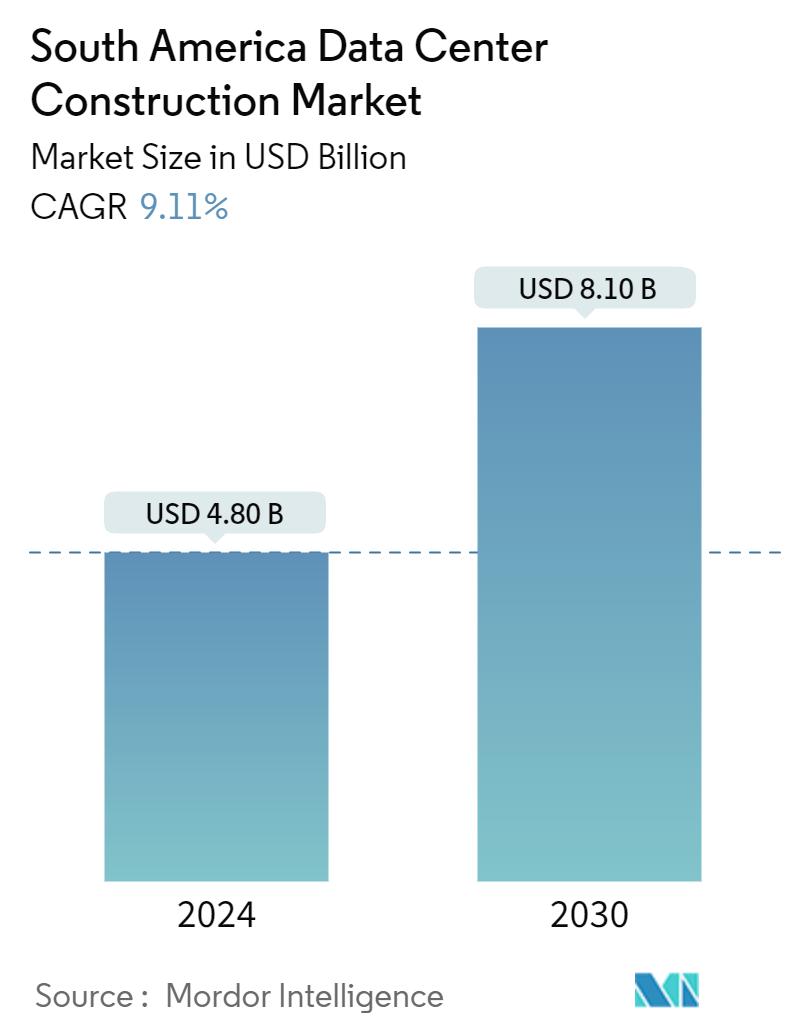

South America Data Center Construction Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Market Size (2024) | USD 4.80 Billion |

| Market Size (2030) | USD 8.10 Billion |

| CAGR (2024 - 2030) | 9.11 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

South America Data Center Construction Market Analysis

The South America Data Center Construction Market size is estimated at USD 4.80 billion in 2024, and is expected to reach USD 8.10 billion by 2030, growing at a CAGR of 9.11% during the forecast period (2024-2030).

- The upcoming IT load capacity in South America is expected to reach more than 1,800 MW by 2030 for under construction IT load capacity.

- The construction of raised floor area for data centers in the region is expected to reach more than 7 million sq. ft by 2030 for under construction raised floor space.

- The region's total number of racks to be installed is expected to reach above 250,000 units by 2030, with Brazil expected to house the maximum number of racks by that time for planned racks.

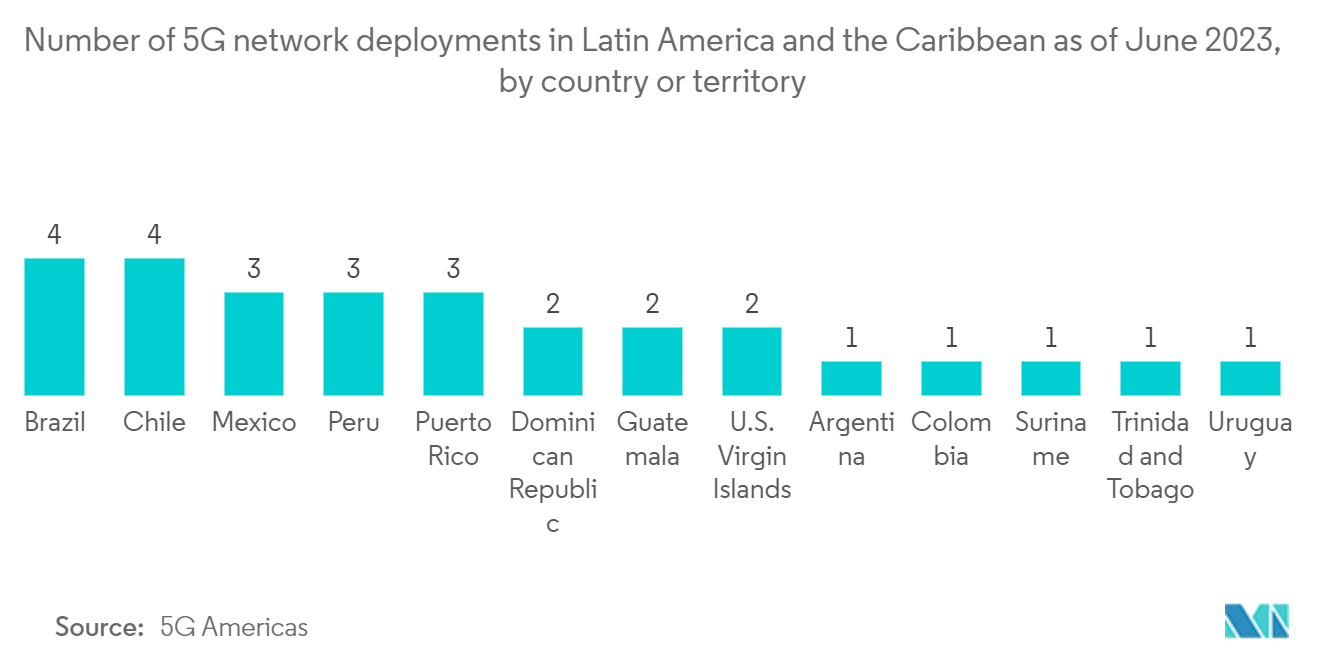

- The region is witnessing rising submarine cable projects. One such submarine cable, estimated to start service in 2025, is Caribbean Express (CX), stretching over 3,472 kilometers with landing points from Cartagena, Colombia, for planned submarine cables.

- Latin America is one of the developing regions for the data center market. The region is seeing more installations of submarine network connectivity, leading to higher data center development driven by efforts from government agencies, telecommunication service providers, and utility providers. Latin America is connected by 68 submarine cables, which has increased the region's capacity five-fold in the last 20 years. Brazil and Chile have the highest number of data centers in terms of massive, large, and medium-sized facilities.

South America Data Center Construction Market Trends

Cloud Segment Expected to Grow Fastest During the Forecasted Period

- The demand for cloud services is promising in Brazil, Chile, Argentina, and other countries. In Argentina, the evolution of the legal and regulatory environment for cloud computing has been faster and more in line with recent technological developments compared to other regional countries. Recently, Amazon Web Services announced plans to invest approximately USD 800 million over a decade in a new data center in Argentina.

- Cloud service providers are the main contributors to Latin America's data center storage market. Expanding cloud presence through establishing multiple cloud regions across countries like Brazil, Chile, Colombia, and Argentina is expected to drive high-performance storage adoption in the market. Software-as-a-service (SaaS) was the leading business model of Brazilian startups, accounting for more than 41% of emerging companies in the country. With platform-as-a-service (PaaS) and infrastructure-as-a-service (IaaS), SaaS is one of Brazil's three principal categories of cloud computing.

- In Mexico, 48% of businesses made investments in cloud-related goods and services in 2018. Microsoft announced "Innovate for Mexico" in 2020 to aid in the development of the country. The primary goal of the strategy is to hasten Mexico's digital transformation through democratizing access to technology. The corporation's five-year USD 1.1 billion investment plan would be implemented to build an area for cloud data centers in the country.

- The IT sector contributed 2.7% to Chile's GDP in 2021. Many data centers run by well-known companies, like Google, Century Link, Huawei, and HP, as well as regional telcos Entel and Gtd, are already located in Chile. As more players enter, Colombia is emerging as the next major Latin American market. Huawei targets a dedicated physical location for its cloud infrastructure and is expecting to activate a new cloud point-of-presence (PoP) in Colombia. The Argentine government is implementing a 'cloud first' policy by investing in and developing a robust national data center at ARSAT. Overall, the Latin American market for cloud data centers is expected to grow significantly.

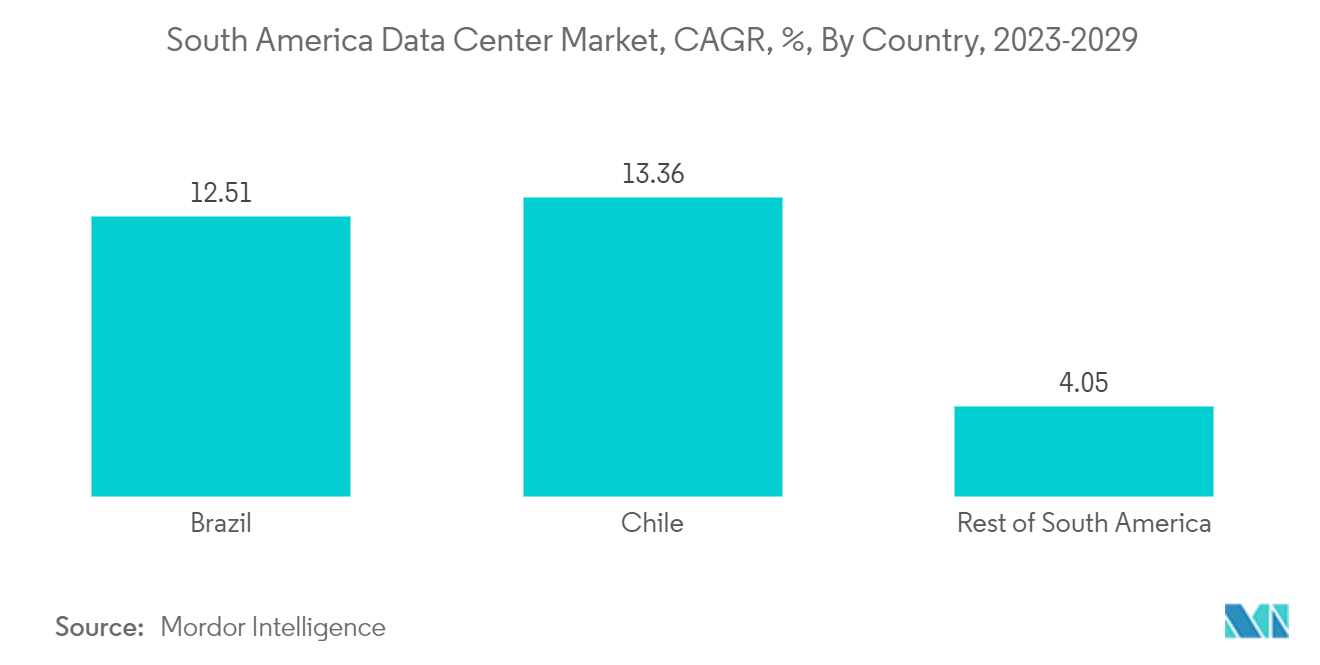

Brazil is Projected to Witness Majority Data Center Construction Activities

- Brazil and Chile hold the largest South American data center market shares. The Brazilian government provides incentives through the Regime Especial de Tributação do Programa Nacional de Banda Larga (REPNBL) program, which includes incentives for purchasing infrastructure that help improve colocation services in the country.

- Rio de Janeiro is expected to lead investments in public data processing and IT entities in Brazil in 2023, with close to BRL 592 million initially earmarked by the state's Proderj company for ICT services and expansions. In January 2023, Brazilian telecom services company Telecall announced plans to expand its fiber optics network to interconnect the main data centers in Rio de Janeiro. The three new redundant and underground fiber routes, totaling 80 km, will be deployed by Telecall to connect at least four new data centers that are being installed in Rio de Janeiro. Overall, Brazil is a major hub for data center locations.

- Chile has competitive energy prices, primarily fueled by plans to take advantage of its natural renewable energy generation potential over the coming years. Energy costs have dropped to one-third of what they were five years ago, mainly based on renewable energy that now makes up 46% of the total produced.

- Chile traditionally has some of the region's best telecommunications infrastructure, and two major fiber projects are underway to ensure it will have a fully redundant fiber backbone. These include the state-funded Fibra Optica Austral (FOA) submarine cable connecting the deep south and Gtd's 3,500 km north-south submarine cable. In 2022, colocation operators, such as Scala Data Centers, ODATA, Ascenty (Digital Realty), and EdgeConneX, were the major investors in the Chilean data center market.

- Chile has competitive energy prices, primarily fueled by plans to take advantage of its natural renewable energy generation potential over the coming years. Energy costs have dropped to one-third of what they were five years ago, mainly based on renewable energy that now makes up 46% of the total produced. Chile traditionally has some of the region's best telecommunications infrastructure, and two major fiber projects are underway to ensure it will have a fully redundant fiber backbone. These include the state-funded Fibra Optica Austral (FOA) submarine cable connecting the deep south and Gtd's 3,500 km north-south submarine cable. In 2022, colocation operators, such as Scala Data Centers, ODATA, Ascenty (Digital Realty), and EdgeConneX, were the major investors in the Chilean data center market.

South America Data Center Construction Industry Overview

The South American data center construction market is fairly fragmented, with significant players such as AECOM, DRP Construction, Fortis Construction, Rider Levett Bucknall, and Mercury Engineering. The market players are adopting various strategies, including acquisitions and partnerships, to enhance their product offerings and remain competitive in the market.

February 2024: OData, a prominent data center operator in Latin America, was seen significantly increasing its presence in Mexico. The company, owned by Aligned, revealed plans to expand its existing QR01 data center in Querétaro. Moreover, OData commenced the construction of two new hyperscale data center campuses in Mexico. The first, located in Guanajuato, will be known as the QR02 campus and is set to provide a capacity of 30 MW. The second campus, QR03, situated in El Marqués, is slated to offer an impressive 150 MW.

May 2024: Equinix is injecting USD 94 million into its third data center in Rio de Janeiro, Brazil. Situated in the Sao Joao de Meriti municipality, approximately 30 km from the Botafogo neighborhood in the capital, the RJ3 facility is slated for a 2025 debut. Spanning 1467 sq. m (15,800 sq. ft), the center will house 560 racks for colocation services, with further specifications yet to be revealed.

South America Data Center Construction Market Leaders

-

AECOM

-

DPR Construction Inc.

-

Rider Levett Bucknall

-

McCarthy Building Companies

-

Whiting-turner Contracting Company

*Disclaimer: Major Players sorted in no particular order

South America Data Center Construction Market News

- July 2024: Odata, a subsidiary of Aligned Data Centers, commenced construction on its fifth data center in Brazil, DC SP04. This facility is strategically located in the Sao Paulo metropolitan area. Fonseca Mercadante Constructor has been selected as the construction partner for this project.

- April 2024: V.tal opened its second Edge data center in Barranquilla, Colombia. This new facility boasts a 3 MW capacity and can accommodate up to 200 racks. The company poured over USD 20 million into this venture. Notably, the new center stands adjacent to V.tal's established BDC1 facility, which provides 1 MW of power and room for 80 racks.

South America Data Center Construction Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

2.1 Research Framework

2.2 Secondary Research

2.3 Primary Research

2.4 Data Triangulation and Insight Generation

3. EXECUTIVE SUMMARY

4. MARKET INSIGHT

4.1 Market Overview

4.2 Market Dynamics

4.2.1 Market Drivers

4.2.1.1 Growing Cloud Applications, AI, and Big Data

4.2.1.2 Rising Adoption of Hyperscale Data Centers

4.2.2 Market Restraints

4.2.2.1 Increase in Power and Real Estate Costs

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Consumers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitutes

4.3.5 Intensity of Competitive Rivalry

4.4 Key Data Center Construction Statistics

4.4.1 Number of Data Centers in South America, 2022 and 2023

4.4.2 Data Center Under Construction in South America, in MW, 2024-2029

4.4.3 Average CAPEX and OPEX For South America Data Center Construction Market

4.4.4 Data Center Power Capacity Absorption in MW, Selected Countries, South America, 2022 and 2023

4.4.5 Top CAPEX Spenders on Data Center Infrastructure in South America

5. MARKET SEGMENTATION

5.1 Market Segmentation - By Infrastructure

5.1.1 Market Segmentation - By Electrical Infrastructure

5.1.1.1 Power Distribution Solution

5.1.1.1.1 PDU - Basic & Smart - Metered & Switched solutions

5.1.1.1.2 Transfer Switches

5.1.1.1.2.1 Static

5.1.1.1.2.2 Automatic (ATS)

5.1.1.1.3 Switchgear

5.1.1.1.3.1 Low-Voltage

5.1.1.1.3.2 Medium-Voltage

5.1.1.1.4 Power Panels and Components

5.1.1.1.5 Other Power Distribution Solutions

5.1.1.2 Power Back-up Solutions

5.1.1.2.1 UPS

5.1.1.2.2 Generators

5.1.1.3 Service - Design & Consulting, Integration, Support & Maintenance

5.1.2 Market Segmentation - By Mechanical Infrastructure

5.1.2.1 Cooling Systems

5.1.2.1.1 Immersion Cooling

5.1.2.1.2 Direct-To-Chip Cooling

5.1.2.1.3 Rear Door Heat Exchanger

5.1.2.1.4 In-Row and In-Rack Cooling

5.1.2.2 Racks

5.1.2.3 Other Mechanical Infrastructure

5.1.3 General Construction

5.2 Market Segmentation - By Tier Type

5.2.1 Tier-I and II

5.2.2 Tier-III

5.2.3 Tier-IV

5.3 Market Segmentation - By End User

5.3.1 Banking, Financial Services, and Insurance

5.3.2 IT and Telecommunications

5.3.3 Government and Defense

5.3.4 Healthcare

5.3.5 Other End Users

5.4 Market Segmentation - By Geography

5.4.1 Brazil

5.4.2 Chile

5.4.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 AECOM

6.1.2 Whiting-turner Contracting Company

6.1.3 Turner Construction Co.

6.1.4 Jacobs Solutions Inc.

6.1.5 DPR Construction

6.1.6 Rider Levett Bucknall

6.1.7 Balfour Beatty US

6.1.8 Hensel Phelps

6.1.9 McCarthy Building Companies

6.1.10 Gilbane Building Company

6.1.11 Fonseca Mercadante Constructor

6.1.12 Mercury Engineering

- *List Not Exhaustive

7. INVESTMENTS ANALYSIS

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

9. ABOUT US

South America Data Center Construction Industry Segmentation

A data center is a physical room, building, or facility that holds IT infrastructure used to construct, run, and provide applications and services and store and manage the data connected with those applications and services. Under data center construction, the report tracks the capital expenditure incurred while building the existing data center facilities and also estimates the future CAPEX based on upcoming data center facilities.

The South American data center construction market is segmented by infrastructure (electrical infrastructure (power distribution solution [PDU, transfer switches, switchgear, power panels and components, and other power distribution solutions)], power back-up solution (UPS and generators), and service – design & consulting, integration, support & maintenance)), mechanical infrastructure (cooling systems [immersion cooling, direct-to-chip cooling, rear door heat exchanger, in-row and in-rack cooling]), racks, and other mechanical infrastructure), and general construction), tier type (tier 1 and 2, tier 3, and tier 4), end user (banking, financial services, & insurance, IT & telecommunications, government & defense, healthcare, and other end users), and geography (Brazil, Chile, and Rest of South America). The market sizes and forecasts are provided in value (USD) for all the above segments.

| Market Segmentation - By Infrastructure | ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| General Construction |

| Market Segmentation - By Tier Type | |

| Tier-I and II | |

| Tier-III | |

| Tier-IV |

| Market Segmentation - By End User | |

| Banking, Financial Services, and Insurance | |

| IT and Telecommunications | |

| Government and Defense | |

| Healthcare | |

| Other End Users |

| Market Segmentation - By Geography | |

| Brazil | |

| Chile | |

| Rest of South America |

South America Data Center Construction Market Research FAQs

How big is the South America Data Center Construction Market?

The South America Data Center Construction Market size is expected to reach USD 4.80 billion in 2024 and grow at a CAGR of 9.11% to reach USD 8.10 billion by 2030.

What is the current South America Data Center Construction Market size?

In 2024, the South America Data Center Construction Market size is expected to reach USD 4.80 billion.

Who are the key players in South America Data Center Construction Market?

AECOM, DPR Construction Inc., Rider Levett Bucknall, McCarthy Building Companies and Whiting-turner Contracting Company are the major companies operating in the South America Data Center Construction Market.

What years does this South America Data Center Construction Market cover, and what was the market size in 2023?

In 2023, the South America Data Center Construction Market size was estimated at USD 4.36 billion. The report covers the South America Data Center Construction Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the South America Data Center Construction Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

South America Data Center Construction Industry Report

Statistics for the 2024 South America Data Center Construction market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. South America Data Center Construction analysis includes a market forecast outlook to for 2024 to (2024to2030 and historical overview. Get a sample of this industry analysis as a free report PDF download.

South America Data Center Construction Market Report Snapshots