Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 414.60 Million |

| Market Size (2031) | USD 589.60 Million |

| Growth Rate (2026 - 2031) | 7.30% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Feed Probiotics Market Analysis by Mordor Intelligence

The South America feed probiotics market size stood at USD 414.60 million in 2026 and is forecast to reach USD 589.70 million by 2031, reflecting a 7.3% CAGR over the period. The acceleration of regulatory bans on antibiotic growth promoters, expansion of industrial livestock operations, and increased consumer demand for antibiotic-free meat are collectively driving up probiotic inclusion rates across poultry, swine, ruminant, and aquaculture diets. Brazil’s 2024 Bio-inputs Law, which halved registration timelines, and Chile’s complete prohibition on antibiotic growth promoters, are signaling to integrators that microbial solutions are now the primary path to sustained performance without residue risk[1]Source: Brazilian Ministry of Agriculture, “Bio-inputs Law,” gov.br. The scale of opportunity is underscored by the region’s 96.4 million metric tons of feed output in 2024, 45.6 million metric tons of which was broiler feed, giving suppliers a high-volume channel to amortize strain-development costs[2]Source: Alltech, “Global Feed Survey 2024,” alltech.com . Competitive activity is intensifying, as encapsulation patents, strain libraries, and feed-mill partnerships enable the top five suppliers to protect around 70% of their revenue. By investing in regional manufacturing, they are reducing lead times and tailoring blends to cassava- and soybean-based meal diets. Still, stability challenges in humid, high-temperature environments and rural logistics gaps in Paraguay and Bolivia temper the growth curve, making product robustness and last-mile reach essential differentiators.

Key Report Takeaways

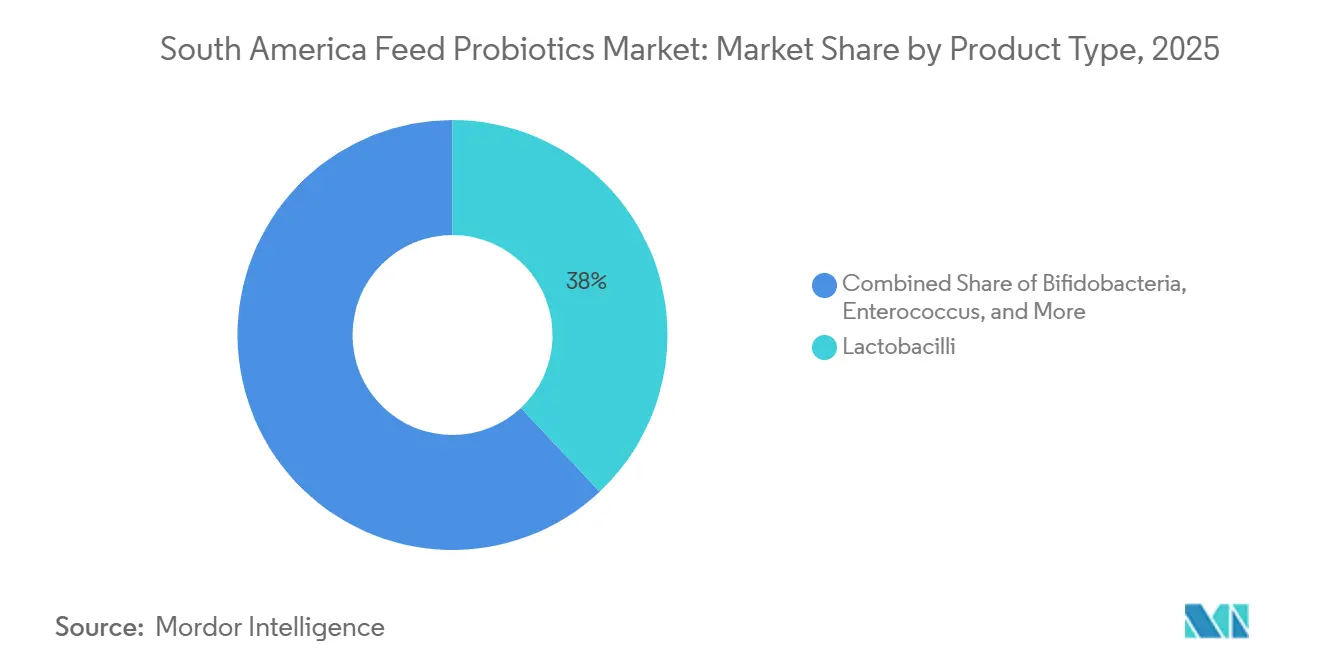

- By product type, lactobacilli dominated with 38% revenue share in 2025, while pediococcus is advancing at an 9.6% CAGR through 2031.

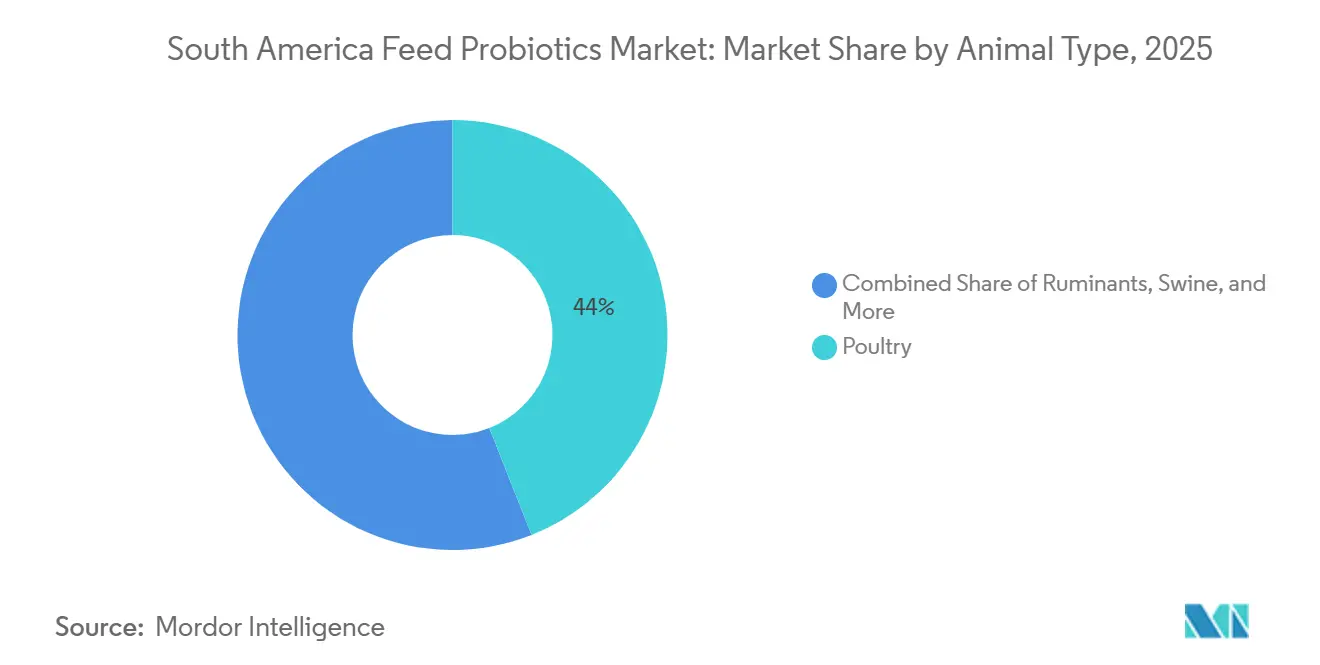

- By animal, poultry held 44% of the South America feed probiotics market share in 2025, as aquaculture recorded the fastest CAGR at 12% to 2031.

- By geography, Brazil accounted for 51% of the South America feed probiotics market size in 2025, whereas Colombia is projected to expand at a 10.6% CAGR through 2031.

- By company concentration, the top five companies together captured a significant revenue share of the South America feed probiotics market in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Feed Probiotics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising meat demand and antibiotic-free protein trend | +2.1% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Regulatory bans on antibiotic growth promoters | +2.5% | Brazil, Chile, Argentina, Colombia | Short term (≤ 2 years) |

| Expansion of industrial livestock operations | +1.8% | Brazil, Argentina, Colombia | Long term (≥ 4 years) |

| Farmer awareness of gut-health benefits | +1.3% | Brazil, Argentina | Medium term (2-4 years) |

| Shrimp farming boom in Ecuador driving aquatic use | +1.0% | Ecuador, Colombia | Short term (≤ 2 years) |

| Indigenous Bacillus strains for tropical diets | +0.6% | Brazil, Paraguay | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Meat Demand and Antibiotic-Free Protein Trend

Per-capita poultry consumption climbed to 44.6 kg in 2025, and Brazil’s 15.3 million metric tons of chicken meat output positions exporters to meet Asia-Pacific and Middle-East orders that increasingly require antibiotic-free certifications[3]Source: Brazilian Animal Protein Association, “Poultry Statistics 2025,” abpa-br.org. Supermarket audits show domestic consumers paying 15-20% premiums for chicken labeled “raised without antibiotics,” prompting integrators to embed probiotics into every formulation tier. The 2024 Bio-inputs Law halved registration timelines, letting suppliers capture faster shelf entry and iterate strains more rapidly. Commercial broiler trials in São Paulo and Paraná demonstrated 3% or better feed-conversion improvements with Lactobacillus blends, clearing the payback threshold even at a two-to-three-times additive cost premium. The pull effect extends to swine and beef channels where processors seek “no-antibiotic-ever” labels to enter premium retail and export segments. As retailers expand private-label antibiotic-free lines, probiotic volumes scale proportionally, boosting the South America feed probiotics market value in tandem.

Regulatory Bans on Antibiotic Growth Promoters

Chile’s Servicio Agrícola y Ganadero now prohibits every antibiotic growth promoter, forcing layer operations that produce 3.94 billion eggs to rely on probiotics and organic acids for performance enhancement[4]Source: Servicio Agrícola y Ganadero, “Antibiotic Growth Promoter Ban,” sag.gob.cl. Brazil’s 2020 ban on tylosin, lincomycin, and thiamulin erased roughly 40% of the antibiotic volume previously used in poultry and swine diets, costing producers USD 183 million in additive substitution but establishing probiotics as the de facto replacement. Argentina and Colombia restrict critically important antibiotics, compelling feed formulators to design multi-strain blends capable of cross-jurisdiction efficacy. Ministry of Agriculture, Livestock and Food Supply's (MAPA) 2024 guidelines require strain deposit, Colony Forming Unit (CFU) guarantees, and antimicrobial-resistance testing, increasing compliance costs but elevating market credibility. Rapid enforcement in Brazil and Chile accelerates demand within 24 months, while slower rule harmonization in Argentina extends the window for supplier education. The regulatory push adds 2.5% points to the forecast CAGR, underpinning the sustained expansion of the South America feed probiotics market.

Expansion of Industrial Livestock Operations

Brazil’s top three poultry integrators controlled 62% of slaughter capacity by 2025 and rolled out standardized probiotic inclusion for contract growers to stabilize feed conversion and carcass yield[5]Source: Brazilian Animal Protein Association, “Poultry Statistics 2025,” abpa-br.org. Argentina’s 3.8 million-heads beef feedlot inventory is consolidating, with feedlots above 10,000 heads adopting microbial solutions to comply with export-market residue limits while maintaining average daily gain. Colombia’s aquaculture tonnage rose 9% annually to 125,037 metric tons, with biofloc and recirculating systems that ban antibiotics and instead rely on Bacillus-based inoculants for nitrogen management[6]Source: Colombian Agricultural Institute, “Aquaculture Production 2024,” ica.gov.co. Scale confers cost leverage, enabling integrators to absorb probiotic premiums and negotiate volume-linked discounts that can shave USD 0.50/kg from list pricing. Feed-mill retrofits to include post-pelleting spraying lines further facilitate probiotic standardization. Combined, these structural shifts underpin a 1.8% uplift to the category CAGR through 2031.

Farmer Awareness of Gut-Health Benefits

Field demonstrations in Brazilian swine herds showed maternal supplementation cutting post-weaning diarrhea by 18% and reducing piglet mortality by 2.3 points. Beef feedlot trials in 2025 revealed narasin plus yeast products matching ionophore performance, encouraging antibiotic substitution without profit erosion. Education lags in Paraguay and Bolivia, where smallholders rely on visual cues rather than metrics to validate new inputs, yet regional cooperatives are piloting smartphone-based feed-efficiency trackers that let producers link probiotic spend to gain. As extension programs replicate success stories, adoption curves steepen in secondary markets. Increased visibility into gut-health ROI benefits the South America feed probiotics market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price premium versus conventional additives | -1.2% | Brazil, Argentina | Short term (≤ 2 years) |

| Probiotic stability during pelleting and storage | -0.9% | Brazil, Colombia | Medium term (2-4 years) |

| Variable strain efficacy with local feed ingredients | -0.7% | Brazil, Paraguay | Medium term (2-4 years) |

| Rural distribution gaps in Paraguay and Bolivia | -0.5% | Paraguay, Bolivia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Premium Versus Conventional Additives

Probiotics are priced at USD 5–15/kg compared with USD 2–5/kg for organic acids and enzymes, so feed formulators demand at least a 3% feed-conversion gain to justify the incremental spend. Argentine beef feedlots operating on slim margins of USD 0.05–0.10/kg live-weight prefer cheaper ionophores that deliver predictable weight gain. In smallholder swine systems across Paraguay and Bolivia, limited performance tracking tools make cost per bag the decisive factor, relegating probiotics to a discretionary purchase. Integrators mitigate sticker shock by bundling technical support and performance guarantees, but such programs only work above 10,000 heads annual throughput. High interest rates further raise working-capital costs, amplifying resistance to price premiums.

Probiotic Stability During Pelleting and Storage

Pelleting lines in Brazil and Colombia routinely operate at 80–85 °C, temperatures that kill non-spore-formers unless they are encapsulated in alginate-chitosan or whey-maltodextrin matrices, adding USD 2–4/kg to production costs. Even encapsulated Lactobacilli lose 1–2 log CFU over 90 days when stored at 70% humidity, typical of coastal warehouses. Spray- and freeze-drying plants require USD 0.5–1 million in capital, limiting adoption to large multinationals. Bacillus spores survive pelleting but lack some immune-modulating attributes, forcing formulators to choose between resilience and efficacy. Loss of viability means end-users must overdose to hit target CFU counts, inflating cost-in-use and undermining perceived value. These dynamics trim 0.9% from the forecast CAGR until encapsulation technologies become cheaper at scale.

Segment Analysis

By Product Type: Lactobacilli Dominance Meets Pediococcus Momentum

The South America feed probiotics market size for Lactobacilli accounted for 38% of the overall revenue in 2025. Despite this leadership, Pediococcus posted the highest trajectory with a 9.6% CAGR, reflecting superior heat tolerance that avoids costly encapsulation above 80 °C pelleting thresholds. In poultry and swine, Lactobacillus acidophilus, L. plantarum, and L. reuteri remain staples because of consistent feed-conversion gains. Pediococcus acidilactici is infiltrating aquaculture and high-temperature feed mills, trimming formulation costs by USD 2–3/kg and widening profit margins in Ecuadorian shrimp ponds. Bifidobacteria currently hold a minimal share, but new micro-encapsulation patents promise shelf-life extensions that could unlock ruminant opportunities. Enterococcus faecium demonstrated a moderate reduction in post-weaning diarrhea during Brazilian trials at a dose of 1 × 10⁹ CFU/kg and is gaining recognition among swine veterinarians. Regulatory strain-deposit mandates now favor suppliers with large libraries, pushing Chr. Hansen and DSM-Firmenich to localize fermentation for faster approvals and bespoke blends tuned to cassava-rich diets.

Non-lactic acid categories are emerging as wild cards. Bacillus spores, classified within ‘Other Probiotics,’ logged strong growth as their pelleting resilience addresses stability gaps affecting Lactobacilli. Yeast-based postbiotics such as Levucell SB attract dairy and beef producers who want rumen pH control without antibiotics. Spray-drying and lipid-matrix encapsulation lines now installed in Brazil shorten supply chains, lowering lead times from 90 days import to 30 days domestic. As Pediococcus captures pelleted-feed niches and Bacillus gains share in aquaculture, the product-type landscape remains fluid, giving nimble formulators room to chip away at incumbent dominance while propelling the broader South America feed probiotics market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Animal Type: Poultry Scale Versus Aquaculture Velocity

The South America feed probiotics market size for poultry is anchoring 44% of the total revenue in 2025. Brazil’s vertically integrated broiler giants standardize Lactobacillus blends across 15.3 million metric tons of chicken output, delivering 2.5–3.5% feed-conversion improvements and slashing necrotic enteritis outbreaks. Layers claim a significant share of poultry probiotic use, leveraging microbial additives to fortify shell thickness and extend peak lay for several additional weeks. Turkey and duck niches remain minor but capture export premiums that justify probiotic spending. Swine adoption has expanded across Brazilian herds, driven by maternal supplementation that enhances gut morphology and reduces post-weaning mortality. Ruminants still lag in penetration, held back by ionophore loyalty, but direct-fed microbials based on Bacillus and Saccharomyces are steadily entering dairy applications.

Aquaculture carries strong momentum, with its market share forecast to grow at a 12% CAGR through 2031, the fastest among all species segments. Shrimp accounts for the majority of aquatic probiotic volume, where Bacillus and Pediococcus strains combat Vibrio, improving survival performance. Fish applications, led by Colombian tilapia operations, are reducing Streptococcus agalactiae losses and improving feed conversion efficiency. Recirculating aquaculture systems near urban centers increasingly rely on probiotic water conditioners to control nitrogen levels, making feed-embedded microbes essential rather than optional. Other animal segments, including equine, remain small but are registering strong uptake among high-income owners seeking gut-health benefits.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Brazil retained a 51% revenue grip on the South America feed probiotics market in 2025, due to 96.4 million metric tons of compound feed and a decisive 2020 ban that removed 40% of antibiotic volume from rations. The Bio-inputs Law of 2024 reduced registration lead time to 12 months, letting suppliers accelerate product refresh cycles and fuel market expansion. Southern states São Paulo, Paraná, and Santa Catarina, hosting significant poultry slaughter capacity, impose standardized probiotic inclusion that cascades through contract growers. Swine hotspots in Rio Grande do Sul and Minas Gerais integrate maternal blends to mitigate post-weaning gut disruptions, demonstrating replicable ROI in field trials.

Colombia is projected to lead the market with a CAGR of 10.6% through 2031, driven by the use of probiotics in tilapia and shrimp farms to stabilize biofloc ecosystems. The Huila department accounts for a significant portion of national aquaculture production, where high pond stocking intensities necessitate effective microbial control. In the poultry and swine industries, probiotic adoption is increasing in Antioquia and Valle del Cauca, as integrators implement Brazil's antibiotic-free models to access export markets.

In Argentina, the adoption of probiotics in beef production remains below 20%, as feedlots continue to favor more affordable ionophores. Partial restrictions on antibiotics reduce the immediate need for alternatives, although poultry integrators are beginning to adapt in anticipation of future export market requirements. In Chile, where antibiotic growth promoters are fully banned, cage-based egg farms depend on probiotics to manage disease pressure. Across the rest of South America, the situation varies significantly. Ecuador's shrimp industry drives an increase in probiotic imports, while Paraguay and Bolivia face logistical challenges that hinder penetration into rural areas.

Competitive Landscape

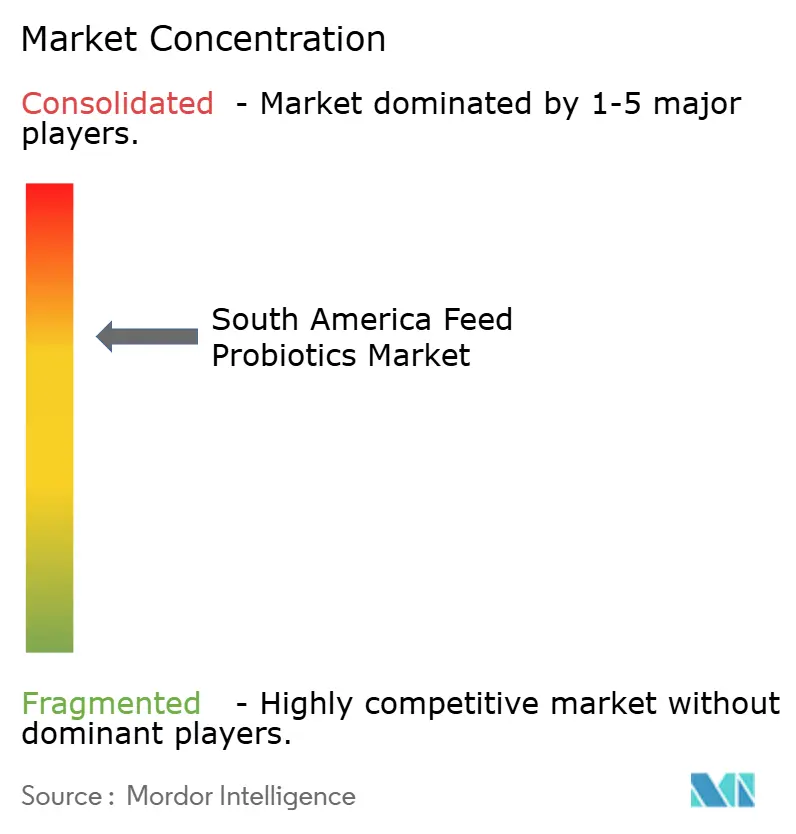

Regional revenue is moderately concentrated, with Cargill Incorporated, Novozymes Group, DSM-Firmenich AG, Adisseo (Bluestar Adisseo Company), and Alltech Inc. collectively holding a significant share in 2025 through the use of proprietary strains, encapsulation technology, and long-term feed mill agreements. Each operates regional laboratories capable of antimicrobial-resistance testing to meet MAPA’s 2024 guidelines, sharpening entry barriers for smaller rivals. Capital deployments of USD 0.5–1 million per spray-drying or freeze-drying line allow incumbents to produce heat-labile Lactobacilli that withstand pelleting, a capability still rare among local challengers.

Niche players capitalize on indigenous strains. Biorigin leverages sugarcane fermenters to scale Bacillus subtilis adapted to cassava diets, bypassing cold-chain dependencies and undercutting imports by 10%. Unique Biotech focuses on B. licheniformis variants that thrive in high-fiber swine and beef rations, winning share in Paraguay. Novus International’s 2024 purchase of BioResource International added novel Bacillus libraries, while Orffa’s 2025 tie-up with Florates embeds gut-health diagnostics that inform strain selection.

Aquaculture remains comparatively uncongested, offering white-space for suppliers with salt-tolerant and pH-flexible strains. Encapsulation remains the technology battleground for alginate-chitosan, whey-maltodextrin, and lipid matrices distinguish premium labels and push efficacy differentials in humid storage. As suppliers race to prove consistent performance across cassava, cassava (DDG), and soybean (DDG), and soybean substrates, strain-library breadth and field-support bandwidth dictate competitive outcomes, shaping the next phase of the South America feed probiotics industry.

South America Feed Probiotics Industry Leaders

Novonesis Group

Alltech Inc.

DSM-Firmenich AG

Cargill, Incorporated

Adisseo (Bluestar Adisseo Company)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Orffa partnered with Florates to launch the “Instant Insight in Animal Gut Health” diagnostic service, enabling real-time microbiome profiling for strain selection.

- July 2024: Nutreco inaugurated a cell-feed plant aimed at high-density aquaculture, technology adaptable for Ecuadorian shrimp ponds. This expansion playing a key role in the development of new probiotic solutions.

- March 2024: Novus International acquired BioResource International, gaining proprietary Bacillus strains tuned to antibiotic-free broiler programs.

South America Feed Probiotics Market Report Scope

Feed probiotics are live microorganisms that, when included in animal feed in sufficient quantities, provide health benefits to the host. These benefits include improving the balance of intestinal microflora, enhancing nutrient absorption, supporting immune function, and boosting overall animal performance.

The South America Feed Probiotics Market Report is Segmented by Product Type (Bifidobacteria, Enterococcus, Lactobacilli, Pediococcus, Streptococcus, and Other Probiotics), by Animal Type (Ruminant, Poultry, Swine, Aquaculture, and Other Animals), and by Country (Brazil, Argentina, Chile, Colombia, and Rest of South America). The Report Offers the Market Size and Forecasts in Terms of Value (USD) and Volume (Metric Tons) for all the Above-Mentioned Segments.

By Product Type

| Bifidobacteria |

| Enterococcus |

| Lactobacilli |

| Pediococcus |

| Streptococcus |

| Other Probiotics |

By Animal Type

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Swine | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Other Animals |

By Country

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Rest of South America |

| By Product Type | Bifidobacteria | |

| Enterococcus | ||

| Lactobacilli | ||

| Pediococcus | ||

| Streptococcus | ||

| Other Probiotics | ||

| By Animal Type | Poultry | Broiler |

| Layer | ||

| Other Poultry Birds | ||

| Swine | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Aquaculture | Fish | |

| Shrimp | ||

| Other Aquaculture Species | ||

| Other Animals | ||

| By Country | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the South America feed probiotics market?

The South America feed probiotics market size reached USD 414.6 million in 2026 and is projected to hit USD 589.6 million by 2031.

Which animal segment is growing the fastest in probiotic adoption across South America?

Aquaculture leads growth with a 14% CAGR, driven primarily by Ecuador’s shrimp farms and Colombia’s tilapia operations.

How have regulatory bans influenced probiotic demand?

Chile’s and Brazil’s bans on antibiotic growth promoters have accelerated probiotic inclusion, adding about 2.5 percentage points to market CAGR.

Which probiotic product type is expanding quickest?

Pediococcus strains are rising at an 11.6% CAGR due to superior heat tolerance in pelleted feeds.

Why are probiotics priced higher than conventional additives?

Probiotics involve complex fermentation, encapsulation, and viability-testing processes, resulting in USD 5–15/kg prices versus USD 2–5/kg for acids or enzymes, though they offset costs by improving feed conversion ratios.

What are the main obstacles to wider probiotic adoption in rural Paraguay and Bolivia?

Lack of cold-chain infrastructure and long delivery cycles raise costs and erode CFU viability, limiting access for smallholder producers.