Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

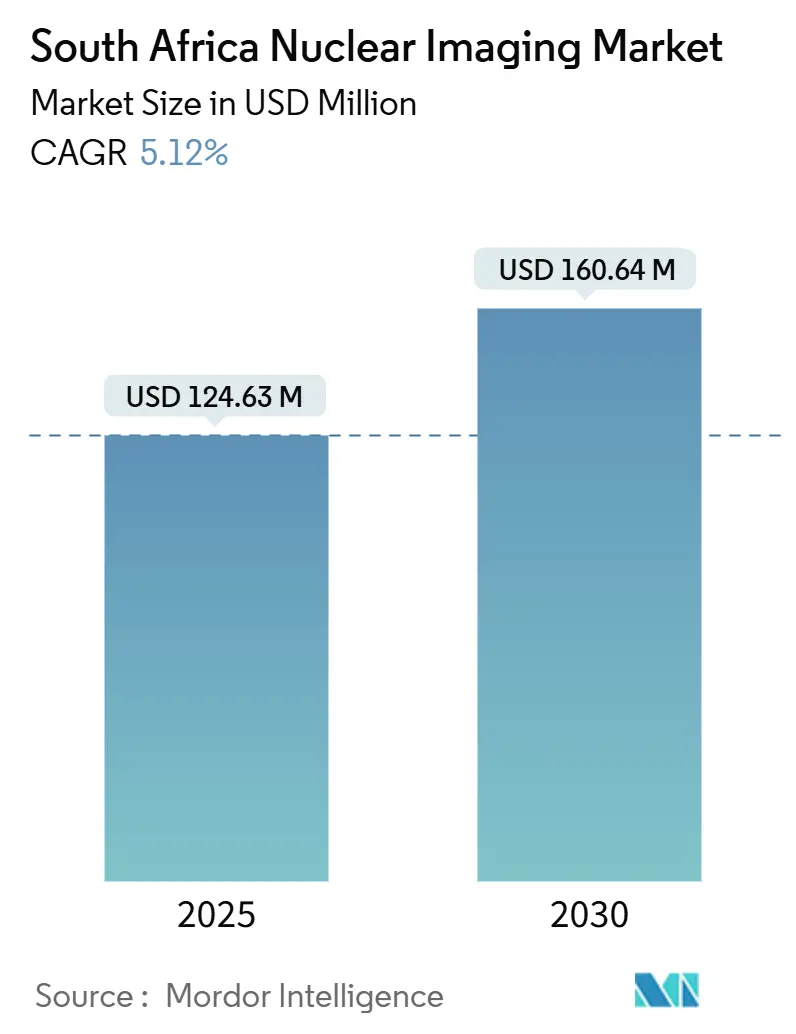

| Market Size (2025) | USD 124.63 Million |

| Market Size (2030) | USD 160.64 Million |

| Growth Rate (2025 - 2030) | 5.12% CAGR |

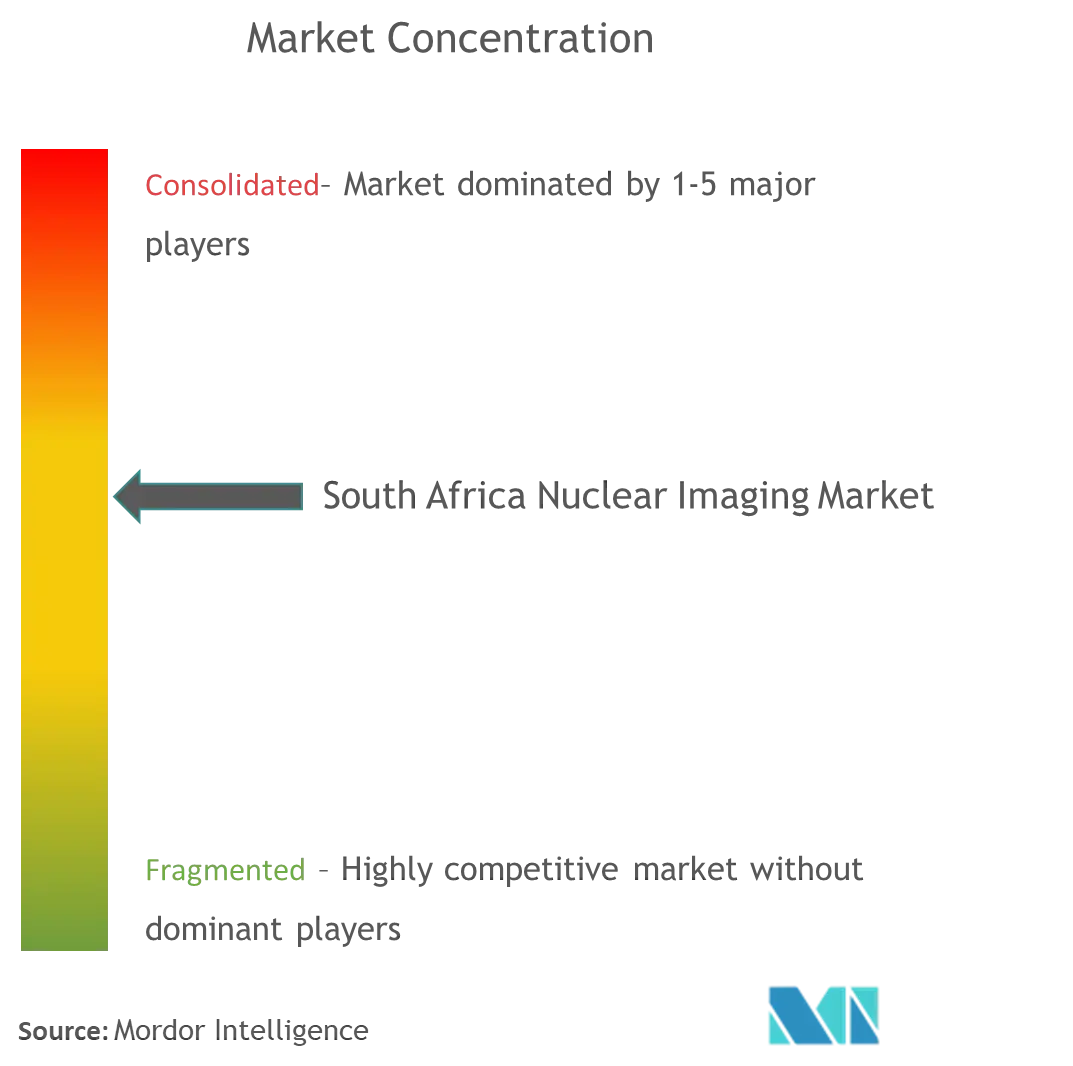

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Nuclear Imaging Market Analysis by Mordor Intelligence

The South Africa nuclear imaging market size stands at USD124.63 million in 2025 and is forecast to rise to USD160.64 million by 2030, advancing at a 5.12% CAGR. Continued demand for PET and SPECT scans, expanding private‐sector capital expenditure, and on-going National Health Insurance (NHI) roll-out sustain the current growth tempo. Domestic radioisotope production from SAFARI-1 secures clinical scheduling while underpinning export earnings, yet the reactor’s 60-year age profile elevates supply-side risk. Hybrid imaging suites in Gauteng and Western Cape signal competitive differentiation among private hospital groups. Meanwhile, the regulatory backlog at SAHPRA prolongs product launch timelines, prompting vendors to include extended service contracts and flexible financing in bids. Baseline demand is further strengthened by rising cancer and cardiovascular disease prevalence, aligning with global shifts toward precision imaging and theranostics.

Key Report Takeaways

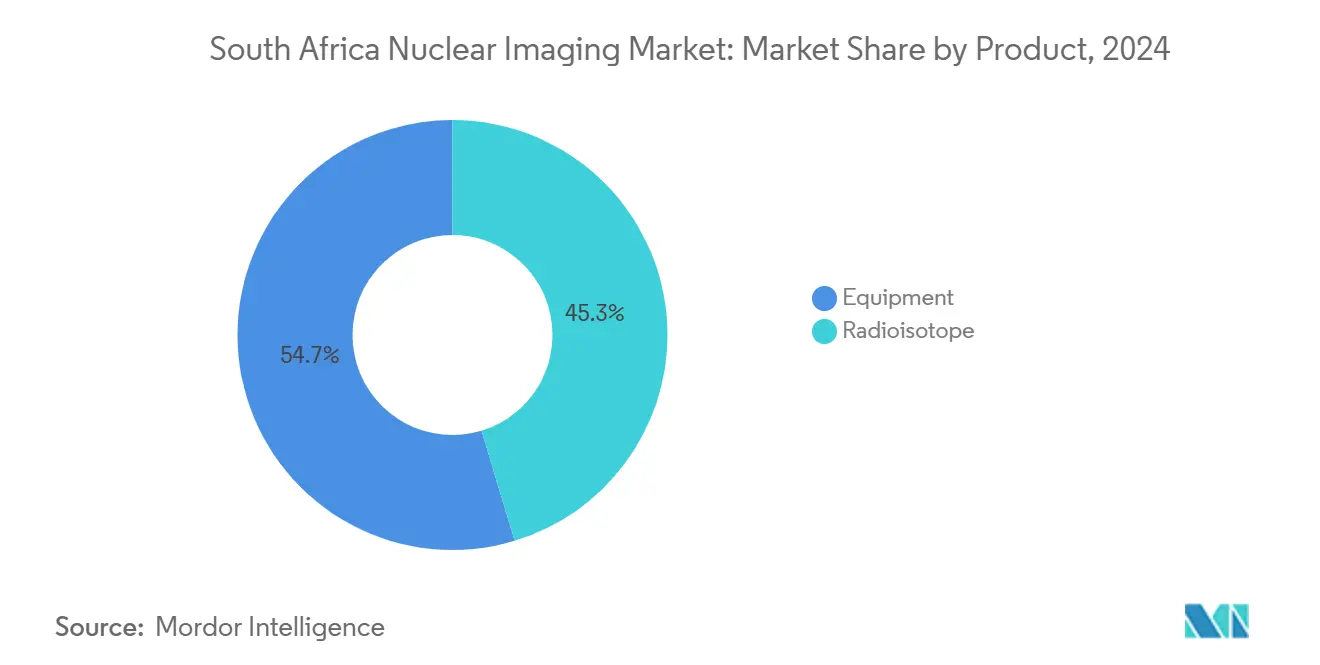

- By product, equipment led with 54.67% of South Africa nuclear imaging market share in 2024, Radioisotopes are projected to expand at a 5.67% CAGR through 2030.

- By application, cardiology captured 38.89% of South Africa nuclear imaging market size in 2024, Neurology applications are expected to grow at a 5.89% CAGR between 2025 and 2030.

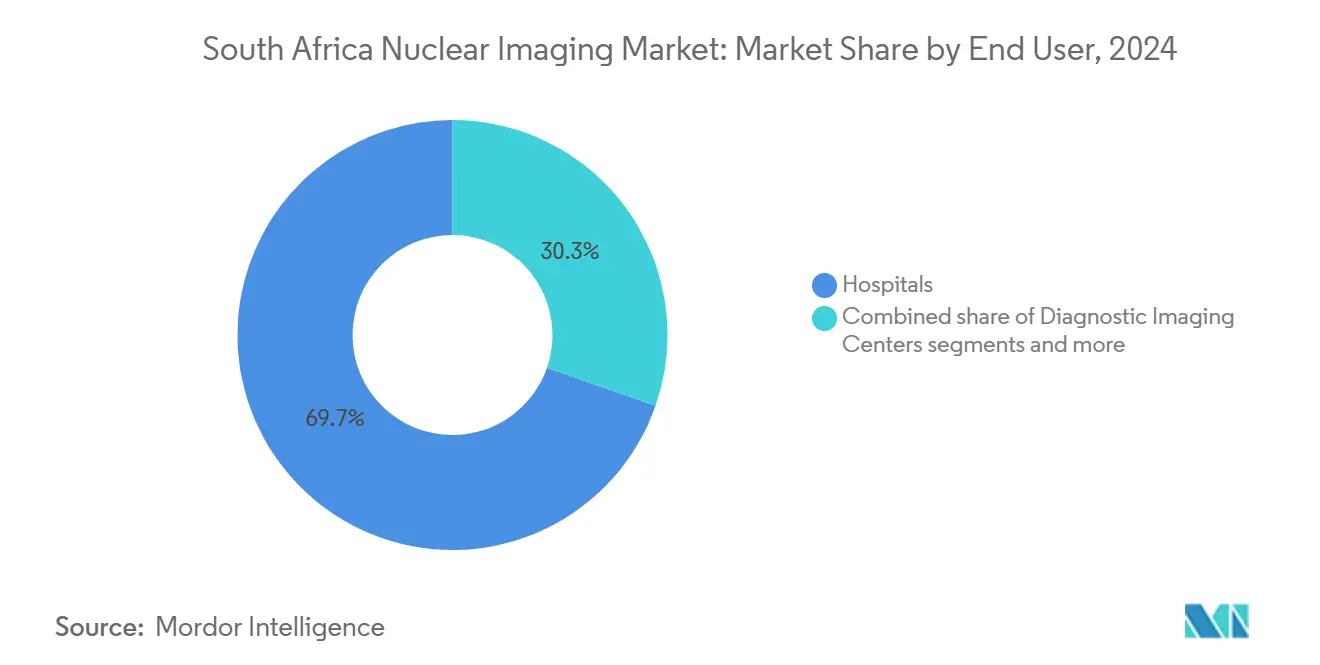

- By end user, hospitals held 69.67% revenue share in 2024, while diagnostic imaging centers register the fastest trajectory at 6.12% CAGR to 2030.

South Africa Nuclear Imaging Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising oncology & CVD incidence driving PET/SPECT demand | +1.8% | National, concentrated in Western Cape, Gauteng | Medium term (2-4 years) |

| Expanding private hospital investments in hybrid imaging suites | +1.2% | Major metropolitan areas, Western Cape, Gauteng | Short term (≤ 2 years) |

| National Health Insurance reimbursement reforms | +0.9% | National implementation, phased rollout | Long term (≥ 4 years) |

| In-country Mo-99 supply via Necsa SAFARI-1 reactor | +0.7% | National supply security, export markets | Medium term (2-4 years) |

| Growing theranostics programs at academic centers | +0.4% | Academic hospitals, Steve Biko, Tygerberg | Medium term (2-4 years) |

| Technological shift to digital detectors & AI image-reconstruction | +0.2% | Private sector early adoption, urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Oncology & CVD Incidence Driving PET/SPECT Demand

Cancer and cardiovascular disease keep imaging volumes on an upward curve as demographic aging and lifestyle transitions converge. Higher-resolution PET studies improve staging accuracy, enabling clinicians to tailor therapy plans earlier in care pathways. The 225Ac-PSMA program at Mediclinic Panorama illustrates therapeutic innovation with minimal off-target toxicity. Domestic radioisotope supply limits price volatility, keeping scan costs stable despite currency swings. Nonetheless, payer pre-authorization processes can delay access, highlighting an administrative hurdle that tempers immediate volume conversion. Governmental plans to add new scanning hubs promise scale efficiencies that may lower procedure costs over time.

Expanding Private Hospital Investments in Hybrid Imaging Suites

Life Healthcare’s multiyear, ZAR2.1 billion allocation underscores a race toward integrated PET/CT and SPECT/CT installations. Hybrid rooms compress diagnostic timelines, allowing same-day anatomical and functional studies that feed value-based care metrics. Concentration in Gauteng and Western Cape means rural patients still travel long distances, a pattern aggravated by uneven public-sector capacity. Comparative billing studies show South African private tariffs approximate those of higher-income economies despite lower national GDP per capita, suggesting premium positioning that may narrow addressable demand. Vendors now counter affordability objections with refurbished systems and usage-based payment models that shrink capital hurdles for mid-tier facilities.

National Health Insurance Reimbursement Reforms

The NHI Act introduces strategic purchasing that could fold nuclear imaging into a USD30 billion pooled budget by 2030, broadening access beyond the 16% of citizens with private cover. Health technology assessments will determine service inclusion, placing cost-effectiveness at center stage. During the transition, private medical schemes retain authority, sustaining existing referral volumes. Dual oversight—pharmaceutical quality and radiation safety—prolongs dossier review, yet accredited private providers may secure NHI contracts to bridge early capacity gaps. Successful integration hinges on robust fraud controls and clear reimbursement coding to safeguard budget integrity.

In-Country Mo-99 Supply via Necsa SAFARI-1 Reactor

SAFARI-1 contributes roughly 20% of global Mo-99, anchoring a regional export franchise while meeting domestic diagnostic demand. Cabinet approval of a ZAR1.2 billion multipurpose successor reactor secures future output, though construction timelines invite interim disruption risk. Rosatom’s planned small reactors and cyclotrons diversify isotope sources and hedge against unplanned outages. NTP Radioisotopes holds a 90% domestic share, providing scale advantages but concentrating supply risk. Conversion to low-enriched uranium keeps the facility compliant with global non-proliferation standards.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & lifecycle costs of PET/SPECT equipment | -1.4% | National, more pronounced in rural areas | Short term (≤ 2 years) |

| Shortage of nuclear medicine specialists & technologists | -0.8% | National, severe in public sector | Medium term (2-4 years) |

| Ageing SAFARI-1 reactor creating future isotope-supply risk | -0.6% | National supply chain, export markets | Long term (≥ 4 years) |

| SAHPRA approval delays for new radiopharmaceuticals | -0.4% | National regulatory bottleneck | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Lifecycle Costs of PET/SPECT Equipment

Purchase prices for state-of-the-art PET/CT scanners can exceed USD2 million, straining public budgets. Maintenance and calibration add recurring expenses that often outpace CPI inflation, particularly when imported parts require hard-currency outlays. Private facilities pass costs to patients, yielding tariffs comparable with OECD averages despite South Africa’s lower income baseline. Refurbished systems offer savings but raise questions about warranty coverage and detector longevity. Leasing and pay-per-scan contracts help first-time entrants, yet these models remain underused in public procurement.

Shortage of Nuclear Medicine Specialists & Technologists

Only 26.8% of imaging centers employ the required complement of medical physicists, causing scheduling bottlenecks and quality-assurance gaps30198-3/abstract). Training pipelines output fewer than 15 new physicists annually, insufficient to meet incremental equipment installations. The diagnostic radiology workforce has diversified demographically, yet absolute numbers lag population norms. Private-sector internships could absorb surplus graduates from related physics disciplines, but stipend funding remains inconsistent. International recruitment supplies a short-term stopgap but risks brain-drain critiques.

Segment Analysis

By Product: Equipment Remains Foundational While Radioisotopes Accelerate

Equipment held 54.67% South Africa nuclear imaging market share in 2024, with PET/CT upgrades accounting for the largest capital spending tranche. The South Africa nuclear imaging market size tied to equipment is projected to expand steadily as private groups refresh analog fleets and public tenders catch up to digital standards. Radioisotopes, however, post the faster 5.67% CAGR, buoyed by theranostics demand and domestic Mo-99 production security.

SPECT tracers such as Technetium-99m dominate volume, leveraging SAFARI-1’s weekly output. PET tracers led by Fluorine-18 underpin oncology and neurology protocols, while Gallium-68 enables PSMA imaging. ASP Isotopes’ enrichment of Ytterbium-176 positions the nation to support Lutetium-177 therapy production, further tilting momentum toward therapeutic isotopes. Vendors improve system uptime with AI-driven predictive maintenance, reducing unscheduled downtime that historically plagued public installations.

By Application: Cardiology Anchors Volume, Neurology Captures Growth

Cardiology led with 38.89% South Africa nuclear imaging market size in 2024 as SPECT myocardial perfusion imaging (MPI) remained standard for ischemia evaluation. Neurology, though smaller, outpaces other segments with a 5.89% CAGR on the back of dementia screening programs and FDG-PET uptake.

The South Africa nuclear imaging market share for neurology will likely increase as third-generation tracers for amyloid and tau receive approvals. Oncology benefits from dual imaging-therapy workflows where PSMA scans guide alpha- or beta-emitter treatments, closing feedback loops within a single care episode. Thyroid imaging maintains steady demand, supported by standard iodine protocols that require minimal capital investment. Cross-disciplinary protocols, such as infection imaging with labeled white blood cells, keep the other-applications bucket relevant, though absolute volumes remain modest.

By End User: Hospitals Dominate While Imaging Centers Gain Speed

Hospitals controlled 69.67% of total examinations in 2024, reflecting their integrated service footprints and ready access to surgical and oncology suites. Diagnostic centers, however, enjoy a 6.12% CAGR as entrepreneurs leverage flexible hours and suburban locations to attract insured walk-ins. Private providers integrate PACS and cloud reporting, shortening turnaround and winning referrals from busy cardiology clinics.

The South Africa nuclear imaging market size sourced from academic institutes remains smaller but strategic; these sites handle high-complexity theranostics and spearhead clinical trials. NHI purchasing could reallocate volumes once accreditation frameworks mature, shifting some activity from private hospitals to contracted independent centers. All end-user categories grapple with SAHPRA compliance, and most pursue ISO 9001 or ISO 13485 certification to streamline audits.

Geography Analysis

Western Cape and Gauteng account for well over half of national equipment installations, propelled by higher private-insurance penetration and proximity to academic hubs. Gauteng hosts the NuMeRI facility and the Steve Biko Academic Hospital, reinforcing its status as a translational research nexus. Western Cape benefits from Tygerberg’s protocol innovation and Mediclinic’s aggressive suite roll-outs.

KwaZulu-Natal and Eastern Cape trail in scanner density, creating outbound patient flows to metropolitan centers. Limpopo’s workforce growth accelerates from a low base, signaling potential for future site expansion once NHI reimbursements stabilize. Free State and Northern Cape rely on mobile outreach and tele-consulting, methods that partially offset travel distances.

Internationally, South Africa functions as a continental nuclear medicine anchor, supplying over 40 African hospitals with Mo-99 derivatives. The African Association of Radiopharmacy, co-chaired by South African experts, underlines leadership in professional standards. This role attracts technology transfers and training grants that may ease provincial inequities over the forecast horizon.

Competitive Landscape

Global OEMs—GE HealthCare, Siemens Healthineers, Philips—compete fiercely for replacement cycles, bundling service, AI modules, and financing to entice hospital groups. GE HealthCare’s acquisition of Nihon Medi-Physics expands its radiopharmaceutical line-up and could reshape tracer availability and pricing locally.

On the isotope front, NTP Radioisotopes wields scale economics while ASP Isotopes enters with niche enriched products, adding supply diversity. Smaller cyclotron operators offer F-18 FDG regionally but lack nationwide distribution. Clinical service competition centers on patient experience; providers differentiate with shorter wait times, AI-enhanced reporting, and bundled oncology pathways.

Moderate market concentration persists because high fixed costs deter new entrants, yet no single player exceeds 25% of service volumes. Workforce limitations act as a protective moat for incumbents but also cap total market throughput. OEM after-sales networks influence tender awards, as hospitals favor suppliers with local engineer pools capable of sub-4-hour response times.

South Africa Nuclear Imaging Industry Leaders

Bracco Imaging Spa

GE Healthcare

Siemens AG

Koninklijke Philips N.V.

Canon Medical Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ASP Isotopes announced commercial production commencement of Enriched Carbon-14 and Silicon-28 at its three facilities in Pretoria, alongside proposed secondary listing on the Johannesburg Stock Exchange to enhance liquidity and attract South African institutional investors, emphasizing the country's strategic position in isotope production for healthcare applications

- April 2025: ASP Isotopes appointed respected South African businessman Sipho Maseko to its board, highlighting South Africa's potential in producing critical materials for nuclear medicine industries, while planning separation of nuclear fuels and isotope services into independent entities by second half 2025

South Africa Nuclear Imaging Market Report Scope

As per the scope of this report, Nuclear medicine imaging procedures are non-invasive, with the exception of intravenous injections, and are usually painless medical tests that help physicians diagnose and evaluate medical conditions. These imaging scans use radioactive materials called radiopharmaceuticals or radiotracers. These radiopharmaceuticals are used in diagnosis and therapeutics. South Africa Nuclear Imaging Market is segmented by Product (Equipment, Diagnostic Radioisotopes), and Application (SPECT Applications, PET Applications). The report offers the value (in USD million) for the above segments.

By Product

| Equipment | ||

| Radioisotope | SPECT Radioisotopes | Technetium-99m (TC-99m) |

| Thallium-201 (TI-201) | ||

| Gallium (Ga-67) | ||

| Iodine (I-123) | ||

| Other SPECT Radioisotopes | ||

| PET Radioisotopes | Fluorine-18 (F-18) | |

| Rubidium-82 (RB-82) | ||

| Other PET Radioisotopes | ||

By Application

| Cardiology |

| Neurology |

| Thyroid |

| Oncology |

| Other Applications |

By End User (Value)

| Hospitals |

| Diagnostic Imaging Centres |

| Academic & Research Institutes |

| By Product | Equipment | ||

| Radioisotope | SPECT Radioisotopes | Technetium-99m (TC-99m) | |

| Thallium-201 (TI-201) | |||

| Gallium (Ga-67) | |||

| Iodine (I-123) | |||

| Other SPECT Radioisotopes | |||

| PET Radioisotopes | Fluorine-18 (F-18) | ||

| Rubidium-82 (RB-82) | |||

| Other PET Radioisotopes | |||

| By Application | Cardiology | ||

| Neurology | |||

| Thyroid | |||

| Oncology | |||

| Other Applications | |||

| By End User (Value) | Hospitals | ||

| Diagnostic Imaging Centres | |||

| Academic & Research Institutes | |||

Key Questions Answered in the Report

What is the current value of the South Africa nuclear imaging market?

The market is valued at USD124.63 million in 2025 and is forecast to reach USD160.64 million by 2030.

How fast is demand for radioisotopes growing?

Radioisotopes are projected to expand at a 5.67% CAGR through 2030, outpacing equipment growth.

Which application segment is expanding the quickest?

Neurology is advancing at a 5.89% CAGR owing to increased PET adoption for dementia diagnosis.

Why is SAFARI-1 important to imaging services?

The reactor supplies about 20% of global Mo-99, guaranteeing tracer availability for local scans and exports.

How will National Health Insurance affect imaging access?

NHI strategic purchasing could finance nuclear imaging for uninsured citizens, potentially increasing scan volumes nationwide.

Page last updated on: