Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

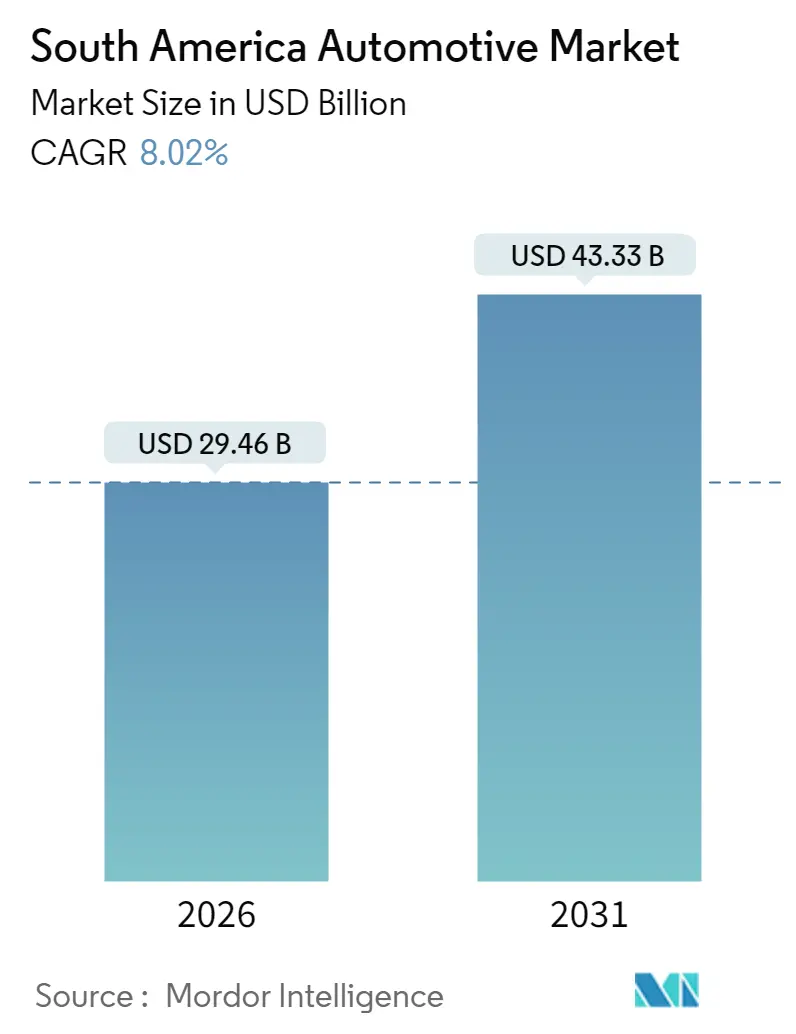

| Market Size (2026) | USD 29.46 Billion |

| Market Size (2031) | USD 43.33 Billion |

| Growth Rate (2026 - 2031) | 8.02% CAGR |

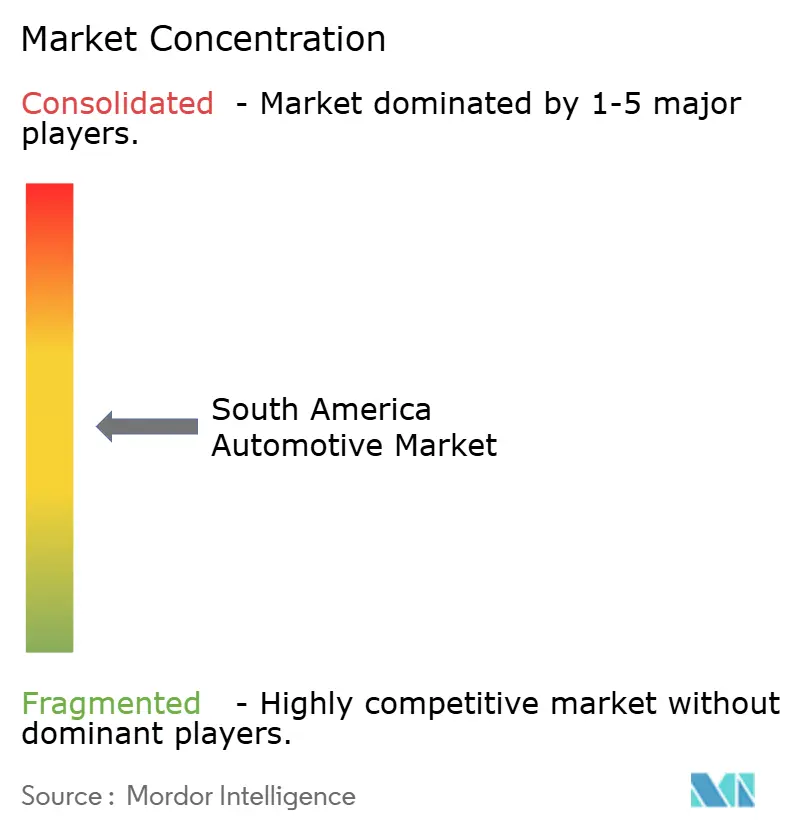

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Automotive Market Analysis by Mordor Intelligence

The South American automotive market is expected to grow from USD 27.28 billion in 2025 to USD 29.46 billion in 2026 and is forecast to reach USD 43.33 billion by 2031 at 8.02% CAGR over 2026-2031. The South American automotive market continues to benefit from swift infrastructure spending, flexible-fuel policy enhancements such as Brazil’s E30 mandate, and the proliferation of digital retail platforms that shorten purchase cycles and expand consumer reach. Elevated borrowing costs and semiconductor shortages continue to pose near-term headwinds, yet resilient household consumption and an expanding middle class underpin the region’s long-term growth profile. Competitive intensity has risen as Stellantis commits EUR 5.6 billion through 2030, and Chinese OEMs localize production to avoid rising Mercosur tariffs, all of which is reshaping the product mix, technology adoption, and supplier ecosystems.

Key Report Takeaways

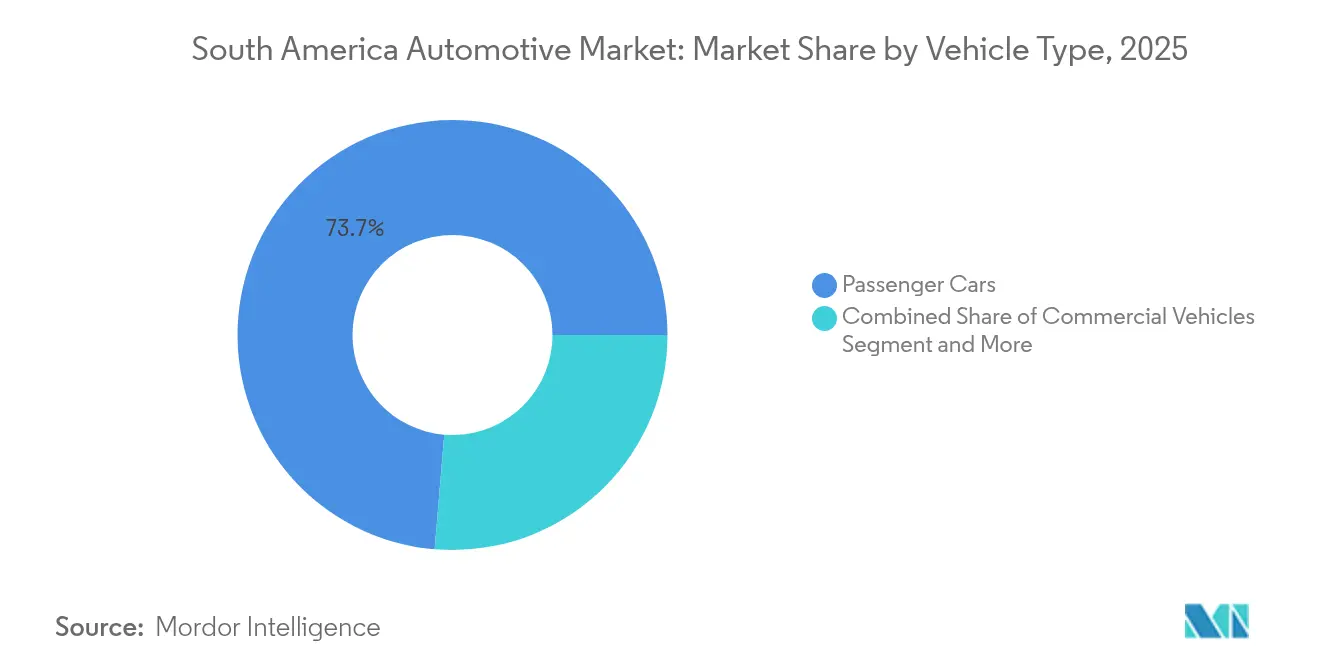

- By vehicle type, passenger cars captured 73.68% of the South American automotive market share in 2025, and this segment is expected to advance at a 11.95% CAGR through 2031.

- By propulsion, internal-combustion engines held 72.95% of the South American automotive market share in 2025, whereas battery electric vehicles represented the fastest trajectory at an 11.15% CAGR.

- By sales channel, dealer and retail Sales retained a 53.02% share in 2025; online direct-to-consumer platforms are growing at an 11.25% CAGR.

- By end user, individual buyers accounted for 62.74% of demand in 2025; however, mobility operators are expanding at a 11.12% CAGR.

- By country, Brazil commanded 60.85% of the South American automotive market share in 2025, while Colombia is set to rise at a 12.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Automotive Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regional OEM Platforms | +2.1% | Brazil and Argentina hubs | Long term (≥ 4 years) |

| GDP and Credit Rebound | +1.8% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Chinese EVs via Mercosur | +1.5% | Brazil, Argentina | Medium term (2-4 years) |

| Brazil Flex-Fuel Incentives | +1.2% | Primarily Brazil, spillover Mercosur | Long term (≥ 4 years) |

| Digital Trade-In Platforms | +0.9% | Major urban centers | Short term (≤ 2 years) |

| Mining-Funded EV Subsidies | +0.7% | Chile, Peru, Colombia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

OEM Investments in Regional Vehicle Platforms

In South America, growing sales of traditional and electrified vehicles and heightened investments from major players like Volkswagen AG and Stellantis NV have increased profitability. Stellantis alone invested EUR 5.6 billion, the most significant single commitment in regional history [1]“Investment Plan South America 2025-2030,”, Stellantis, stellantis.com. Volkswagen AG allocated USD 580 million to an Argentina-based Amarok program tailored to local duty-cycle needs. At the same time, Toyota Motor and BMW Group announced multi-year expansions focusing on hybrid and flex-fuel drivetrains. Joint projects such as the GM-Hyundai collaboration covering five models and targeting 800,000 annual sales illustrate a pivot toward shared cost structures and accelerated product cadence. These localized platforms reduce currency risk, meet regional regulatory norms, and leverage Mercosur tariff preferences, collectively enhancing the competitiveness of the South American automotive market.

Post-Pandemic Rebound in GDP and Consumer Credit Availability

Regional GDP is projected to increase by 2.5% in 2025, up from 1.9% the previous year, which is expected to lift household incomes and stimulate automotive lending, even as benchmark rates remain elevated [2]“World Economic Situation and Prospects 2025,”, United Nations, un.org. Brazil's economy expanded by 3.4% in 2024, with an unemployment rate of 6.5%, creating a supportive backdrop for vehicle purchases. Argentina’s reforms have cut monthly inflation to 2.8%, unlocking new credit channels for auto buyers, while Colombia’s manufacturing output is growing annually, reinforcing the momentum in the South American automotive market. Although financing costs remain restrained, easing monetary conditions across most central banks should gradually revive loan accessibility. Stronger macroeconomic fundamentals are expected to translate into higher showroom traffic and order backlogs throughout 2025.

Chinese OEM Green-Field EV Plants Using Mercosur Tariff Breaks

BYD’s complex in Bahia became operational in July 2025, with an annual capacity of 50,000 units, setting the stage for duty-free exports within Mercosur [3]“Camaçari Plant Inauguration,”, BYD Company, byd.com. Great Wall Motor repurposed a former Mercedes-Benz facility, meeting 40% local-content thresholds to qualify for tariff exemptions. Shared facilities such as the Renault-Geely tie-up in Paraná blend existing infrastructure with Chinese manufacturing discipline, yielding faster scale-up at lower capital intensity. Local footprints neutralize Brazil’s scheduled EV import tariff rise to 35% by mid-2026, keeping sticker prices competitive. Combined, these moves fortify China’s position in the South American automotive market while accelerating technology transfer to local supply bases.

Digitally Enabled Used-Car Platforms Boosting Trade-Ins

Online players like Kavak are entering Brazil to capitalize on the used-car market. AI-driven appraisal engines offer transparent pricing, which raises consumer trust and speeds up transaction times. Cross-border partnerships such as Auto Avaliar with Argentina-based Karvi extend platform footprints, linking inventory across Mercosur and enhancing liquidity. Dealers increasingly integrate these tools to widen reach and convert trade-ins into new-car sales, improving lot turnover. The net effect is a more efficient secondary market that indirectly supports new-vehicle demand in the South American automotive market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Financing and Inflationary Vehicle Costs | -1.9% | Brazil dominant, regional spillover | Short term (≤ 2 years) |

| Semiconductor Supply Volatility | -1.1% | Brazil, Mexico hubs | Medium term (2-4 years) |

| Port Delays for CKD and Battery Imports | -0.8% | Brazil, Argentina ports | Short term (≤ 2 years) |

| Charging Network Distrust | -0.6% | Regional EV corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Elevated Financing Rates and Inflation-Driven Vehicle Prices

Brazil’s Selic rate climbed to 14.25% in 2025, pushing automotive loan coupons as high as and squeezing affordability[4]“Monetary Policy Committee Minutes, June 2025,”, Banco Central do Brasil, bcb.gov.br. Although Argentina’s inflation has moderated, peso volatility keeps lending spreads wide, while regional currency fluctuations cloud import-price visibility. OEMs now offer tenures and subsidized rates, but credit penetration still lags pre-pandemic norms. Consequently, near-term volumes in the South American automotive market may undershoot potential until monetary conditions ease.

Semiconductor Supply Volatility for Local Assembly

Flood-induced shutdowns at suppliers in Rio Grande do Sul halted Volkswagen's production lines, illustrating how localized shocks ripple through just-in-time inventory models. Brazil lacks a domestic chip foundry capable of automotive-grade output, making OEMs dependent on Asian imports vulnerable to logistics snarls. The shortage disproportionately affects BEVs that require battery-management ICs, jeopardizing rollout schedules. Automakers have begun redesigning platforms around multi-sourcing strategies, yet full resilience remains several years away. Intermittent stoppages, therefore, continue to weigh on capacity utilization across the South American automotive market.

Segment Analysis

By Vehicle Type: Passenger Cars Dominate Growth

Passenger cars accounted for 73.68% of the South American automotive market size in 2025 and are projected to expand at a 11.95% CAGR through 2031, benefiting from rising urbanization and middle-class income gains. SUVs and crossovers lead the surge, prized for higher seating positions and perceived safety, whereas compact sedans preserve a foothold due to fuel efficiency at premium pump prices. Though smaller in unit terms, commercial vehicles underpin logistics in agriculture and mining corridors, with light pickups favored by Brazilian farms and heavy trucks powering Chilean copper exports. Two-wheelers are proliferating in congested megacities as cost-effective mobility, while off-highway equipment enjoys tailwinds from public works spending.

The passenger-car momentum is reinforced by Stellantis’ plan to launch more than 40 new products by 2030, many of them on localized platforms geared to flexible-fuel drivetrains. Financing promotions aim to mitigate loan-rate headwinds that otherwise dampen showroom traffic. Meanwhile, used-car digital platforms improve trade-in liquidity, lowering the effective upgrade cost and sustaining turnover. The vehicle-type mix underscores how the South American automotive market balances personal-mobility aspirations with commercial transport imperatives.

Note: Segment shares of all individual segments available upon report purchase

By Propulsion Type: ICE Dominance Faces Electric Disruption

Internal-combustion engines retained 72.95% of the South American automotive market in 2025; however, battery electrics are accelerating at a 11.15% CAGR as fiscal incentives and localized Chinese production narrow the price gaps. Brazil’s E30 scheme provides a cost-parity hedge for flex-fuel engines, reducing gasoline imports and increasing domestic ethanol demand. Hybrids serve as a bridge technology, especially ethanol-compatible variants that achieve greater emission reductions compared to gasoline equivalents.

Diesel retains relevance in heavy-duty routes that span thousands of kilometers, while CNG finds niche use in municipal fleets where refueling networks exist. Fuel-cell exploration is nascent but gaining attention following Hyundai’s USD 1.1 billion hydrogen roadmap for Brazil. As import tariffs on C-segment BEVs rise to 35% by 2026, localized motor and battery plants are expected to protect affordability and accelerate adoption, gradually shifting the propulsion landscape of the South American automotive market.

By Sales Channel: Digital Transformation Accelerates

Dealer and retail sales still accounted for 53.02% of 2025 sales, but online direct-to-consumer models are forecasted to grow at an annual rate of 11.25% to 2031. Pandemic-era buying habits moved research and financing pre-approval online, and platforms now integrate virtual showrooms, AI-guided configurators, and instant trade-in quotes. Dealers are increasingly pivoting to experience centers that focus on after-sales care, extended warranties, and subscription services. Fleets and corporate buyers prioritize total cost of ownership and telematics integration, whereas OEM-direct sales remain largely confined to premium EV launches that bundle charging equipment and software.

Cross-border e-commerce is also emerging as websites harmonize pricing across Mercosur duties, providing regional shoppers with transparent, landed-cost quotes. As broadband penetration climbs, the digital channel’s share of the South American automotive market is expected to rise steadily, supported by fintech partnerships that deliver near-instant loan approvals and dynamic insurance offers.

Note: Segment shares of all individual segments available upon report purchase

By End User: Individual Consumers Drive Mobility Evolution

Private buyers generated 62.74% of 2025 vehicle demand, reflecting the enduring appeal of personal mobility amid improving employment and wage trends. Millennials and Gen Z urbanites, however, increasingly opt for ride-hailing or car-sharing services, propelling demand for mobility operators at an 11.12% CAGR. Small-enterprise fleets expand alongside e-commerce logistics, while large corporates deploy advanced telematics to optimize routing and fuel spend. Government fleets maintain steady replacement cycles driven by public service mandates and green procurement policies.

Shifts toward usage-based insurance, subscription models, and pay-per-mile financing encourage flexible ownership structures, gradually diversifying end-user profiles. These dynamics signal that the South American automotive market is evolving from a pure ownership paradigm to a hybrid mix of possession and shared access modes.

Geography Analysis

Brazil represented 60.85% of the South American automotive market size in 2025. Brazil’s commanding position rests on deep industrial roots, a supportive flex-fuel ecosystem, and high consumer volumes. Record OEM commitments, led by Stellantis’ EUR 5.6 billion pledge, underscore confidence in domestic scale even as interest rates challenge affordability. Meanwhile, escalating EV import duties have already catalyzed local battery and motor production, ensuring longer-term cost competitiveness within the South American automotive market.

Colombia, although smaller, is the standout growth engine, with a 12.74% CAGR. Colombia is translating manufacturing momentum and favorable demographics into double-digit sales growth, aided by strategic export corridors to Central America. Investment incentives, including free-trade zones and tariff relief on advanced components, further encourage vehicle assembly localization, positioning the country as an emerging sub-regional hub.

Argentina’s macro reset curbed inflation and stabilized the peso sufficiently to resurrect consumer confidence and unlock delayed fleet purchases. Mining-rich Chile and Peru use royalty revenues and aggressive depreciation schemes to seed EV adoption. At the same time, smaller economies such as Ecuador leverage transport-infrastructure upgrades to catalyze first-time ownership. These geographic vectors reveal a South American automotive market whose demand is concentrated in Brazil and increasingly diversified across fast-rising neighbors.

Competitive Landscape

The competitive arena has shifted from a tight oligopoly toward moderate concentration as Chinese newcomers, digital disruptors, and cross-OEM alliances gain share. High-profile collaborations such as GM-Hyundai and Renault-Geely highlight a strategic pivot toward shared architectures that reduce cost and accelerate launch cycles. Investment intensity is at an all-time high; Toyota’s USD 2 billion hybrid push and BMW’s USD 200 million tech upgrade signal that established brands are unwilling to cede ground.

White-space opportunities are most visible in rural distribution, mobility services, and premium electrified nameplates where European marques retain cachet. Digital retail giants like Kavak and MercadoLivre Auto are redrawing the dealer landscape by injecting AI-based pricing and seamless financing that compress gross margins but lift turnover. Meanwhile, supply-chain constraints spur vertical integration, with OEMs negotiating direct contracts for lithium, semiconductors, and bio-ethanol to shield production against volatility.

Regulatory frameworks, particularly Brazil’s decarbonization tax credits and looming CO₂ ceilings, favor players capable of flex-fuel hybrid or full-electric platform flexibility. As capacity additions outpace demand growth, price competition will intensify, raising the prospect of consolidation among mid-tier assemblers. Overall, technology prowess, local content, and channel agility will define leadership in the South America automotive market.

South America Automotive Industry Leaders

General Motors

Stellantis NV

Volkswagen AG

Toyota Motor Corporation

Ford Motor Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: General Motors and Hyundai revealed plans to co-develop five vehicles for Central and South America, aiming for 800,000 annual sales by 2028.

- April 2025: Volkswagen allocated USD 580 million to develop the next-gen Amarok at its Pacheco, Argentina, facility.

South America Automotive Market Report Scope

The South America Automotive Market Report is Segmented by Vehicle Type (Passenger Cars, Commercial Vehicles, Two-Wheelers, and Off-Highway Vehicles), Propulsion Type (Internal-Combustion Engine and Electrified Vehicles), Sales Channel (OEM/Direct, Dealer/Retail, and More), End User (Individual/Private, SME Fleets, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

By Vehicle Type

| Passenger Cars | Hatchbacks |

| Sedans | |

| SUVs and Crossovers | |

| MPVs | |

| Commercial Vehicles | Light Commercial Pick-ups |

| Light Commercial Vans | |

| Heavy Trucks | |

| Buses and Coaches | |

| Two-Wheelers | Motorcycles |

| Scooters/Mopeds | |

| Off-Highway Vehicles | Agricultural Tractors |

| Construction Equipment |

By Propulsion Type

| Internal-Combustion (ICE) | Gasoline |

| Diesel | |

| Flexible-Fuel (Ethanol) | |

| Natural Gas (CNG/LNG) | |

| Electrified Vehicles | Battery-Electric (BEV) |

| Hybrid Electric (HEV) | |

| Plug-in Hybrid (PHEV) | |

| Fuel-Cell (FCEV) |

By Sales Channel

| OEM / Direct Sales |

| Dealer and Retail Sales |

| Fleet and Corporate Sales |

| Online Direct-to-Consumer |

By End User

| Individual / Private Consumers |

| Small and Medium Enterprise Fleets |

| Large Corporate Fleets |

| Government and Municipal Fleets |

| Mobility Operators (Ride-hailing, Car-sharing) |

By Country

| Brazil |

| Argentina |

| Chile |

| Peru |

| Colombia |

| Ecuador |

| Rest of South America |

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| SUVs and Crossovers | ||

| MPVs | ||

| Commercial Vehicles | Light Commercial Pick-ups | |

| Light Commercial Vans | ||

| Heavy Trucks | ||

| Buses and Coaches | ||

| Two-Wheelers | Motorcycles | |

| Scooters/Mopeds | ||

| Off-Highway Vehicles | Agricultural Tractors | |

| Construction Equipment | ||

| By Propulsion Type | Internal-Combustion (ICE) | Gasoline |

| Diesel | ||

| Flexible-Fuel (Ethanol) | ||

| Natural Gas (CNG/LNG) | ||

| Electrified Vehicles | Battery-Electric (BEV) | |

| Hybrid Electric (HEV) | ||

| Plug-in Hybrid (PHEV) | ||

| Fuel-Cell (FCEV) | ||

| By Sales Channel | OEM / Direct Sales | |

| Dealer and Retail Sales | ||

| Fleet and Corporate Sales | ||

| Online Direct-to-Consumer | ||

| By End User | Individual / Private Consumers | |

| Small and Medium Enterprise Fleets | ||

| Large Corporate Fleets | ||

| Government and Municipal Fleets | ||

| Mobility Operators (Ride-hailing, Car-sharing) | ||

| By Country | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Ecuador | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will vehicle sales in South America be by 2031?

At an 8.02% CAGR, the South America automotive market is projected to reach USD 43.33 billion in value by 2031, implying sustained unit growth over the period.

Which country is expanding fastest in regional auto demand?

Colombia is forecast to post a 12.74% CAGR through 2031 thanks to rapid industrialization and supportive assembly incentives.

How are online sales channels evolving?

Direct-to-consumer platforms are rising 11.25% annually as buyers seek transparent pricing and streamlined financing.

What policies are boosting alternative fuels?

Brazil’s E30 ethanol mandate and the wider “Fuel of the Future” framework are spurring flex-fuel uptake and slashing gasoline imports.

Which propulsion technology is gaining the most ground?

Battery electric vehicles are on an 11.15% CAGR, supported by local Chinese OEM production and royalty-funded purchase subsidies in mining-rich countries.

Page last updated on: