Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 118.38 Million |

| Market Size (2031) | USD 160.53 Million |

| Growth Rate (2026 - 2031) | 5.49% CAGR |

| Market Concentration | Medium |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Collagen Market Analysis by Mordor Intelligence

The South American collagen market size stands at USD 118.38 million in 2026 and is projected to reach USD 160.53 million by 2031, advancing at a 5.49% CAGR. This growth rests on Brazil’s dominant cattle-processing base, the region’s expanding aquaculture by-products pipeline, and urban demand for functional foods, nutricosmetics, and regenerative therapies. Market participants leverage plentiful hides, bones, and fish skins while upgrading enzymatic hydrolysis and spray-drying capacity to supply low-molecular-weight peptides to global brands. Brazil’s favorable tariff profile, high social-media penetration, and physician-led supplement positioning accelerate product launches, whereas MERCOSUR regulatory convergence trims cross-border compliance friction. Strategic joint ventures, such as Nextida, further consolidate processing expertise, leaving space for agile entrants to differentiate through sustainability claims and clinical validation. Altogether, the South American collagen market continues to transition from bulk gelatin exports toward value-added consumer and medical applications.

Key Report Takeaways

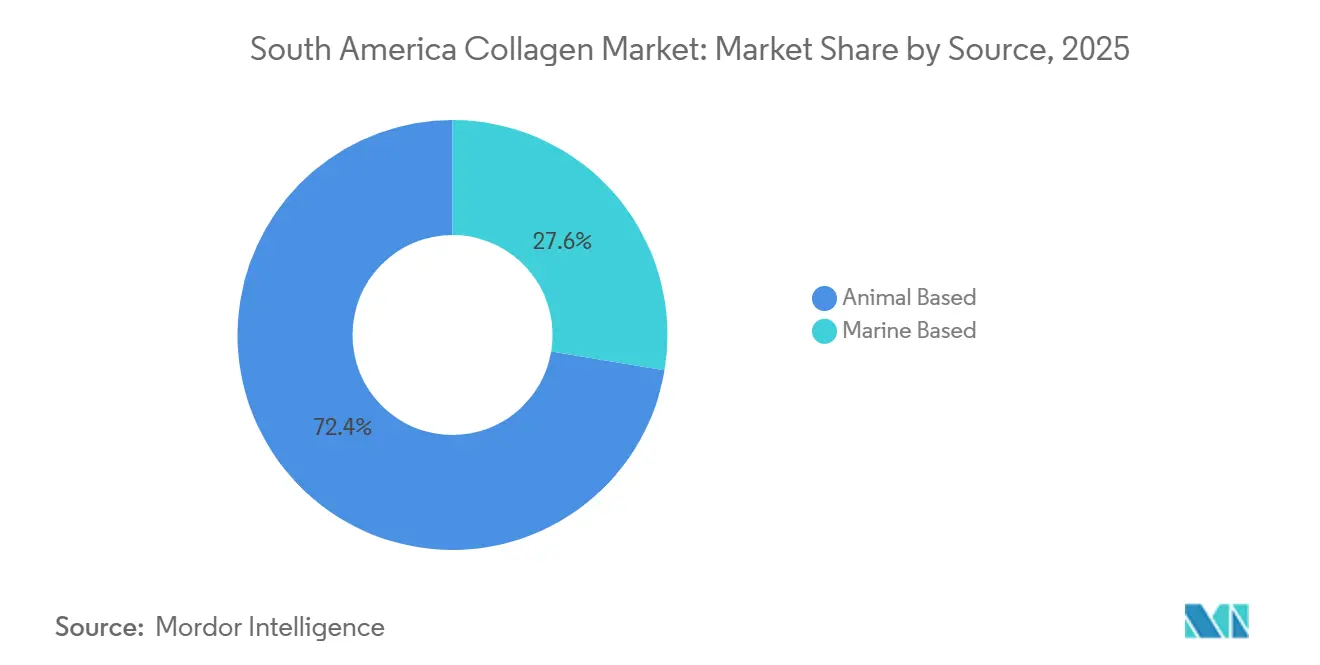

- By source, animal-based collagen captured 65.21% of the South American collagen market share in 2025, while marine collagen posts the fastest 7.89% CAGR to 2031.

- By form, powder formats held 78.12% of the South America collagen market size in 2025; liquid collagen leads growth at 7.22% CAGR through 2031.

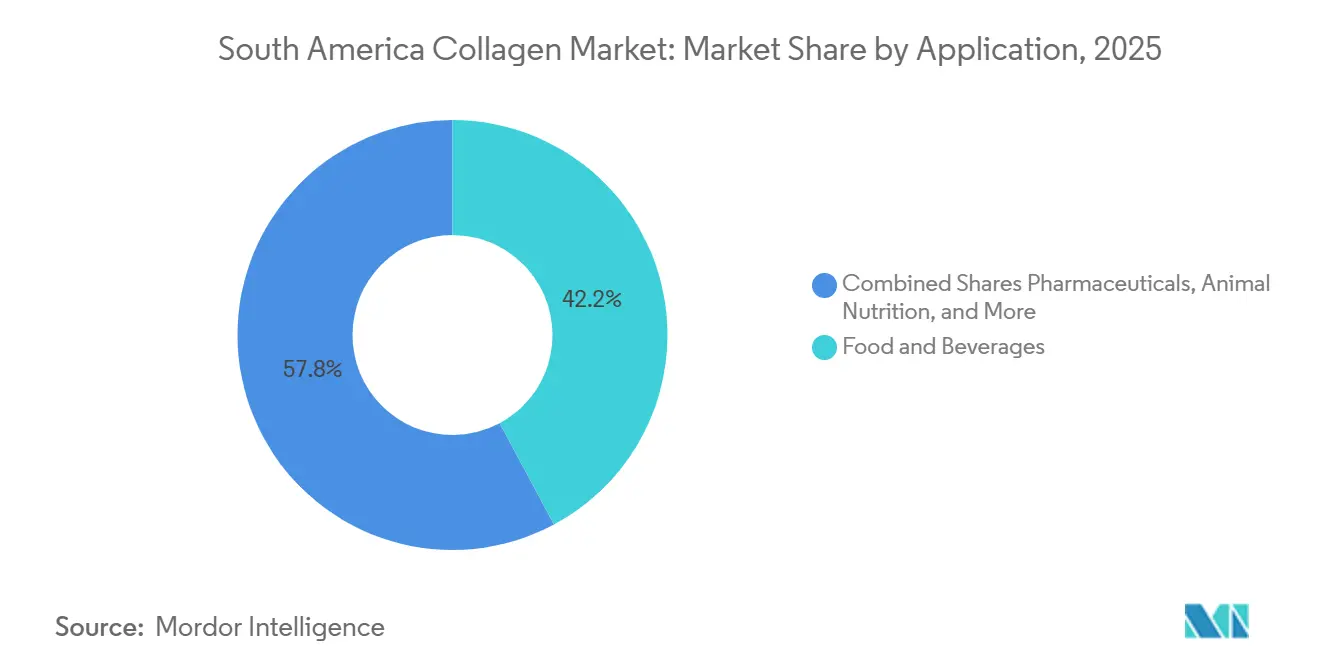

- By application, food and beverages led with 42.18% revenue in 2025, yet cosmetics and personal care expanded at a leading 7.01% CAGR to 2031.

- By geography, Brazil generated 35.68% of 2025 revenue, whereas Argentina recorded the highest 6.62% CAGR for 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Collagen Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for protein-rich functional foods & beverages | +1.2% | Brazil (urban centers), Argentina (Buenos Aires, Córdoba), Chile | Medium term (2-4 years) |

| Rising adoption of collagen-based nutraceutical supplements | +1.0% | Brazil, Argentina, Uruguay | Medium term (2-4 years) |

| Expanding cosmetics & personal-care focus on anti-aging actives | +0.9% | Brazil (São Paulo, Rio de Janeiro), Argentina (Buenos Aires) | Short term (≤ 2 years) |

| Abundant bovine & fish by-products lowering raw-material costs | +0.8% | Brazil, Argentina, Uruguay, Paraguay | Long term (≥ 4 years) |

| Emerging use of injectable collagen in regenerative medicine | +0.6% | Brazil (metropolitan areas), Argentina (Buenos Aires) | Long term (≥ 4 years) |

| Bio-economy incentives for valorising agro-industrial waste | +0.5% | Brazil, Argentina, Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Protein-Rich Functional Foods and Beverages

Urban consumers in São Paulo and Buenos Aires are increasingly identifying collagen as a convenient protein source that provides both macronutrient density and functional benefits, such as joint support and skin hydration. This trend aligns with the broader Latin American shift toward on-the-go nutrition. In Brazil, the functional beverage segment has achieved double-digit growth, driven by manufacturers incorporating hydrolyzed collagen peptides into ready-to-drink formats that cater to busy professionals. GELITA offers products like RTE-JELLY and RTE-DRINK, which dissolve rapidly in cold liquids. This innovation enables brands to enhance juices, smoothies, and sports drinks without compromising their sensory qualities. Beyond beverages, bakery items and snack bars present a growing opportunity. Collagen peptides in these products not only improve texture and moisture retention but also contribute to meeting daily protein requirements. Rousselot's Peptan brand, produced at its Brazilian facility, emphasizes the ingredient's bioavailability. Approximately 57% of consumed collagen peptides convert into free amino acids, while 43% transform into di- and tri-peptides within hours. This positions collagen as a highly efficient protein source, particularly for sports nutrition and meal-replacement products. Collagen's dual functionality—combining macronutrient and bioactive properties—sets it apart from standard whey or soy proteins, supporting its premium pricing in the functional food market.

Rising Adoption of Collagen-Based Nutraceutical Supplements

Consumers in Brazil and Argentina are increasingly purchasing collagen supplements through pharmacies and e-commerce platforms. This growth is primarily driven by awareness campaigns emphasizing collagen's benefits, such as improved skin elasticity, stronger nails, and enhanced joint comfort. Eurofarma launched its Fortice supplement in 2021, targeting over 400,000 doctors monthly. The company markets the over-the-counter product as a prescription-like solution for arthritis and chondromalacia. Eurofarma aims to generate R$ 45 million (USD 9 million) in revenue within three years, establishing a niche in Brazil's domestic market, which is valued at approximately R$ 240 million annually. In February 2024, Brazilian producer GelcoPEP demonstrated the effectiveness of hydrolyzed collagen (types I and III) in a randomized, single-blind, placebo-controlled trial. Participants who consumed 10 grams daily for 180 days reported an 88% improvement in nail resistance and a 78% reduction in hair loss, compared to 47% for both outcomes in the placebo group. This clinical evidence not only supports marketing claims but also aids reimbursement discussions with private health insurers, potentially accelerating adoption among middle-income consumers. In a key regulatory development, Argentina's Resolution 2/2024, effective August 2024, officially approved collagen and hydrolyzed collagen as permissible ingredients in dietary supplements under the Código Alimentario Argentino[1]Source: Brazilian Ministry of Agriculture, “Brazilian gelatin and collagen exports,” GOV.BR. This decision resolves previous regulatory ambiguities that had limited product launches.

Expanding Cosmetics and Personal-Care Focus on Anti-Aging Actives

Brazil established itself as a global leader by recording 10.6 million aesthetic procedures, including both surgical and non-surgical treatments. Collagen-based beauty products, available in both topical and ingestible forms, have become essential in the nutricosmetics market. Brands like Naära market collagen powders formulated with VERISOL peptides, hyaluronic acid, lycopene, and lutein. These powders, promoted as "beauty drinks," claim to combat photoaging, sagging, and wrinkles with a recommended daily dose of 10 grams. GELITA's VERISOL received ANVISA approval for its skin-health claims, confirming its efficacy at a 2.5-gram daily intake. This approval has enabled co-branding partnerships with cosmetics manufacturers. The combination of ingestible and topical collagen reflects a growing "inside-out" beauty trend in South American urban markets, where consumers focus on achieving systemic benefits rather than surface-level results. Products like AestheFill, which contain poly-L-lactic acid (PLLA), have opened a premium segment for dermatologists and plastic surgeons. However, a 2024 Brazilian study identified 55 cases of complications related to PLLA, calcium hydroxylapatite, and polycaprolactone fillers. This highlights the urgent need for thorough practitioner training and stringent post-market monitoring, even as demand continues to grow.

Emerging Use of Injectable Collagen in Regenerative Medicine

ANVISA's recent classification of collagen-based implants and dermal fillers as Class IV medical devices under RDC 751/2022 highlights the regulatory advancements necessary to support regenerative medicine applications, including tissue scaffolds, ocular implants, bone fillers, and surgical sealants. GELITA's MedellaPro portfolio reflects this shift, featuring ultra-low-endotoxin gelatin (≤10 EU/g) designed for 3D bioprinting and tissue engineering. This change represents a move from commodity gelatin to high-purity, application-specific grades that command premium pricing in the market. In 2024, researchers from the University of São Paulo conducted regenerative skin studies, examining collagen matrices for wound healing and burn treatments[2]Source: University of São Paulo. "Regenerative skin research and collagen complications study." usp.br. If these approaches demonstrate cost-effectiveness, they could drive significant institutional demand, particularly within Brazil's public health system. However, the injectable segment continues to face challenges. The requirement for full marketing authorization, supported by clinical evidence and Good Manufacturing Practice certification, extends product timelines to 18-24 months.

Restraint Impact Analysis

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory approvals for medical and food-grade collagen | -0.7% | Brazil (ANVISA jurisdiction), Argentina (ANMAT jurisdiction) | Medium term (2-4 years) |

| Heavy reliance on imports for advanced collagen | -0.5% | Argentina, Chile, Uruguay | Short term (≤ 2 years) |

| Price sensitivity among lower-income groups | -0.4% | Brazil (North, Northeast regions), Argentina (provincial markets) | Short term (≤ 2 years) |

| High costs of sourcing and processing high-quality collagen raw materials | -0.6% | Brazil, Argentina, Uruguay | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Approvals for Medical and Food-Grade Collagen

In March 2023, ANVISA's RDC 751/2022 established a tiered risk classification system for collagen-based medical devices. Implantable or systemically absorbed products are classified as Class III or IV, requiring marketing authorization, detailed technical dossiers, biocompatibility testing, and Good Manufacturing Practices certification, which must be verified through on-site audits. Approvals for Class III and IV devices remain valid for 10 years but must be renewed with updated clinical evidence, resulting in recurring costs for manufacturers. Foreign manufacturers without a legal entity in Brazil are required to appoint a Brazil Registration Holder. This entity handles technical file management, ensures labeling in Portuguese, and oversees post-market surveillance, increasing administrative responsibilities. In 2024, Argentina's ANMAT simplified import procedures for Class I and II medical devices. However, higher-risk collagen products still face lengthy review timelines of several months. In November 2025, Senasa's Resolution 859/2025 revised the definitions of collagen and gelatin to align with European Pharmacopoeia and USP standards. While this change facilitates export certification, it also requires domestic producers to reformulate or re-label their products to meet the updated specifications. As a result, medical-grade collagen now faces a 12-to-24-month delay from development to market entry, discouraging smaller firms from pursuing pharmaceutical or regenerative medicine applications.

High Costs of Sourcing and Processing High-Quality Collagen Raw Materials

South America has abundant bovine and fish by-products but faces challenges in extracting and purifying pharmaceutical- or cosmetic-grade collagen due to the limited availability of advanced equipment, such as enzymatic hydrolysis, ultrafiltration, and spray-drying systems, among regional processors. Marine collagen extraction from fish skins and scales produces lower yields per ton of raw material compared to bovine hides. For instance, studies indicate that Tambatinga fish skins from Brazilian Amazonian aquaculture yield only 35.5% collagen, necessitating higher processing throughput to achieve commercial viability. The cost difference between commodity gelatin and bioactive collagen peptides can exceed 300%, driven by the need for molecular-weight control, low endotoxin levels, and consistent batch quality. JBS's R$ 150 million (USD 30 million) investment in April 2024 to expand its Campo Grande II slaughterhouse capacity to 4,400 cattle per day underscores the scale required to generate sufficient hide volumes for collagen extraction. However, smaller abattoirs find it difficult to justify similar investments. Brazil remains reliant on imports for specialty marine collagen and hydrolyzed peptides. In 2023, the country's import bill reached USD 252.7 billion, with collagen ingredients subject to a 7.86% average tariff, according to the Brazilian Ministry of Economy[3]Source: Brazilian Ministry of Economy. "Brazil trade statistics and tariff data 2023." Gov.br.

Segment Analysis

By Source: Marine Collagen Gains Despite Bovine Dominance

In 2025, animal-based collagen led South America's market, accounting for 65.21% of the revenue, highlighting the region's strong integration into global beef and pork supply chains. In 2024, Brazil and Argentina together processed over 3.2 million tonnes of beef, generating by-products such as hides, bones, and connective tissues essential for gelatin and collagen extraction. However, marine collagen is growing rapidly, with a 7.89% CAGR, as aquaculture skins appeal to consumers seeking "cleaner" peptides. Tambatinga fish gelatin, with an impressive 263 Bloom strength, has proven its viability for gummies and capsules. The increasing popularity of sustainability labels and pescatarian diets is driving premium spending on marine products, signaling a positive outlook for South America's collagen market.

Porcine collagen occupies a niche within the animal-based segment, limited by religious dietary restrictions in certain consumer groups. Nevertheless, its valued amino acid profile and gel strength make it a preferred option for pharmaceutical capsules. In March 2024, the UK approved imports of Brazilian porcine gelatin and collagen, joining El Salvador and the US, which had granted approvals earlier that year. This development could shift supplies toward higher-value international markets, potentially reducing domestic availability. Argentina's Instituto Nacional de Tecnología Agropecuaria (INTA) has advanced a bioactive peptides project to extract collagen from meat by-products. By 2025, the project reached a technology readiness level of 4-5, reflecting public-sector efforts to upgrade commodity by-products into functional ingredients. Although marine collagen's premium pricing—often 200-300% higher than bovine alternatives—limits its reach in price-sensitive segments, it serves as a differentiation tool for brands targeting affluent urban consumers who are willing to pay for perceived purity and sustainability.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Liquid Formats Accelerate in Ready-to-Drink Channels

In 2025, powder products led South America's collagen market, accounting for 78.12% of the market share. This dominance was driven by their logistical advantages and formulation flexibility. Spray-dried peptides, for example, dissolve instantly, enabling bakeries, confectioners, and smoothie brands to fortify their recipes without altering texture or quality. Additionally, the ease of transportation plays a significant role; a 25 kg drum that does not require a cold chain is particularly suitable for distribution across remote Amazonian or Andean regions, where maintaining cold storage is challenging.

On the other hand, liquid collagen is experiencing robust growth, with a projected CAGR of 7.22%. This growth is fueled by increasing consumer demand for convenience-oriented products. Single-serve vials, pre-mixed with peptides, vitamins, and hyaluronic acid, cater to on-the-go lifestyles and are popular as impulse purchases in pharmacies and gyms. The expansion of functional beverage aisles further highlights a shift in consumer preferences, where sensory appeal and time efficiency often outweigh the higher cost per unit. These evolving consumer behaviors are shaping the research and development strategies of ingredient suppliers within South America's collagen sector, emphasizing the importance of innovation to meet these demands.

By Application: Cosmetics Overtakes Pharmaceuticals in Growth

In 2025, the food and beverage sector represented 42.18% of South America's collagen application revenue. This share underscores the extensive use of gelatin in confectionery, desserts, and dairy products, along with the rising adoption of collagen peptides in protein bars, fortified juices, and sports nutrition. Rousselot's Peptan brand has made significant progress in the functional foods market by partnering with over 300 companies through co-branding initiatives. They provide marketing materials and technical support to facilitate seamless product launches. Dietary supplements remain a key application area, with collagen powders and capsules widely distributed through pharmacies, e-commerce platforms, and multi-level marketing channels. Eurofarma's Fortice supplement, designed for physician prescriptions, exemplifies the growing trend of medicalizing collagen supplementation in Brazil.

Cosmetics and personal care, the fastest-growing segment, are projected to grow at a 7.01% CAGR through 2031. This growth is driven by Brazil's 10.6 million aesthetic procedures recorded in 2020 and sustained consumer demand for ingestible beauty products. GELITA's VERISOL and QYRA brands, both approved by ANVISA for skin-health claims, are pivotal in nutricosmetic formulations. These products offer benefits such as wrinkle reduction, improved hydration, and enhanced elasticity with daily doses as low as 2.5 grams. In a 2024 clinical trial, GelcoPEP reported a 94% satisfaction rate among participants regarding hair appearance after 180 days of hydrolyzed collagen supplementation. This evidence supports marketing claims and validates premium pricing. Pharmaceutical applications, including injectable dermal fillers and tissue scaffolds, face challenges due to ANVISA's Class IV medical device requirements. However, the December 2020 approval of AestheFill (PLLA) has established a regulatory pathway for collagen-based biostimulators. Lastly, in the smallest application segment, animal nutrition incorporates collagen peptides into aquaculture feeds and pet supplements. Marine Protein, based in Ecuador, markets its PerfectDigest FPI for poultry, claiming benefits such as improved feed conversion ratios and increased daily weight gain in broilers.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

In 2025, Brazil contributed 35.68% of South America's collagen market revenue, driven by USD 375 million in gelatin and collagen exports to nearly 70 countries, as reported by GOV.BR. The country’s collagen industry is supported by three GELITA plants, which employ 350 staff and hold ANVISA-endorsed health claims, serving as a foundation for domestic R&D clusters. Furthermore, Rousselot’s upgraded Amparo lab and JBS’s USD 30 million investment in expanding its slaughterhouse have significantly enhanced feedstock availability and innovation capacity, strengthening Brazil’s supply chain and positioning it as a key player in the regional market.

Argentina is projected to lead the market with a 6.62% CAGR growth through 2031, driven by regulatory advancements such as Resolution 2/2024, which legalized collagen use in supplements, and Resolution 859/2025, which aligned collagen definitions with global pharmacopoeias. The introduction of RFID-based cattle traceability in 2026 will ensure hide provenance, further solidifying Argentina’s position as a premium exporter. Additionally, the public research agency INTA is actively piloting bioactive peptide extraction technologies, which are expected to facilitate technology transfers to private firms, fostering innovation and growth in the collagen sector.

The rest of South America is leveraging regional trade agreements to drive market growth. Uruguay’s robust SNIG/SIRA traceability system ensures the production of export-grade hides, while Gelnex’s planned plant in Paraguay is set to take advantage of favorable investment incentives, boosting the region’s production capacity. In Chile, the salmon industry is emerging as a key supplier of marine skins for peptide extraction, addressing bovine supply shortages in coastal markets. These cross-border collaborations and synergies are enhancing the integration of the South American collagen market, creating opportunities that extend beyond national boundaries.

Competitive Landscape

The South American collagen market, with a moderate concentration, indicates moderate consolidation. A few multinational players, along with regional specialists and emerging entrants, hold significant influence. Highlighting this trend, Darling Ingredients and Tessenderlo Group agreed in December 2025 to form the Nextida joint venture. This collaboration combines USD 1.5 billion in revenue and an annual capacity of 200,000 metric tonnes across 22 facilities, including South American plants acquired by Darling in 2023 through its USD 1.2 billion purchase of Gelnex. The industry's shift toward vertical integration and economies of scale is evident, driven by the need for consistent feedstock quality, advanced processing equipment, and global distribution networks.

GELITA's presence in South America is anchored by its three plants in Cotia, Mococa, and Maringá, which collectively employ approximately 350 people. These facilities enable GELITA to secure ANVISA health claims for its products, FORTIGEL and VERISOL, thereby differentiating its portfolio with regulatory validation. Growth opportunities remain in areas such as marine collagen valorization, pharmaceutical-grade collagen for regenerative medicine, and private-label nutraceuticals targeting e-commerce channels. PeptPure's innovative Jundiaí plant, which eliminates the intermediate gelatin step, reduces production time by 50% and cuts water and energy consumption by half, showcasing how process innovation can disrupt traditional cost structures.

The October 2025 acquisition by BRF and MBRF of a 50% stake in Gelprime for BRL 312.5 million (USD 62.5 million), adding 9,000 tonnes of capacity, highlights a strategic shift. It reflects how poultry and pork processors are increasingly viewing collagen as a valuable revenue stream rather than a by-product disposal challenge. Smaller players like GelcoPEP are leveraging clinical trials—such as their February 2024 study, which demonstrated an 88% improvement in nails and a 78% reduction in hair loss after 180 days—to build credibility and establish co-branding partnerships with cosmetics brands. Technology adoption focuses on enzymatic hydrolysis, ultrafiltration, and spray-drying to produce low-molecular-weight peptides with high bioavailability. However, the capital-intensive nature of these processes remains a significant barrier, particularly for smaller gelatin producers aiming to transition from commodity-grade to bioactive-grade products.

South America Collagen Industry Leaders

-

Nitta Gelatin NA Inc

-

Gelnex B.V

-

PB Leiner

-

Gelita AG

-

Rousselot

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2024: Brazilian protein giant BRF, through newly formed MBRF Global Foods (post-Marfrig merger), has agreed to acquire a 50% stake in Gelprime, a specialist in animal-derived gelatin and collagen production.

- August 2024: Argentina's Secretariat for Health Quality and Secretariat for Bioeconomy issued Joint Resolution 2/2024, amending Article 1417 of the Food Code to officially authorize hydrolyzed collagen as an ingredient in foods and dietary supplements.

- November 2022: Acquion Food Tech, a new Brazilian venture led by entrepreneur André Albuquerque, begins operations with a plan to invest BRL 250 million (USD 46.6 million) over the next four years to produce collagen and gelatin for the coming years.

South America Collagen Market Report Scope

Collagen is the main structural protein found in skin and other connective tissues and is widely used in purified form for cosmetic surgical treatments.

The South American collagen market is segmented by source, application, and geography. Based on the source, the market is segmented into animal-based collagen and marine-based collagen. The market is segmented based on application into dietary supplements, meat processing, food and beverage, cosmetics and personal care, and other applications. Based on geography, the report provides a detailed regional analysis, which includes Brazil, Colombia, and the Rest of South America.

The report offers the market size in value terms in USD for all the above-mentioned segments.

By Source

| Animal-based |

| Marine-based |

By Form

| Powder |

| Liquid |

By Application

| Food & Beverages |

| Dietary Supplements |

| Personal Care & Cosmetics |

| Pharmaceuticals |

| Animal Nutrition |

By Geography

| Brazil | Argentina |

| Rest of South America |

| By Source | Animal-based | |

| Marine-based | ||

| By Form | Powder | |

| Liquid | ||

| By Application | Food & Beverages | |

| Dietary Supplements | ||

| Personal Care & Cosmetics | ||

| Pharmaceuticals | ||

| Animal Nutrition | ||

| By Geography | Brazil | Argentina |

| Rest of South America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the South America collagen market?

The South America collagen market size is USD 118.38 million in 2026.

Which country leads regional revenue?

Brazil holds 35.68% of regional revenue, supported by its large cattle-processing base.

Which application segment is growing fastest?

Cosmetics and personal care products expand at a 7.01% CAGR through 2031.

Why is marine collagen gaining momentum?

Aquaculture skins and scales support sustainability narratives, driving a 7.89% CAGR for marine collagen.