Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

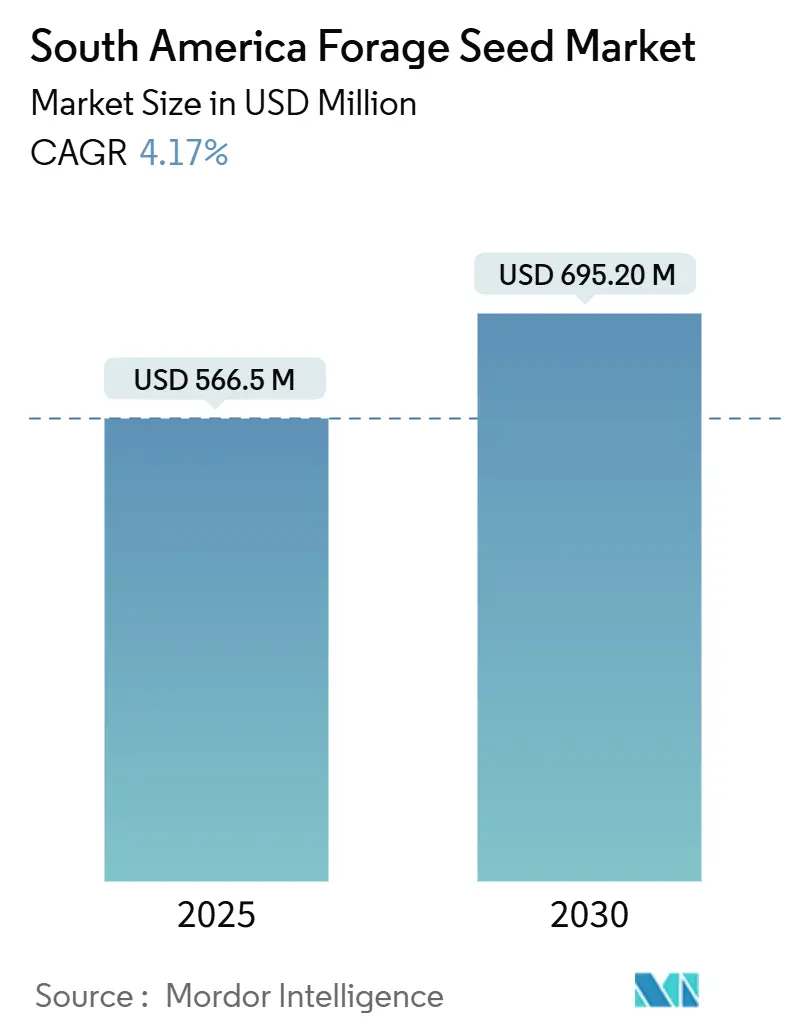

| Market Size (2025) | USD 566.5 Million |

| Market Size (2030) | USD 695.20 Million |

| Growth Rate (2025 - 2030) | 4.17% CAGR |

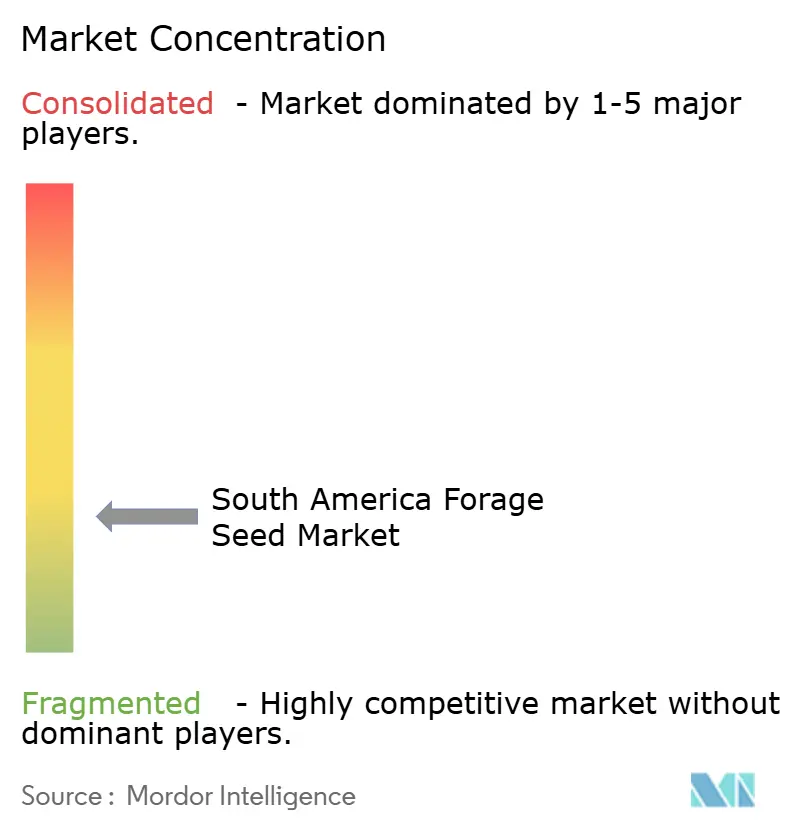

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Forage Seed Market Analysis by Mordor Intelligence

The South America forage seed market is valued at USD 566.5 million in 2025 and is projected to reach USD 695.2 million by 2030, reflecting a 4.17% CAGR. This steady expansion stems from the region’s shift toward sustainable livestock intensification, underpinned by government-backed pasture renovation credit lines and the increasing adoption of crop-livestock integration. Argentina’s peso devaluation improved export competitiveness for alfalfa hay. Hybrid forage technologies preserve yield stability when climate variability intensifies, and integrated crop-livestock systems in Brazil’s Cerrado region create structural demand for rapidly establishing grasses and legumes.

Key Report Takeaways

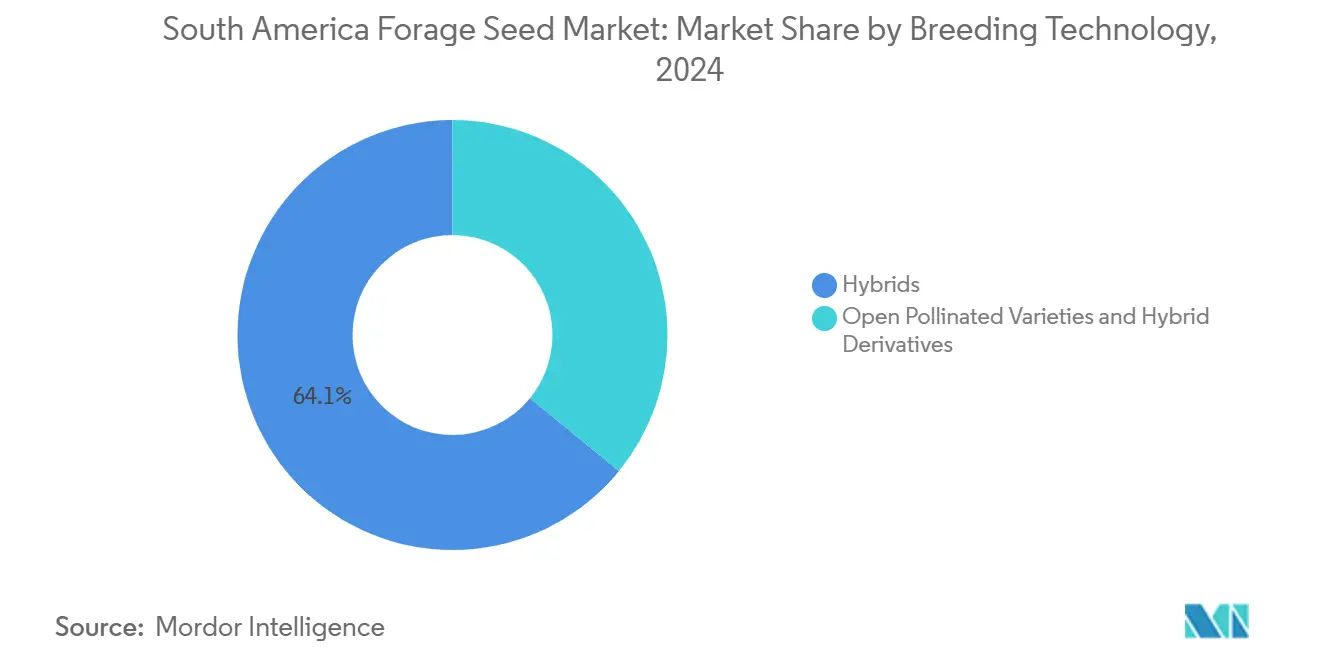

- By breeding technology, hybrid seed held 64.1% of the South America forage seed market share in 2024, and open-pollinated varieties are forecast to grow at a 4.22% CAGR through 2030.

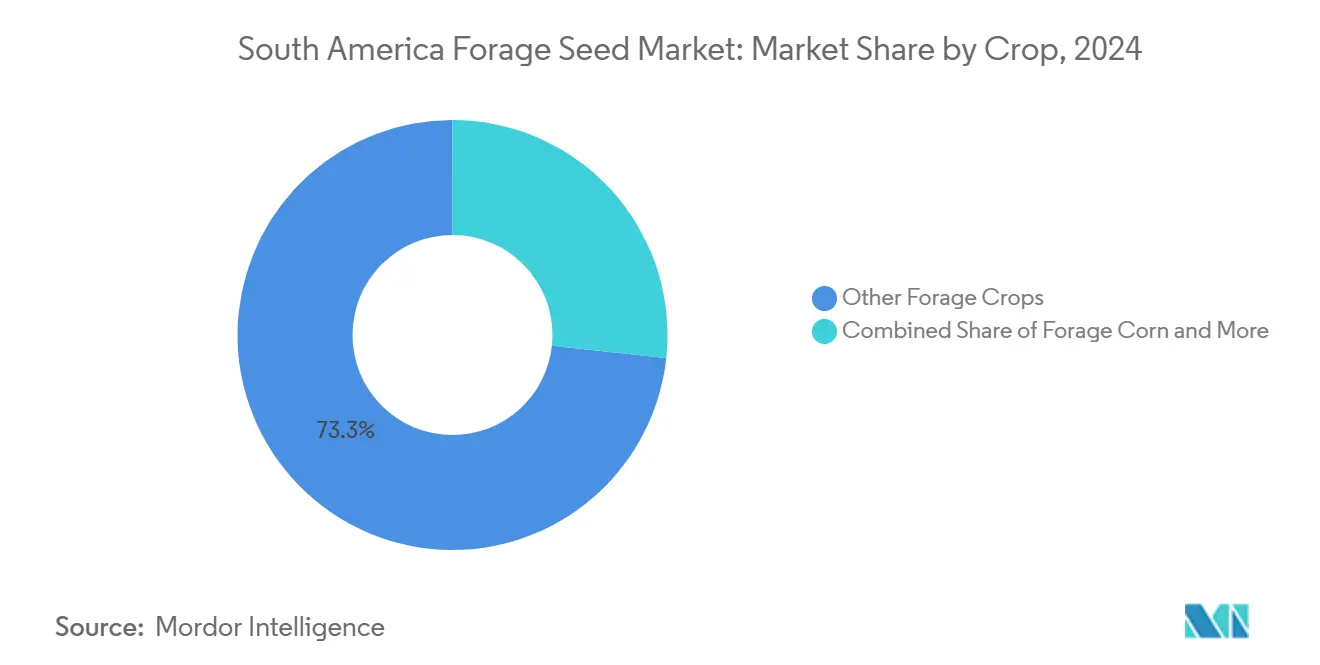

- By crop, other forage species accounted for 73.3% of the South America forage seed market size in 2024, while forage corn is projected to expand at a 5.43% CAGR to 2030.

- By geography, Brazil commanded 75.7% revenue share in 2024, Argentina is anticipated to climb at a 4.57% CAGR during the forecast period.

South America Forage Seed Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dairy and beef herd expansion across Mercosur | +0.8% | Brazil, Argentina, Paraguay, and Uruguay | Medium term (2-4 years) |

| Government subsidies for pasture-renovation programs | +1.2% | Brazil primary and Argentina secondary | Short term (≤ 2 years) |

| Rising adoption of herbicide-tolerant forage hybrids | +0.6% | Brazil Cerrado and Argentina Pampas | Medium term (2-4 years) |

| Growth of integrated crop-livestock systems in Brazil's Cerrado | +0.4% | Brazil Cerrado and Mato Grosso expansion | Long term (≥ 4 years) |

| Emergence of export-oriented alfalfa-hay farms in Argentina | +0.3% | Argentina and spillover to Uruguay | Short term (≤ 2 years) |

| Carbon-credit incentives favoring permanent pastures | +0.2% | Global and early adoption in Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Dairy and beef herd expansion across Mercosur

Cattle numbers reached more than 230 million head in Brazil in 2024, while Argentina maintained its head count despite episodic export curbs. Producers need resilient forages that deliver uniform biomass under heat stress, prompting strong demand for herbicide-tolerant hybrids with improved digestibility. Integrated crop-livestock-forestry systems now span 17.4 million hectares in Brazil, where rotational pastures extend soil cover between grain crops and cut concentrate feed costs.[1]Source: Embrapa, “Integrated Crop-Livestock-Forestry Systems,” embrapa.br Argentina’s premium beef processors call for alfalfa with higher protein to lift marbling scores for Asian markets, while Paraguay and Uruguay replicate intensified grazing models for export certifications.

Government subsidies for pasture-renovation programs

Brazil’s ABC+ window supplies subsidized loans at 7% interest for pasture renewal, 5 percentage points below commercial lines, accelerating large-scale reseeding of degraded grasslands. The RenovAgro program alone budgets BRL 5.05 billion (USD 923 million) through 2030, prioritizing certified varieties that carry documented yield data.[2]Source: Brazilian Development Bank, “RenovAgro Program Guidelines,” bndes.gov.br Argentina’s Buenos Aires Province rebates 50% of seed costs on registered pasture-improvement projects, encouraging operators to switch from uncertified seed to branded germplasm. Favorable terms shorten payback periods, especially when combined with carbon-credit revenue streams, strengthening seed-purchase intent during planting windows.

Rising adoption of herbicide-tolerant forage hybrids

Roundup Ready alfalfa achieved rapid traction in Argentina’s export-hay clusters, where buyers pay premiums for weed-free bales. Brazil’s Law 13.123/2015 treats many (Clustered Regularly Interspaced Short Palindromic Repeats) CRISPR edits as conventional, accelerating clearances from CTNBio and permitting trait-stacking strategies that marry herbicide tolerance with digestibility gains.[3]Source: CTNBio, “Genetically Modified Organism Approvals,” ctnbio.mcti.gov.br Producers in the Cerrado employ these hybrids to manage weed carryover from soybean and corn rotations, improving stand establishment and reducing replanting expenses. Licensing costs remain high, but larger integrated producers accept fees as insurance against yield losses on expansive holdings.

Growth of integrated crop-livestock systems in the Cerrado

Adoption of crop-livestock integration rises 8.2% annually, where rapidly establishing Brachiaria cultivars follow soybean harvests and sustain animal weight gains during the dry season. Embrapa trials confirm productivity lifts of 23% per hectare, coupled with lower greenhouse-gas intensity, drawing institutional land investors. Seed suppliers now market multi-species blends optimized for staggered germination and forage gaps, bundling biological coatings that promote root development in low-phosphorus soils.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy biotech approval timelines for GM forage seeds | -0.4% | Brazil, Argentina regulatory bottlenecks | Medium term (2-4 years) |

| Exchange-rate volatility raising parent-seed import costs | -0.6% | Argentina primary, Brazil secondary | Short term (≤ 2 years) |

| Feed-industry shift toward DDGS and oil-seed meals | -0.3% | Brazil ethanol regions, Argentina soy belt | Medium term (2-4 years) |

| Poor cold-chain logistics restricting coated-seed distribution | -0.2% | Rural Brazil, northern Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lengthy biotech approval timelines for GM forage seed

Regulators in Brazil and Argentina still take 12-36 months to clear genetically modified forage lines, increasing time-to-market costs. Smaller breeders confront steep dossier expenses and multi-site trial mandates, allowing multinational firms with deep regulatory staffs to monopolize early launches. Uncertainty around gene-edited classification causes additional reviews, delaying next-generation traits and capping near-term technology turnover.

Exchange-rate volatility raising parent-seed import costs

Argentina’s peso lost 54% against the USD in 2024, inflating landed costs of U.S. and European parent seed by more than half in local terms. Brazilian real swings complicate forward-contract pricing, encouraging dealers to widen margins or shorten payment windows. Large growers hedge currency exposure, but smaller distributors carry the brunt of cost spikes, translating into retail price inflation and occasional supply rationing.

Segment Analysis

By Breeding Technology: Hybrids Sustain Market Leadership

Hybrid seed accounted for 64.1% of the South America forage seed market in 2024 and attracted producer loyalty through consistent vigor and disease tolerance. Licensing of glyphosate-tolerant genes underpins hybrid alfalfa adoption in Argentina, while non-transgenic Brachiaria hybrids target certification-sensitive beef exporters. Although open-pollinated varieties register faster unit growth at a 4.22% CAGR, yield penalties keep many intensive operations anchored in hybrid lines.

Producers that depend on self-saved seed face yield instability during drought years and gradually convert acreage when financing permits. Price-sensitive ranchers in Paraguay and Uruguay become gateway customers for hybrid derivatives that offer partial heterosis at discounted price points. Multinational suppliers leverage global germplasm libraries to accelerate hybrid development, whereas regional firms focus on local landraces for niche resilience traits. Regulatory streamlining for CRISPR edits may shorten commercial timelines, but dossier preparation still demands significant capacity that favors established leaders.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Crop: Diverse Forage Portfolio Anchors Risk Management

Other forage crops, including ryegrass, bermudagrass, and tropical perennial grasses, captured 73.3% revenue in 2024, reflecting their central role in extensive grazing systems. Alfalfa remains critical in Argentina, but forage corn’s 5.43% CAGR positions it as the fastest-growing crop, particularly near large dairies that value high-energy silage.

Seed companies deploy climate-resilience traits across all categories; drought-tolerant sorghum fills gaps in marginal rainfall zones, and temperate ryegrass lines with enhanced rust resistance penetrate Uruguay’s coastal belt. Cross-pollination of know-how between corn and sorghum breeders accelerates trait introgression, compressing development cycles. Still, regulatory approval costs curb experimentation with novel species lacking historic food or feed dossiers, steering investment toward improving incumbents rather than introducing outsiders.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Brazil provided 75.7% of 2024 sales, powered by its degraded pasture under restoration incentive programs. The 2025 Plano Safra ceiling offers concessional financing terms that drop interest rates below commercial benchmarks, crowding in private capital for reseeding equipment and bio-stimulant upgrades. Seed companies stationed in Mato Grosso and Goiás run automated coating lines that integrate micro-nutrients and rhizobia, addressing Cerrado acid-soil constraints while differentiating premium SKUs. CTNBio’s expedited review of gene-edited cultivars reduces regulatory lag, allowing suppliers to deploy new drought-tolerance edits within 18 months of proof-of-concept trials.

Argentina is the fastest riser, surging 4.57% annually as devalued currency improves export margins on alfalfa hay and feed corn. Buenos Aires and Córdoba provinces invest in center-pivot irrigation, maximizing cut cycles per season and requiring seed lots with strict germination standards. SENASA’s rolling approvals for glyphosate-tolerant alfalfa and low-lignin variants enhance forage quality and field cleanliness. Despite these advances, peso volatility inflates imported parent-line costs, pushing local breeders to accelerate public-private collaborations that develop regionally adapted germplasm free from foreign-royalty exposures.

Rest of South America, led by Paraguay and Uruguay, presents a combined opportunity where modernization programs and export certifications cultivate demand for improved seed. Uruguay’s premium grass-fed beef branding relies on high-nutrient pasture mixtures, while Paraguay’s frontier ranches in the Chaco require salt-tolerant and drought-resistant lines. Limited local R&D capacity invites joint ventures between global breeders and domestic firms to test tropical grasses under diverse soil pH and rainfall patterns. Growing interest in carbon-insetting among European retailers supplies additional revenue streams, raising the value proposition of regenerative grazing that depends on quality seed.

Competitive Landscape

The South America forage seed market remains fragmented, with the top five players holding a minor combined share, creating meaningful headroom for regional specialists. Corteva Agriscience leads through stacked herbicide-tolerant traits and a complementary crop-protection portfolio that locks in whole-farm solution contracts. Bayer AG strengthens its footprint after acquiring Gentos, integrating local alfalfa genetics into its global pipeline, and aligning seed and chemistry cross-selling. Deutsche Saatveredelung AG capitalizes on temperate-grass specialization and digital agronomy tools that monitor biomass accumulation via satellite, enabling variable-rate overseeding advice.

Strategic emphasis shifts from bulk seed tonnage to trait-rich value capture, with patent filings around drought tolerance, nitrogen use efficiency, and condensed tannin expression rising sharply in the United States Patent and Trademark Office (USPTO) database. The arrival of (Clustered Regularly Interspaced Short Palindromic Repeats) CRISPR-derived varieties shortens development cycles and forces incumbents to accelerate regulatory affairs hiring. Smaller disruptors target niche problem statements, such as biological seed coatings to counter nematodes in sandy Cerrado soils or smart pellet sizing compatible with high-speed air seeders.

Investment flows mirror this pivot; Corteva committed in 2024 to expand breeding stations equipped with drone phenotyping and AI-driven selection algorithms, compressing product-development timelines by 30%. Advanta Seeds, now part of UPL, exploits its herbicide-tolerant alfalfa launch in Argentina to cross-sell pasture grass blends. Barenbrug’s joint venture with Sementes Caiapó brings European ryegrass expertise to tropical contexts, challenging incumbents in premium dairy corridors.

South America Forage Seed Industry Leaders

Corteva Agriscience

Bayer AG

Advanta Seeds (UPL Limited)

DLF

Deutsche Saatveredelung AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Argentina's repeal of seed registration requirements has eliminated mandatory Comparative Yield Tests for alfalfa and sorghum crops. This regulatory change simplifies the approval process for new cultivars, allowing faster adaptation to market needs and environmental conditions. The revised regulations aim to increase innovation and competition in the seed industry.

- July 2024: KWS established a research and development facility in Uberlândia, Brazil, and acquired a breeding program specializing in tropical corn and sorghum. This expansion enhances the company's ability to develop cultivars resistant to diseases, pests, and environmental stress, which are essential characteristics for forage production systems.

South America Forage Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Alfalfa, Forage Corn, Forage Sorghum are covered as segments by Crop. Argentina, Brazil are covered as segments by Country.Breeding Technology

| Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | |

| Other Traits | ||

| Open Pollinated Varieties and Hybrid Derivatives | ||

Crop

| Alfalfa |

| Forage Corn |

| Forage Sorghum |

| Other Forage Crops |

Country

| Argentina |

| Brazil |

| Rest of South America |

| Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | ||

| Other Traits | |||

| Open Pollinated Varieties and Hybrid Derivatives | |||

| Crop | Alfalfa | ||

| Forage Corn | |||

| Forage Sorghum | |||

| Other Forage Crops | |||

| Country | Argentina | ||

| Brazil | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms

Get More Details On Research Methodology

Download PDF