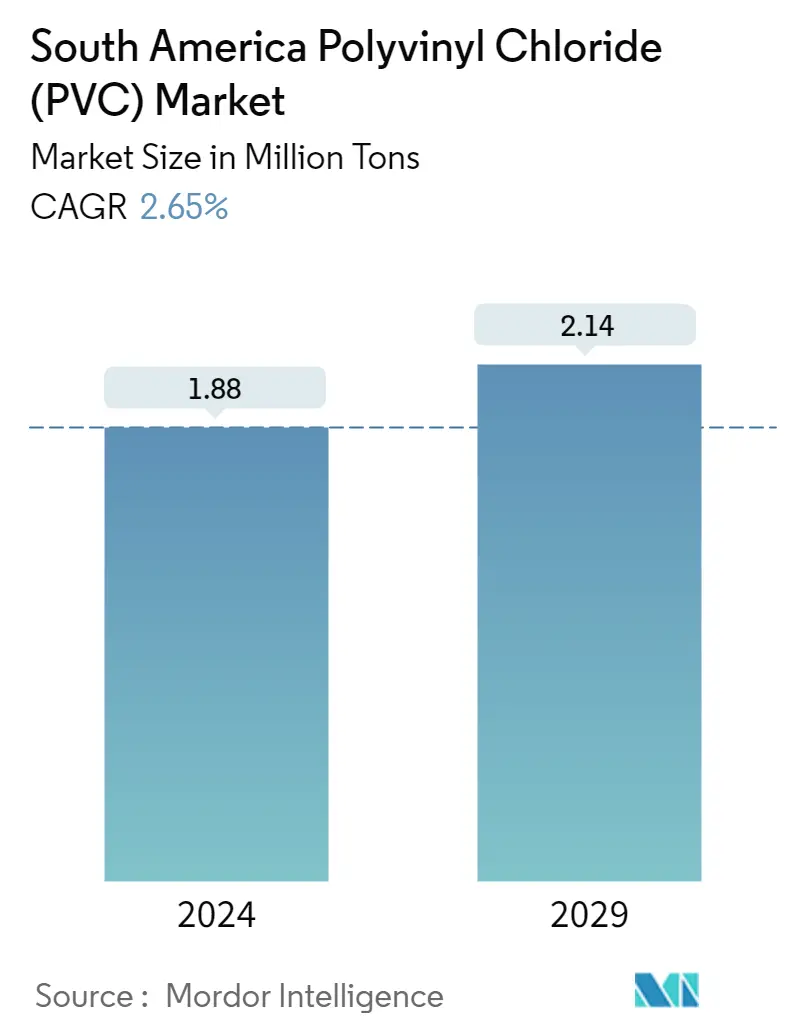

| Market Volume (2024) | 1.88 Million tons |

| Market Volume (2029) | 2.14 Million tons |

| CAGR (2024 - 2029) | 2.65 % |

| Fastest Growing Market | South America |

| Largest Market | South America |

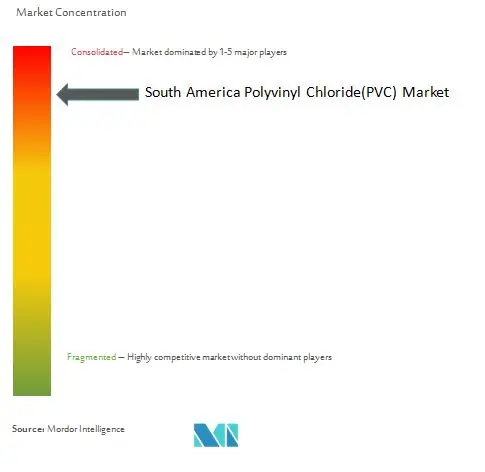

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

South America Polyvinyl Chloride (PVC) Market Analysis

The South America Polyvinyl Chloride Market size is estimated at 1.88 Million tons in 2024, and is expected to reach 2.14 Million tons by 2029, growing at a CAGR of 2.65% during the forecast period (2024-2029).

PVC is strong and lightweight, durable to weathering, rotting, chemical corrosion and abrasion, versatile, and easy to use, as it can be cut, shaped, welded, and joined in any style.

- Major factors driving the market studied are the increasing use of plastics to reduce vehicle weight and enhance fuel economy, growing demand from the construction industry, and increasing applications in the healthcare industry

- However, hazardous impacts on humans and the environment are expected to majorly hinder the growth of the market studied.

- The accelerating usage of electric vehicles and PVC recycling are likely to act as an opportunity in the future.

South America Polyvinyl Chloride (PVC) Market Trends

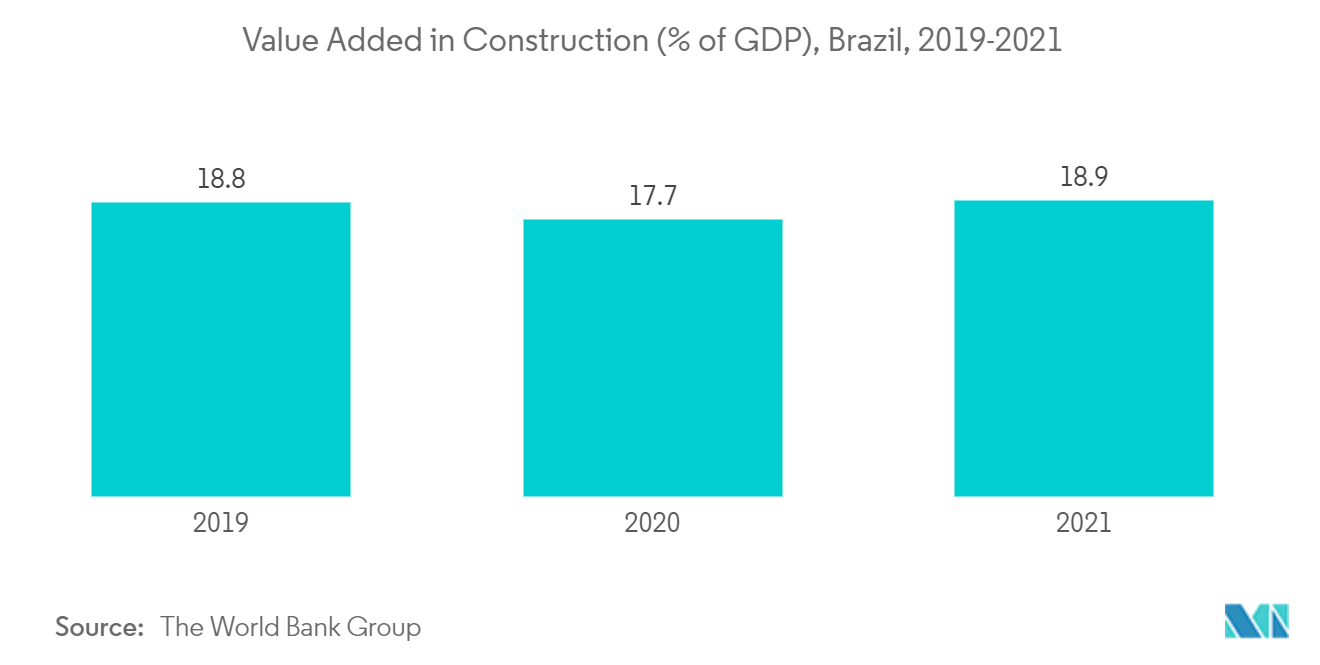

Growing Demand from the Construction Industry

- PVC pipes have been used in building and construction for over 60 years, as they offer valuable energy savings during production, low-cost distribution, and a safe, maintenance-free lifetime of service. These pipes are widely used for pipeline systems for water, waste, and drainage as they suffer no build-up, scaling, corrosion, or pitting, and they provide smooth surfaces reducing energy requirements for pumping.

- In Q2 2022, the region's total hospitality construction pipeline includes 555 projects and 90,496 rooms. Following nearly two years of uncertainty caused by the pandemic, the Latin American hotel industry is finally showing signs of recovery. Consumer confidence has risen as border restrictions and quarantine requirements across the region have been relaxed.

- In South America, 40 projects totaling 8,481 rooms began construction in the first half of 2022. In Q2 2022, new project announcements increased 57% year-on-year to 36 projects or 6,208 rooms.

- In December 2022, Brazil's polyvinyl chloride (PVC) market was awaiting new policies to be announced by the government in the infrastructure and construction sectors, which will improve the supply chain and business conditions.

- Brazil's infrastructure investment amounted to 148 billion Brazilian reals (USD 27.45 billion) in 2021.

- All the above-mentioned factors are likely to drive the market growth during the forecast period.

Brazil to Dominate the Market

- Brazil dominated the market in South America and is likely to continue its dominance during the forecast period. The country is attributed to the rise in construction, automotive, and electronics industries.

- The government of Brazil launched the 'Infrastructure Concessions Program' to invest in infrastructure for roads, airports, ports, and energy, in the country. In this program, the government announced an investment of USD 14.4 billion in transport, energy, and sanitation projects.

- Additionally, the government plans to balance the demand for and supply of affordable housing (created by the increasing population and rapid urbanization) and its efforts to improve the country's aging transport infrastructure using the public-private partnership (PPP) model.

- According to a News Blog, Gateway to South America, Brazil's business confidence indicator (ICEI) in the construction industry improved in the first five months of 2022, rising to 56.2 in May 2022 from 55.5 in April and 55.3 in March 2022.

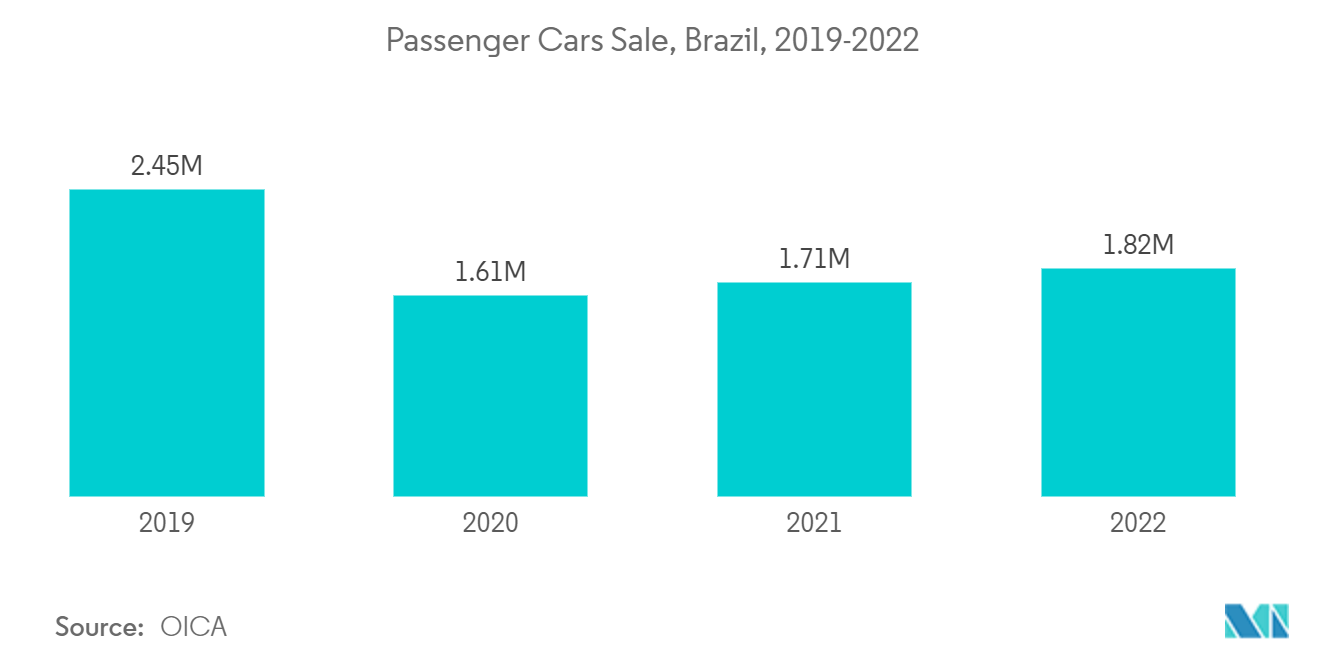

- Brazil has a high demand for vehicles and is considered among the ten leading passenger vehicle manufacturers across the world. According to the International Organization of Motor Vehicle Manufacturers (French: Organisation Internationale des Constructeurs d'Automobiles (OICA)), Brazil's passenger cars sale was 18,24,833 in 2022.

- Sales of consumer electronics appear to have reached a point of saturation in the country. Consumers are careful while buying expensive products, and this behavior is expected to continue in the upcoming years.

- All such factors are likely to drive the PVC market growth in Brazil over the forecast period.

South America Polyvinyl Chloride (PVC) Industry Overview

South America's polyvinyl chloride market is consolidated in nature. The top companies have been focusing on providing better materials for various end-user industries. Major manufacturers of South American PVCs are Formosa Plastics Corporation, INEOS, Shin-Etsu Chemical Co., Ltd., Occidental Petroleum Corporation, and Westlake Vinnolit GmbH & Co. KG, among others.

South America Polyvinyl Chloride (PVC) Market Leaders

-

Formosa Plastics Corporation

-

INEOS

-

Shin-Etsu Chemical Co., Ltd.

-

Westlake Vinnolit GmbH & Co. KG

-

Occidental Petroleum Corporation

*Disclaimer: Major Players sorted in no particular order

South America Polyvinyl Chloride (PVC) Market News

- May 2023: The Brazilian government launched the 'Infrastructure Concessions Program' with an aim to invest in infrastructure for roads, airports, ports, and energy, in the country. In this program, the government announced an investment of USD 14.4 billion in transport, energy, and sanitation projects.

- October 2022: INEOS Styrolution launched new polymer modifiers, which increase sustainability, physical properties, and processability styrolution's modifiers help PVC to cope with the increasing effects of climate change by enhancing its heat and UV resistance plus its mechanical property retention.

South America Polyvinyl Chloride (PVC) Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Usage of Plastics to Reduce Vehicle Weight and Enhance Fuel Economy

4.1.2 Increasing Application in the Healthcare Industry

4.1.3 Growth from the Construction Industry

4.2 Restraints

4.2.1 Hazardous Impact on Humans and the Environment

4.2.2 Other Restrainta

4.3 Industry Value-Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Volume)

5.1 Product Type

5.1.1 Rigid PVC

5.1.1.1 Clear Rigid PVC

5.1.1.2 Non-Clear Rigid PVC

5.1.2 Flexible PVC

5.1.2.1 Clear Flexible PVC

5.1.2.2 Non-Clear Flexible PVC

5.1.3 Low-smoke PVC

5.1.4 Chlorinated PVC

5.2 Stabilizer Type

5.2.1 Calcium-based Stabilizers (Ca-Zn Stabilizers)

5.2.2 Lead-based Stabilizers (Pb Stabilizers)

5.2.3 Tin- and Organotin-based Stabilizers (Sn Stabilizers)

5.2.4 Barium-based and Others (Liquid Mixed Metals)

5.3 Application

5.3.1 Pipes and Fittings

5.3.2 Films and Sheets

5.3.3 Wires and Cables

5.3.4 Bottles

5.3.5 Profiles, Hoses and Tubings

5.3.6 Other Applications

5.4 End-User Industry

5.4.1 Building and Construction

5.4.2 Automotive

5.4.3 Electrical and Electronics

5.4.4 Packaging

5.4.5 Footwear

5.4.6 Healthcare

5.4.7 Other End-User Industries

5.5 Geography

5.5.1 Brazil

5.5.2 Argentina

5.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%) Analysis**/ Market Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Braskem

6.4.2 Formosa Plastics Corporation

6.4.3 INEOS

6.4.4 Occidental Petroleum Corporation

6.4.5 Orbia

6.4.6 Shin-Etsu Chemical Co., Ltd.

6.4.7 Westlake Vinnolit GmbH & Co. KG

6.4.8 Xinjiang Zhongtai Chemical Co., Ltd.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Shifting Focus Towards PVC Recycling

7.2 Accelerating Usage of Electric Vehicles (EVs)

South America Polyvinyl Chloride (PVC) Industry Segmentation

Polyvinyl Chloride (PVC) is a strong and lightweight plastic that is easy to use and easily processed to any shape and processed. The PVC material is highly durable against weather, rotting, chemical corrosion, and abrasion.

The South American PVC market is segmented by product type, stabilizer type, application, and end-user industry. By product type, the market is segmented into rigid type, flexible type, low smoke PVC, and chlorinated PVC. By stabilizer type, the market is segmented into calcium-based stabilizers, lead-based stabilizers, tin- and organotin-based stabilizers (SN stabilizers), barium-based, and others (liquid mixed metals). By application, the market is segmented into pipes and fittings, films and sheets, wires and cables, bottles, profiles, hoses and tubings, and other applications. By end-user industry, the market is segmented into building and construction, automotive, electrical & electronics, packaging, footwear, and healthcare, and other end-user industries. The report also covers the market size and forecasts for the South American PVC market across major countries.

For each segment, the market sizing and forecasts have been done on the basis of volume (kilotons).

| Product Type | ||||

| ||||

| ||||

| Low-smoke PVC | ||||

| Chlorinated PVC |

| Stabilizer Type | |

| Calcium-based Stabilizers (Ca-Zn Stabilizers) | |

| Lead-based Stabilizers (Pb Stabilizers) | |

| Tin- and Organotin-based Stabilizers (Sn Stabilizers) | |

| Barium-based and Others (Liquid Mixed Metals) |

| Application | |

| Pipes and Fittings | |

| Films and Sheets | |

| Wires and Cables | |

| Bottles | |

| Profiles, Hoses and Tubings | |

| Other Applications |

| End-User Industry | |

| Building and Construction | |

| Automotive | |

| Electrical and Electronics | |

| Packaging | |

| Footwear | |

| Healthcare | |

| Other End-User Industries |

| Geography | |

| Brazil | |

| Argentina | |

| Rest of South America |

South America Polyvinyl Chloride (PVC) Market Research FAQs

How big is the South America Polyvinyl Chloride (PVC) Market?

The South America Polyvinyl Chloride (PVC) Market size is expected to reach 1.88 million tons in 2024 and grow at a CAGR of 2.65% to reach 2.14 million tons by 2029.

What is the current South America Polyvinyl Chloride (PVC) Market size?

In 2024, the South America Polyvinyl Chloride (PVC) Market size is expected to reach 1.88 million tons.

Who are the key players in South America Polyvinyl Chloride (PVC) Market?

Formosa Plastics Corporation, INEOS, Shin-Etsu Chemical Co., Ltd., Westlake Vinnolit GmbH & Co. KG and Occidental Petroleum Corporation are the major companies operating in the South America Polyvinyl Chloride (PVC) Market.

Which is the fastest growing region in South America Polyvinyl Chloride (PVC) Market?

South America is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in South America Polyvinyl Chloride (PVC) Market?

In 2024, the South America accounts for the largest market share in South America Polyvinyl Chloride (PVC) Market.

What years does this South America Polyvinyl Chloride (PVC) Market cover, and what was the market size in 2023?

In 2023, the South America Polyvinyl Chloride (PVC) Market size was estimated at 1.83 million tons. The report covers the South America Polyvinyl Chloride (PVC) Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the South America Polyvinyl Chloride (PVC) Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

South America Polyvinyl Chloride (PVC) Industry Report

Statistics for the 2024 South America Polyvinyl Chloride (PVC) market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. South America Polyvinyl Chloride (PVC) analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

South America Polyvinyl Chloride (PVC) Market Report Snapshots