Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

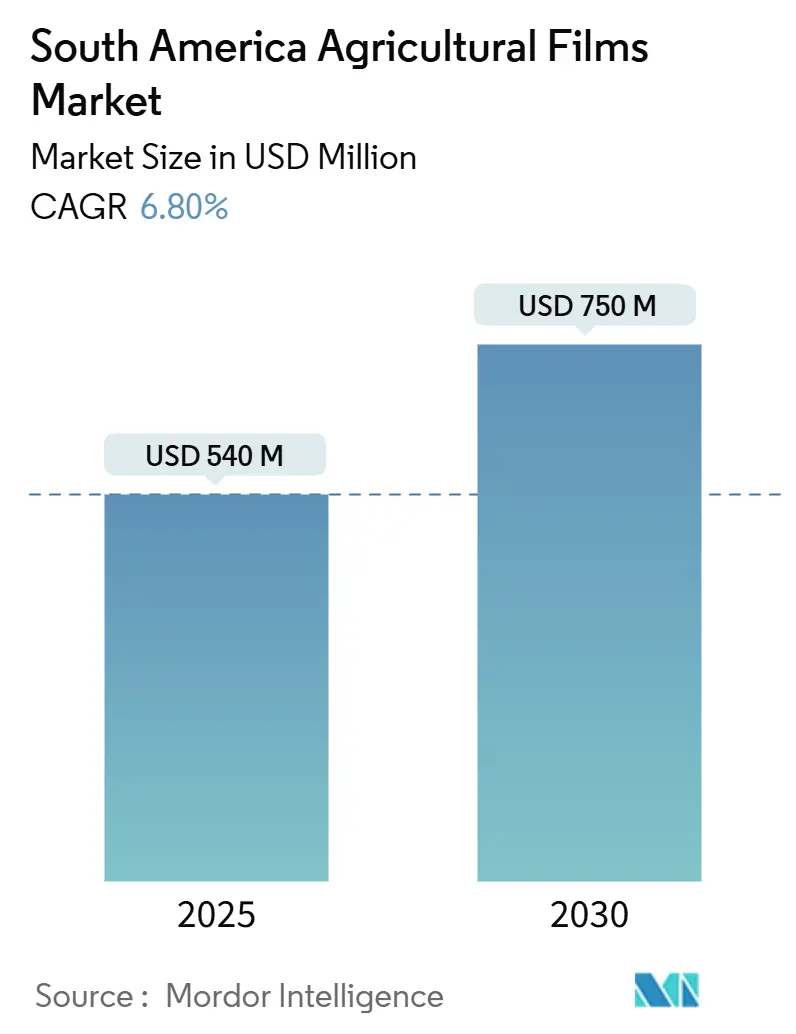

| Market Size (2025) | USD 540 Million |

| Market Size (2030) | USD 750 Million |

| Growth Rate (2025 - 2030) | 6.80% CAGR |

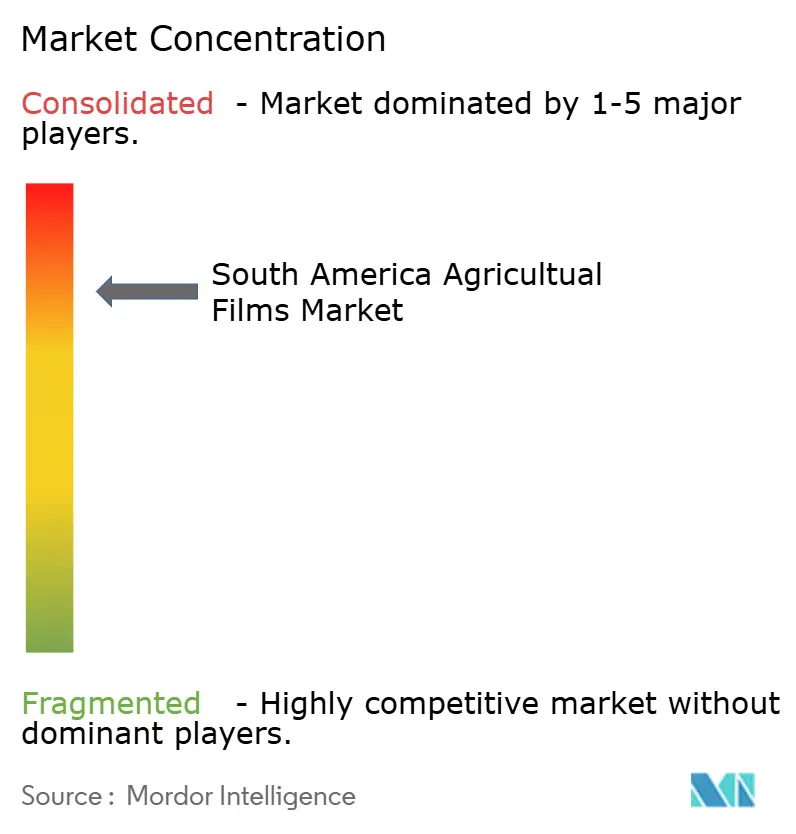

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Agricultural Films Market Analysis by Mordor Intelligence

The South America agricultural films market is valued at USD 540 million in 2025 and is projected to reach USD 750 million by 2030, reflecting a 6.80% CAGR through 2030. Expansion in export-oriented horticulture is driving demand for polyethylene and biodegradable coverings that extend growing seasons and enhance yields. Brazil’s 2024/25 Crop Plan unlocked USD 88.2 billion of subsidized credit, steering growers toward UV-stabilized mulch and silage films. Chile’s avocado shippers reported 29.8% export growth in the 2024/25 season after scaling greenhouse and mulch systems that curb water stress. Regional mandates for recycled content are compelling converters to incorporate post-consumer resin, while capacity expansions in bio-polyethylene are narrowing the price gap with fossil-derived resins.

Key Report Takeaways

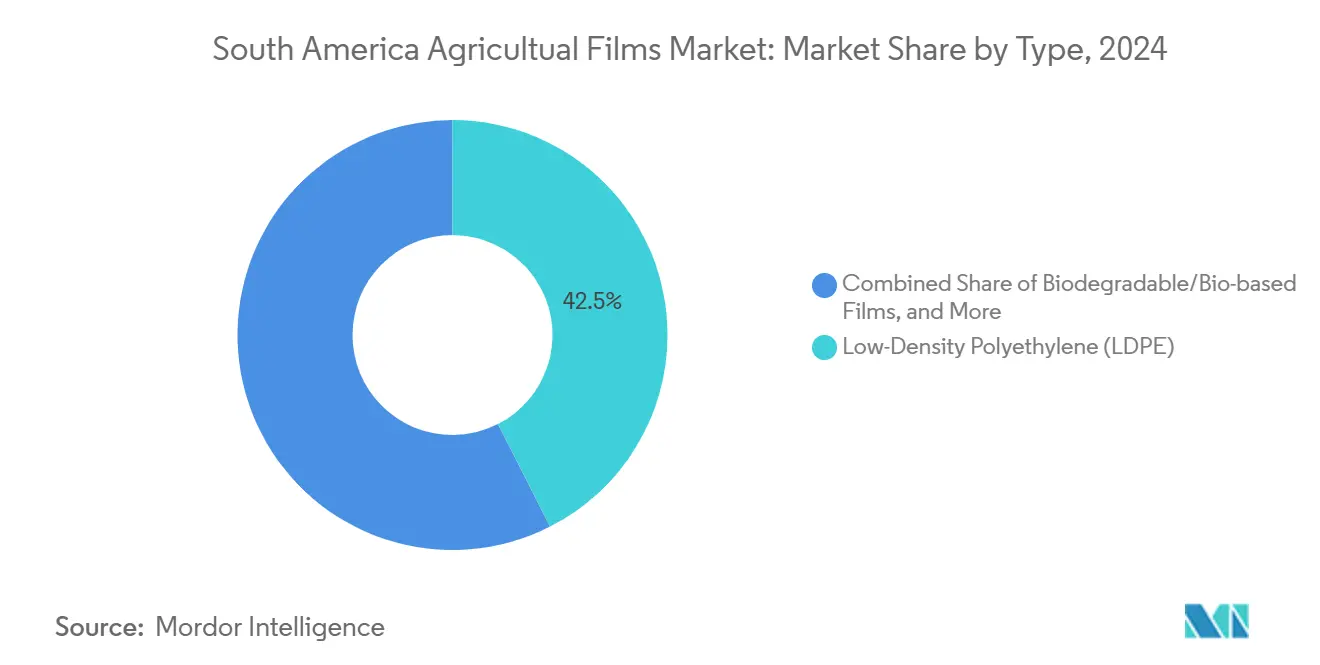

- By type, Low-Density Polyethylene (LDPE) captured 42.5% of the South America agricultural films market size in 2024. Biodegradable and bio-based films are projected to advance at an 11.8% CAGR through 2030.

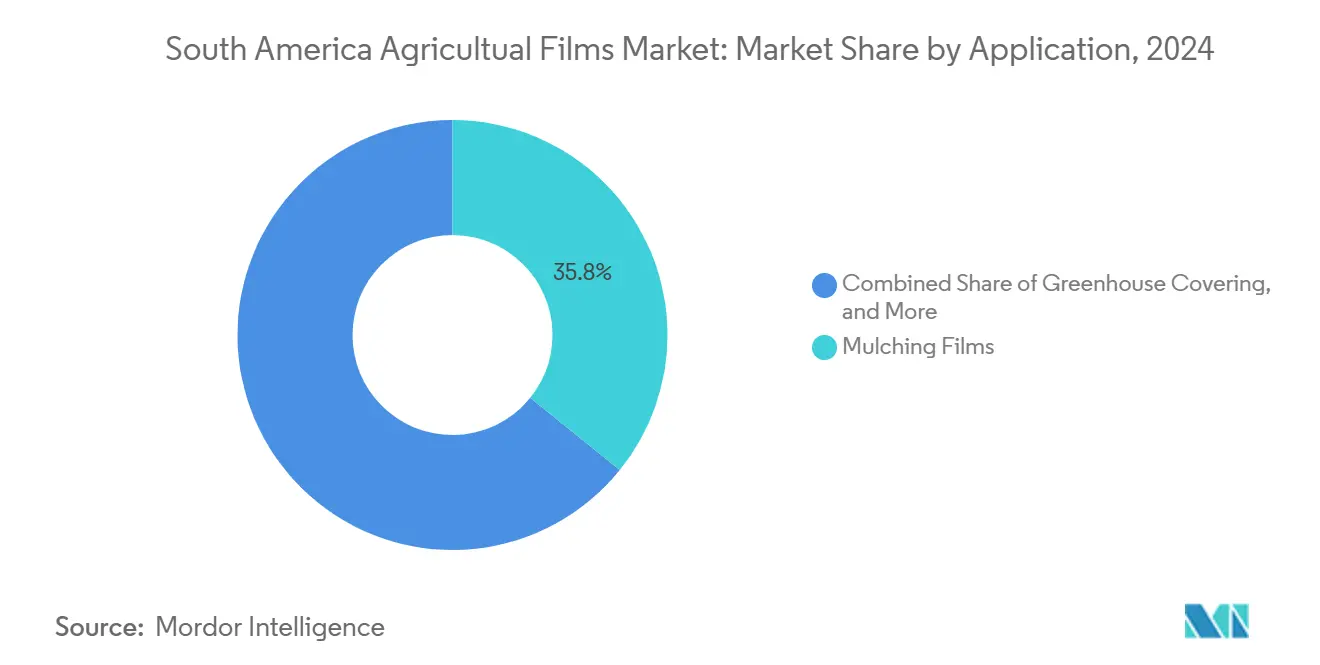

- By application, mulching films accounted for 35.8% of the South America agricultural films market size in 2024, and greenhouse films are the fastest-growing application, with a 10.4% CAGR through 2030.

- By geography, Brazil held 54.0% revenue share in 2024, while Colombia is forecast to grow at a 9.8% CAGR to 2030.

South America Agricultural Films Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of greenhouse farming | +1.2% | Brazil, Argentina, Chile (national, with early gains in São Paulo, Corrientes, Valparaíso) | Medium term (2-4 years) |

| Growth of protected horticulture exports | +1.4% | Chile, Colombia, Peru (national, with concentration in Coquimbo, Antioquia, La Libertad) | Short term (≤ 2 years) |

| Government incentives for climate-smart agriculture | +0.9% | Brazil (national, ABC+ plan focuses on the Cerrado and Amazon transition zones) | Long term (≥ 4 years) |

| Expansion of high-value berry and avocado crops | +1.1% | Chile, Peru, Colombia (national, with hotspots in Valparaíso, Ica, Antioquia) | Medium term (2-4 years) |

| Emergence of biodegradable/Bio-PE film capacity | +1.3% | Brazil (national, Braskem bio-PE hub in Triunfo), Argentina, Chile | Long term (≥ 4 years) |

| Agri-tech financing for plasticulture start-ups | +0.6% | Brazil, Argentina (national, with digital-credit penetration in São Paulo, Buenos Aires) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Greenhouse Farming

Mid-sized greenhouse installations for tomatoes, peppers, and cucumbers are proliferating across Brazil's interior and Argentina's peri-urban zones, driven by urban demand for year-round fresh produce and the need to buffer against erratic rainfall. Chile's greenhouse tomato production reached 180,000 metric tons in 2023, primarily concentrated in Coquimbo, Valparaíso, and the Metropolitan Region, where growers utilize Low-Density Polyethylene (LDPE) and Ethyl Vinyl Acetate/Ethylene Butyl Acrylate (EVA/EBA) films with anti-drip additives to minimize disease pressure. The capital intensity of these structures, typically 30 to 40% above bare-soil systems, is being offset by cooperative purchasing models and leasing arrangements brokered through regional extension services. Satellite mapping studies published in Nature Food during 2024 identified a 12% annual increase in greenhouse footprint across South America's temperate zones, a rate that outpaces global averages and signals sustained film demand.

Growth of Protected Horticulture Exports

Export-oriented berry, grape, and avocado sectors are shifting to plasticulture to meet stringent phytosanitary and cosmetic standards imposed by North American and European buyers. Peru's blueberry exports totaled USD 1.5 billion in 2024, sourced from 23,000 hectares in La Libertad and Ica, where drip irrigation under mulch films reduces water consumption by 40% and lifts marketable yields by 25%. Chile's grape sector, which accounts for 9% of global fresh table grape exports, is transitioning from open-field to netted and partially covered systems that shield fruit from hail and sunburn, a trend that increases demand for greenhouse-grade polyethylene with enhanced tensile strength. The premium pricing these crops command justifies the incremental cost of specialty films, creating a virtuous cycle where export revenue funds further plasticulture adoption.

Government Incentives for Climate-Smart Agriculture

Brazil's ABC+ (Low-Carbon Agriculture) plan, launched in 2020 and extended through 2030, offers subsidized credit lines for technologies that sequester carbon or reduce methane emissions, including biodegradable mulch films and silage systems that minimize spoilage. The 2024 Crop Plan earmarked USD 88.2 billion for rural credit, with a dedicated tranche for climate-smart inputs that carry interest rates 2 to 3 percentage points below commercial benchmarks. This policy framework has accelerated trials of Braskem's bio-polyethylene and BASF's ecovio M2351, a biodegradable mulch certified to EN 17033 that degrades in soil within 24 months, leaving no microplastic residues [1]Source: BASF Agricultural Solutions, basf.com . The long-term impact of these programs hinges on whether subsidy mechanisms can be sustained through electoral cycles and commodity-price downturns, a risk that introduces volatility into biodegradable-film adoption curves.

Expansion of High-Value Berry and Avocado Crops

Higher margins on berries and avocados justify the premium cost of UV-stabilized and anti-oxidant-laden films that extend service life to 18 months in tropical sunlight. Peru's avocado exports reached 650,000 metric tons in 2024, valued at USD 1.1 billion, with Hass orchards in La Libertad and Ica utilizing reflective mulch to mitigate heat stress and enhance fruit set during flowering. Chile's raspberry and blackberry plantations, concentrated in the Maule and Bío Bío regions, are adopting tunnel systems with anti-drip films that prevent condensation-related fungal infections, a shift that has cut fungicide applications by 20% according to field trials conducted by the Chilean Agricultural Research Institute. The expansion of these crops is geographically concentrated in zones with established cold-chain logistics, limiting near-term spillover to frontier regions but ensuring robust film demand in core production areas.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental concerns and plastic-waste legislation | -0.8% | Brazil, Chile, Argentina (national, with enforcement focus in coastal and urban-adjacent zones) | Medium term (2-4 years) |

| High initial cost versus conventional coverings | -0.9% | Brazil, Argentina, Colombia (national, with acute impact in smallholder regions) | Short term (≤ 2 years) |

| Supply-chain volatility in ethylene feedstocks | -0.5% | Regional (reliance on imported NGL from USA, Middle East) | Short term (≤ 2 years) |

| Slow farmer adoption outside Brazil’s south-east interiors | -0.4% | Brazil (north-east, north, center-west), Paraguay, Bolivia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Environmental Concerns and Plastic-Waste Legislation

Brazil's Decree 12,688, enacted in November 2024, mandates reverse logistics for plastic packaging, requiring a 32% recovery rate and 22% recycled content by 2026, with the goal of escalating to 50% recovery by 2040 [2]Source: Decreto 12.688 de 2024, Ministério do Meio Ambiente e Mudança do Clima, gov.br. These regulations compel converters to invest in mechanical-recycling infrastructure and source post-consumer resin, raising production costs by 10 to 15% according to industry estimates. Compliance frameworks such as ISO 14021 for recycled-content claims and EN 13432 for compostability are becoming de facto market-entry requirements, favoring larger players with dedicated sustainability teams. The enforcement timeline remains uncertain in Argentina and Colombia, where budget constraints limit the capacity of environmental agencies to audit film waste streams, creating a patchwork regulatory landscape that complicates regional supply-chain planning.

High Initial Cost Versus Conventional Coverings

The capital expenditure for transitioning from bare-soil cultivation to mulch or greenhouse systems is 30 to 40% above conventional methods, a threshold that deters adoption among smallholders with limited access to credit. A greenhouse installation for 1 hectare of tomatoes in Argentina's Corrientes province costs approximately USD 25,000, including polyethylene covering, drip irrigation, and structural framing, compared to USD 8,000 for open-field cultivation with basic inputs. Cooperative purchasing models, which aggregate demand across 50 to 100 growers to secure volume discounts, have reduced per-unit film costs by 15 to 20% in Brazil's strawberry cooperatives and Chile's grape associations, but these structures require social capital and organizational capacity that are scarce in frontier regions. The payback period for plasticulture investments ranges from 2 to 4 years depending on crop type and market access, a timeline that exposes growers to commodity-price risk and weather volatility.

Segment Analysis

By Type: Bio-Based Films Gain Share Despite LDPE Dominance

Low-Density Polyethylene (LDPE) captured 42.5% of the South America agricultural films market size in 2024, underpinned by its cost advantage, ease of processing, and proven performance in mulching and silage applications across Brazil's strawberry belt and Argentina's greenhouse vegetable zones. The dominance of Low-Density Polyethylene (LDPE) reflects its versatility across multiple applications and the installed base of extrusion equipment optimized for its melt-flow characteristics. Low-Density Polyethylene (LDPE) puncture resistance makes it the preferred choice for silage wrap, where a single tear can compromise anaerobic fermentation and lead to feed spoilage.

Biodegradable and bio-based films, which are projected to advance at an 11.8% CAGR through 2030, are driven by Braskem's bio-PE capacity expansion to 191 kilotons in 2024 and regulatory tailwinds from Brazil's recycled-content mandates. The shift toward biodegradable films is accelerating in organic-certified operations, where post-harvest film removal is labor-intensive and costly, but mainstream adoption hinges on further cost reductions and field trials demonstrating equivalent agronomic performance. Compliance with EN 17033 and ISO 17033 standards for soil biodegradability is emerging as a baseline requirement for market access in Chile and Brazil, a dynamic that favors suppliers with formulation expertise and third-party certification.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Mulching Leads, Fumigation Accelerates

Mulching films accounted for 35.8% of the South America agricultural films market size in 2024, driven by Brazil's 155,000 metric tons strawberry sector and Chile's avocado plantations, where reflective and UV-stabilized mulches reduce water consumption by 40% and suppress weed competition. Mulching films deliver measurable return on investment through water savings, yield lifts, and reduced herbicide costs, making them the entry point for plasticulture adoption among smallholders. Silage wrap demand is counter-cyclical to grain prices, as livestock producers shift to preserved forage when feed-grain costs spike, a dynamic that provides demand stability during crop-price downturns.

Greenhouse films are the fastest-growing application, with a 10.4% CAGR through 2030, is expanding in Colombia's Antioquia blueberry region and Chile's Valparaíso tomato clusters, where EVOH-layered films with anti-drip additives extend service life to 4 years and reduce fungicide applications by 20%. Greenhouse covering represents the highest capital commitment per hectare but offers the longest service life and the greatest yield stability, a trade-off that appeals to export-oriented growers with access to long-term financing. The application mix is shifting toward higher-value segments as growers seek to differentiate output through quality and sustainability attributes, a trend that favors converters with technical-service capabilities and product portfolios spanning multiple film types.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Brazil held 54.0% revenue share in 2024, reflecting the country's position as South America's agricultural powerhouse, with film demand spanning grain silage, greenhouse horticulture, and mulched row crops. The 2024/25 Crop Plan's allocation of USD 88.2 billion in rural credit, including dedicated lines for climate-smart technologies, is accelerating the adoption of biodegradable mulch and UV-stabilized greenhouse covers in the Cerrado and Amazon transition zones. Braskem's bio-PE production, which reached 191 kilotons in 2024, positions Brazil as the only South American country with domestic bio-based resin capacity, a strategic advantage that insulates local converters from import-price volatility.

Colombia is forecast to grow at a 9.8% CAGR to 2030, driven by blueberry exports that reached 40,000 metric tons in 2024, up from 7,000 hectares in Antioquia, where growers utilize greenhouse covers with EVOH (Ethylene Vinyl Alcohol) oxygen barriers to maintain modified-atmosphere conditions. Avocado shipments climbed 15% year-on-year to 120,000 metric tons in 2024, with Hass plantations adopting UV-stabilized mulch to reduce heat stress and improve fruit set during flowering. Greenhouse vegetable production in Corrientes, Salta, and Buenos Aires provinces is expanding, with tomato, pepper, and cucumber growers adopting anti-drip films to reduce disease pressure and extend harvest windows. Chile's 9.4% share in 2024 is concentrated in the Coquimbo and Valparaíso regions, where avocado, grape, and tomato growers face stringent export-quality standards that justify the premium cost of UV-stabilized and anti-oxidant-laden films

Peru, Uruguay, Paraguay, and Ecuador collectively represent with Peru's blueberry and avocado sectors driving incremental film demand. Peru's blueberry exports totaled USD 1.5 billion in 2024, sourced from 23,000 hectares in La Libertad and Ica, where drip irrigation under mulch films reduces water consumption by 40%. Uruguay's grain-storage market sustains steady silage-wrap consumption, while Paraguay's soybean sector is beginning to adopt mulch films for high-value vegetable rotations. Ecuador's banana export industry, which ships over 6 million metric tons annually, relies on UV-stabilized bunch covers to protect fruit from sunburn and insect damage, a niche application that commands premium pricing due to the technical requirements for tropical-sunlight resistance.

Competitive Landscape

The South America agricultural films market exhibits high consolidation, with the top five players including Dow Inc. and Amcor plc. (Berry Global Inc.), BASF SE, Manupackaging Deutschland GmbH & Co. KG, Agroflex Indústria de Plásticos Ltda. holding a significant share in 2024. Dow and Berry Global leverage vertically integrated resin-to-film supply chains and multi-decade relationships with large agribusiness cooperatives, enabling them to offer volume discounts and technical-service packages that smaller converters cannot match. BASF and Novamont differentiate through certified biodegradable formulations, with BASF's ecovio M2351 meeting EN 17033 standards for soil incorporation and Novamont's Mater-Bi films gaining traction in Chile's organic strawberry sector and Argentina's greenhouse vegetable zones[3]Source: BASF Agricultural Solutions, basf.com .

Regional players such as Manupackaging and Agroflex capture a share in niche applications like banana bunch covers and reservoir liners by offering shorter lead times and localized technical support, which provides a competitive advantage in markets where import logistics add 4 to 6 weeks to delivery schedules. The competitive intensity is rising as European suppliers, including RKW Group and Trioplast, expand distribution networks in Chile and Peru, targeting export-oriented growers who prioritize film longevity and UV-stabilization performance over price.

Opportunities lie in the development of EVOH-layered films with enhanced oxygen barriers for modified-atmosphere silage systems, a segment where European suppliers currently dominate imports and command 20 to 30% price premiums. Agri-fintech platforms such as Agrolend and Traive are lowering the capital barrier for smallholder adoption by embedding film purchases into buy-now-pay-later credit lines, a model that could unlock demand in Brazil's fragmented north-east and Colombia's emerging avocado zones. ISO 17033 and EN 13432 certifications for biodegradable and compostable films are becoming de facto market-entry requirements in Chile and Brazil, a dynamic that favors larger players with dedicated sustainability teams and third-party audit infrastructure.

South America Agricultural Films Industry Leaders

-

Dow Inc.

-

Amcor plc. (Berry Global Inc.)

-

BASF SE

-

Manupackaging Deutschland GmbH & Co. KG

-

Agroflex Indústria de Plásticos Ltda.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2024: Brazil's Ministry of Environment enacted Decree 12,688, mandating reverse logistics for plastic packaging with 32% recovery targets and 22% recycled-content minimums by 2026, escalating to 50% recovery by 2040. The regulation explicitly includes agricultural films, compelling converters to invest in mechanical-recycling infrastructure and source post-consumer resin.

- October 2024: Dow and Ambipar established a partnership to expand plastic recycling operations in South America, with a focus on Brazil. The collaboration aims to process 80,000 metric tons of plastic waste annually and convert it into 60,000 metric tons of post-consumer resin through mechanical recycling facilities, supporting agricultural film production.

- January 2024: Kuraray Co., Ltd. announced that its Niigata Plant received ISCC PLUS certification for its 3-methyl-1,5-pentanediol (MPD) production. ISCC PLUS is an international certification program that validates sustainable product manufacturing.

South America Agricultural Films Market Report Scope

Agricultural films are polymeric sheets used in farming to enhance crop growth and protection by regulating soil temperature, retaining moisture, suppressing weeds, and shielding crops from environmental factors. The South America Agricultural Films Market is segmented by type (Low-Density Polyethylene, Linear Low-Density Polyethylene, High-Density Polyethylene, and Ethyl Vinyl Acetate (EVA)/Ethylene Butyl Acrylate (EBA)), by application (Greenhouse, Silage, Mulching, and Others), and by geography (Brazil, Argentina, and Rest of South America). The report offers the market size and forecasts in terms of value (USD) for all the above segments.

By Type

| Low-Density Polyethylene (LDPE) |

| Linear Low-Density Polyethylene (LLDPE) |

| High-Density Polyethylene (HDPE) |

| Ethyl Vinyl Acetate / Ethylene Butyl Acrylate (EVA/EBA) |

| Biodegradable/Bio-based Films |

By Application

| Greenhouse Covering |

| Silage and Stretch Wrap |

| Mulching Films |

| Fumigation and Solarization |

| Others |

By Geography

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Rest of South America |

| By Type | Low-Density Polyethylene (LDPE) |

| Linear Low-Density Polyethylene (LLDPE) | |

| High-Density Polyethylene (HDPE) | |

| Ethyl Vinyl Acetate / Ethylene Butyl Acrylate (EVA/EBA) | |

| Biodegradable/Bio-based Films | |

| By Application | Greenhouse Covering |

| Silage and Stretch Wrap | |

| Mulching Films | |

| Fumigation and Solarization | |

| Others | |

| By Geography | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the value of the South America agricultural films market in 2025?

It is valued at USD 540 million and is projected to reach USD 750 million by 2030.

Which application leads demand for agricultural films in South America?

Mulching films lead with 35.8% revenue share in 2024, supported by strawberry and avocado production.

Why are biodegradable films gaining traction?

Braskem's bio-PE capacity growth and regional recycled-content mandates are narrowing cost gaps and encouraging adoption.

How do reverse-logistics laws affect film suppliers?

Brazil and Chile require converters to source post-consumer resin, increasing costs but favoring firms with in-house recycling.

Page last updated on: