Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 11.46 Billion |

| Market Size (2030) | USD 11.81 Billion |

| Growth Rate (2025 - 2030) | 0.61% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Aviation Market Analysis by Mordor Intelligence

The South America Aviation Market size is estimated at USD 11.46 billion in 2025, and is expected to reach USD 11.81 billion by 2030, at a CAGR of 0.61% during the forecast period (2025-2030).

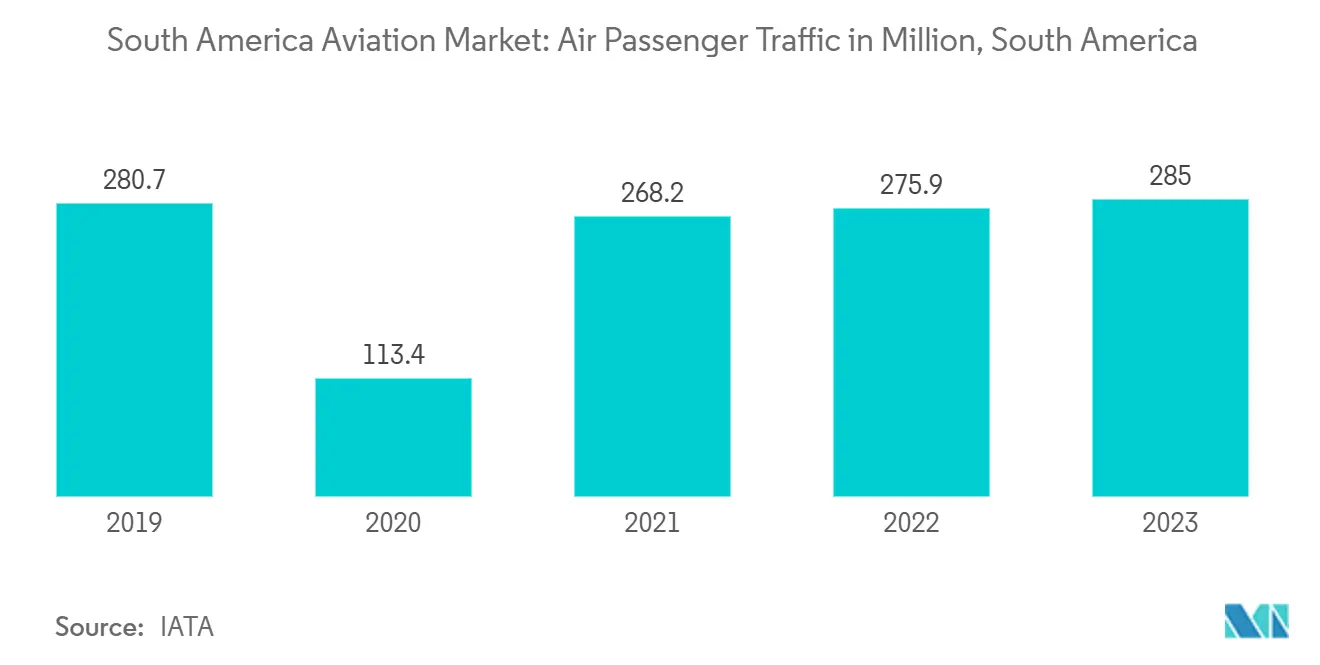

The South American aviation market is experiencing a resurgence, driven by increasing demand for domestic travel and cargo services, as well as the growth of low-cost carriers. As travel restrictions ease, passenger flows within the region and toward North America have rebounded, bolstering overall passenger traffic. Countries such as Chile, Colombia, and Argentina are experiencing an expansion in aviation services within the Rest of South America. In 2023, the region experienced a total of 47.6 million air passenger trips, a slight decrease from 48.2 million in 2022.

Several countries, including Brazil and Peru, are moving towards privatizing their airports. This strategic move is poised to enhance airport infrastructure and capacity, as well as bolster the region's general aviation market. Despite economic challenges and the lingering effects of the pandemic, South American nations are gearing up to modernize their military aircraft fleets. This move aims to bolster their armed forces and drive growth in the military aviation sector.

South America Aviation Market Trends and Insights

The Commercial Aircraft Segment will Dominate the Market During the Forecast Period

South America's commercial segment is poised to dominate the market, driven by a surge in aircraft deliveries and passenger traffic. Historically, airlines like Colombia's SCADTA (now Avianca) and Brazil's VARIG expanded their networks with Boeing aircraft, underscoring the region's appetite for new planes. Airbus will deliver 2,550 new aircraft in South America from 2022 to 2041, nearly doubling the existing fleet from 1,450 to an estimated 2,850.

While South America is expected to rank second to last in projected aircraft deliveries over the next two decades, it surpasses Africa, anticipating 1,230 deliveries and 370 conversions. Notably, 81% of South America's existing fleet comprises narrowbody aircraft, a trend set to intensify as Airbus forecasts that 92% of upcoming deliveries will be narrowbody jetliners. This preference for narrowbodies is further fueled by the region's growing low-cost carrier segment, which leverages these planes for enhanced efficiency and increased traffic.

Highlighting the region's fleet modernization, Bolivia's national carrier unveiled plans in March 2022 to replace its aging fleet, including B737-300s (26.3 years old) and B767-300ERs (27.2 years old), with newer models like the Airbus A330-200s and B737-800s. Similarly, in the same month, Avianca, a prominent Colombian airline, inked a deal with Airbus for 88 A320 neo aircraft, aligning with its strategic fleet expansion, set for integration between 2025 and 2031.

Brazil will Showcase Significant Growth During the Forecast Period

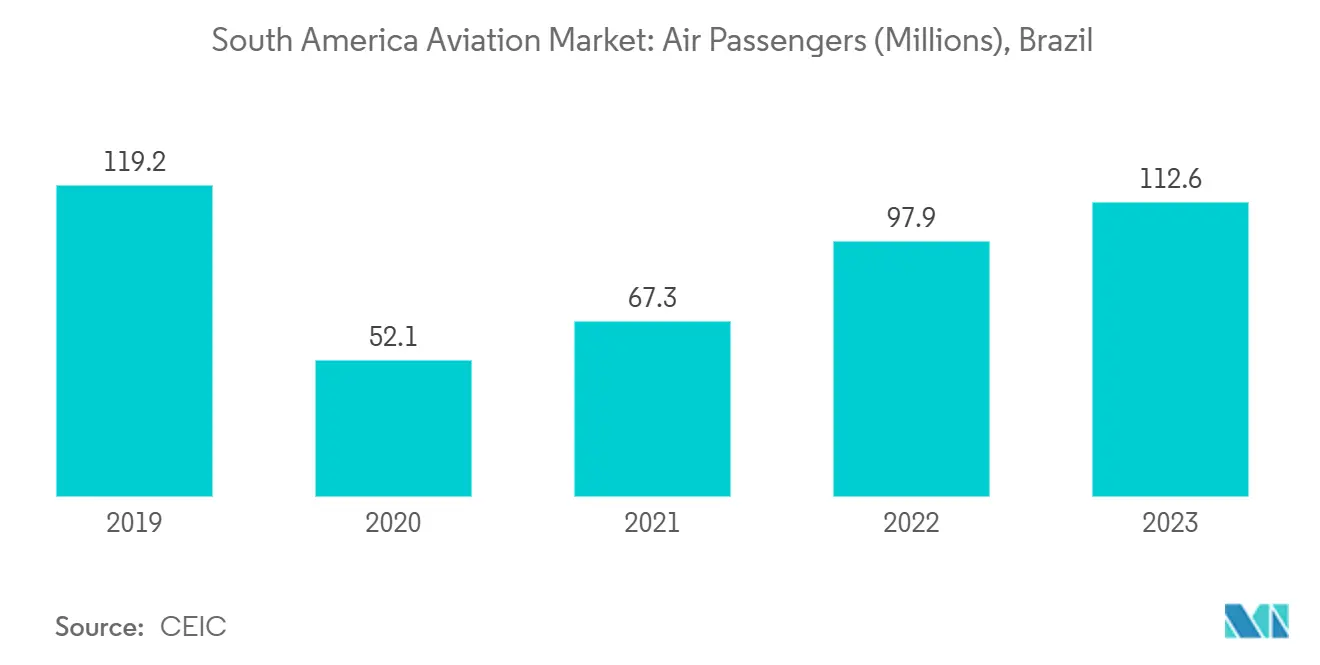

The burgeoning middle class in Brazil is propelling the demand for air travel. With more individuals entering the middle-income bracket, domestic air traffic is witnessing a notable uptick. Additionally, as discretionary spending rises, Brazilians increasingly explore domestic and international destinations, further fueling the demand. In 2023, the number of passengers traveling on domestic and international flights in Brazil surged to 112.6 million, reflecting a 15.3% rise from the previous year's 97.6 million. Introducing low-cost carriers (LCCs) has been a transformative move in the Brazilian aviation landscape. These carriers have reshaped air travel dynamics by offering competitive pricing, appealing to budget-conscious travelers, and spurring interest in short-haul routes.

By December 2023, GOL Airlines, a prominent LCC in Brazil, had a backlog of 91 B737 MAX aircraft. By the end of 2023, GOL Airlines was expected to have 53 B737 MAX planes, making them 50% of its fleet by 2025. In a strategic move, Azul announced the acquisition of seven Airbus A330neos in February 2024, with deliveries slated to commence in 2026.

Brazil leads South America in the number of active general aviation aircraft, with over a third of the region's total fleet based in the country. In 2023, Brazil's business jets constituted 58% of South America's fleet, with Cessna (a Textron Inc. subsidiary) and Embraer being the primary manufacturers. Furthermore, in September 2022, Brazil's armed forces, under the Combat Aircraft Programme Coordinating Committee (COPAC), procured 27 single-engine H125 helicopters. These helicopters are set to enhance the training capabilities of the Brazilian Navy and Air Force, replacing the aging AS350 and Bell 206 models. Such strategic acquisitions, spanning military and civilian aircraft, are poised to drive market demand in Brazil in the coming years.

Competitive Landscape

The South American aviation market is consolidated and is dominated by a few key players, including Lockheed Martin Corporation, Embraer SA, Bombardier Inc., Airbus SE, and The Boeing Company. With a surge in air passengers, the demand for new aircraft in the region has risen. Consequently, several South American aircraft manufacturers have increased production capacities to meet this demand. Notably, government initiatives propel the market's growth, primarily through support for indigenous aircraft development and manufacturing.

Anticipated innovations in aircraft design are set to revolutionize safety, comfort, and efficiency for passengers and manufacturers. Companies are eagerly eyeing these technological advancements to bolster their market shares. Moreover, collaborative efforts among multiple countries to develop new military aircraft models are poised to significantly benefit local players.

South America Aviation Industry Leaders

-

Embraer SA

-

Airbus SE

-

Lockheed Martin Corporation

-

Bombardier Inc.

-

The Boeing Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2024: The Argentine Air Force signed a deal to procure a Basler BT-67 turboprop utility aircraft. This acquisition fell under an FMS agreement greenlit by the US State Department. Alongside the primary aircraft, the Argentine government secured additional equipment, including spare engines, logistics, and training support, totaling USD 143 million. Notably, the aircraft is powered by PT6A-67R turboprop engines sourced from Pratt & Whitney Canada.

- September 2022: Avianca and Boliviana de Aviación unveiled an interline agreement, enabling seamless connections for their passengers. This collaboration streamlined travel, allowing passengers to journey to and from seven Bolivian cities with a single ticket. Travelers can check their luggage straight through to their final destination. The partnership allowed access to approximately 125 Avianca routes, facilitating connections to 24 countries across South America and Europe.

South America Aviation Market Report Scope

The South American aviation market encompasses the sales of fixed-wing and rotary-wing aircraft in the region's commercial, military, and general aviation sectors. The report offers the latest trends, size, share, and market overview.

The South American aviation market is segmented by type and geography. By type, the market is segmented into commercial, military, and general aviation. The report also covers the market sizes and forecasts for the three countries across the region. For each segment, the market size is provided in terms of value (USD).

By Type

| Commerical Aircraft |

| Military Aircraft |

| General Aviation |

By Geography

| Brazil |

| Argentina |

| Rest of South America |

| By Type | Commerical Aircraft |

| Military Aircraft | |

| General Aviation | |

| By Geography | Brazil |

| Argentina | |

| Rest of South America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the South America Aviation Market?

The South America Aviation Market size is expected to reach USD 11.46 billion in 2025 and grow at a CAGR of 0.61% to reach USD 11.81 billion by 2030.

What is the current South America Aviation Market size?

In 2025, the South America Aviation Market size is expected to reach USD 11.46 billion.

Who are the key players in South America Aviation Market?

Embraer SA, Airbus SE, Lockheed Martin Corporation, Bombardier Inc. and The Boeing Company are the major companies operating in the Latin America Aviation Market.

What years does this South America Aviation Market cover, and what was the market size in 2024?

In 2024, the South America Aviation Market size was estimated at USD 11.39 billion. The report covers the Latin America Aviation Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Latin America Aviation Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: