Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

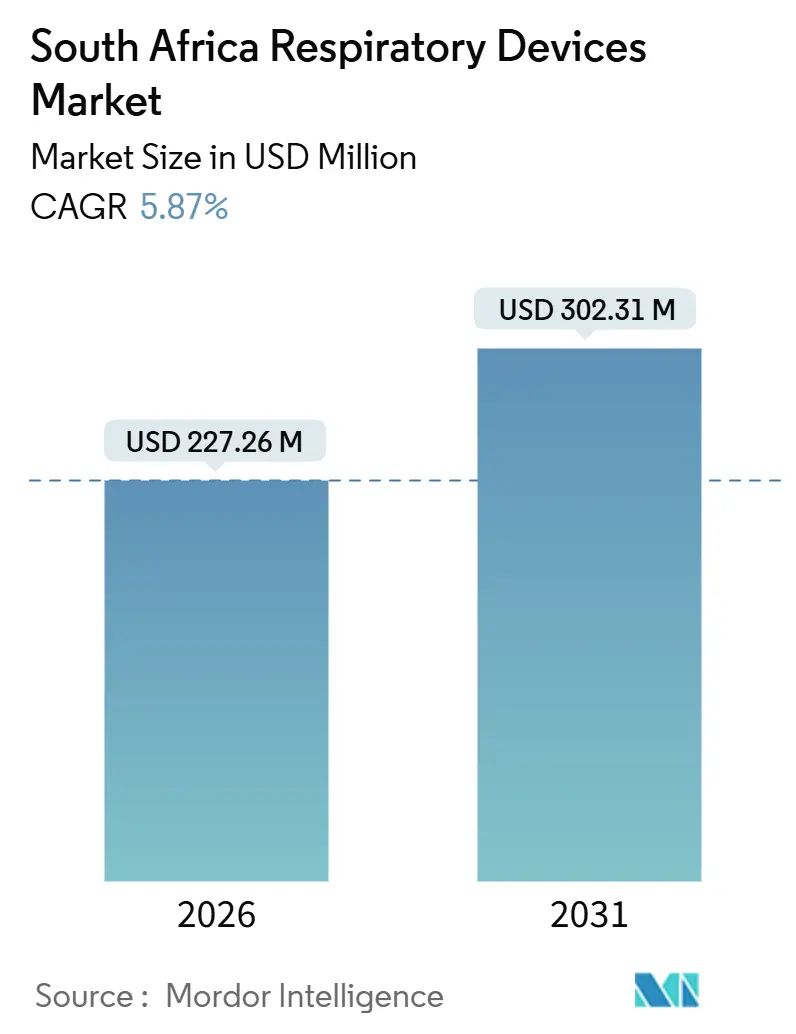

| Market Size (2026) | USD 227.26 Million |

| Market Size (2031) | USD 302.31 Million |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

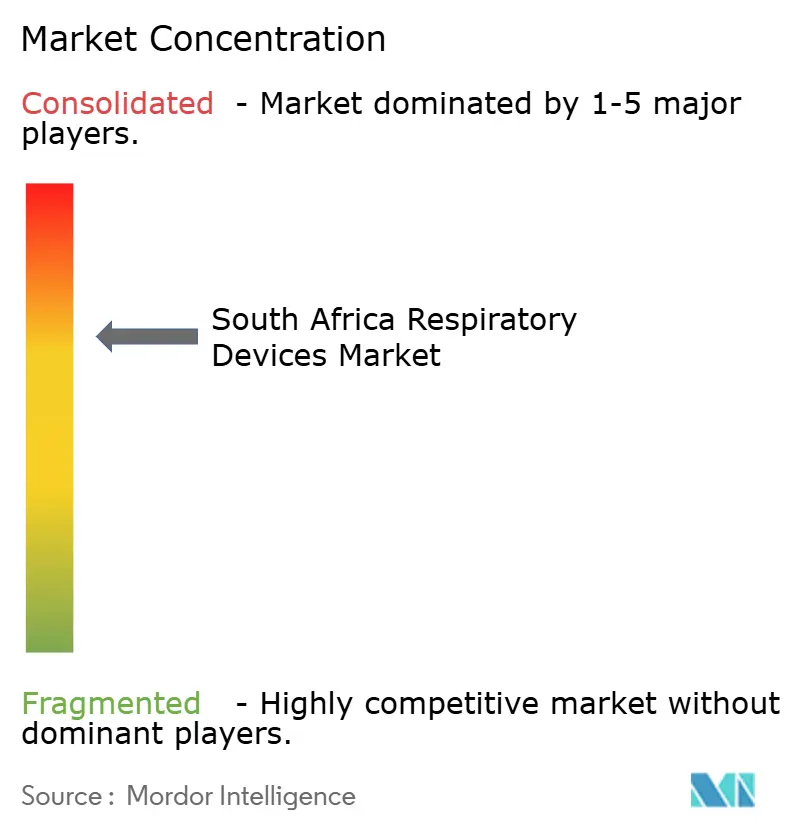

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Respiratory Devices Market Analysis by Mordor Intelligence

The South Africa Respiratory Devices Market size is estimated at USD 227.26 million in 2026, and is expected to reach USD 302.31 million by 2031, at a CAGR of 5.87% during the forecast period (2026-2031).

Accelerating chronic disease prevalence, an expanding base of home care users, and mandated infection control protocols form the core narrative of growth. Hospitals replaced aging intensive-care ventilators in the wake of the COVID-19 pandemic, while private sleep clinics upgraded to connected positive-airway-pressure (PAP) systems that upload adherence data to cloud-based dashboards. Simultaneously, demand for single-use masks and breathing circuits surged as facilities tightened hygiene standards, moving disposables ahead of capital equipment in growth momentum. A reliance above 90% on imports leaves procurement costs exposed to rand depreciation, yet new local-assembly incentives aim to trim landed expenses by 15% to 25% over the next five years. Electricity supply instability imposes a structural surcharge on devices that require continuous mains power, prompting the adoption of battery-equipped concentrators and ventilators designed for off-grid resilience.

Key Report Takeaways

- By product type, therapeutic devices led with 46.31% revenue share in 2025; disposables are forecast to expand at an 8.72% CAGR through 2031.

- By application, COPD accounted for 39.73% of the South African respiratory devices market share in 2025, while sleep apnea is projected to record the fastest growth at a 9.29% CAGR through 2031.

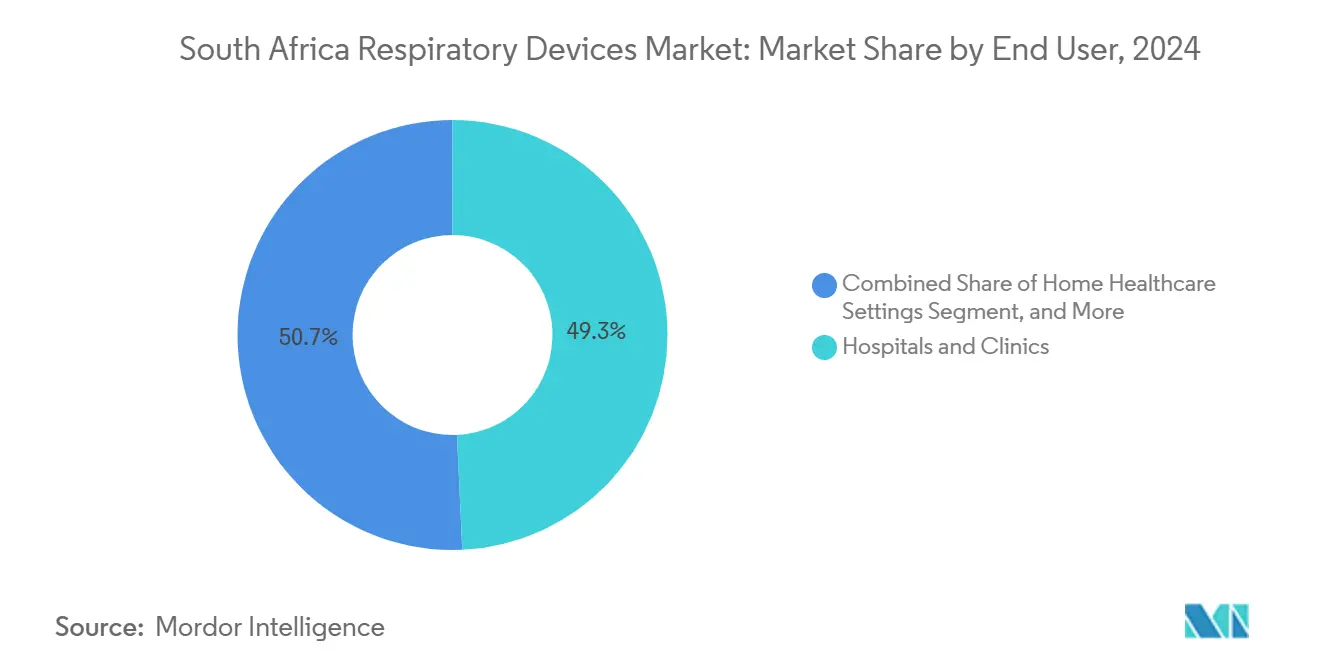

- By end user, hospitals and clinics accounted for 49.28% of the 2025 demand; meanwhile, home healthcare settings are projected to advance at a 7.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Respiratory Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of COPD, Asthma, TB & Sleep Apnea | +1.3% | National, with concentration in Gauteng, Western Cape, KwaZulu-Natal | Long term (≥ 4 years) |

| Increasing Adoption of Home-Care & Portable Devices | +1.1% | National, accelerated in urban metros (Johannesburg, Cape Town, Durban) | Medium term (2-4 years) |

| Technological Advances: AI-Enabled & Connected Devices | +0.9% | Gauteng and Western Cape private sector, gradual public-sector uptake | Medium term (2-4 years) |

| Expansion of Private-Sector Healthcare Expenditure | +0.8% | Gauteng, Western Cape, KwaZulu-Natal with spillover to Free State | Long term (≥ 4 years) |

| Growth In Tele-Respiratory and Remote-Monitoring Services | +0.7% | National, with early adoption in private medical schemes | Short term (≤ 2 years) |

| Local Manufacturing Incentives for Critical Devices | +0.5% | Gauteng and Western Cape industrial zones, potential expansion to Eastern Cape | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Rising Prevalence of COPD, Asthma, TB & Sleep Apnea

Tuberculosis notifications fell from 450,000 in 2015 to about 230,000 in 2022, yet drug-resistant strains sustain the need for portable nebulizers in community clinics. Sleep apnea affects 29.3% of rural older adults but remains underdiagnosed in urban areas, leaving a sizeable potential for PAP therapy expansion.[1]F. Xavier Gómez-Olivé et al., “Prevalence of Sleep Apnea in Rural South Africa,” BMC Public Health, bmcpublichealth.biomedcentral.com Biomass-fuel exposure and post-TB airway damage elevate COPD risk, driving oxygen-concentrator rentals across informal settlements. The prevalence of urban childhood asthma, reaching up to 20%, signals an ongoing demand for peak-flow meters and inhalers as primary care infrastructure expands. Population aging and deteriorating air quality in industrial corridors ensure these diseases remain the main demand anchor through 2031.

Increasing Adoption of Home-Care & Portable Devices

The National Health Insurance (NHI) Act prioritizes decentralized care, promoting the use of portable concentrators weighing under 3 kg for enhancing mobility and load-shedding resilience.[2]Government of South Africa, “National Health Insurance Act 2024,” gov.za Private medical schemes reimburse home PAP therapy at rates up to 50% lower than facility-based titration, incentivizing clinics to prescribe auto-adjusting devices that minimize follow-up visits. Nebulizer rentals bundled with nursing services cut readmissions by roughly 20% at leading hospital groups. Frequent power interruptions reported by 30% to 40% of home-care patients make battery backup a must-have specification. User-friendly interfaces and six-month filter-replacement intervals cater to caregivers in multigenerational households.

Technological Advances: AI-Enabled & Connected Devices

ResMed’s AirSense 11 utilizes machine-learning algorithms to tailor pressure delivery, resulting in lower early therapy abandonment rates, which are below the historical 30% mark.[3]ResMed Inc., “Annual Report 2025,” investor.resmed.com Philips’ DreamStation 2 relays nightly usage to cloud dashboards, helping clinicians intervene when adherence drops under the 4-hour threshold for reimbursement. Fisher & Paykel’s Optiflow adjusts humidity based on real-time sensor data, improving patient tolerance in step-down units. Bluetooth-enabled spirometers automatically upload lung-function data to electronic records, although public-sector adoption lags due to gaps in Wi-Fi coverage. The South African Society of Anaesthesiologists offers training modules to bridge the digital literacy divide among clinicians.

Growth in Tele-Respiratory & Remote-Monitoring Services

Pulse oximeters with cellular chips alert clinicians when saturation falls below 88%, averting emergency visits for COPD patients. Medical schemes reimburse virtual monitoring at 60% to 70% of in-person rates, opening a viable revenue stream for pulmonologists. Western Cape pilots using connected nebulizers in TB care raised treatment completion by 15%. The 2025 Telemedicine Framework mandates HL7 FHIR compliance for device interoperability; however, only 4G coverage of below 60% in parts of the Eastern Cape and Limpopo hampers real-time data flow.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost & Import Dependency of Advanced Devices | -0.6% | National, acute in public sector and rural facilities across all provinces | Long term (≥ 4 years) |

| Stringent SAHPRA Regulatory Approvals & Tender Delays | -0.4% | National, affecting both public and private sector procurement timelines | Medium term (2-4 years) |

| Shortage of Trained Respiratory Therapists | -0.3% | National, severe in Eastern Cape, Limpopo, Northern Cape, Mpumalanga | Long term (≥ 4 years) |

| Electricity-Supply Instability Impacting Device Uptime | -0.4% | National, severe in Gauteng, KwaZulu-Natal, Eastern Cape during peak demand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost & Import Dependency of Advanced Devices

More than 90% of respiratory devices are imported, making landed prices vulnerable to currency swings and customs duties. ICU ventilators that leave factories at USD 25,000 to USD 35,000 reach USD 50,000 after taxes and logistics. Median household income constraints force many sleep-apnea patients to rent PAP units for ZAR 800–1,200 per month. The 2024 Medical Devices Localization Strategy offers tax credits to spur the assembly of ventilators and concentrators; however, uptake remains slow due to unclear regulatory pathways for locally built units. Rand depreciation averaging 8% to 12% annually further stretches replacement cycles to seven years and drives demand for refurbished imports.

Electricity-Supply Instability Impacting Device Uptime

Load shedding reached 6,342 hours in 2023, compelling facilities to purchase diesel generators and UPS systems, which increase total device costs by up to 20%. Home-based COPD patients risk hypoxemic events during four-hour blackouts because concentrators halt mid-therapy. Battery-equipped portable concentrators cost 20% to 30% more but posted 12% to 15% annual sales growth as patients seek uninterrupted care. Rural public hospitals lacking backup power often resort to manual bag-valve ventilation during outages, which increases caregiver fatigue and risks of complications. Eskom pledges to cut outages below 1,000 hours by 2027, yet funding and execution risks remain high.

Segment Analysis

By Product Type: Infection-Control Mandates Lift Disposables

The South Africa respiratory devices market size for disposables is growing faster than any other category, expanding at an 8.72% CAGR to 2031 as single-use masks and breathing circuits become mandatory in revised hospital protocols. Therapeutic devices retained a 46.31% revenue share in 2025, primarily driven by the installation of ventilators and PAP units during pandemic-era upgrades. Ventilators such as the Carescape R860 and Evita V800 lead ICU budgets due to their lung-protective modes, which lower the risk of barotrauma. CPAP systems, spearheaded by AirSense 11 and DreamStation 2, account for roughly one-third of therapeutic revenue as diagnostic labs double output. Portable battery-powered concentrators captured 40% of fresh home-therapy placements in 2025, underscoring consumer preference for mobility amid load shedding.

Private pulmonologists invest in handheld spirometers, shortening the diagnosis-to-treatment window from four weeks to same-day initiation. Smart inhalers with Bluetooth-enabled adherence logs are awaiting SAHPRA clearance, creating pent-up demand among asthma specialists. Local assembly of entry-level nebulizers could shave prices by 20%, positioning domestic firms for public tenders that favor local content. Overall, tightening infection-control rules and a push toward local manufacturing position disposables and basic therapeutic devices for above-market growth.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Sleep Apnea Surges Ahead of COPD

COPD accounted for 39.73% of the revenue in 2025, driven by chronic oxygen therapy and nebulized bronchodilators. However, sleep-apnea revenue is climbing at a 9.29% CAGR as awareness and employer screening programs proliferate. Diagnostic polysomnography labs remain scarce, with fewer than 50 nationwide, so payers approving home sleep-test kits are catalyzing shifts in volume. Home studies cost ZAR 2,500–4,000 compared with ZAR 8,000–12,000 for in-lab tests, unlocking demand among middle-income groups.

Asthma affects up to 20% of urban children, resulting in substantial turnover of inhalers and nebulizers in primary-care clinics. Tuberculosis still underpins specialized demand for aerosol antibiotic nebulizers, with Omron and Drive DeVilbiss competing on ease of cleaning for community-based programs. Smaller segments such as cystic fibrosis obtain devices via SAHPRA’s Section 21 pathway, reflecting high-value but low-volume dynamics. Inclusion of chronic respiratory care in the NHI essential benefits package could add 50,000–70,000 new device users by 2028.

By End User: Home Healthcare Accelerates Under NHI

Hospitals and clinics generated 49.28% of 2025 revenue, yet home-healthcare spending is rising at a 7.64% CAGR as reimbursement models shift toward community care. Medical schemes now contract home-nursing agencies on a capitated basis, cutting per-patient cost by up to 40%. Gauteng and the Western Cape account for 60%–65% of home placements, thanks to their dense nursing networks and higher insurance coverage.

Ambulatory surgical centers utilize high-flow nasal oxygen systems to support procedural sedation, thereby creating a modest but growing market for advanced humidification platforms. Occupational health clinics in mining utilize spirometers for mandated lung-function surveillance, thereby establishing a recurring niche for diagnostic devices. Long-term care and rehabilitation centers, which collectively account for less than 10% of demand, seek battery-ready devices to hedge against power outages. Overall, the integration of portable device innovation and telehealth makes the home channel the most dynamic growth pocket through 2031.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Competitive Landscape

Five to seven multinationals, ResMed, Philips, Fisher & Paykel Healthcare, GE Healthcare, Medtronic, Drager, and Getting, are led by ICU ventilators and connected PAP systems. These firms lock in clients through service contracts, clinician education, and IT integration that raise switching costs. ResMed’s myAir platform, with 2.5 million connected users, exemplifies ecosystem monetization, where device placements generate recurring cloud subscription and replacement mask income.

Local-assembly opportunities in nebulizers and CPAP masks could trim costs by 20% and win price-sensitive public tenders. Post-acute facilities represent a white-space segment for intermediate-complexity ventilators and high-flow oxygen systems. Telemedicine platforms that bundle device rental with virtual pulmonology visits appeal to medical schemes seeking cost efficiency. SAHPRA’s alignment with ISO 13485 and IEC 60601 raises the compliance bar but offers clearer pathways for global entrants.

South Africa Respiratory Devices Industry Leaders

Drägerwerk AG & Co. KGaA

Koninklijke Philips NV

Akacia Medical & Healthcare Group

Hamilton Bonaduz AG (Hamilton Medical AG)

Teleflex Incorporated

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: Inogen launched its Aurora CPAP masks, marking its entry into the sleep apnea market. The Aurora masks are designed to enhance comfort, fit, and usability for patients who require CPAP therapy. This development expands Inogen’s portfolio beyond oxygen therapy devices, positioning the company to address a broader spectrum of respiratory health needs and tap into the growing market for sleep apnea treatments.

- October 2025: Cipla has expanded the reach of its flagship Breathefree respiratory initiative, designed to support patients with chronic respiratory conditions, including asthma and COPD. The programme focuses on raising awareness, improving access to inhalation therapy, and empowering patients through education and engagement. This expansion underscores Cipla’s commitment to strengthening respiratory care and enhancing patient outcomes across new geographies.

- May 2025: The Lung Institute of South Africa has shared updates on its ongoing research, innovation, and clinical programmes in respiratory health. The institute continues to focus on advancing treatments for lung diseases, conducting clinical trials, and promoting public health initiatives. Its work highlights the importance of local research capacity in tackling respiratory challenges and improving patient care in South Africa.

South Africa Respiratory Devices Market Report Scope

As per the scope of the report, respiratory devices include respiratory diagnostic devices, therapeutic devices, and breathing devices for administering long-term artificial respiration. It also contains resuscitation equipment, such as a breathing machine that pumps oxygen into the lungs. The South Africa Respiratory Devices Market is segmented by Type (Diagnostic and Monitoring Devices, Therapeutic Devices, and By Disposables). The report offers the value (in USD million) for the above segments.

By Product Type

| Diagnostic & Monitoring Devices | Spirometers |

| Sleep Test Devices | |

| Peak Flow Meters | |

| Pulse Oximeters | |

| Capnographs | |

| Other Diagnostic & Monitoring Devices | |

| Therapeutic Devices | CPAP Devices |

| BiPAP Devices | |

| Humidifiers | |

| Nebulizers | |

| Oxygen Concentrators | |

| Ventilators | |

| Inhalers | |

| Other Therapeutic Devices | |

| Disposables | Masks |

| Breathing Circuits | |

| Other Disposables |

By Application

| COPD |

| Asthma |

| Sleep Apnea |

| Tuberculosis |

| Other Application |

By End User

| Hospitals & Clinics |

| Home Healthcare Settings |

| Ambulatory Surgical Centers |

| Other End Users |

| By Product Type | Diagnostic & Monitoring Devices | Spirometers |

| Sleep Test Devices | ||

| Peak Flow Meters | ||

| Pulse Oximeters | ||

| Capnographs | ||

| Other Diagnostic & Monitoring Devices | ||

| Therapeutic Devices | CPAP Devices | |

| BiPAP Devices | ||

| Humidifiers | ||

| Nebulizers | ||

| Oxygen Concentrators | ||

| Ventilators | ||

| Inhalers | ||

| Other Therapeutic Devices | ||

| Disposables | Masks | |

| Breathing Circuits | ||

| Other Disposables | ||

| By Application | COPD | |

| Asthma | ||

| Sleep Apnea | ||

| Tuberculosis | ||

| Other Application | ||

| By End User | Hospitals & Clinics | |

| Home Healthcare Settings | ||

| Ambulatory Surgical Centers | ||

| Other End Users | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the South Africa respiratory devices market in 2031?

The market is expected to reach USD 302.31 million by 2031.

Which product category is growing fastest in South Africa’s respiratory segment?

Disposables such as single-use masks and breathing circuits are expanding at an 8.72% CAGR.

Why are portable oxygen concentrators gaining popularity in South Africa?

Frequent load shedding and the National Health Insurance focus on home care are driving demand for battery-equipped portable units.

Which application segment is poised for the highest growth through 2031?

Sleep apnea devices are projected to grow at a 9.29% CAGR as diagnosis rates rise.

How does electricity instability affect respiratory device usage?

Load shedding raises ownership costs by 15%–20% and forces hospitals and patients to adopt battery-ready or generator-backed solutions.