South America Electric Vehicle Charging Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

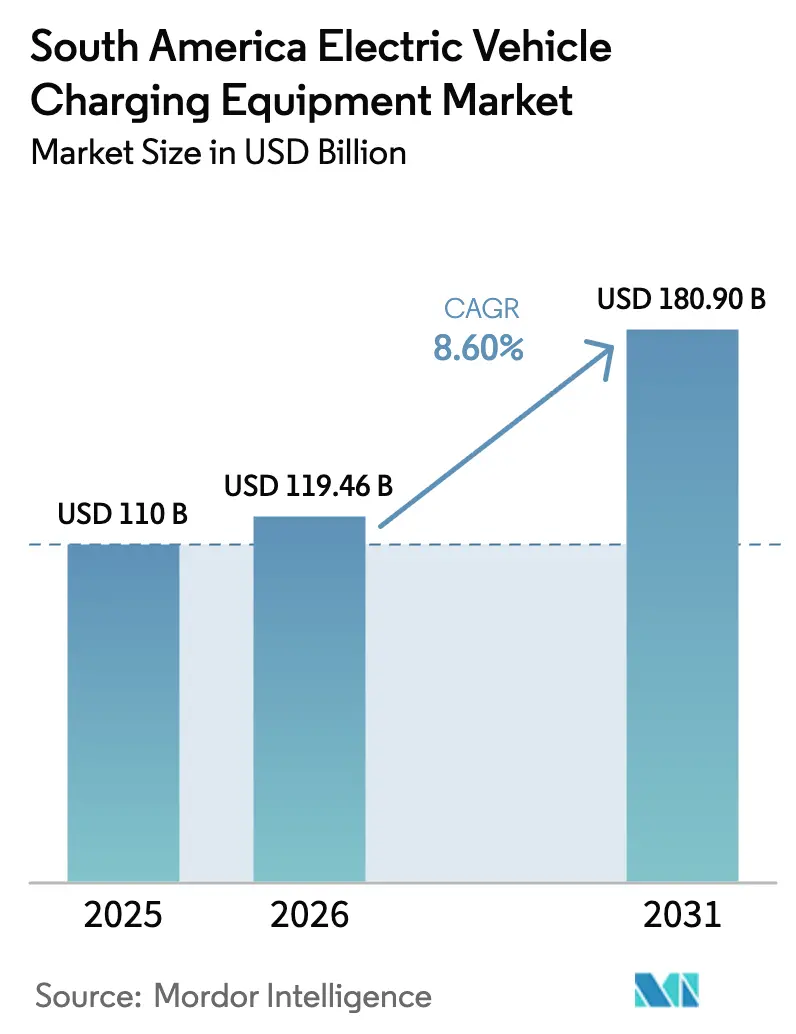

| Base Year Market Size (2025) | USD 110 Billion |

| Market Size (2026) | USD 119.46 Billion |

| Market Size (2031) | USD 180.9 Billion |

| Growth Rate (2026 - 2031) | 8.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Electric Vehicle Charging Equipment Market Analysis by Mordor Intelligence

South America Electric Vehicle Charging Equipment Market size in 2026 is estimated at USD 119.46 million, growing from 2025 value of USD 110 million with 2031 projections showing USD 180.9 million, growing at 8.60% CAGR over 2026-2031.

The measured yet steady trajectory reflects the early stage of the regional transition, where Brazil’s dominant position co-exists with fast-rising pockets such as Peru and Chile. Interplay between home charging convenience, corridor fast-charging economics, and industrial megawatt systems is widening the solution mix that underpins growth. Demand is further amplified by government purchase-tax incentives, falling battery prices that shrink the total cost of ownership, and utility-driven corridor projects that reduce range anxiety. At the same time, high capital expenditure for public DC ports, protracted permitting cycles, and fragmented connector standards continue to temper near-term momentum, holding the penetration of DC fast chargers to only 16% of installed points in Brazil.

Key Report Takeaways

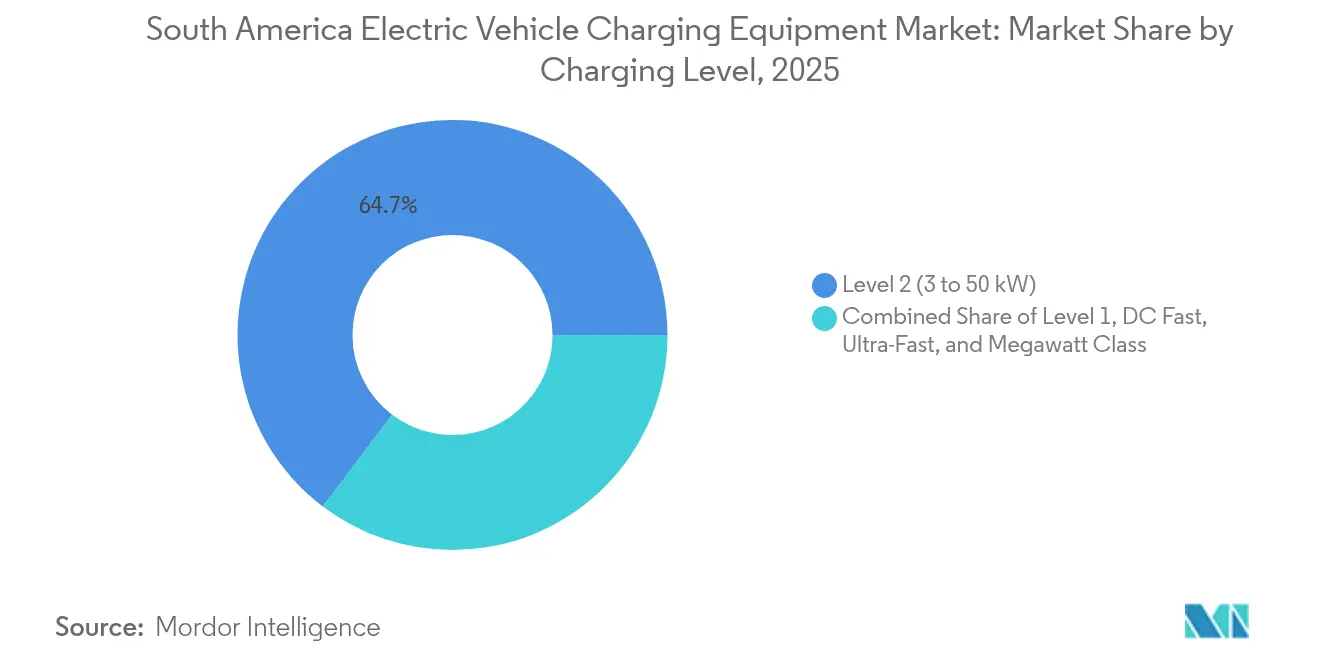

- By charging level, Level 2 equipment held 64.70% of the South America electric vehicle charging equipment market share in 2025, whereas megawatt-class systems above 350 kW are forecast to post a 29.26% CAGR through 2031.

- By installation site, residential locations captured 56.40% of the South America electric vehicle charging equipment market size in 2025, while transportation hubs are projected to grow at a 30.9% CAGR to 2031.

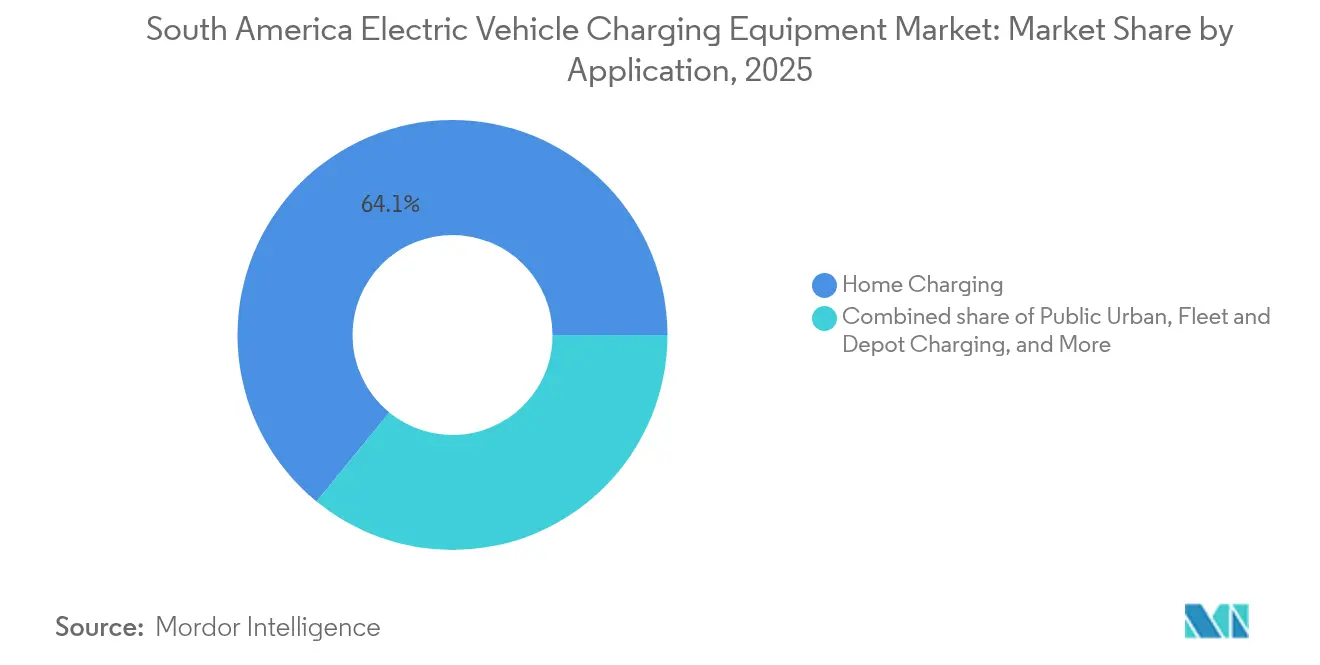

- By application, home charging accounted for a 64.10% share of the South America electric vehicle charging equipment market size in 2025, and fleet–depot installations are advancing at a 34.8% CAGR through 2031.

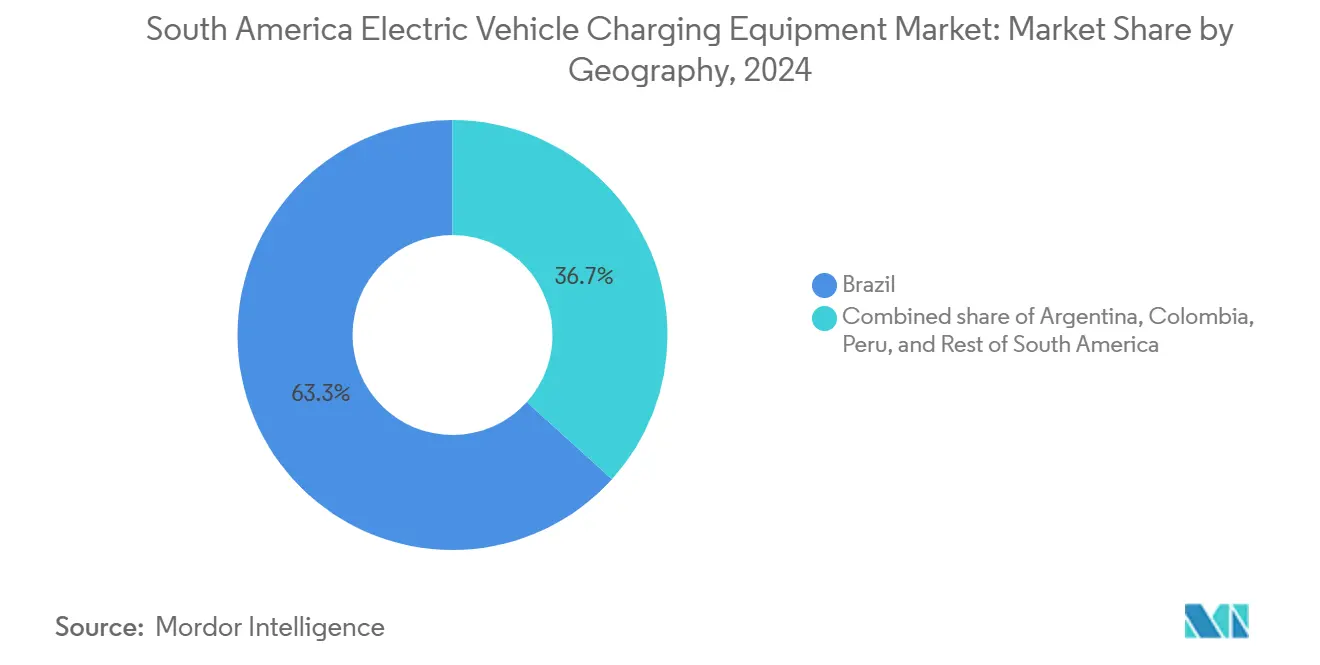

- Brazil led geography rankings with 62.70% revenue share in 2025; Colombia is the fastest-growing geography at a projected 25.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Electric Vehicle Charging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising light-duty EV parc in Brazil & Chile | +2.3% | Brazil (São Paulo, Rio de Janeiro), Chile (Santiago, Valparaíso) | Medium term (2-4 years) |

| Falling lithium-ion battery pack prices | +1.8% | Global, with spillover to Brazil, Argentina, Colombia | Long term (≥ 4 years) |

| Expansion of government purchase-tax incentives | +2.1% | Brazil (Mover Programme), Argentina (tariff removal), Colombia (Law 1964/2019) | Short term (≤ 2 years) |

| Utility-led DC fast-charging corridor projects | +1.5% | Brazil (Northeast corridor), Chile (Northern Route), Colombia (Bogotá) | Medium term (2-4 years) |

| Mining-fleet electrification commitments (Rio, Vale) | +0.9% | Chile (Escondida), Brazil (Vale operations), Peru (copper mines) | Long term (≥ 4 years) |

| Emerging carbon-credit revenue streams for CPOs | +0.5% | Brazil, Chile (early pilots) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Light-Duty EV Parc in Brazil & Chile

Brazil registered 177,358 electric vehicles in 2024, an 89% year-on-year increase, and Chile recorded 480.6% growth in monthly EV sales during September 2024.[1]International Energy Agency, “Global EV Outlook 2025,” iea.org Broader adoption boosts hardware demand because each additional vehicle adds an average of 0.7 public and private charging connections to the South America electric vehicle charging equipment market. Network coverage, however, remains uneven: in February 2025, Brazil had charging facilities in only one-quarter of municipalities, even after a 22% jump in total points since November 2024.[2]Associação Brasileira do Veículo Elétrico, “Infraestrutura de recarga cresce 22% em três meses,” abve.com.brChile’s 140-plus public fast chargers now span all 16 regions, but the presence of four competing connector protocols, Type 2, CCS-2, CHAdeMO, and GB/T, limits roaming and deters inter-regional travel. According to IEA scenarios, Latin America must multiply its public charging stock sixfold by 2030 to meet announced policy goals, which elevates the urgency for interoperable standards and reinforces residential charging as the short-term fallback for most users. Brazil’s incoming SAVE regulation, effective February 2026, imposes strict fire-safety requirements on enclosed garages and could price out legacy condominium retrofits, shifting incremental demand toward curbside and workplace locations.

Falling Lithium-Ion Battery Pack Prices

Global lithium-ion pack prices dropped below USD 100 per kWh in 2024, making several EV segments cost-competitive with internal-combustion models. Brazil’s five-year BRL 19.3 billion Mover Programme subsidizes local battery assembly, promising further cost compression and higher vehicle uptake. Argentina’s tariff exemption for low-cost electrified vehicles targets Chinese models equipped with lithium iron phosphate cells, whose higher cycle life supports more aggressive fast-charging without accelerated degradation. As battery chemistries evolve, charging-equipment specifications adapt: LFP packs tolerate sustained 2C rates, thereby justifying investments in 150 kW–350 kW DC systems and nudging suppliers to expand above-100 kW product lines. Yet only 16% of Brazil’s 14,827 charging points are DC, underscoring the gap between technical readiness and real-world deployment.

Expansion of Government Purchase-Tax Incentives

Federal and provincial tax relief accelerates vehicle uptake, indirectly raising demand for the South America electric vehicle charging equipment market. Brazil exempts EVs from IPI and offers IPVA relief, while Argentina scrapped import duties on up to 50,000 electrified units annually, trimming sticker prices by as much as 35%. Colombia’s Law 1964/2019 sets a 600,000-unit target by 2030 and embeds mandatory fast chargers every 80 km on national highways. Despite the boost to sales, fiscal levers still prioritize vehicles over infrastructure. Draft Bill 497/25 in Brazil seeks to close the gap by granting income-tax deductions for EV-charger investments and waiving PIS/COFINS on hardware sales. If adopted, such measures would shift payback periods for charge-point operators to within typical project-finance horizons of five to seven years.

Utility-Led DC Fast-Charging Corridor Projects

Utilities view the South America electric vehicle charging equipment market as a strategic load-growth lever. Neoenergia’s 1,200 km Green Corridor, fitted with 60 kW–150 kW chargers, cuts intercity travel anxiety in Northeast Brazil. Enel X added 15 fast chargers in Bogotá and rolled out a 103-point hub in Santiago’s Las Rejas shopping center, pairing high-dwell-time venues with rapid top-ups. Chile’s Northern Route places DC stations in remote mining zones such as San Pedro de Atacama, proving the thesis that infrastructure begets demand beyond major metros. Corridor projects also pressure distribution system operators to reinforce substations; Enel Américas earmarked USD 6.1 billion for grid upgrades through 2027 to ensure hosting capacity for clustered fast-charge loads.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex per public DC port (>USD 45,000) | -1.2% | Brazil, Chile, Argentina, Colombia | Short term (≤ 2 years) |

| Slow permitting & grid-connection timelines | -0.9% | Brazil (ANEEL), Chile (CNE), Argentina (ENRE) | Medium term (2-4 years) |

| Inter-network roaming & payment fragmentation | -0.7% | Chile (4 connector standards), regional cross-border | Short term (≤ 2 years) |

| Import tariffs on power-electronics sub-assemblies | -0.4% | Brazil (IPI reinstatement), Argentina (selective tariffs) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex per Public DC Port

A 150 kW DC unit in Brazil costs roughly R$400,000 (USD 80,000) and exceeds R$1 million (USD 200,000) at 350 kW, discouraging private capital in corridors with sub-10% utilization.[3]O Tempo, “Carregadores rápidos custam até R$1 milhão,” otempo.com.br Component bills show galvanic isolation transformers represent 60% of power-electronics expense; technical redesigns that incorporate double-earthing architectures could cut total cost by up to 50% without compromising safety. The IEA indicates charging-station subsidies deliver up to four times the adoption impact of vehicle rebates, yet few South American governments have prioritized hardware grants. Consequently, charge-point operators bundle Level 2 posts (installation cost near USD 1,600) alongside DC stalls to smooth revenue curves and shorten payback periods.

Slow Permitting & Grid-Connection Timelines

Distribution utilities already face 6%–25% incremental load from full fleet electrification, stretching legacy networks and extending approval cycles to 6–12 months in urban centers such as São Paulo.[4]Celesc, “Procedimentos de ligação para sistemas de recarga,” celesc.com.br Chile’s average residential capacity of 4.4 kVA, well below the 6–12 kVA common in developed markets, requires costly service upgrades before installing even modest 7 kW wallboxes. Absence of standardized fast-track procedures at Argentina’s ENRE and Colombia’s CREG leaves applicants navigating ad-hoc municipal rules. The result is inconsistent project timelines that can derail financing schedules and jeopardize corridor continuity. Charge-point operators, therefore, favor co-location with substations at malls, airports, and industrial parks where spare capacity and streamlined permitting offset higher land costs.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Charging Level: Megawatt Systems Emerge for Mining and Logistics

Level 2 solutions retained 64.70% of 2025 revenue, showing that overnight residential and workplace charging still anchors the South America electric vehicle charging equipment market. In contrast, megawatt systems, defined as 350 kW and above, are projected to grow at a 29.26% CAGR as miners, ports, and heavy-duty fleets electrify. Vale’s Caterpillar truck trials and BHP’s USD 250 million Escondida trolley-assist line underline demand for 1 MW–3 MW connectors that the CharIN MCS standard now supports. Neoenergia’s 60 kW–150 kW corridor stations fill the intercity gap between home charging and depot megawatt hubs, yet they comprise only 16% of Brazil’s installed base, highlighting runway for expansion.

Ultra-fast 150 kW–350 kW units cluster in Chile, where Copec Voltex has deployed nationwide coverage, and in Bogotá, where Enel X runs 150 kW posts. Level 1 sockets face regulatory sunset: Brazil’s SAVE ruling will ban Mode 1 and Mode 2 plugs in enclosed garages starting in 2026, forcing condominiums to upgrade. On the opposite end of the spectrum, DP World’s 2 MW Callao array and APM Terminals’ forthcoming electrified yard in Suape confirm that industrial campuses will act as anchor tenants for early megawatt deployments. These high-power hubs, with predictable duty cycles and on-site renewables, improve load-factor economics and position suppliers to diversify revenue via energy-as-a-service contracts.

Note: Segment shares of all individual segments available upon report purchase

By Installation Site: Transportation Hubs Accelerate as Ports Electrify

Residential sites accounted for 56.40% of 2025 installations, mirroring the global pattern where more than four in five EV owners prefer at-home charging. Yet transportation hubs, airports, ports, and rail yards are forecast to contribute a disproportionate share of incremental volume through 2031, rising at a 30.9% CAGR. DP World’s 10-stall, 2 MW truck station at Callao illustrates how ports can amortize high capex across continuous freight activity, while APM Terminals’ USD 320 million Suape rebuild will embed megawatt chargers into crane and yard-tractor operations.

Commercial–retail co-locations offer similar advantages: Enel X’s Las Rejas hub combines 103 chargers with shopping-center dwell time, unlocking utilization north of 20% versus sub-10% averages at dispersed urban posts. Public curbside nodes lag because fragmented municipal rules extend permitting lead times. Brazil’s SAVE regulation further complicates upgrades in older garages, nudging capital toward greenfield mixed-use projects that meet the new fire-safety code. Collectively, these factors reinforce the shift of the South America electric vehicle charging equipment market toward professionally managed, high-demand hubs rather than purely residential deployment.

By Application: Fleet and Depot Charging Outpaces Consumer Segments

Home charging still dominates with 64.10% of 2025 revenue, but fleet and depot installations will be the principal growth engine at a 34.8% CAGR. Shell-backed Raízen and BYD plan 600 stations across eight Brazilian capitals, explicitly targeting commercial fleet contracts that guarantee high throughput. Enel X’s TuCar service in Chile and Mercado Libre’s electrified delivery vans confirm that shared-mobility and e-commerce fleets deliver utilization rates two to three times those of private users.

Depot charging also aligns with predictable charging windows, enabling sophisticated energy-management software to shift loads and avoid peak-time tariffs. Colombia’s mandate for fast chargers every 80 km complements depot infrastructure by ensuring long-haul continuity. In Argentina, micro-EV models such as Coradir’s Chiki sell on the promise of household charging that bypasses public infrastructure, but without parallel public expansion, adoption risks stalling once early majority buyers require intercity capability. Consequently, charge-point operators consider depot contracts a bankable revenue hedge that de-risks public-network capex.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

In 2025, Brazil accounted for a significant 62.70% of total revenue. The Mover Programme, with its BRL 19.3 billion incentive package, is effectively reducing the total cost of ownership. This initiative solidifies Brazil's position as the dominant player in South America's electric vehicle charging equipment market. However, it's noteworthy that only 16% of charging points are DC fast chargers. With the impending SAVE regulation, retrofit costs in older condominiums are set to rise, which may pivot demand towards workplace and curbside charging sites. On the supply side, local manufacturers like WEG are reaping the benefits. WEG has notably quadrupled its output in 2024, capitalizing on the escalating tariffs on imported hardware, which are projected to reach 35% by 2026. Meanwhile, Neoenergia's Green Corridor and Raízen–BYD's ambitious plan for a 600-station network signal a move towards national-scale coverage. Yet, challenges persist, especially in the expansive northern interior.

Colombia, though small today, is on track for a 25.4% CAGR through 2031. Fast-charging mandates every 80 km on national roads have pushed the public tally to 173 stations, accompanying an 85.3% jump in 2024 EV sales. Peru's growth is propelled by Lima-centric passenger sales and mining-sector electrification. DP World's Callao facility, Latin America's first 2 MW truck station, sets a template for high-power coastal nodes that tie into international shipping lanes. Regulatory clarity under Decreto 022-2020-EM de-risks investment, but public density remains sparse outside the capital. Corridor expansion along the Pan-American Highway could unlock tourism and long-haul logistics, extending benefits beyond mining hot spots. Argentina removed import tariffs on 50,000 low-cost electrified vehicles per year, sparking interest among urban drivers; however, with only 17 public chargers nationwide, infrastructure lags far behind vehicle momentum. The risk of stranded assets may curb enthusiasm unless state governments introduce robust station incentives. Chile maintains leadership in per-capita charging density, but connector and payment fragmentation dampen cross-regional travel. Across the rest of South America, Uruguay, Costa Rica, and Ecuador, adoption varies, yet each government cites participation in the ALAMOS electric-route initiative as a priority to boost interoperability.

Note: Segment shares of all individual segments available upon report purchase

Competitive Landscape

Global OEMs such as ABB, Siemens, Schneider, and Delta dominate hardware supply, but regional energy incumbents control site access and consumer relationships. Copec Voltex operates 140-plus public fast chargers and 450 industrial posts across Chile, adding 17 Gogoro battery-swap kiosks that remove dwell-time barriers for two-wheel mobility. Enel X manages 11,000 points region-wide, up 15% in 2024, leveraging its USD 6.1 billion grid-reinforcement plan to integrate front-of-the-meter upgrades with behind-the-meter charging assets. White-space remains in Argentina and Peru, where charger density is below early-adoption thresholds, and first movers can secure top-tier real estate.

Tariff escalation in Brazil has catalyzed local manufacturing: WEG’s quadrupled production challenges imported units on price and lead time, while ABB’s Campinas plant allows the firm to bid competitively on corridor tenders at Graal forecourts. Competitive differentiation now hinges on back-end software, OCPP 1.6 integration, smart-energy management, and carbon-credit accounting. Early adopters of open roaming stand to capture fleet contracts that demand multi-country coverage.

Battery-swap models are emerging as a parallel threat and opportunity. Copec–Gogoro’s network in Santiago and Terpel Voltex’s motorcycle exchange service in Bogotá demonstrate volume potential in two-wheeler segments that value time savings over connector ubiquity. Players that can straddle plug-in and swap formats, while meeting ABNT and CharIN standards, will be better positioned as the South America electric vehicle charging equipment industry broadens in scope and stakeholder complexity.

South America Electric Vehicle Charging Equipment Industry Leaders

ABB Ltd

Siemens AG

Enel X

Copec Voltex

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Colombia's Ministry of Mines and Energy greenlit a suite of incentives aimed at bolstering EV-charging infrastructure. These incentives encompass tax benefits and simplified procedures for operators establishing charging stations.

- April 2025: CharIN e.V., a global advocate for EV charging standards, joined forces with Chile's Agencia de Sostenibilidad Energética (ASE), the nation's energy efficiency policy authority. This collaboration seeks to advance technologies like "Plug & Charge" and "Vehicle-to-Grid (V2G)" in charging infrastructure, while also facilitating the planning of high-power chargers tailored for trucks and heavy vehicles.

- April 2024: Copec Voltex announced that it completed the implementation of five new fast charging points for electric vehicles (EVs) across the southern cities of Chile. In order to continue promoting e-mobility throughout the country, the company has established the equipment in the cities of Talca, Puerto Montt, Osorno, Coyhaique, and Punta Arenas. In addition, it added another charger in Chiloé, which will be ready in the coming days. These latest additions are part of the "+Carga Rápida" program, a joint project to deploy fast charging infrastructure.

- February 2024: Raizen, a leading Brazilian energy firm, and the Chinese automaker BYD have joined forces to create a network of about 600 charging stations for EVs in eight Brazilian cities. The companies aim to meet the forthcoming demand for charging infrastructure in a small but rapidly growing market. The charging points are planned to be installed under the Shell Recharge brand over the next three years in São Paulo, Rio de Janeiro, and six other state capitals in Brazil. Shell and conglomerate Cosan control Raizen.

South America Electric Vehicle Charging Equipment Market Report Scope

Electric vehicle (EV) charging equipment refers to the equipment and infrastructure used to charge electric vehicles at home or in commercial and public spaces. The EV charging equipment plays a key role in the widespread adoption of electric vehicles in South America. The availability of robust EV charging infrastructure is essential for overcoming range anxiety, a primary concern for potential EV buyers. It helps in reducing carbon emissions and improving air quality.

The South America electric vehicle charging equipment Market is segmented by charging level, installation site, application, and geography. By charging level, the market is segmented into level 1, level 2, DC fast, ultra-fast, and megawatt-class charging systems. By installation site, the market is categorized into residential, commercial and retail, public municipal, and transportation hubs. By application, the market is segmented into home, workplace, public urban, highway corridor, and fleet and depot charging. The report also includes market sizes and forecasts for the South America electric vehicle charging equipment market across major countries in the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Level 1 (Up to 3 kW) |

| Level 2 (3 to 50 kW) |

| DC Fast (50 to 150 kW) |

| Ultra-Fast (150 to 350 kW) |

| Megawatt Class (Above 350 kW) |

| Residential |

| Commercial and Retail |

| Public Municipal |

| Transportation Hubs (Airports, Ports) |

| Home Charging |

| Workplace Charging |

| Public Urban Charging |

| Highway Corridor/En-Route Fast Charging |

| Fleet and Depot Charging |

| Brazil |

| Argentina |

| Colombia |

| Peru |

| Rest of South America |

| By Charging Level | Level 1 (Up to 3 kW) |

| Level 2 (3 to 50 kW) | |

| DC Fast (50 to 150 kW) | |

| Ultra-Fast (150 to 350 kW) | |

| Megawatt Class (Above 350 kW) | |

| By Installation Site | Residential |

| Commercial and Retail | |

| Public Municipal | |

| Transportation Hubs (Airports, Ports) | |

| By Application | Home Charging |

| Workplace Charging | |

| Public Urban Charging | |

| Highway Corridor/En-Route Fast Charging | |

| Fleet and Depot Charging | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

How large is the South America electric vehicle charging equipment market in 2026?

It stands at USD 119.46 million and is forecast to reach USD 180.9 million by 2031, growing at a 8.60% CAGR.

Which country leads regional installations?

Brazil holds 62.70% of 2025 revenue and had 14,827 chargers by February 2025.

What segment is growing the fastest?

Megawatt-class systems above 350 kW show a projected 29.26% CAGR thanks to mining and logistics applications.

Are residential chargers still dominant?

Yes, they accounted for 56.40% of 2025 installations, but transportation hubs are catching up at a 30.9% CAGR.

What slows public fast-charger rollout?

High capex per port, long permitting cycles, and fragmented connector standards are key obstacles.

How are utilities participating?

Firms like Neoenergia and Enel X build corridor networks, seeing charging as a long-term load-growth opportunity.