Market Trends of South America Diesel Generator Industry

This section covers the major market trends shaping the South America Diesel Generator Market according to our research experts:

Industrial Sector to Dominate the Market

- South American region has countries that are in their developing stage or are under-developed. These countries are highly reliable on standby power generation or non-conventional methods of power generation. Industrial operations mainly depend on electricity generated from diesel generators during power outages and in regions with limited grid access.

- The increase in the demand for diesel generators in the region is mainly attributed to the growth in numerous end-use industries, including mining, oil & gas exploration, power generation, and construction, that demand heavy-duty generators for continuous and reliable power supply for operation.

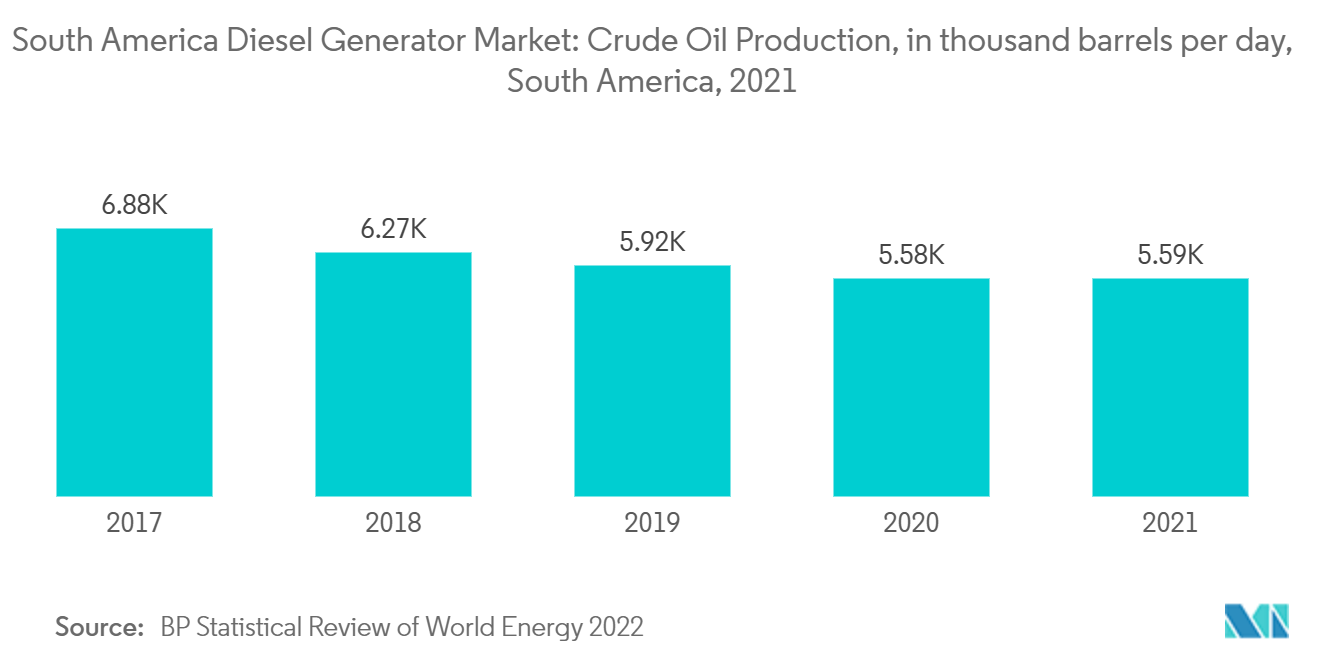

- One of the primary industrial sectors driving demand is the oil and gas exploration sector. As of 2021, South America's crude oil output stood at 5588 thousand barrels/day, which has been fell by nearly 18.7% since 2017. As demand for refined products and petrochemicals rises, the demand for crude oil has been rising, resulting in higher import volumes. As the South American region has significant oil and gas reserves, most of the countries in the region are investing heavily in the development of new reserves. Additionally, the countries are also investing significant amounts in the midstream and downstream sectors to match domestic demand and maximize profits.

- For instance, in Guyana, the recent significant discoveries in the Atlantic, off Guyana's coast, promise an oil revenue boom, which, in turn, is expected to positively impact the market during the forecast period. The offshore Stabroek Block is one of the most significant hydrocarbon discoveries in this decade, and in October 2021, ExxonMobil, the operator of the block, updated its estimate of the recoverable hydrocarbon resources to 10 billion oil-equivalent barrels.

- To leverage its hydrocarbon potential, Guyana has started the process of the development of the rest of its underdeveloped hydrocarbon value chain. GoInvest, a Guyana government agency, announced in October 2021 that the country was planning to build a 220 km-long subsea gas pipeline, which will have the capacity to transport about 50MMSCFD from ExxonMobil-operated Liza Phase 1 and 2 projects. The pipeline will also supply gas to a proposed gas-fired power plant, construction of which is expected to begin in 2022. In September 2021, Guyana approved the USD 600 million Vreed-en-Hoop onshore oil terminal.

- The Brazilian government has made several reforms to attract foreign companies and to end the disinvestment scenario. A series of bids had been held by the government in the past to increase exploration activity in the country. Brazil has several large-scale offshore upstream projects in the pipeline, and the country is expected to contribute more than 20% of global offshore crude oil and condensate production by 2025. The majority of the production is expected to come from the Pão de Açúcar in the Campos basin and Carcará fields. With the commencement of the production from these two fields, the demand for diesel generators in the upstream and midstream industries is expected to increase significantly, driving the market during the forecast period.

- Based on capacity, more than 375 kVA segment is expected to have substantial growth in the segment owing to the wide range of power output, these power rating generators are widely used in the large-scale industrial sector in South America, as they provide uninterrupted power supply and reduced industry downtime, which results in capital gain. Hence, the growing industrialisation in core sectors such as oil and gas, construction, and oil and gas, is expected to drive the market during the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

Argentina is Expected to Witness a Significant Growth in the Market

- Argentina is expected to witness faster growth over the coming years on the back of surging demand for diesel generators in improving the power industry and increasing investment to develop oil & gas activities, airports, and other transportation hubs.

- In Argentina, the diesel generator market is predicted to grow over the forecast period on the back of an increasing number of infrastructure projects in transportation, oil & gas, and the commercial sector. Further, upcoming projects in the residential and hospitality sectors, in the areas such as Buenos Aires and Cordoba cities funded by foreign and private investors, are likely to support the increase in demand for diesel generators in the country.

- The construction of new residential units, hotels, hospitals, etc., is one of the major factors for the growth of the diesel generator market in Argentina. Moreover, the commercial sector dominates the overall Argentina diesel generator market to provide efficient power support to the growing number of construction projects.

- In addition, the country's shale has tremendous potential for companies to expand, businesses to start-up, and for investors to prosper. This is expected to provide diesel generators to aid companies in tapping the shale resource scattered throughout Argentina's basins.

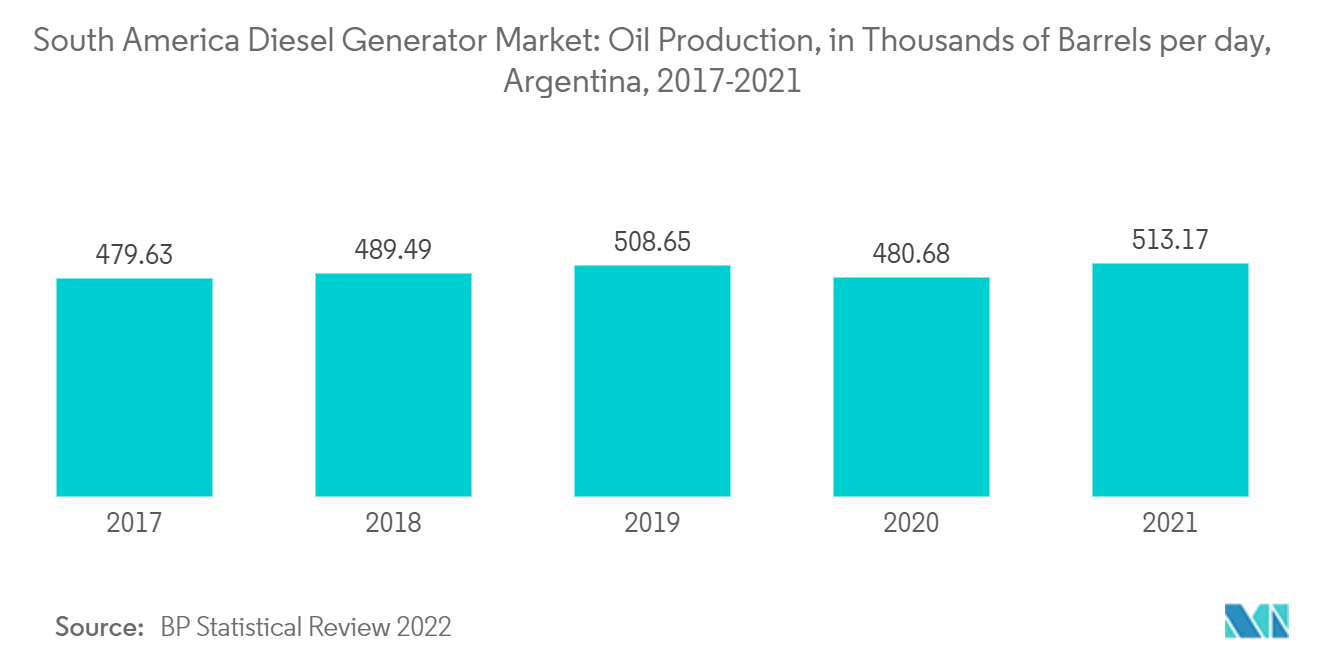

- The upstream sector in the country is relatively well developed. As of 2021, Argentina's crude oil production stood at 513 thousand barrels per day, up by nearly 6.9% from 2017, in stark contrast to the falling production in the rest of the region. Argentina's state-owned energy company YPF has announced that the company's present strategy is more focused on unconventional exploration and production, such as the Vaca Muerta Formation, which mainly constitutes shale gas and oil.

- In January 2022, it was reported that Argentina's Shale gas production witnessed a 42% YoY growth from January 2021, up to 69 million cubic meters per day. This is expected to provide new avenues for the companies engaged in the cooling system business. In September 2021, the Argentina government passed a bill to promote hydrocarbon investment in a bid to increase domestic production in the vast Vaca Muerta shale formation and beyond, as well as to boost oil and gas exports.

- Argentina has also tried to attract foreign investments in its mining sector, and in October 2021, it reduced export taxes from 12% to 8%. According to the Argentine government, mining investment announced nearly USD 9.3 billion in 2020 and 2021 combined, with 94.5% of the projects focused on expansion and construction. According to the government, the country needs USD 22.2 billion to develop identified copper assets and USD 7.3 billion to tap into its lithium deposits. In contrast, investments required to produce gold are pegged at USD 1.65 billion and at USD 1.11 billion for silver,

- Most of the deals in 2021 were in the Lithium mining sector, where investments totaled USD 5.3 billion. Orocobre-Toyota, an Australian and Japanese partnership, and Livent announced capacity expansions. At the same time, Lithium Americas and Ganfeng Lithium approved a second-stage increase at the Caucharí-Olaroz lithium project in Jujuy province, which is expected to enter production in Q4 2022.

- Therefore, the surging power outage and rise in oil & gas explorations and, production, and mining in the country is projected to contribute to the growth of the South America diesel generator market.

Get Analysis on Important Geographic Markets

Download PDF