South America Insecticide Market Size and Share

Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

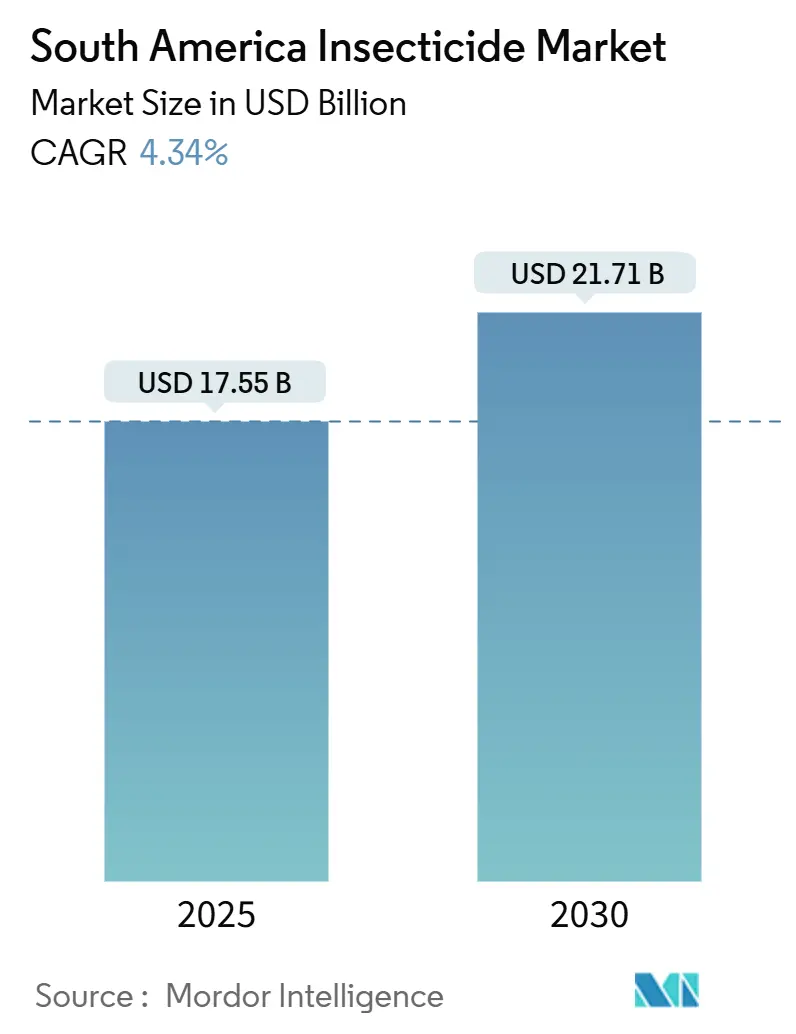

| Market Size (2025) | USD 17.55 Billion |

| Market Size (2030) | USD 21.71 Billion |

| Growth Rate (2025 - 2030) | 4.34% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Insecticide Market Analysis by Mordor Intelligence

The South America insecticides market size stands at USD 17.55 billion in 2025 and is forecast to reach USD 21.71 billion by 2030, advancing at a 4.34% CAGR over the period. Growth is driven by record soybean acreage, mounting insect resistance to legacy chemistries, and wider use of premium novel modes of action. Brazil’s dominance keeps procurement volumes high, while Argentina’s acreage rebound after drought accelerates regional momentum. Multinational suppliers deepen local production to limit currency shocks and logistics risk, even as biological innovators carve niches on residue-sensitive export farms. Digital tools, drones, and integrated pest management (IPM) protocols further expand addressable demand, positioning the South America insecticides market for steady value gains.

Key Report Takeaways

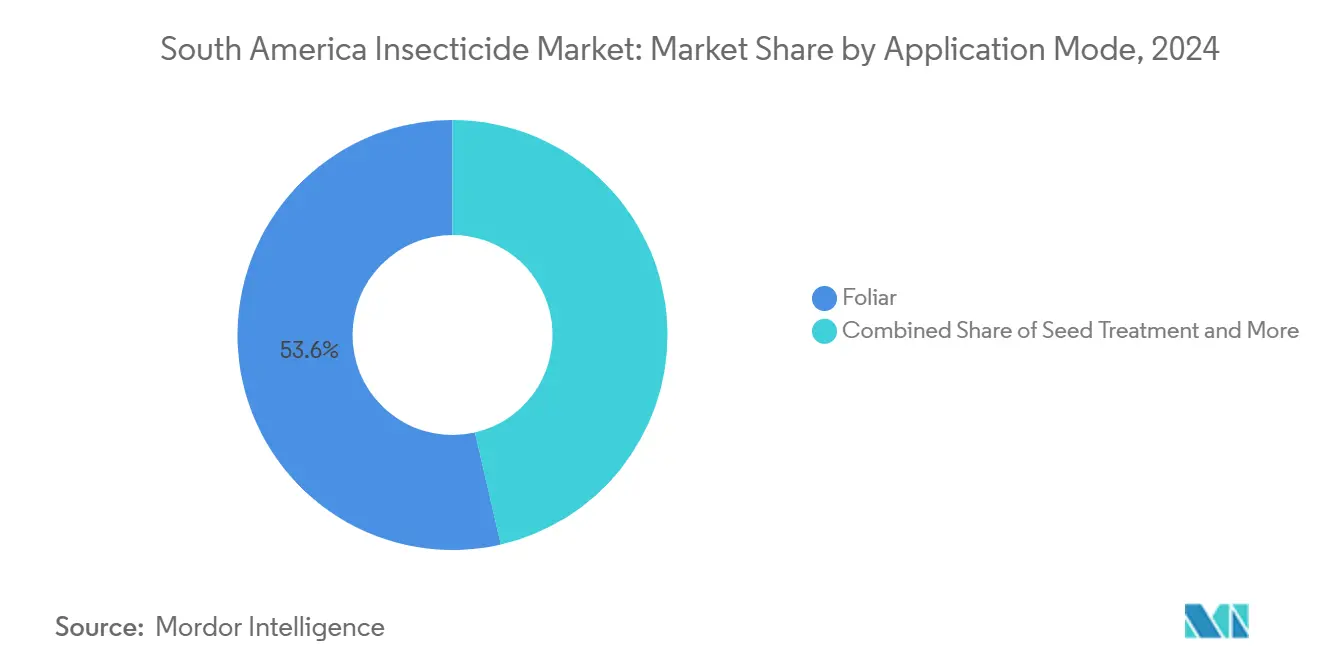

- By mode of application, foliar captured 53.6% of the South America insecticides market share in 2024; seed treatment is advancing at a 4.61% CAGR to 2030.

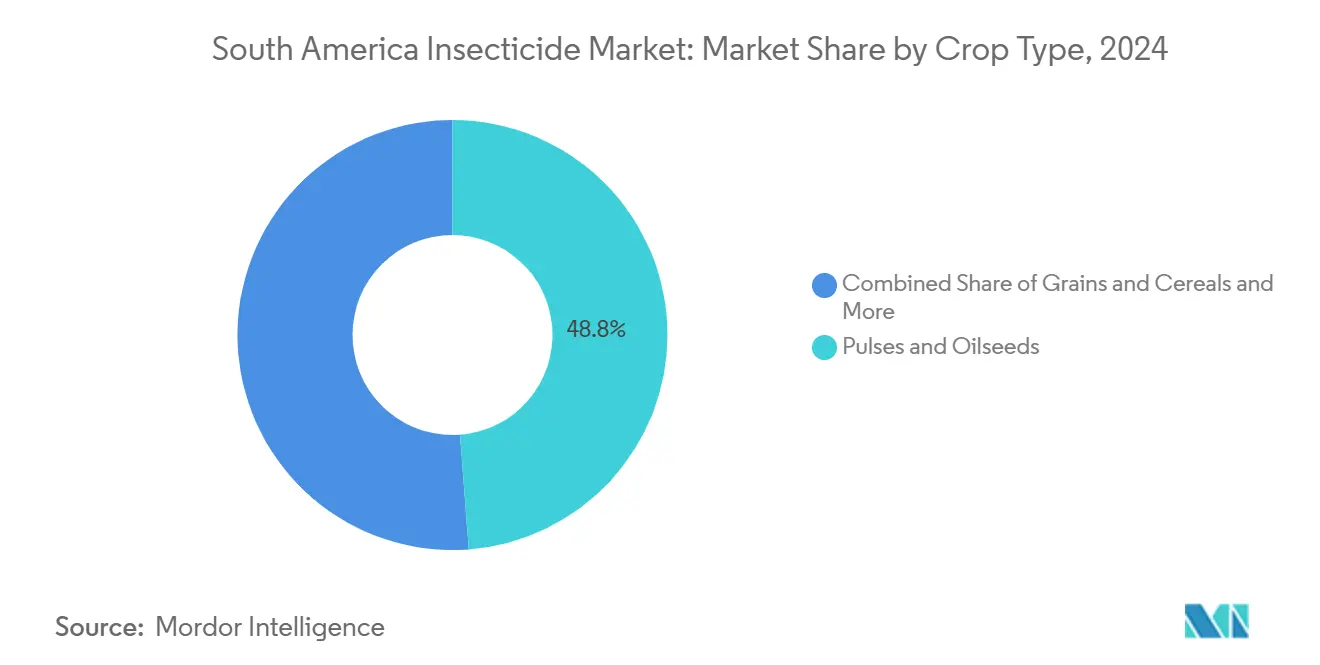

- By crop type, pulses & oilseeds accounted for 48.8% of the South America insecticides market size in 2024 and remain the fastest growing segment with a CAGR of 4.53%.

- In 2024, Brazil dominated the South American insecticides market, holding a 94% share, while Argentina emerged as the fastest-growing segment, projected to grow at a 4.57% CAGR.

South America Insecticide Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of soybean acreage in exporting nations | +0.8% | Brazil, Argentina, Paraguay | Medium term (2-4 years) |

| Rising insect resistance fueling demand for novel modes of action | +1.2% | Brazil, Argentina, Colombia | Long term (≥ 4 years) |

| Growing adoption of integrated pest management programs | +0.6% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Increasing outbreaks of invasive pest species | +0.9% | Brazil, Argentina, Colombia, Peru | Short term (≤ 2 years) |

| Accelerated registration of RNA-i based insecticides | +0.4% | Brazil, Argentina | Long term (≥ 4 years) |

| Rapid deployment of drone-assisted ultra-low-volume spraying | +0.5% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Soybean Acreage in Exporting Nations

Brazil's soybean planted area expanded to 45.2 million hectares in 2024, representing a 3.1% increase from the previous season, while Argentina recovered from drought conditions to plant 16.8 million hectares. [1]Source: USDA Foreign Agricultural Service, “Brazil Soybean Production Outlook 2024-2025,” fas.usda.govThis expansion directly correlates with increased prophylactic insecticide applications, as newly cultivated areas often lack established beneficial insect populations that provide natural pest control. The economic incentive structure favors preventive treatments over curative applications, particularly in regions where fall armyworm pressure has historically caused yield losses exceeding 20% in untreated fields. Paraguay's emergence as a significant soybean producer adds another 3.7 million hectares to regional demand, with growers adopting Brazilian pest management protocols that emphasize early-season insecticide applications. The expansion into marginal lands with higher pest pressure necessitates more intensive chemical interventions, supporting sustained volume growth across multiple application modes.

Rising Insect Resistance Fueling Demand for Novel Modes of Action

Pyrethroid resistance in key lepidopteran pests has reached critical thresholds across South America, with Spodoptera frugiperda populations showing resistance frequencies exceeding 80% in major soybean-producing regions. This resistance crisis compels growers to adopt diamide insecticides and other novel chemistries that command price premiums of 40-60% over conventional pyrethroids. The economic pressure intensifies as resistance spreads to organophosphates and carbamates, effectively eliminating lower-cost rotation options that previously provided adequate control. Regulatory authorities have responded by fast-tracking registration of new modes of action, including RNA interference products that target essential insect genes. The resistance management imperative drives adoption of tank-mix strategies and sequential applications using different modes of action, increasing both volume consumption and average selling prices across the market.

Growing Adoption of Integrated Pest Management Programs

Brazilian agricultural extension services report that 67% of commercial soybean growers now implement formal IPM protocols, up from 43% in 2020, driven by sustainability certification requirements and export market pressures. These programs mandate the use of multiple pest control tactics, including biological agents, resistant varieties, and targeted chemical applications based on economic thresholds. The IPM approach paradoxically increases insecticide consumption in the short term as growers apply multiple products with different modes of action to prevent resistance development. Argentina's SENASA (Servicio Nacional de Sanidad y Calidad Agroalimentaria) has introduced IPM certification programs that provide preferential access to export markets, creating economic incentives for adoption. The integration of digital monitoring tools and predictive models enables more precise application timing, reducing waste while maintaining efficacy standards that support premium pricing for specialized formulations.

Increasing Outbreaks of Invasive Pest Species

Fall armyworm infestations reached epidemic proportions across South America in 2024, with Brazil reporting damage to over 12 million hectares of crops and Argentina declaring agricultural emergency in 8 provinces. The pest's rapid dispersal and high reproductive rate create recurring demand spikes that strain supply chains and drive spot pricing volatility. Locust swarms in Argentina's northern provinces during 2024 required emergency aerial spraying campaigns covering 2.3 million hectares, demonstrating the market's vulnerability to episodic pest outbreaks. Climate change patterns have extended the geographic range of tropical pests into previously temperate zones, creating new market segments for specialized control products. The invasive nature of these pests necessitates immediate intervention with broad-spectrum insecticides, supporting volume growth in emergency-use segments that command premium pricing due to urgent application requirements.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU maximum-residue limits shrinking active portfolios | -0.7% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Uptake of insect-resistant GMO seeds lowering foliar demand | -0.5% | Brazil, Argentina | Long term (≥ 4 years) |

| Anti-microplastics legislation targeting capsule suspensions | -0.3% | Brazil, Chile, Colombia | Long term (≥ 4 years) |

| Carbon-credit schemes discouraging synthetic chemistries | -0.4% | Brazil, Argentina | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent EU Maximum-Residue Limits Shrinking Active Portfolios

The European Union's progressive reduction of maximum residue limits has eliminated 23 active ingredients from export-oriented crop protection programs since 2024, forcing South American growers to reformulate their pest management strategies. Brazilian soybean exporters face particular pressure as 78% of production targets EU markets, where residue violations result in immediate shipment rejections and long-term market access restrictions. The regulatory tightening creates a two-tier market structure where export-oriented producers pay premium prices for compliant formulations while domestic market growers continue using lower-cost restricted actives. Argentina's wheat and corn exports to Europe have declined 15% since 2024 due to residue compliance challenges, reducing overall insecticide demand in export-focused regions. The compliance burden disproportionately affects smaller formulation companies that lack resources to reformulate products, leading to market consolidation that may ultimately support pricing discipline.

Uptake of Insect-Resistant GMO Seeds Lowering Foliar Demand

Bt corn adoption in Brazil reached 89% of planted area in 2024, while Bt soybean varieties captured 34% market share, reducing foliar insecticide applications by an estimated 2.3 million liters annually. The transgenic traits provide season-long protection against key lepidopteran pests, eliminating the need for multiple foliar sprays that previously generated significant volume demand. Argentina's rapid adoption of stacked traits combining herbicide tolerance and insect resistance has created similar demand displacement in corn production systems. However, the technology's effectiveness shows signs of degradation as target pests develop resistance to Bt proteins, potentially creating future demand recovery opportunities. The refuge requirements mandated for Bt crops maintain some conventional insecticide demand, but at significantly reduced application rates compared to non-transgenic production systems.

Segment Analysis

By Application Mode: Seed Treatment Accelerates

Foliar application commands 53.6% market share in 2024 but grows at below-average rates as growers shift toward preventive strategies that reduce spray frequency and labor requirements. Seed treatment emerges as the fastest-growing segment at 4.61% CAGR, driven by neonicotinoid adoption and systemic insecticide technologies that provide early-season protection. Foliar method has gained considerable traction, particularly in the pulses and oilseeds segment, where it accounts for the highest share of usage. Foliar application provides targeted and rapid control against various pests like lepidopterans and stink bugs, contributing to increased crop yields and improved quality. The method's popularity is further enhanced by its ability to offer uniform distribution of insecticides and immediate response to pest outbreaks across various crop types.

Seed treatment, compared to foliar spraying, not only cuts application costs but also enhances worker safety. This segment's growth is fueled by its effectiveness in curbing plant infections and countering insect vectors, all while bolstering crop productivity. By reducing pesticide use, aiding crop establishment, and promoting sustainable farming, seed treatment has cemented its value in contemporary agriculture. Regions grappling with early-season pests and soil-borne insects are notably embracing seed treatment, as it offers vital early protection and disrupts pest lifecycles. While soil treatment and fumigation cater to niche markets for high-value crops and protected cultivation, their demand remains steady despite limited growth. In most South American nations, chemigation's uptake is hampered by both infrastructure demands and regulatory hurdles.

Note: Segment shares of all individual segments available upon report purchase

By Crop Type: Oilseeds Drive Demand

Pulses and oilseeds capture 48.8% market share in 2024 and is also the fastest growing market with a CAGR of 4.53%, reflecting South America's position as the world's largest soybean production region with over 180 million metric tons of annual output, while The segment's dominance stems from intensive pest pressure in monoculture production systems and high economic value that justifies premium insecticide investments. Grains and cereals represent the second-largest segment, driven by corn production expansion and wheat cultivation in Argentina's Pampas region.

Commercial crops including cotton and sugarcane maintain specialized demand for targeted pest control solutions, particularly in Brazil's Cerrado region where cotton area has expanded 23% since 2020. Fruits and vegetables command premium pricing for residue-compliant formulations but represent limited volume due to smaller planted areas. The turf and ornamentals segment serves urban markets with growth potential tied to economic development and landscaping investments. Regulatory frameworks under ANVISA oversight ensure product safety standards while supporting innovation in crop-specific formulations.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Brazil maintains overwhelming market dominance with 94.0% share in 2024, supported by 45.2 million hectares of soybean cultivation and intensive pest management programs that generate USD 16.5 billion in annual insecticide consumption. Argentina emerges as the fastest-growing market at 4.57% CAGR through 2030, recovering from drought-related contractions in 2022-2023 to capture expanding market opportunities. Brazil's leadership stems from favorable climate conditions that support year-round crop production and pest reproduction cycles requiring continuous chemical intervention. São Paulo and Mato Grosso states account for 67% of national consumption, driven by large-scale commercial agriculture operations that adopt premium technologies and integrated pest management protocols. [2]Source: Brazilian Ministry of Agriculture, “Integrated Pest Management Guidelines 2024,” gov.brThe regulatory environment under ANVISA oversight supports innovation while maintaining safety standards that enable export market access.

Argentina's 16.8 million hectares of soybean area and 6.5 million hectares of corn create substantial demand for foliar and seed treatment applications, particularly in Buenos Aires and Córdoba provinces where intensive agriculture predominates. SENASA's regulatory framework has accelerated registration of novel insecticides while implementing resistance management protocols that support sustainable market growth Argentine National Service of Agri-food Health and Quality. The peso devaluation in 2024 created temporary pricing pressures but improved export competitiveness that supports long-term agricultural expansion and associated insecticide demand.

Chile, Colombia, and Peru collectively represent emerging opportunities driven by agricultural modernization and export market development. Chile's fruit and vegetable sectors demand specialized residue-compliant formulations for European and North American markets, creating premium pricing opportunities for innovative products. Colombia's expanding palm oil and coffee sectors generate demand for targeted pest control solutions, while Peru's agricultural diversification into high-value crops supports market development.

Competitive Landscape

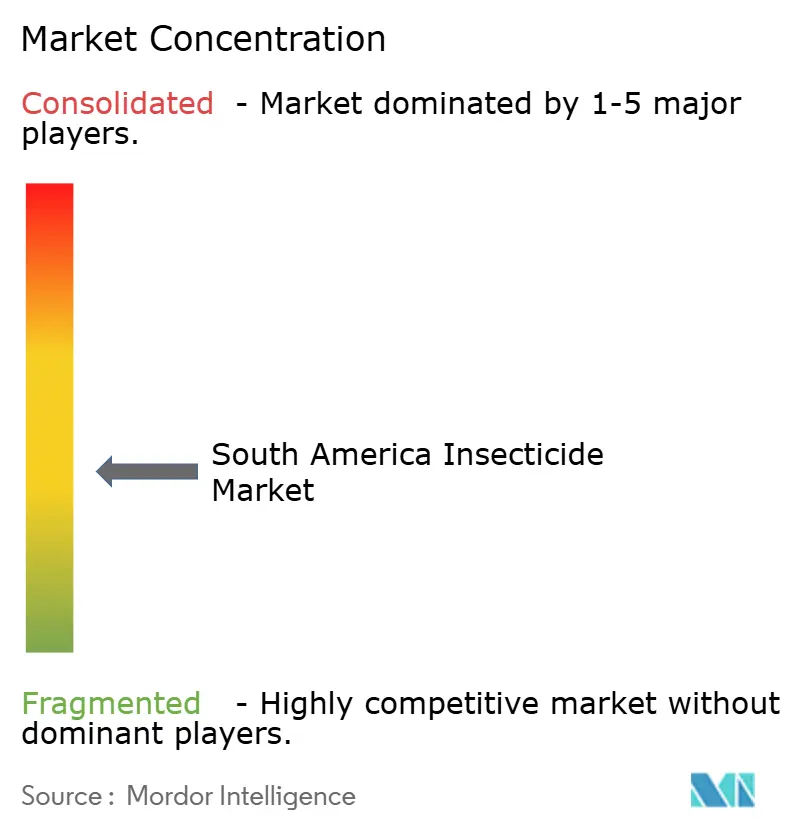

The South America insecticides market exhibits moderate concentration with the top 5 players controlling roughly 23.4% combined market share, creating opportunities for both multinational expansion and regional specialist growth. FMC Corporation leads, through its diamide portfolio and strong distribution networks, while Syngenta Group follows through with broad-spectrum solutions and biological innovations. The competitive intensity has escalated as established players invest in local formulation facilities to reduce import dependency and improve supply chain resilience.[3]Source: SEC Edgar Database, “FMC Corporation Form 10-K 2024,” sec.gov Strategic patterns emphasize portfolio diversification across synthetic and biological solutions, with particular focus on resistance management and sustainability credentials that align with export market requirements.

Technology adoption drives competitive differentiation, with leaders leveraging precision application systems, digital advisory services, and integrated pest management platforms to capture premium pricing and customer loyalty. White-space opportunities exist in biological control segments where regulatory approval timelines favor smaller innovative companies over established multinational corporations. Operational agility is demonstrated through the establishment of local manufacturing facilities and distribution networks across key agricultural regions. Strategic partnerships and collaborations have become increasingly common, allowing companies to combine technological expertise and expand market reach.

Emerging disruptors including Chinese manufacturers and regional formulators challenge incumbent positions through cost-competitive offerings and specialized local market knowledge. Patent expiration cycles create generic competition in established chemistries while opening opportunities for novel formulation technologies and combination products that extend intellectual property protection.

South America Insecticide Industry Leaders

-

ADAMA Agricultural Solutions Ltd

-

Bayer AG

-

Corteva Agriscience

-

FMC Corporation

-

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Syngenta Group invested USD 180 million to expand its biological manufacturing facility in Uberlândia, Brazil, targeting increased production of Bacillus-based insecticides for South American markets. The expansion will triple production capacity by 2026 and includes research partnerships with Brazilian universities to develop region-specific biological solutions.

- September 2024: FMC Corporation received regulatory approval from ANVISA for its RNA interference insecticide Calantha, marking the first commercial RNAi product registration in South America. The approval covers soybean and corn applications with initial market launch planned for the 2025 growing season.

- August 2024: Corteva Agriscience acquired Brazilian biotech company Biotrop for USD 85 million, gaining access to proprietary microbial insecticide platforms and established distribution networks in the Cerrado region. The acquisition strengthens Corteva's biological portfolio for South American markets.

South America Insecticide Market Report Scope

| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

| Commercial Crops |

| Fruits & Vegetables |

| Grains & Cereals |

| Pulses & Oilseeds |

| Turf & Ornamental |

| Argentina |

| Brazil |

| Chile |

| Rest of South America |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits & Vegetables | |

| Grains & Cereals | |

| Pulses & Oilseeds | |

| Turf & Ornamental | |

| Country | Argentina |

| Brazil | |

| Chile | |

| Rest of South America |

Market Definition

- Function - Insecticides are chemicals used to control or prevent insects from damaging the crop and prevent yield loss.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms