Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

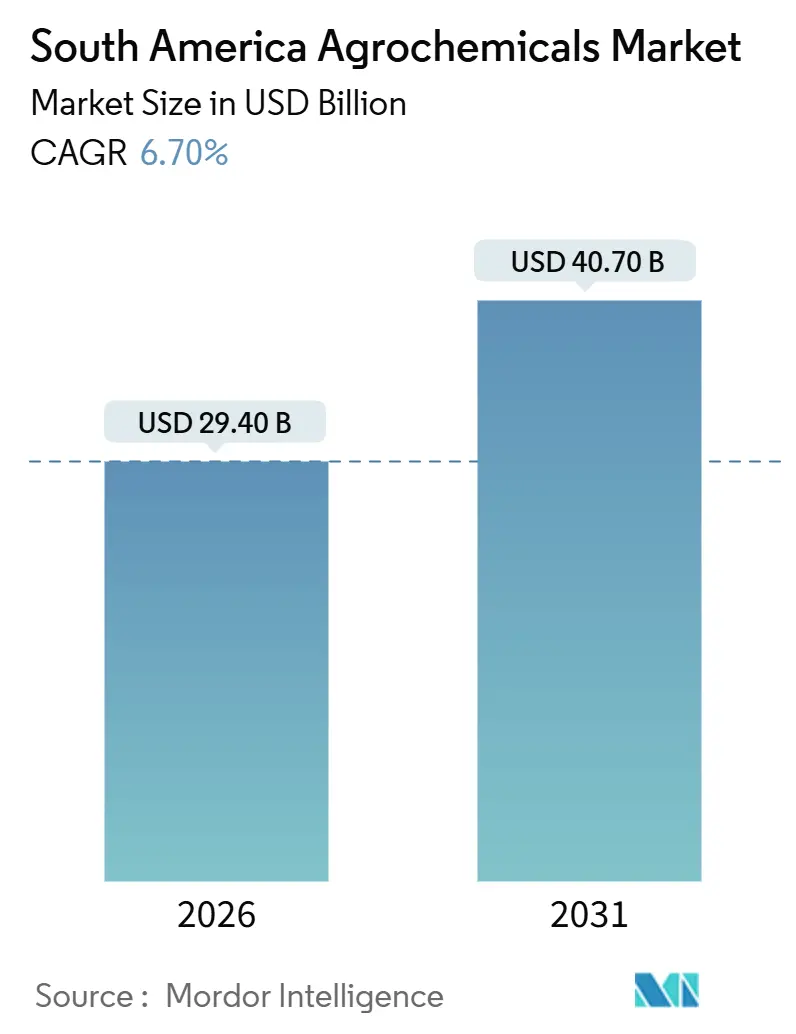

| Market Size (2026) | USD 29.40 Billion |

| Market Size (2031) | USD 40.70 Billion |

| Growth Rate (2026 - 2031) | 6.70% CAGR |

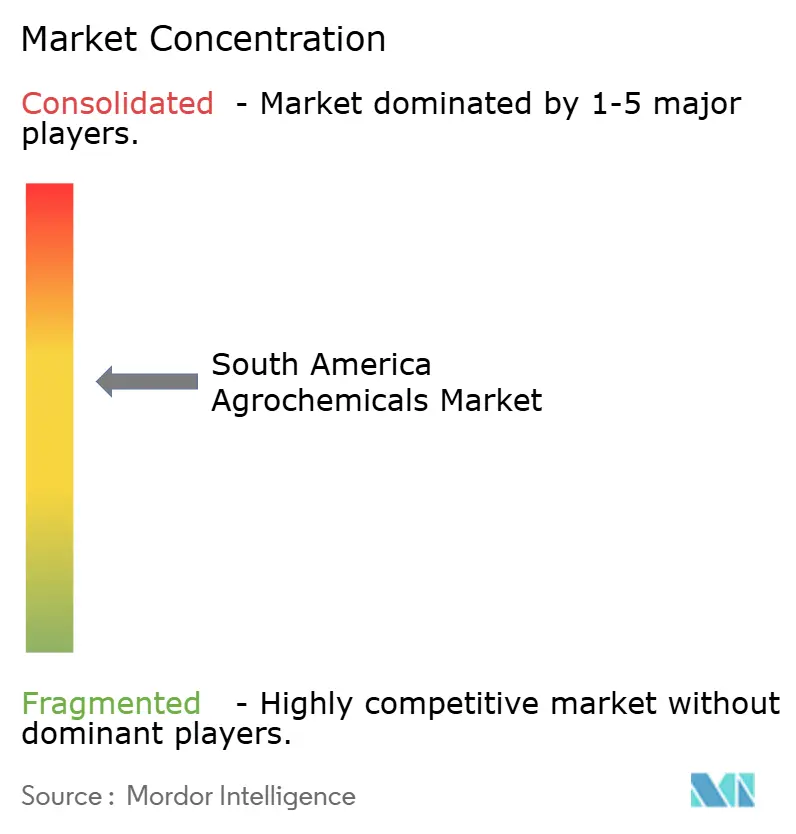

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Agrochemicals Market Analysis by Mordor Intelligence

The South America agrochemicals market size is estimated to be USD 29.40 billion in 2026 and is projected to reach USD 40.70 billion by 2031, growing at a 6.70% CAGR over the forecast period. Rising soybean acreage in Brazil and Argentina, near-universal uptake of herbicide-tolerant seeds, and zero-tariff fertilizer imports in Brazil continue to anchor volume growth. Rapid adoption of fertigation and precision-spray systems is shifting demand toward liquid formulations and premium selective chemistries. Multinational companies are localizing formulation capacity to offset inland logistics delays, while regulatory phase-outs of paraquat, 2,4-D, and organophosphates are prompting a shift toward alternative chemical solutions. Export-oriented specialty crops in Chile and Peru are driving intensified fungicide and micronutrient programs to meet strict residue limits in North America and European markets.

Key Report Takeaways

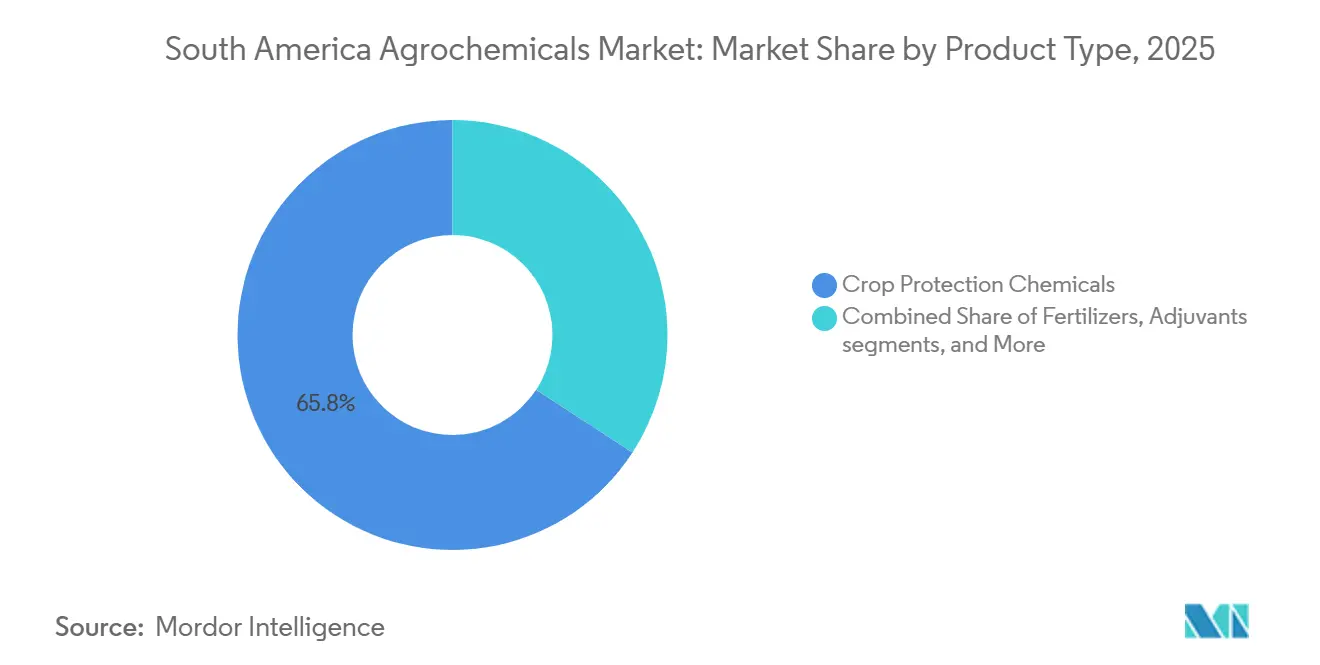

- By product type, crop protection chemicals led with a 65.8% of the South America agrochemicals market share in 2025, while adjuvants are projected to expand at a 9.2% CAGR through 2031.

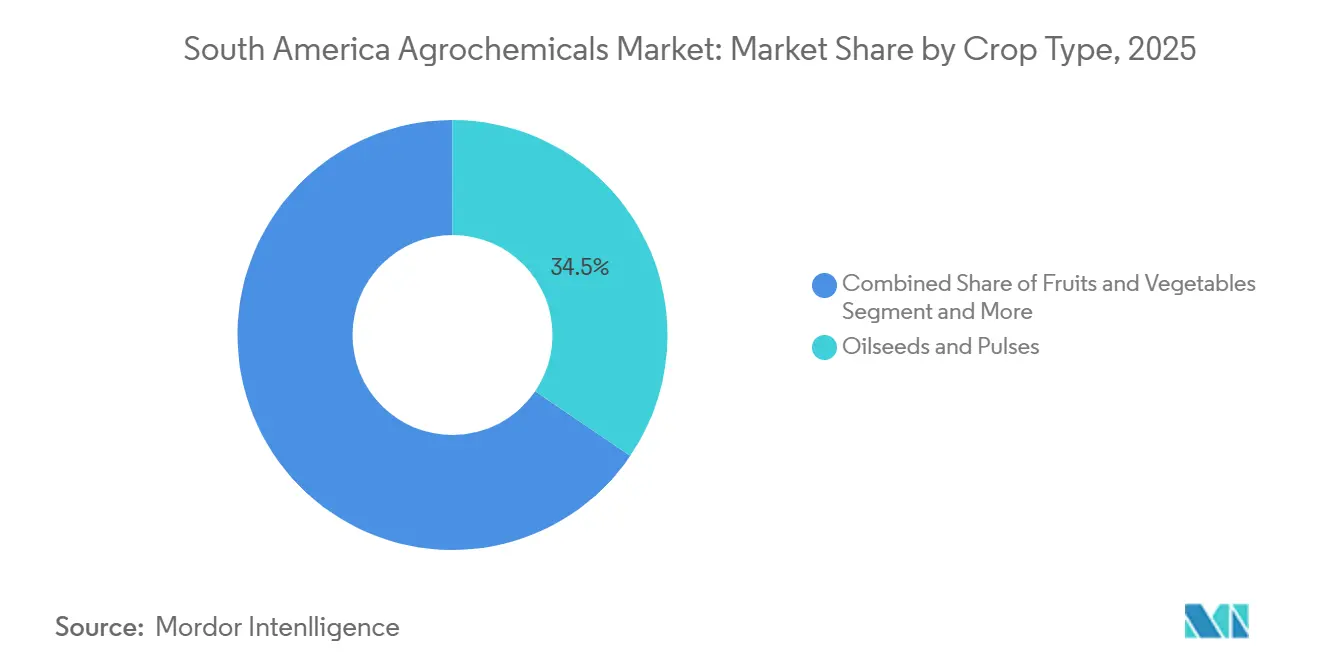

- By crop type, the oilseeds and pulses segment commanded 35.4% share of the South America agrochemicals market in 2025, whereas fruits and vegetables are forecast to grow at an 8.3% CAGR through 2031.

- By country, Brazil captured 65.4% of the South America agrochemicals market size in 2025, yet Colombia is projected to register the fastest 7.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Agrochemicals Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of soybean cultivation area | +1.8% | Brazil (Mato Grosso and Goiás) and Argentina (Pampas) | Medium term (2-4 years) |

| Adoption of herbicide-tolerant biotech seeds | +1.4% | Brazil, Argentina, and Paraguay border zones | Short term (≤ 2 years) |

| Government fertilizer subsidy programs | +1.1% | Brazil (zero-tariff), and Colombia (smallholder support) | Short term (≤ 2 years) |

| Growth in export-oriented specialty crops | +0.9% | Chile (blueberries, and grapes), Peru (avocados, and mangoes) | Medium term (2-4 years) |

| Climate-linked crop-insurance uptake | +0.6% | Brazil (Cerrado), and Argentina (drought zones) | Long term (≥ 4 years) |

| AI-driven precision-spraying technologies | +0.5% | Brazil (large estates), and Argentina (cooperatives) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Expansion of soybean cultivation area

Brazil planted 46.2 million ha of soybeans in the 2024-2025 season, up 3.8% year on year, and Argentina reached 16.8 million ha in 2025, reversing prior drought losses. Larger acreage lifts herbicide volumes because each hectare receives 2-3 sequential applications, including glyphosate, residual pre-emergents, and burndown chemistries. Fertilizer demand is increasing steadily. The average NPK usage in Brazilian soybean cultivation rose to 185 kg per hectare in 2025, compared to 168 kg per hectare in 2020[1]Companhia Nacional de Abastecimento, “Crop Supply and Fertilizer Application Data,” conab.gov.br. The intensified soy-corn double-crop model compresses spray windows, favoring ready-to-mix liquids applied via high-clearance sprayers. Herbicide-tolerant varieties now cover 97% of Brazilian soybean hectares, enabling over-the-top applications that streamline weed control but spur resistance in Amaranthus species.

Adoption of Herbicide-Tolerant Biotech Seeds

Glyphosate- and glufosinate-tolerant traits dominated the majority of soybean seed sales in Argentina and Brazil during the 2025 planting season. Corteva’s Enlist E3 platform gained a higher market share in Brazil, lifting sales of complementary herbicides Enlist One and Enlist Duo. BASF’s Credenz varieties with Xtend technology captured larger Argentine acreage, boosting Engenia volumes. Trait-chemistry linkages lock in recurring revenue for integrated suppliers but concentrate purchasing power among large growers that negotiate discounts. The use of certified seeds in Paraguay increased significantly between 2023 and 2025, driven by cooperatives offering bundled packages that included seeds, herbicides, and credit.

Government fertilizer subsidy programs

Brazil’s zero-tariff policy for potassic and nitrogenous fertilizers through December 2026 cut muriate-of-potash landed costs by 18% in 2025 versus 2021[2]Ministério da Agricultura e Pecuária, “Zero-Tariff Fertilizer Import Policy,” gov.br/agricultura. Colombia allocated COP 150 billion (USD 37 million) to subsidize fertilizer for smallholder coffee and cocoa producers in 2025. Argentina introduced province-level tax rebates covering up to 15% of balanced NPK costs for growers who submit soil tests, lifting soil-testing volumes by 28% in participating provinces. These incentives lower growers’ price sensitivity and sustain application rates even when global prices are volatile.

Climate-linked crop-insurance uptake

The Brazilian government’s Rural Insurance Premium Subsidy Programme (PSR) has been instrumental in subsidizing 20-45% of insurance premiums, thereby making insurance coverage more accessible to many smallholder farmers. Insurers often require insured farmers to follow recommended fungicide and fertility programs, indirectly boosting agrochemical demand. Argentina relaunched its crop insurance subsidy in 2025, budgeting USD 80 million to cover 30% of premiums for soybean, corn, and wheat growers. Satellite-based indices accelerate parametric payouts, while bundled micro-insurance options expand coverage to smallholders.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter bans on synthetic active ingredients | -1.2% | Brazil (Brazilian National Health Surveillance Agency), and Argentina (National Agri-Food Health and Quality Service) | Medium term (2-4 years) |

| Volatile raw-material costs | -0.9% | Import-dependent Chile, and Peru | Short term (≤ 2 years) |

| Rising herbicide resistance in key weeds | -0.7% | Brazil (Cerrado), and Argentina (soy belt) | Long term (≥ 4 years) |

| Amazon corridor logistics bottlenecks | -0.5% | Brazil (Mato Grosso, and Pará) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Bans on Synthetic Active Ingredients

Brazilian National Health Surveillance Agency (ANVISA) scheduled paraquat phase-out by December 2026 and restricted 2,4-D use to closed systems by 2027. Paraquat represented 8% of Brazilian herbicide volume in 2024. Substitution with glufosinate or saflufenacil raises per-hectare costs by up to 50% and requires new application timing. National Service of Agri-Food Health and Quality SENASA (Argentina) announced bans on chlorpyrifos and carbofuran by mid-2027, impacting corn and sugarcane insecticide programs. Compliance investments favor large farms. Smaller growers may cut application frequency, risking yield losses.

Volatile Raw-Material Costs (Oil-Derived Intermediates)

Crude prices fluctuated between USD 72 and USD 89 per barrel in 2025, swinging naphtha costs by 31%. Chilean distributors import 85-90% of formulations, so currency depreciation raised landed costs. Argentine natural gas spikes to USD 6.20 per million British Thermal Units in Q2 2025, forcing local urea plants to curtail output, increasing reliance on imports. Volatility makes growers delay purchases, creating erratic demand and pressuring distributors working capital.

Segment Analysis

By Product Type: Crop Protection Dominates While Adjuvants Lead Growth

Crop protection chemicals dominated the market in 2025, contributing 65.8% of product-type revenue. This emphasizes the role of herbicides, insecticides, fungicides, and other pesticides in protecting vast hectares of crops across the region. Fertilizers accounted for the next largest market share of revenue, supported by Brazil's zero-tariff import policy, which ensured high urea and potash volumes despite global price fluctuations. Adjuvants, while comprising a smaller share, emerged as the fastest-growing segment. This segment is projected to grow at a 9.2% CAGR through 2031, driven by the adoption of precision-spraying systems, drone applications, and the demand for advanced surfactants, drift-control agents, and pH conditioners in increasingly complex tank mixes.

Within crop protection, herbicides remain the key driver of demand, supported by herbicide-tolerant soybean systems. Insecticides and fungicides continue to play a vital role due to pest and disease pressures affecting crops such as cotton, corn, soybeans, grapes, and other high-value crops. Adjuvant growth is closely associated with the adoption of spot-spraying and variable-rate technologies, which boost adjuvant usage per treated hectare. Fertilizers continue to gain traction, particularly in nitrogenous and potassic products, supported by favorable policies and consistent demand. Plant growth regulators, while accounting for niche market value, show steady growth due to their high margins and expanding applications in sugarcane and export-oriented fruit crops. This niche segment is anticipated to experience specialized growth through 2031.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Crop Type: Specialty Crops Outpace Commodity Grains

Oilseeds and pulses led revenue at 35.4% of the South America agrochemicals market size in 2025, with soybeans dominating herbicide and inoculant demand. Fruits and vegetables are forecast to grow at an 8.3% CAGR, the fastest among crop types, supported by export-driven horticulture. The South America agrochemicals market share for fruits and vegetables is projected to reach a significant share by 2031. Cereals and grains held a significant share, while commercial crops like sugarcane and coffee contributed notably.

Blueberry growers in Chile averaged 9 fungicide sprays per season in 2025, up 18% from 2022 levels. Peruvian avocado plantations added 8,600 ha and rely on fertigation, lifting soluble fertilizer sales by 31%. Colombian coffee rehabilitation distributed 142 million rust-resistant seedlings, each requiring seed treatment and foliar micronutrients. Argentine wheat farmers boosted triazole fungicide use by 18% to curb Fusarium head blight.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Brazil captured 65.4% of the South America agrochemicals market revenue in 2025. Mato Grosso alone accounted for 28% of national volumes due to intensive soy-corn rotations that average 185 kg NPK per ha[3]Source: Brazilian Fertilizer Association, “Fertilizer Import Data,” anda.org.br. Goiás and Mato Grosso do Sul added 1.8 million ha of soybeans from 2023-2025, intensifying herbicide resistance issues that drive multi-mode programs. Bayer committed USD 150 million in March 2025 to enlarge its Belford Roxo fungicide plant, underscoring confidence despite regulatory headwinds.

Argentina accounted for a substantial share of regional revenue in 2025, achieving notable year-on-year growth following currency stabilization, which facilitated the import of inputs. This economic improvement enabled greater access to agricultural resources, supporting the modernization of farming practices. The adoption of variable-rate technologies witnessed significant expansion, reflecting increased technological integration and efficiency in agricultural operations, which contributed to enhanced productivity and resource management. Colombia is the fastest-growing geography at 7.6% CAGR, driven by coffee renovation and 6,800 ha of new avocado orchards.

Chile’s revenue grew 6.8% in 2025 as driven by intensified fungicide programs aimed at meeting stricter European Union residue limits. These programs are being implemented to ensure compliance with evolving regulations and to maintain access to key export markets. Peru is projected to expand, supported by increased avocado and blueberry acreage that depends on fertigation, a method that enhances nutrient delivery and water efficiency. The rest of South America, led by Paraguay and Bolivia, collectively contributes to the remaining revenue share. Paraguay has seen a rise in certified HT seed adoption, which is improving crop yields and resilience, while Bolivia is adding 120,000 hectares of soybeans to boost its agricultural output and meet growing demand.

Competitive Landscape

The top five companies accounted for a significant portion of the market, reflecting moderate market concentration. Bayer AG leads the market, driven by its integrated seed and chemistry portfolio. Syngenta Group follows closely, supported by its broad-spectrum fungicide offerings. BASF SE holds a strong position, bolstered by its capacity expansion at Guaratinguetá. Corteva Agriscience's market presence is attributed to its Enlist traits and complementary herbicides, while FMC Corporation's position is supported by its diamide insecticides.

Localization is a core strategy. Multinational plants near São Paulo reduce dependency on congested Amazon corridors that add up to 15 days to inbound shipments. Syngenta’s November 2024 patent for microencapsulated herbicides aims to stretch residual activity by 30%. Digital agronomy platforms are emerging as tie-breakers among tech-forward cooperatives, with firms offering satellite disease forecasts and variable-rate prescriptions capturing incremental share.

Regional specialists are entering previously untapped categories. Lavoro capitalizes on its distribution network to offer bundled adjuvants and plant growth regulators, which represent a smaller portion of revenue but deliver strong margins. UPL Ltd., Nutrien Ltd., and Yara International ASA are enhancing fertilizer supply chains through long-term import agreements and the development of new terminals to address raw material volatility.

South America Agrochemicals Industry Leaders

BASF SE

Corteva Agriscience

FMC Corporation

Bayer AG

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Stepan Company is expanding its presence in Brazil's agricultural market by establishing a new laboratory at Parque Tecnológico de Piracicaba. This facility aims to enhance formulation development, performance testing, and cross-team collaboration. It will focus on developing formulations for chemical and biological crop protection products, adjuvants, and specialty fertilizers.

- July 2025: Mosaic has inaugurated a new blending, storage, and distribution facility in Palmeirante, Tocantins, Brazil. This facility is to enhance the supply chain efficiency and availability of agrochemicals in the South America market.

- May 2024: FMC Corporation has obtained registration in Brazil for Azugro and Ezanya herbicides, approved for use in cotton, tobacco, and wheat crops. These formulations offer growers additional options to address herbicide resistance effectively across various agronomic practices.

South America Agrochemicals Market Report Scope

Agrochemicals are applied to protect crops from yield losses caused by insect infestations, pests, and plant diseases. The South America Agrochemicals Market report provides an in-depth analysis of prevailing market trends, key growth drivers, competitive dynamics, and investment opportunities, along with comprehensive profiles of leading market participants.

The South America Agrochemicals Market Report is Segmented by Product Type (Fertilizers, Crop Protection Chemicals, Adjuvants, and Plant Growth Regulators), by Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, Commercial Crops, and Turf and Ornamentals), and by Country (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Fertilizers | Nitrogenous |

| Phosphatic | |

| Potassic | |

| Other Fertilizers | |

| Crop Protection Chemicals | Herbicides |

| Insecticides | |

| Fungicides | |

| Other Pesticides | |

| Adjuvants | |

| Plant Growth Regulators |

By Crop Type

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Commercial Crops |

| Turf and Ornamentals |

By Country

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Product Type | Fertilizers | Nitrogenous |

| Phosphatic | ||

| Potassic | ||

| Other Fertilizers | ||

| Crop Protection Chemicals | Herbicides | |

| Insecticides | ||

| Fungicides | ||

| Other Pesticides | ||

| Adjuvants | ||

| Plant Growth Regulators | ||

| By Crop Type | Cereals and Grains | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Commercial Crops | ||

| Turf and Ornamentals | ||

| By Country | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the South America agrochemicals market in 2026?

The South America agrochemicals market size is USD 29.40 billion in 2026 and is projected to reach USD 40.70 billion by 2031.

Which product type leads regional sales?

Crop Protection Chemicals are the largest product type, holding 65.8% of 2025 revenue, led by glyphosate use in herbicide-tolerant soybean systems.

Why is Colombia the fastest-growing geography?

Colombia’s 7.6% CAGR is fueled by coffee rehabilitation programs and rapid avocado acreage expansion that increase fungicide and micronutrient demand.

Which companies dominate the competitive landscape?

Bayer AG, Syngenta Group, BASF SE, Corteva Agriscience, and FMC Corporation collectively hold significant share of regional market.