Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

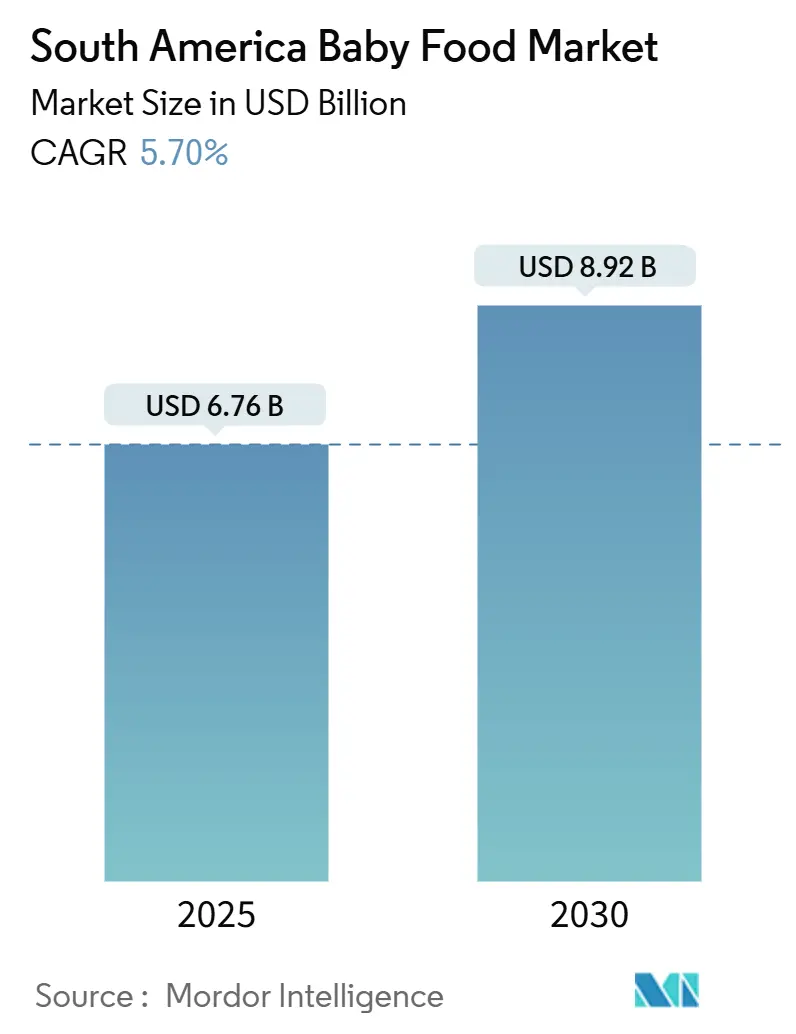

| Market Size (2025) | USD 6.76 Billion |

| Market Size (2030) | USD 8.92 Billion |

| Growth Rate (2025 - 2030) | 5.70% CAGR |

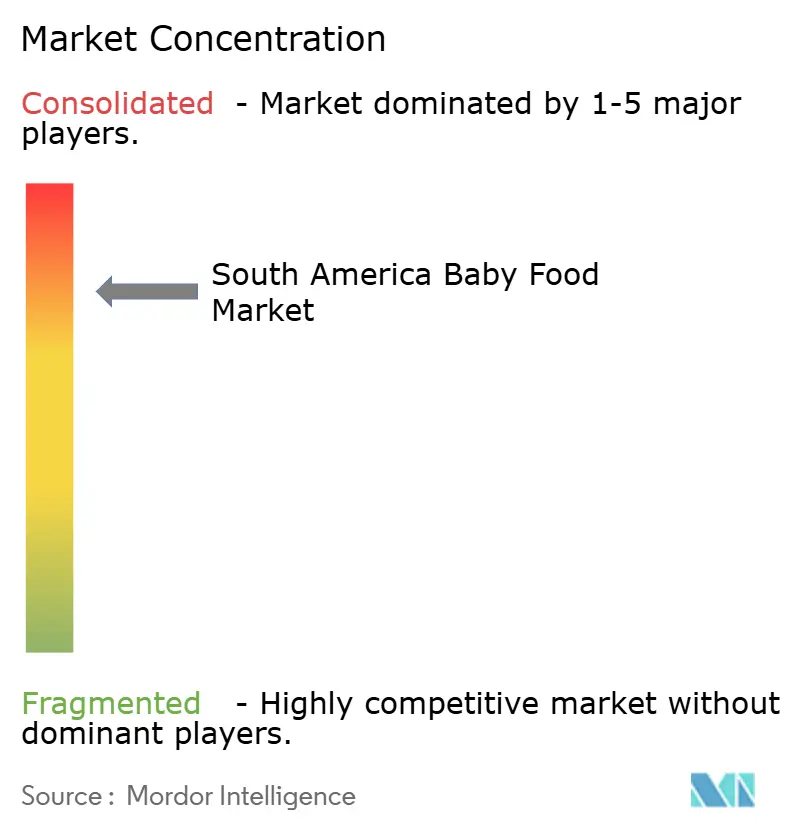

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Baby Food Market Analysis by Mordor Intelligence

The South America baby food market size is valued at USD 6.76 billion in 2025 and is projected to reach USD 8.92 billion by 2030, advancing at a 5.70% CAGR during the period. Near-term momentum stems from Brazil’s scale, Colombia’s demographic dividend, and an online sales boom, yet cost pressure from volatile dairy and grain inputs tempers expansion. Supermarket private-label rollouts, subscription-based e-commerce models, and rising clean-label adoption are reshaping channel power. Manufacturers continue to spotlight science-backed fortification and toddler-nutrition ranges to lengthen customer lifecycles while hedging raw-material risks through supply-chain partnerships. Regulatory tightening around sugar disclosure is accelerating reformulation and premiumization, even as infrastructure gaps in the Andes confine fresh-purée growth to major cities.

Key Report Takeaways

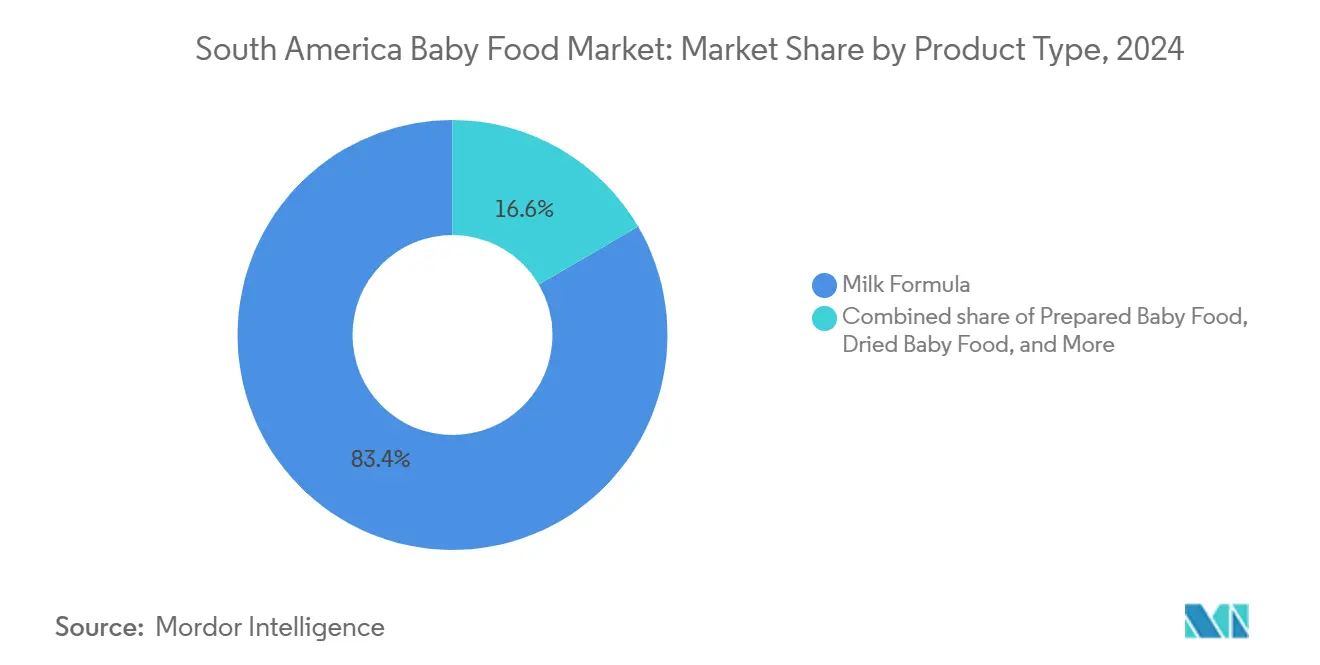

- By product type, Milk Formula led with 83.41% revenue share of the South America baby food market in 2024; Dried Baby Food is forecast to grow at a 6.57% CAGR to 2030.

- By category, Conventional SKUs held 79.11% of the South America baby food market share in 2024, while Organic products are advancing at a 7.03% CAGR through 2030.

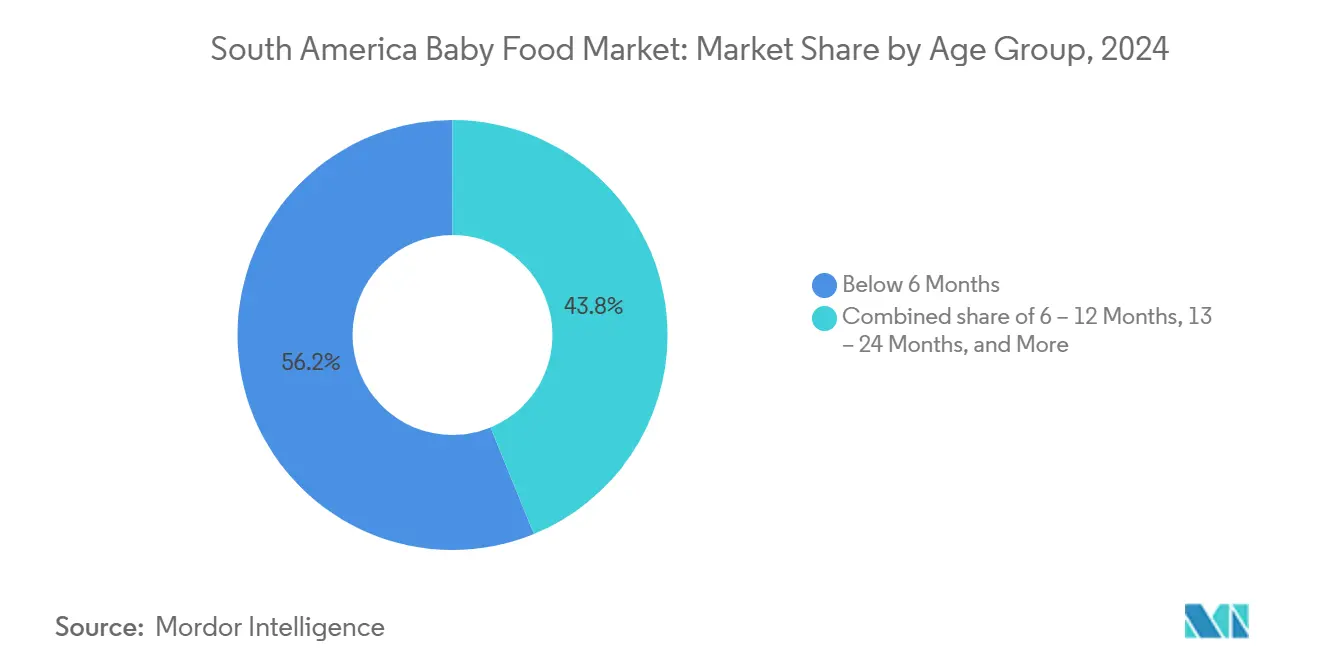

- By age group, Below 6 Months accounted for 56.19% share of the South America baby food market size in 2024 and the 13-24 Months cohort is expanding at a 6.92% CAGR to 2030.

- By distribution channel, Supermarkets/Hypermarkets captured 38.71% revenue in 2024; Online Retail Stores record the fastest 7.56% CAGR through 2030.

- By geography, Brazil contributed 42.23% of 2024 revenue, while Colombia posts the highest 6.73% CAGR outlook through 2030.

South America Baby Food Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising middle-class demand for clean-label infant nutrition in Brazil and Chile | +1.2% | Brazil, Chile; spillover to Argentina urban centers | Medium term (2-4 years) |

| Awareness regarding nutrition labeling promoting demand | +0.8% | Global, with early adoption in Brazil, Chile, Colombia | Short term (≤ 2 years) |

| Rapid expansion of online baby specialty retailers | +1.0% | Brazil, Colombia, Chile; limited Peru, rural areas | Short term (≤ 2 years) |

| Growing participation of women in workforce boosting demand | +1.1% | Global, with highest impact in Brazil, Colombia, Chile | Long term (≥ 4 years) |

| Growing popularity of plant-based diets influencing baby food choices | +0.7% | Brazil, Chile, Argentina; nascent in Colombia, Peru | Medium term (2-4 years) |

| Rise in e-commerce platforms facilitating easy access to baby food | +0.9% | Brazil, Colombia; expanding to Argentina, Chile | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Middle-Class Demand for Clean-Label Infant Nutrition in Brazil and Chile

Middle-income households in Brazil and Chile are significantly influencing the baby food market. Parents are paying closer attention to ingredient lists, avoiding products with added sugars, artificial flavors, or undisclosed additives. In Brazil, the Ministry of Agriculture (MAPA) requires organic baby foods to display the SisOrg seal. This certification ensures full traceability from farm to shelf and prohibits the use of synthetic pesticides. These strict regulations benefit established companies with integrated supply chains but create challenges for smaller brands trying to enter the market. In Chile, while regulations are less strict, many brands are voluntarily adopting clean-label standards to stand out in a market where per-capita income is growing faster than the regional average. This shift is reducing the traditional 40-50% price premium for organic products compared to conventional ones. The change is driven by economies of scale and retailers using organic products to attract more customers. The trend is particularly noticeable in cities like Santiago and São Paulo. Supermarket chains such as Cencosud and Grupo Pão de Açúcar have increased their organic baby-food shelf space by an estimated 20-25% since 2024. This expansion highlights how clean-label products are helping retailers boost basket values and encourage repeat purchases.

Growing Participation of Women in Workforce Boosting Demand

In South America, as female labor-force participation steadily climbs, the region's care infrastructure struggles to keep pace. This mismatch amplifies the demand for convenient infant-feeding solutions. According to World Bank gender profiles, women in Latin America shoulder 2-3 times the unpaid care work compared to men. This disparity tightens time constraints for working mothers, leading many to adopt formula and prepared baby foods as substitutes for partial breastfeeding. According to World Bank data, 53% of women in Brazil in 2024 are part of the labor force, highlighting the growing need for such solutions[1]World Bank Group, "Labor force participation rate, female (% of female population ages 15+) Brazil," data.worldbank.org. Meanwhile, urbanization in Colombia's major cities, Bogotá, Medellín, and Cali, has propelled female workforce participation past the 50% mark. Both trends align with increased per-capita spending on infant nutrition. The OECD highlights that 44.8% of Latin America's children under five reside in households with entirely informal employment. This demographic often faces income volatility and a lack of maternity benefits, which can shorten breastfeeding durations and hasten the shift to formula feeding. Such realities explain the 56.19% share of the "Below 6 Months" age group in 2024, as many infants, whose mothers return to work shortly after delivery, default to formula feeding. The situation is exacerbated by employers' scant provision of on-site childcare or lactation facilities. This oversight not only reinforces the trend but also bolsters the demand for milk-formula, even in light of WHO's recommendations advocating exclusive breastfeeding for the first six months.

Rapid Expansion of Online Baby Specialty Retailers

E-commerce in baby products is growing faster than the overall retail market, driven by subscription services, targeted digital marketing, and partnerships that enable next-day delivery in urban areas. In Brazil, platforms like Mercado Livre and Magazine Luiza have strengthened e-commerce infrastructure, particularly in the Southeast and South regions. This development has reduced delivery times and allowed brands to avoid traditional distributor costs. In Colombia, the adoption of digital payments, which accelerated during the pandemic and continues to grow through 2024-2025, is making transactions easier. World Bank data (2024) revealed that about 84% of Brazil’s population uses the Internet[2]International Telecommunication Union (ITU), “Individuals Using the Internet (% of Population), " itu.int. This digital surge has empowered smaller brands to reach consumers in secondary cities like Barranquilla and Cartagena without needing physical stores. Online retail stores are expected to grow at a 7.56% CAGR through 2030, surpassing supermarkets and hypermarkets by over 200 basis points. Parents prefer online shopping for its convenience, home delivery, and the ability to compare nutritional labels and reviews before buying. This shift is reducing the influence of retailers, as brands can now directly access consumer data and adjust prices or promotions in real-time. Such flexibility was not possible in the traditional trade model, which still accounts for 38.71% of distribution in 2024.

Growing Popularity of Plant-Based Diets Influencing Baby Food Choices

Environmental concerns, rising awareness of lactose intolerance, and the emergence of specialized brands have propelled plant-based infant nutrition from a niche market to the mainstream. In 2024, Harmony Baby Nutrition debuted a plant-based infant formula in Brazil, touting it as allergen-free and ideal for vegan households. While this market segment is still modest, it's witnessing rapid double-digit growth in urban areas. Danone, in November 2024, rolled out a "Dairy & Plants Blend" formula, merging 60% plant-based protein with 40% dairy. This move caters to flexitarian parents and shields the company from dairy-price fluctuations. Danone asserts that this blend boasts a 30% reduced carbon footprint per pack compared to traditional formulas. Regulatory bodies are catching up: Brazil's ANVISA and Chile's ISP now endorse soy-based formulas for infants over six months, given they match the protein and micronutrient standards of dairy counterparts. Such regulatory endorsements are easing concerns for pediatricians, who have been hesitant to recommend plant-based formulas due to past worries over amino acid completeness and calcium absorption. Despite the plant-based segment's projected growth at a 7.03% CAGR through 2030, challenges persist. Higher input costs and the lack of subsidized soy-protein supply chains, unlike those for dairy, continue to limit its scale.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited regional raw-material supply raising COGS for milks and cereals | -0.6% | Argentina, Brazil, Peru; spillover to Chile, Colombia | Medium term (2-4 years) |

| Constrained cold-chain logistics in rural Andes limiting shelf life of fresh purees | -0.5% | Peru, rural Colombia, Bolivia; limited impact in Brazil, Chile urban | Long term (≥ 4 years) |

| Shorter shelf life of products leading to potential wastage | -0.3% | Global, with acute impact in Peru, rural Brazil, Colombia | Medium term (2-4 years) |

| Regulatory hurdles may limit market growth | -0.4% | Brazil (ANVISA), Argentina (ANMAT), Chile (ISP), Colombia (INVIMA) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Regional Raw-Material Supply Raising COGS for Milks and Cereals

In South America, competing export demands and climate volatility are constraining raw-material availability, thereby squeezing margins for manufacturers of infant formula and cereals. In 2023, Brazil churned out 35.4 billion liters of milk. However, in 2024, domestic dairy prices surged. This spike was attributed to a rise in powdered-milk imports from Argentina and Uruguay. While these imports depressed local farmgate prices, they simultaneously tightened the supply available to domestic processors. After enduring years of export restrictions, Argentina's dairy sector pivoted in 2024, channeling more output to international markets. This shift diminished the volume available for regional infant-formula blending. Consequently, Brazilian and Chilean manufacturers found themselves sourcing from pricier suppliers in Europe and Oceania. Meanwhile, Brazil's grain production, hitting record aggregate levels, is increasingly diverted to animal feed and biofuel. This shift has left producers of infant cereals vying for premium-grade oats and rice, now at inflated prices. The pinch is especially felt in organic formulations, where the supply of certified-organic dairy and grains is fragmented and vulnerable to weather-induced shortfalls.

Constrained Cold-Chain Logistics in Rural Andes Limiting Shelf Life of Fresh Purees

Cold-chain infrastructure in Andean markets remains underdeveloped, limiting the distribution of fresh purees and refrigerated baby foods to major urban areas. In Peru, most cold-storage facilities are located in Lima and coastal cities, leaving highland and jungle regions dependent on ambient-stable products. These products have lower nutritional value and offer fewer options for consumers. Colombia has made progress in expanding its cold-chain capacity, but rural areas in the Andes and along the Pacific coast still lack reliable refrigerated transport. This forces retailers to stock only shelf-stable products, restricting access to premium fresh-food options for consumers in these regions. Smaller brands and local producers face additional challenges due to this infrastructure gap. Without sufficient capital to build their own cold-chain networks, they rely on third-party logistics providers, which often deliver inconsistent service. This situation creates a two-tier market. Urban consumers in cities like São Paulo, Santiago, and Bogotá have access to a wide range of products, including refrigerated purees and organic fresh foods. Meanwhile, rural and peri-urban households are limited to powdered cereals and UHT-packaged formulas. This disparity not only reinforces nutritional inequalities but also reduces the market potential for higher-margin fresh products. These premium products, which are priced 20-30% higher, require a reliable cold-chain system from production to delivery.

Segment Analysis

By Product Type: Milk Formula Anchors Volume, Dried Baby Food Captures Margin Growth

In 2024, Milk Formula dominated the product-type market with an 83.41% share. This dominance stems from low exclusive breastfeeding rates in South America, driven by maternal employment, informal work conditions, and limited lactation support. Nestlé plans to launch NAN Sinergity in June 2025 across Latin America. This formula, featuring probiotics and six human milk oligosaccharides (HMOs) designed to mimic breastmilk, highlights the scientific strategies used by major players to counter private-label competition. Positioned as a premium product, priced 15-20% higher than standard formulas, it targets middle- and upper-income families in Brazil and Chile, where parents prioritize immune-support benefits and functional ingredients. The Prepared Baby Food and Others segments accounted for the remaining 16.59% share in 2024, reflecting the market's preference for formula over ready-to-eat purees, which face distribution challenges due to shelf-life and cold-chain limitations.

Dried Baby Food is growing at a 6.57% CAGR through 2030, outpacing Milk Formula by nearly 90 basis points. Manufacturers are focusing on fortified cereals and instant porridges, which offer convenience, longer shelf life, and lower costs. Growth is concentrated in the 6-12 Months and 13-24 Months age groups, as parents transition infants to complementary foods and seek easy-to-prepare options. Brazil's ANVISA RDC 843/2024 regulation, requiring clearer labeling of added sugars and fortificants, led to reformulations with reduced sugar content. While this initially impacted sales, it has driven premiumization, with brands marketing "clean-label" products at 10-15% higher prices. An April 2024 Public Eye investigation revealed that Nestlé's Cerelac in Brazil contained 3 grams of added sugar per serving, compared to zero in Swiss formulations. This prompted faster reformulations and allowed local organic brands to gain market share with sugar-free alternatives.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Category: Conventional Scale Meets Organic Momentum

In 2024, conventional products accounted for 79.11% of the category share, reflecting the price sensitivity of mass-market consumers and the limited availability of certified-organic ingredients at scale. Established brands maintain dominance through wide distribution, strong promotions, and the ability to absorb cost increases without fully passing them to consumers, unlike smaller organic competitors. Supermarkets in Brazil and Chile have expanded private-label conventional baby food, pricing them 15-20% lower than branded products to attract price-conscious households. This competition is pressuring branded-conventional margins, prompting multinational companies to develop mid-tier "better-for-you" sub-brands that balance affordability with partial clean-label features.

Organic baby food is growing at a 7.03% CAGR through 2030, driven by supportive regulations, rising middle-class incomes, and retailers focus on premium products with higher margins. Brazil's SisOrg certification, managed by MAPA, requires organic baby foods to use traceable ingredients from audited farms, improving supply chain quality and consistency. Chile's organic market, though smaller, is growing faster as urban consumers in Santiago and Valparaíso adopt organic diets for their families. Local brands like PachaMama Orgânicos in Brazil and Biorgánicos Chile are gaining market share by offering organic purees and cereals 25-30% cheaper than multinational brands, leveraging shorter supply chains and direct-to-consumer sales. Danone's "Partner for Growth" program supports sustainable farming and emission reductions, helping the company meet rising organic demand while managing input costs.

By Age Group: Toddler Nutrition Gains as Feeding Cycles Extend

In 2024, infants below 6 months accounted for 56.19% of the market share, driven by the shift from breastfeeding to formula in households where maternal employment limits exclusive breastfeeding. Pediatric recommendations, hospital discharge protocols with formula samples, and early brand loyalty reinforce this segment's dominance. Nestlé's USD 1.1 billion investment in Brazil through 2028, including expanding its Ituiutaba plant for infant formulas and growing-up milks, highlights the importance of this cohort as a key entry point for long-term customer acquisition. The 6-12 months segment, though smaller, marks a transition as parents introduce complementary foods alongside formula or breastfeeding, increasing demand for fortified cereals and stage-2 purees. The "more than 24 months" group remains the smallest, as parents shift to family foods and reduce reliance on baby products after the second birthday.

The 13-24 months segment is growing at a 6.92% CAGR through 2030, the fastest among all age groups. Manufacturers are focusing on toddler-nutrition products that meet higher protein and micronutrient needs, supporting rapid growth and cognitive development. Danone’s November 2024 launch of a Dairy & Plants Blend formula targets flexitarian households and toddlers transitioning to plant-based diets, showcasing innovation in this segment. Brands are also using digital platforms to educate parents on toddler nutrition gaps, promoting growing-up milks and fortified snacks as essential complements to home-cooked meals. This approach resonates in urban Brazil and Colombia, where dual-income households value convenience and are willing to pay for products that simplify meal planning.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Traditional Retail Holds Ground, Digital Accelerates

In 2024, Supermarkets and Hypermarkets accounted for 38.71% of the distribution share, driven by their wide reach, strong promotions, and convenience as one-stop shops for household needs. Chains like Grupo Éxito in Colombia, Cencosud in Chile, and Carrefour in Brazil expanded baby-care sections and introduced private-label baby foods priced 15-20% lower than branded products. This strategy attracts price-sensitive shoppers while delivering higher margins. Pharmacies and Drugstores, though smaller in scale, play a key role in formula sales due to their trusted reputation and pharmacists' advisory roles. Convenience and Grocery Stores, located in urban and peri-urban areas, cater to quick purchases for households without access to larger retailers. However, limited shelf space restricts product variety, favoring established brands. The 'Others' category, including specialty baby stores and direct sales, is small but growing as brands explore experiential retail formats with product sampling, lactation consultations, and community events.

Online Retail Stores are the fastest-growing channel, with a 7.56% CAGR through 2030, fueled by improved e-commerce infrastructure and the convenience of home delivery, subscriptions, and product comparisons. In 2024, Brazil's e-commerce penetration for baby products reached 18-20%, led by platforms like Mercado Livre, offering next-day delivery and subscribe-and-save discounts that cut costs by 10-15%. Colombia's growing digital-payment adoption, accelerated during the pandemic, continues into 2024-2025, enabling smaller brands to reach secondary cities without physical stores. Nestlé's November 2024 investor presentation emphasized e-commerce as a priority, with plans to expand online operations and use generative AI for personalized content and customer service. This shift reduces retailer influence and allows brands to collect consumer data directly, transforming promotional and pricing strategies during the forecast period.

Geography Analysis

In 2024, Brazil accounted for 42.23% of regional revenue, driven by its large market size, advanced regulations, and local manufacturing by Nestlé, Danone, and Abbott. Nestlé plans to invest R$7 billion (USD 1.1 billion) by 2028 to expand its Ituiutaba infant-formula plant and modernize 18 factories for energy efficiency, aiming to counter import pressures from Argentina and competition from local organic brands. Regulatory updates by ANVISA, including IN 281/2024 and RDC 843/2024, required brands to reduce added sugars and reformulate products. While this initially impacted sales, it is now boosting premiumization as brands market “clean-label” products. E-commerce, concentrated in the Southeast and South, is growing at a 7.56% CAGR, enabling subscription models and direct-to-consumer sales that bypass distributor margins. In December 2023, Lactalis acquired DPA Brasil for USD 140 million, adding brands like Chandelle and Chamyto, along with two factories, highlighting Merger and Acquisition activity that is consolidating the market and raising entry barriers for smaller players.

Colombia is growing at a 6.73% CAGR through 2030, the fastest in the region. Urbanization in Bogotá, Medellín, and Cali, along with rising middle-class incomes and higher female workforce participation, is driving demand for convenient infant-feeding solutions. Danone’s launch of Danone Baby Nutrition Colombia S.A.S. reflects its focus on Colombia’s younger population and higher birth rates compared to Brazil and Chile, which offer strong growth potential. Digital payments, which surged during the pandemic, continue to support e-commerce growth, with baby product penetration reaching 12-15%. However, cold-chain limitations in rural Andes and Pacific regions restrict fresh puree distribution, leaving rural households reliant on shelf-stable products, which limits the premium market and widens nutritional gaps.

In 2024, Argentina, Chile, Peru, and other South American countries contributed 57.77% of regional revenue. Argentina’s dairy sector, recovering from export restrictions, is prioritizing international markets, tightening domestic supply for infant-formula production and raising costs for local manufacturers. Chile’s smaller market benefits from higher per-capita incomes and strong organic product adoption, with urban consumers in Santiago and Valparaíso favoring clean-label baby foods. Peru faces cold-chain challenges, limiting fresh puree distribution to Lima and coastal cities, while rural areas rely on powdered cereals and UHT formulas. Other South American markets, including Bolivia, Ecuador, Paraguay, and Uruguay, remain underpenetrated by multinationals, creating opportunities for regional players. However, scale and regulatory challenges constrain profitability in these markets.

Competitive Landscape

In South America, a handful of multinational brands, including the Hero Group, Sun-Maid Growers California, Nestlé SA, Danone S.A., and Abbott Laboratories, dominate the baby food market. These brands, backed by robust distribution networks and extensive marketing, have built a strong trust with consumers. Leveraging long-standing ties with retailers and healthcare professionals, these industry leaders reinforce their dominance in both infant formula and prepared baby food categories. Their scale not only facilitates continuous product innovation, especially in organic and premium formulations, but also deepens brand loyalty among consumers.

While local and niche brands are making inroads, they grapple with challenges like regulatory compliance, securing pediatric endorsements, and managing high promotional expenses. However, opportunities abound in areas like plant-based formulations, toddler nutrition platforms, and digital direct channels. In these segments, the scale advantages of established players are diminished, allowing agile challengers to carve out market share through strategic positioning and leaner operations.

Local brands like PachaMama Orgânicos in Brazil and Biorgánicos Chile are capitalizing on shorter supply chains and direct-to-consumer strategies. By offering organic products at 25-30% discounts compared to multinationals, they're appealing to middle-income families. These households, while valuing clean-label products, often find premium imports beyond their budget. Meanwhile, an April 2024 Public Eye investigation highlighted sugar-content differences in Nestlé's South American and European products. This revelation not only tarnished Nestlé's reputation but also accelerated the industry's shift towards clean labels. As a result, the competitive edge that established brands once held, due to their brand equity and distribution reach, is narrowing. Today's parents are more informed, relying on online reviews, ingredient transparency, and third-party certifications. Digital-native brands, adept at leveraging these insights, are outpacing legacy players, who often find themselves hindered by intricate organizational structures and slower decision-making processes.

South America Baby Food Industry Leaders

-

The Hero Group

-

Sun-Maid Growers California

-

Nestlé SA

-

Danone S.A.

-

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Nestlé has expanded its product line with the launch of its new science-based early-life-nutrition product, Sinergity. According to the brand, the product is now made available in markets throughout Latin America and the Middle East. According to the company, Sinergity is a blend that combines probiotics with six human milk oligosaccharides (HMOs) structurally identical to those found in breastmilk.

- October 2023: Arla Foods Ingredients has invested in a major upgrade to its facility in Argentina, enabling it to meet growing demand for high-quality whey ingredients across Latin America and globally. It has also taken the measures necessary to produce infant-formula-grade proteins in Latin America.

- November 2021: Abbott Nutrition Launched Similac 360 Total Care, a baby formula containing five HMO probiotics designed to support babies' immune systems and brain development.

South America Baby Food Market Report Scope

Baby food is any soft, easily digestible meal created particularly for human babies aged 4-6 to two years old.

The South American baby food market is segmented by type, distribution channel, and country. The market is segmented by type into milk formula, dried baby food, prepared baby food, and other baby food. The market is segmented by distribution channel into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. By geography, the market is segmented into Brazil, Argentina, and the Rest of South America.

For each segment, the market sizing and forecasts are done in value terms of USD million.

By Product Type

| Milk Formula |

| Prepared Baby Food |

| Dried Baby Food |

| Others |

By Category

| Conventional |

| Organic |

By Age Group

| Below 6 Months |

| 6 to 12 Months |

| 13 to 24 Months |

| More than 24 Months |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Pharmacies/Drugstores |

| Online Retail Stores |

| Others |

By Geography

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Product Type | Milk Formula |

| Prepared Baby Food | |

| Dried Baby Food | |

| Others | |

| By Category | Conventional |

| Organic | |

| By Age Group | Below 6 Months |

| 6 to 12 Months | |

| 13 to 24 Months | |

| More than 24 Months | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Pharmacies/Drugstores | |

| Online Retail Stores | |

| Others | |

| By Geography | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the South America baby food market?

The market is valued at USD 6.76 billion in 2025 and is projected to reach USD 8.92 billion by 2030.

Which product type holds the largest share in the South America baby food market?

Milk Formula leads with 83.41% of 2024 revenue because working parents adopt formula when exclusive breastfeeding is not feasible.

Which channel is growing fastest for infant nutrition purchases?

Online Retail Stores post a 7.56% CAGR through 2030, driven by next-day delivery, subscription discounts, and broad product comparisons.

Why is Colombia forecast to grow faster than other countries?

Urbanization, a young demographic, and expanding digital payments support a 6.73% CAGR that outpaces regional peers.

Page last updated on: