Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

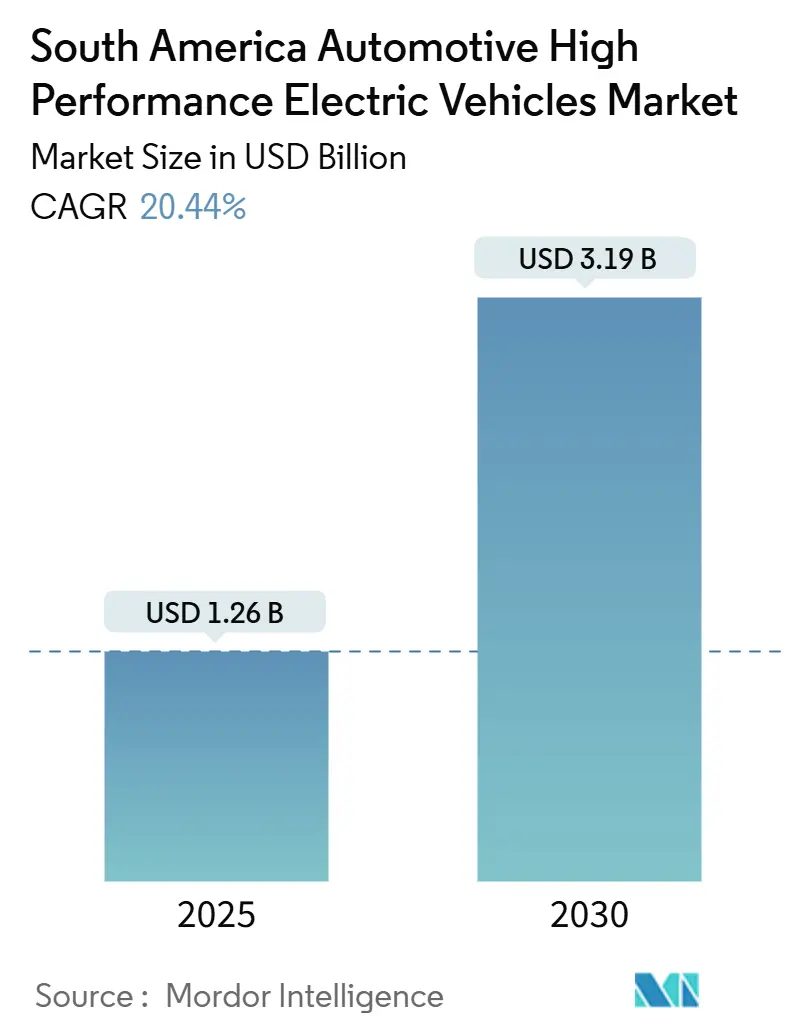

| Market Size (2025) | USD 1.26 Billion |

| Market Size (2030) | USD 3.19 Billion |

| Growth Rate (2025 - 2030) | 20.44% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Automotive High Performance Electric Vehicles Market Analysis by Mordor Intelligence

The South American automotive high-performance electric vehicle market was valued at USD 1.26 billion in 2025 and is forecast to reach USD 3.19 billion by 2030, exhibiting a 20.44% CAGR from 2025 to 2030. This sustained expansion reflects several intertwined forces, including the aggressive entry of Chinese OEMs, large-scale localization commitments from incumbent automakers, and regional supply-chain integration anchored in the lithium triangle. Passenger vehicles dominate sales volume, yet light commercial fleets accelerate faster as last-mile delivery operators chase operating-cost savings. Flex-fuel heritage keeps plug-in hybrids in the lead today, but battery-electric adoption is climbing quickly as public DC corridors roll out and price-performance parity improves. Policy remains a double-edged sword: Brazil’s MOVER program rewards low-emission vehicles even as the ethanol lobby slows full BEV incentives, creating a nuanced playing field for manufacturers and investors.

Key Report Takeaways

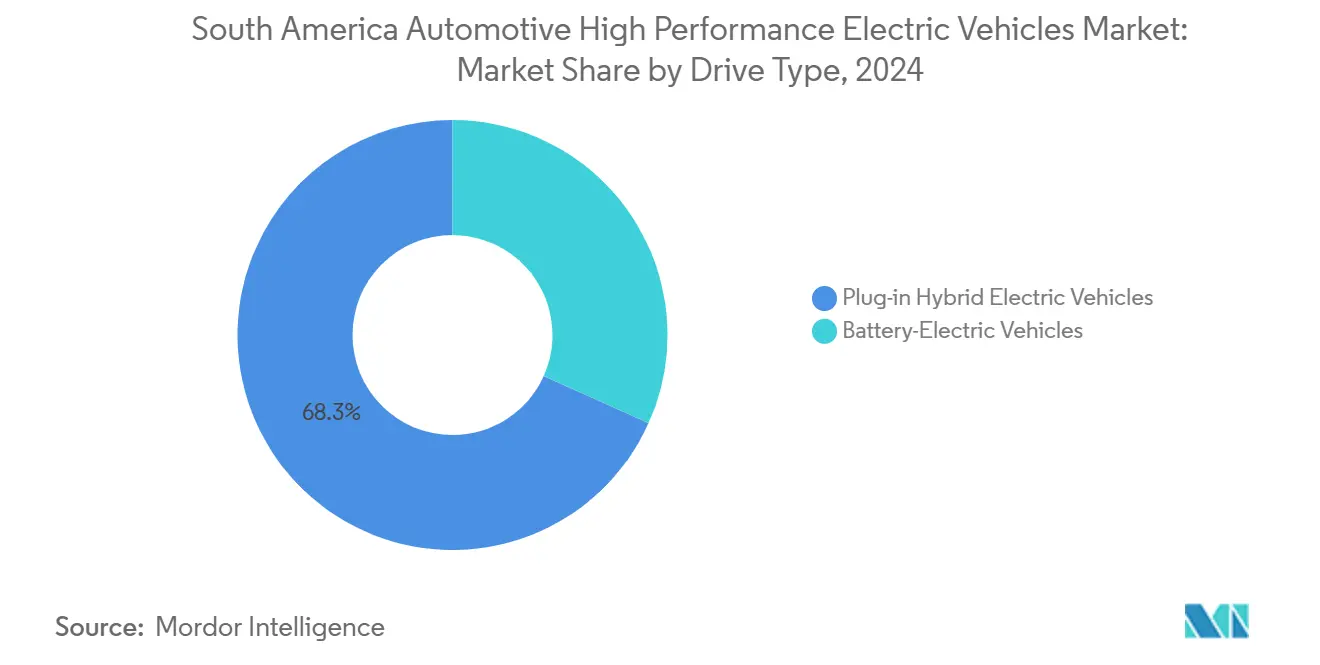

- By drive type, plug-in hybrids led with 68.28% of South America electric vehicle market share in 2024, while battery-electric vehicles are projected to expand at an 18.23% CAGR to 2030.

- By vehicle type, passenger cars accounted for 86.34% of the South America electric vehicle market size in 2024, whereas light commercial vehicles are advancing at a 19.73% CAGR through 2030.

- By peak power output, the 201-400 kW segment captured 56.23% share of the South America electric vehicle market size in 2024; systems above 400 kW are set to grow at a 17.21% CAGR.

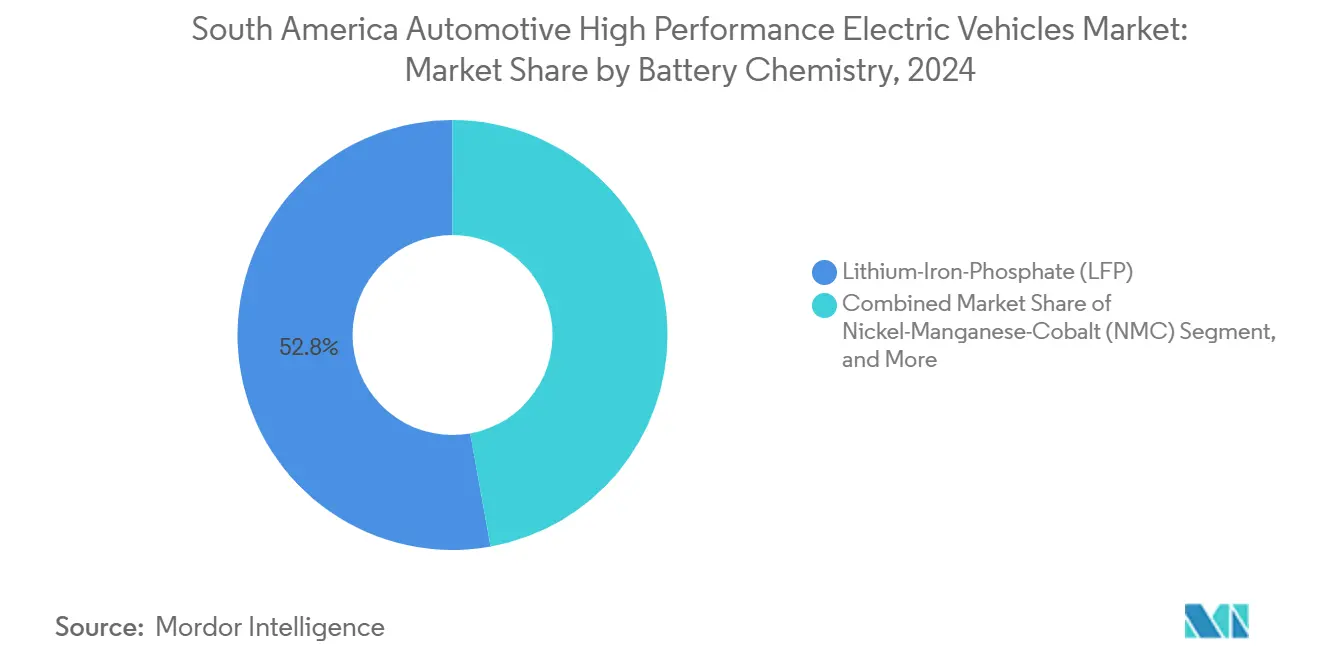

- By battery chemistry, lithium iron phosphate held 52.83% share of the South America electric vehicle market size in 2024, while nickel manganese cobalt batteries record the fastest 21.43% CAGR.

- By price band, sub-USD 50,000 models commanded 58.18% share of the South America electric vehicle market size in 2024; the USD 50,001-75,000 bracket is rising at a 16.78% CAGR.

- By geography, Brazil controlled 65.61% of South America electric vehicle market share in 2024, whereas Uruguay is forecast to post the quickest 19.74% CAGR to 2030.

South America Automotive High Performance Electric Vehicles Market Trends and Insights

Drivers Impact Analysis

| Driver | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integrating Lithium-Triangle Supply Chains into Regional BEV Builds | +4.1% | Chile, Argentina, Bolivia production, Brazil assembly | Long term (≥ 4 years) |

| Rapid Expansion of Public DC Fast-Charging Corridors | +3.2% | Brazil, Chile, Argentina core markets | Medium term (2-4 years) |

| Chinese Premium-Value Entrants Closing Price-Performance Gap | +3.7% | Brazil, Argentina, Chile with regional expansion | Medium term (2-4 years) |

| Rising Performance-EV Imports Helped By Mercosur Tariff Waivers | +2.8% | Brazil, Argentina, Uruguay with spillover to Paraguay | Short term (≤ 2 years) |

| OEM Localisation - E.G., BMW Araquari PHEV Line-Up | +2.1% | Brazil manufacturing hub, regional exports | Long term (≥ 4 years) |

| Prestige Motorsport Marketing (Interlagos EV Lap Records) | +1.4% | Brazil primary, Argentina secondary markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Public DC Fast-Charging Corridors

Brazil targets 150,000 chargers by 2035, requiring USD 2.5 billion and signalling state commitment to eliminate range anxiety.[1]“Brazil sets 150,000 EV charger goal,” T&D World, T&D World Editors, tdworld.com Curitiba’s electrocenters manage power loads dynamically, illustrating how software optimises grid interaction and keeps deployment costs contained. BYD and Raízen Power co-installed stations that leverage Brazil’s 85% renewable grid, giving the South American electric vehicle market a unique sustainability narrative. Uruguay complements this momentum with 240 chargers—40% of them rapid—funded by Evergo and Ventus, proving smaller economies can reach near-national coverage quickly. Chile anchors its roll-out on fast-growing electric bus fleets, turning public procurement into a catalyst for private-use networks.

Rising Performance-EV Imports Helped by Mercosur Tariff Waivers

Brazil’s Resolution 97/2018 temporarily cut import duties from 35% to zero, allowing Chinese OEMs to seize 92% of 2023 BEV imports and flood showrooms with high-spec models at compelling prices. Argentina extended similar treatment for 2025, widening the regional window for tariff-free sales. Manufacturers rushed to pre-position 7,000 units ahead of Brazil’s phased tariff reinstatement that will reach 35% in 2026. During 2024, Brazil’s performance-EV imports jumped 229%, confirming pent-up demand once fiscal barriers drop. The waiver phase primes consumer expectations for next-generation products and pressures incumbents to localise production sooner rather than later.

OEM Localisation – BMW Araquari PHEV Line-Up

BMW will spend USD 200 million to retool its Santa Catarina plant for plug-in hybrids in 2025, showing how legacy brands will counter low-cost imports with local content and hybrid architectures suited to ethanol blending.[2]“BMW to invest USD 200 million in Araquari plant,” SteelOrbis, steelorbis.com Volkswagen’s USD 580 million Amarok programme in Argentina follows a similar path, balancing export goals with Mercosur rules. Great Wall Motor is migrating from CKD kits to 60% local parts by 2028, borrowing incumbent localisation playbooks while retaining supply-chain scale from China. Localization fosters technology transfer: BMW’s first flex-fuel PHEV calibrations are engineered specifically for Brazilian altitude and temperature cycles. Toyota’s Sorocaba expansion to 100,000 hybrids annually demonstrates how localisation underpins cost control and regulatory alignment.[3]“Great Wall acelera localização no Brasil,” Valor Econômico, valor.globo.com

Prestige Motorsport Marketing (Interlagos EV Lap Records)

Formula E’s 2025/26 season opener in São Paulo offers a high-profile stage to showcase electric performance to a motorsport-savvy public. South American spectators prize acceleration and handling, and live lap-record attempts can reshape perceptions lingering from early-generation EVs. BYD schedules track-day events at Interlagos to prove that silence does not mean slow, reinforcing brand credibility beyond price competitiveness. The timing coincides with a marketing ramp-up around locally built models, linking track success to showroom offerings. Motorsport activation also feeds regional social-media channels, multiplying awareness efficiently across adjacent markets such as Argentina.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Sticker Prices Vs. Flex-Fuel ICE Alternatives | -3.4% | Brazil primary, regional spillover | Short term (≤ 2 years) |

| Bio-Ethanol Lobby Delaying BEV Fiscal Incentives In Brazil | -2.8% | Brazil national policy, Mercosur influence | Long term (≥ 4 years) |

| Slow Roll-Out Of 800 V Ultra-Fast Chargers Outside Capital Cities | -2.1% | Brazil, Argentina interior regions | Medium term (2-4 years) |

| Hydropower Droughts Causing Grid-Stability Concerns | -1.9% | Brazil, Ecuador, regional interconnects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Bio-Ethanol Lobby Delaying BEV Fiscal Incentives in Brazil

The sugarcane industry produces 35.3 billion liters annually and commands strong congressional backing, making exclusive BEV incentives politically fraught.[4] “Bioenergia no Brasil 2025,” Energy Research Company (EPE), epe.gov.br Programs like RenovaBio channel decarbonization credits toward biofuels, sidelining electric options. Petrobras has earmarked USD 2.2 billion for ethanol infrastructure, reinforcing long-term demand expectations. As a result, hybrids that still consume liquid fuel gain easier policy passage than full BEVs, slowing the transition despite rising charging coverage.

Hydropower Droughts Causing Grid-Stability Concerns

Droughts cut Ecuador’s Coca Codo Sinclair dam to 30% output in 2024, foreshadowing similar risks for Brazil’s 109 GW hydro fleet. The IEA warns Latin American hydro capacity could fall 10% by 2060, jeopardizing the clean-energy backbone that underwrites EV emissions claims. Utilities weigh distributed solar and storage to offset volatility, yet grid planners remain cautious about large charging loads during dry seasons. This uncertainty pushes some fleet operators to favor plug-in hybrids or extended-range vans that can operate independent of grid peaks.

Segment Analysis

By Drive Type: Hybrids Bridge the Transition Gap

Plug-in hybrid electric vehicles held 68.28% share of the South American high perfromance electric vehicle market in 2024, buoyed by Brazil’s nationwide ethanol pumps that deliver seamless range security. Battery-electric volumes are climbing at an 18.23% CAGR as chargers proliferate and total cost of ownership improves. Consumers weigh trip length and fueling convenience, often selecting hybrids for intercity reliability. Toyota’s flex-fuel hybrid programme, scaled up at Sorocaba, demonstrates how global platforms can localize for ethanol compatibility.

The South American high perfromance electric vehicle market continues to shift as OEMs hone bio-hybrid technologies. Stellantis is allocating part of its EUR 5.6 billion budget to Bio-Hybrid drivetrains that pair smaller batteries with efficient ethanol engines, reducing purchase price while cutting tailpipe CO₂. Renault-Geely’s cooperation brings low-emission crossovers built on cost-efficient Chinese architectures, diversifying options in the mid-price tier. Government fleets are early adopters of pure BEVs where predictable urban duty cycles align with charger density, but private buyers gravitate toward hybrids until infrastructure reaches parity outside capitals.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Vehicle Type: Commercial Fleets Drive Electrification

Passenger cars commanded 86.34% of the South American high performance electric vehicle market size in 2024, anchored by private-use demand in Brazil’s urban centers. However, light commercial vehicles grow fastest at 19.73% CAGR because delivery operators chase fuel and maintenance savings. Depot-based overnight charging minimizes downtime and sidesteps public-infrastructure gaps, making economics straightforward for fleets.

Fleet electrification also attracts policy support. Peru, Paraguay, and Chile channel green-transit grants into e-bus and van procurement, locking in bulk orders that stabilize factory volumes. U Power and Ualabee target 80,000 ride-hailing replacements using battery-swap vans, illustrating creative models for high-utilization vehicles. As supply stabilizes, commercial total-cost parity is forecasted before 2027, amplifying volumes that feed secondary markets for used EVs, catalyzing private adoption.

By Peak Power Output: Mid-Range Systems Dominate

Systems rated 201-400 kW captured 56.23% share of the South American high perfromance electric vehicle market size in 2024, reflecting a balance between capital cost and charging speed suitable for mixed urban-intercity use. Urban taxis, delivery vans, and premium sedans all fall within this bracket, boosting charger utilization.

Ultra-high power installations above 400 kW are expanding at 17.21% CAGR, yet remain largely confined to freight corridors and luxury-oriented hubs where payback timelines justify heavier grid upgrades. ABB’s MCS1200 demonstrates technology readiness. Still, operators face lengthy permitting and transformer lead times outside mega-cities. Below-200 kW home and workplace solutions persist for overnight top-ups, carving out a cost-efficient niche in multi-dwelling residences.

By Battery Chemistry: Cost Drives LFP Leadership

Lithium iron phosphate held 52.83% share in 2024 thanks to thermal stability in tropical climates and lower dollar-per-kWh pricing. Manufacturers leverage abundant regional lithium carbonate to feed LFP cathode plants, reducing shipping and import duties.

Nickel manganese cobalt cells are projected to grow at 21.43% CAGR as premium SUVs require higher energy density for 500-km ranges. Stellantis recently unveiled an Argentina-based battery-materials hub to localise precursor refining, slimming cost differentials with LFP. Advanced chemistries such as LFP-Blade or sodium-ion remain exploratory but could unlock sub-USD 50,000 crossover targets critical for mass adoption in the South America electric vehicle industry.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Price Band: Affordability Steers Volume

Sub-USD 50,000 models represented 58.18% of the South American high perfromance electric vehicle market size in 2024, indicating that value perception governs early adoption. Import-tariff holidays have kept showroom prices in check, though scheduled hikes will pressure OEMs to assemble locally.

The USD 50,001-75,000 tier is registering the fastest 16.78% CAGR as middle-class consumers gain purchasing power and seek longer-range SUVs with advanced driver assistance. Premium segments above USD 75,000 remain lifestyle purchases centered in São Paulo, Santiago, and Montevideo. Yet halo models play a branding role that trickles down technology to future mid-range launches, sustaining the feature race across trims

Geography Analysis

Brazil remains the anchor, holding 65.61% of the South American high performance electric vehicle market share in 2024; automakers have already pledged over USD 23 billion in electrification investments that span batteries, assembly, and charging alliances. Flex-fuel ubiquity shapes strategies: hybrids capitalize on ethanol’s carbon footprint advantages while pure BEVs compete in cities where public chargers are densest. The government’s MOVER programme layers tax breaks on locally produced low-emission vehicles, accelerating factory commitments from Hyundai, Toyota, and BYD. Rising tariffs on imports will further consolidate production footprints within Brazil, helping stabilize pricing once tariff shields expire.

Argentina illustrates high-growth upside. Tariff abolition on EV imports gives consumers immediate access to global models while Volkswagen readies a USD 580 million Amarok line with electrified variants for 2027. The country’s lithium deposits underpin cell-grade carbonate exports; Rio Tinto’s Arcadium buyout injects the capital required to scale refineries. Currency volatility and macro risk remain, yet low-cost renewable resources and raw-material endowment present competitive advantages that entice OEMs seeking vertical integration.

Uruguay, although small, leads in per-capita adoption at 17.4 EVs per 10,000 inhabitants and is forecast to compound at 19.74% annually through 2030. Private-sector charge-point investment has already rendered most intercity routes viable. Chile ranks next on the readiness index, posting a 133% sales lift in May 2024 and deploying the continent’s largest electric bus fleet outside China. Secondary markets such as Colombia and Peru are climbing from low bases, incentivized by air-quality mandates in congested capitals. Paraguay leverages its Itaipu hydro surplus to market domestically assembled e-buses to neighbours, extending supply-chain diversity across the bloc.

Competitive Landscape

Competition is fragmenting as Chinese OEMs erode the incumbents’ historical dominance. BYD’s vertical integration strategy delivers cost control from mine to showroom, sustaining a major slice of Brazil’s BEV channel. Stellantis counters by harnessing a multi-brand network and announcing 40 electrified models under its EUR 5.6 billion regional war-chest. Hybrid-centric Toyota leverages its ethanol expertise, committing USD 2 billion to expand flex-fuel hybrid output that appeals to price-sensitive buyers, avoiding long-distance charging stops.

Strategic logic is bifurcating. Chinese brands press cost and software innovation, rolling out OTA features that lock customers into proprietary ecosystems. Traditional OEMs deploy hybrid and bio-fuel synergies, aiming to differentiate through drivetrain versatility and established after-sales coverage. Partnerships blur boundaries: Renault taps Geely for modular EV platforms, while local suppliers like WEG pivot toward e-drives and chargers to capture new value pools.

Technology arms races intensify around charging networks and battery plants. BYD and Raízen promote bundled energy plus mobility packages tied to renewable electricity contracts. ABB, Siemens, and local integrators compete to supply 400 kW public fast-chargers before 800 V architectures scale. Software interoperability and payment standards may become decisive, echoing telecom battles of prior decades. Consolidation is therefore likely, with deep-pocketed players buying niche specialists as the South America electric vehicle market matures.

South America Automotive High Performance Electric Vehicles Industry Leaders

-

BYD Co. Ltd.

-

BMW Group

-

Tesla Inc.

-

Porsche AG

-

Volkswagen AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: BYD has announced a strategic shift in its operational timeline for its manufacturing facility in Brazil, now projected to be fully operational by the end of 2026. This adjustment means that the ambitious target of producing 150,000 vehicles annually will be postponed, reflecting a recalibration of the company's production goals in response to various challenges.

- April 2025: Renault and Geely have officially launched their joint venture in Brazil, announcing an exciting partnership that aims to reshape the automotive landscape in the region. The collaboration will facilitate the delivery of vehicles through an extensive network of 23 carefully selected dealerships, ensuring customers have easy access to this innovative product range.

- December 2024: U Power and Ualabee formed a strategic partnership to introduce an innovative fleet of battery-swapping electric vehicles (EVs). Their ambitious goal is to roll out a remarkable total of 100,000 ride-hailing units over the next three years, revolutionizing urban transportation and promoting sustainable mobility solutions.

South America Automotive High Performance Electric Vehicles Market Report Scope

The South American automotive high-performance electric vehicles market covers the latest trends and technological development in the automotive high-performance electric vehicles, demand of the drive type, vehicle type, country, and market share of major automotive high-performance electric vehicles manufacturers across South America.

By Drive Type

| Battery-Electric Vehicles (BEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) |

By Vehicle Type

| Passenger Cars |

| Light Commercial/Utility Vehicles |

| Medium and Heavy-Duty Commercial Vehicles |

By Peak Power Output

| Below 200 kW |

| 201 - 400 kW |

| Above 400 kW |

By Battery Chemistry

| Lithium-Iron-Phosphate (LFP) |

| Nickel-Manganese-Cobalt (NMC) |

| Nickel-Cobalt-Aluminum (NCA) |

| Advanced Solid-State / High-Silicon Prototype |

By Price Band (USD)

| Less than 50,000 |

| 50,001 - 75,000 |

| 75,001 - 100,000 |

| More than 100 000 |

By Country

| Brazil |

| Argentina |

| Chile |

| Peru |

| Colombia |

| Uruguay |

| Rest of South America |

| By Drive Type | Battery-Electric Vehicles (BEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) | |

| By Vehicle Type | Passenger Cars |

| Light Commercial/Utility Vehicles | |

| Medium and Heavy-Duty Commercial Vehicles | |

| By Peak Power Output | Below 200 kW |

| 201 - 400 kW | |

| Above 400 kW | |

| By Battery Chemistry | Lithium-Iron-Phosphate (LFP) |

| Nickel-Manganese-Cobalt (NMC) | |

| Nickel-Cobalt-Aluminum (NCA) | |

| Advanced Solid-State / High-Silicon Prototype | |

| By Price Band (USD) | Less than 50,000 |

| 50,001 - 75,000 | |

| 75,001 - 100,000 | |

| More than 100 000 | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Uruguay | |

| Rest of South America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the size of the South America electric vehicle market today and how large will it be by 2030?

The market is worth USD 1.26 billion in 2025 and is projected to reach USD 3.19 billion by 2030, reflecting a 20.44% CAGR.

Which country holds the biggest share and which one is growing the fastest?

Brazil controls 65.61% of regional sales, while Uruguay records the highest forecast growth at a 19.74% CAGR through 2030.

What is the single most important factor driving adoption?

Rapid expansion of public DC fast-charging corridors adds about 3.2 percentage points to the forecast CAGR by improving range confidence.

Why do plug-in hybrids dominate today’s sales mix?

Plug-in hybrids leverage Brazil’s nationwide ethanol infrastructure, giving drivers flexible fueling and limiting range anxiety while chargers roll out.

What key barriers still restrain full battery-electric uptake?

High sticker prices versus flex-fuel cars, slow deployment of 800 V ultra-fast chargers outside capitals, and strong bio-ethanol lobbying all dampen near-term BEV momentum.

Page last updated on: