Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

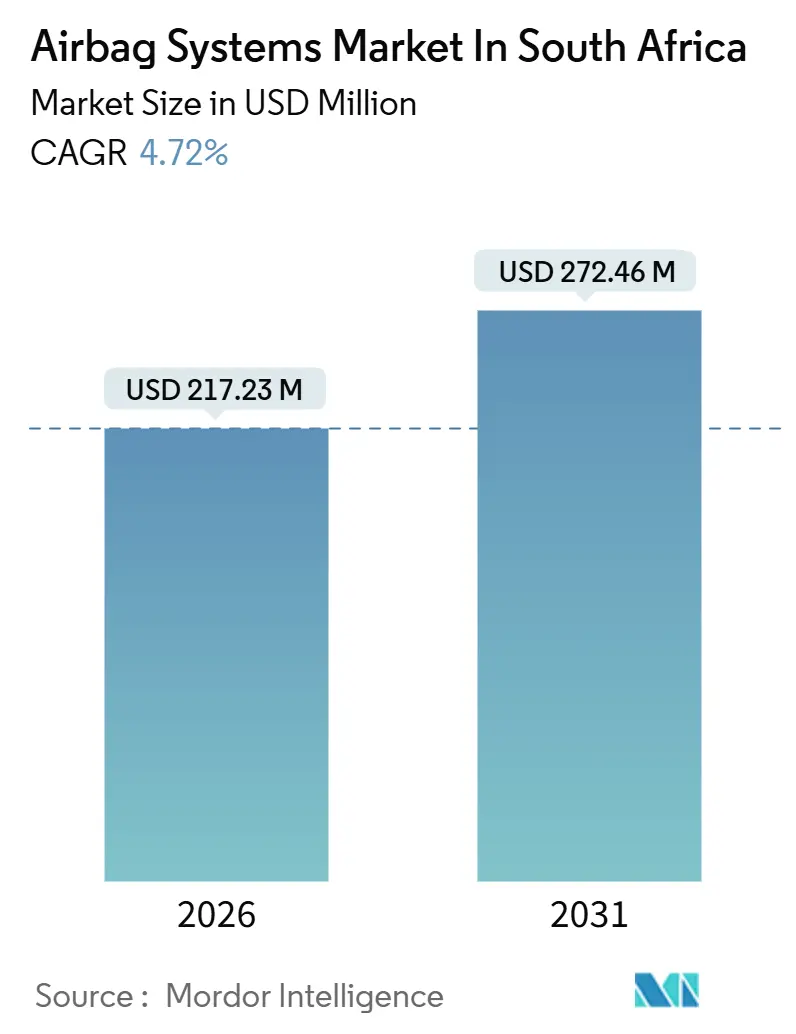

| Market Size (2026) | USD 217.23 Million |

| Market Size (2031) | USD 272.46 Million |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Analysis of Airbag Systems Market In South Africa by Mordor Intelligence

The airbag systems market size in South Africa stands at USD 217.23 million in 2026 and is on track to touch USD 272.46 million by 2031, expanding at a 4.72% CAGR over the forecast period. Growth stems from UNECE-aligned regulations, rising SUV penetration, and localization incentives that lower logistics costs for inflator modules. Curtain and knee airbags are gaining traction as OEMs chase five-star Global NCAP ratings, while hybrid inflators provide a hedge against platinum-group‐metal volatility. Connected-safety modules that merge the airbag ECU with telematics are opening recurring-revenue streams for automatic crash notification and software updates. Load-shedding, however, remains a cost headwind, prompting tier-1 suppliers to deploy battery energy‐storage systems and backup generation to protect uptime.

Key Report Takeaways

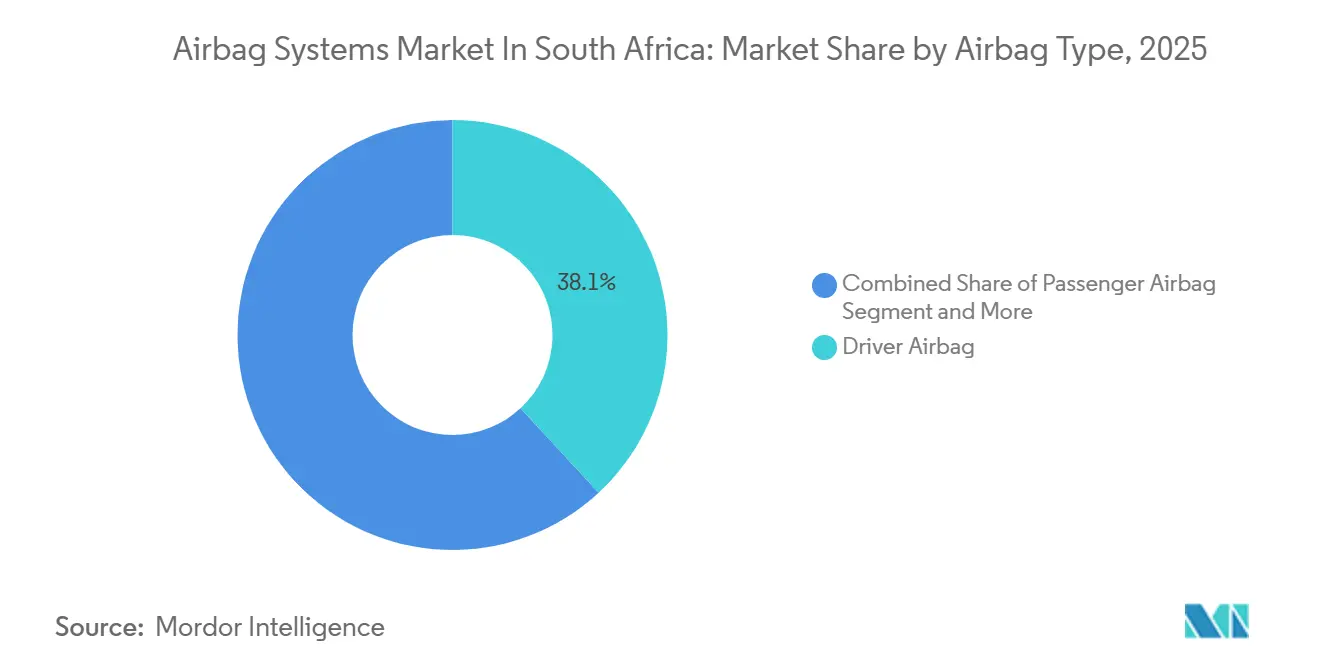

- By airbag type, driver airbags led with a 38.07% share of the airbag systems market in 2025, whereas curtain airbags are forecast to post a 9.84% CAGR through 2031.

- By inflator type, pyrotechnic inflators accounted for 64.12% of the airbag systems market share in 2025, while hybrid inflators are projected to advance at a 12.43% CAGR over the same period.

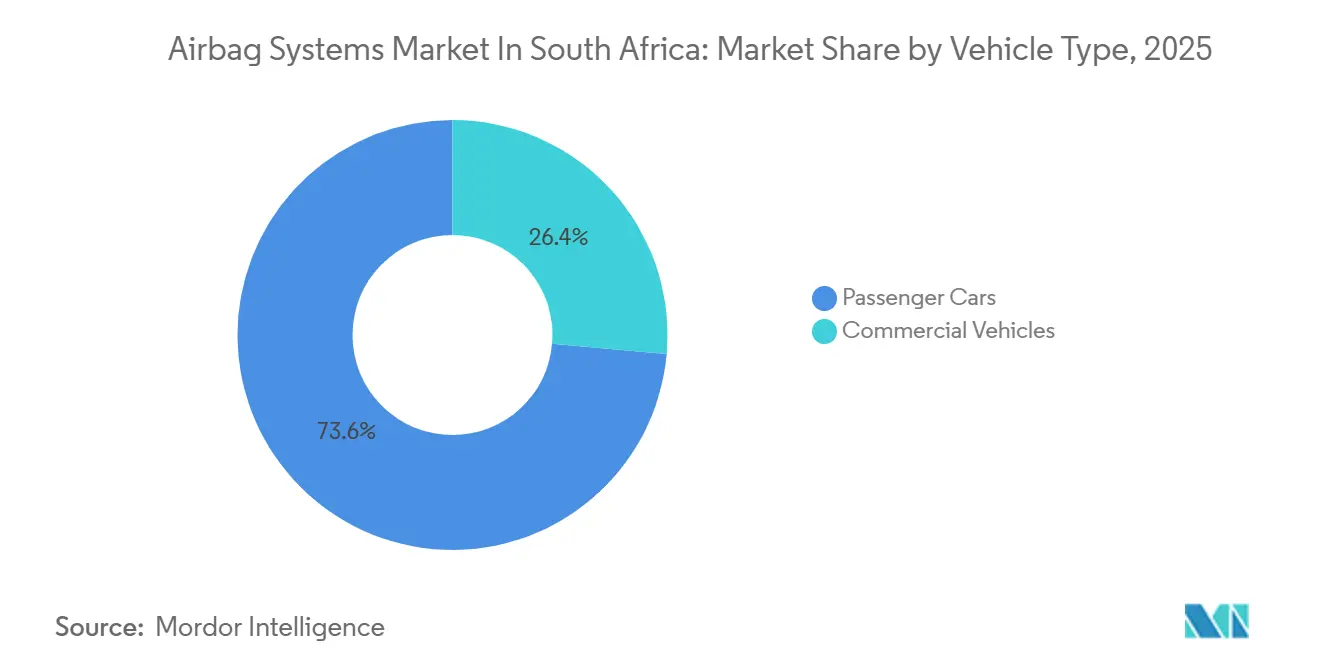

- By vehicle type, passenger cars captured 73.56% of the airbag systems market size in 2025, yet commercial vehicles are poised for a 7.62% CAGR to 2031.

- By distribution channel, OEM factory-fit sales represented 92.08% of installations in 2025, but aftermarket replacement is expected to expand at a 15.27% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Airbag Systems Market In South Africa

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Passenger-Car Production | +1.8% | Gauteng province, with spillover to Eastern Cape (East London, Port Elizabeth) | Short term (≤ 2 years) |

| Stringent UNECE Regulations | +1.2% | National, with early enforcement in Gauteng and Western Cape | Medium term (2–4 years) |

| OEM Localization Incentives | +0.9% | National, concentrated in Gauteng (Rosslyn, Silverton) and Eastern Cape | Medium term (2–4 years) |

| Escalating Demand for Curtain and Knee Airbags | +0.8% | National, led by Gauteng and Western Cape urban centers | Short term (≤ 2 years) |

| Rise of Connected-Safety Modules | +0.7% | National, with pilot deployments in Johannesburg, Cape Town, Durban | Long term (≥ 4 years) |

| Increasing Export-Oriented Vehicle Manufacturing | +0.6% | National, export hubs in Gauteng (OR Tambo logistics) and Eastern Cape (Port Elizabeth) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing Passenger-Car Production in Gauteng

Passenger-car assembly capacity in Gauteng has risen sharply since 2024 as multinational OEMs ramp local production to serve domestic demand and EU-bound exports[1]Mandla Mpangase, "Gauteng assesses its readiness for a transformed automotive sector," Tshwane Automotive Special Economic Zone, tasez.co.za. . Toyota, BMW, Ford, and Nissan plants clustered within 50 km of Pretoria benefit from shared suppliers, enabling just-in-time delivery of airbag modules that lower inventory costs. The same concentration, however, magnifies exposure to load-shedding; one Stage 4 blackout in October 2025 halted three assembly lines for 14 hours. Tier-1 suppliers have answered with onsite generation and shift-pattern adjustments, keeping delivery performance above 95%. Current momentum is expected to hold through 2027 as new derivatives of the Hilux, X3, and Ranger move to full six-airbag suites.

Stringent UNECE-Aligned Frontal-Impact Regulations

South Africa’s adoption of UNECE Regulations 94 and 95 converted dual-frontal and side-impact systems from optional to mandatory[2]"COMPULSORY SPECIFICATION FOR MOTOR VEHICLES OF CATEGORY M1," UNECE, unece.org.. A compressed 24-month retrofit window is forcing OEMs to accelerate hybrid-inflator adoption because the architecture can modulate deployment force for varying occupant loads. Tier-1 suppliers equipped with certified test centers now enjoy shorter homologation cycles, while those lacking in-country validation face costlier overseas testing. Compliance also positions locally built vehicles for duty-free access to Middle-Eastern and sub-Saharan markets that mirror UNECE standards, reinforcing export volumes.

OEM Localization Incentives Under the South Africa Automotive Masterplan

The Automotive Masterplan 2035 sets a target of increasing local content in South African assembled vehicles to 60% by 2035[3]Justin Barnes, "South Africa’s automotive industry masterplan to 2035," South African Automotive Masterplan Project, afsa.org.za.. Airbag systems are difficult to localize fully because propellant chemicals and micro-electronics remain imported, yet cushion cutting, sewing, and module assembly have migrated to Rosslyn and East London. Lead times fell from 9 to 4 weeks, creating flexibility for last-minute model-mix changes. Incentives further include a 150% tax deduction on electric-vehicle investments effective March 2026, encouraging the co-location of battery-disconnect safety systems with airbag ECU manufacturing.

Escalating Demand for Curtain and Knee Airbags in SUVs

This segment shift is accelerating the adoption of curtain airbags, which deploy from the roof rail to protect occupants in side-impact and rollover scenarios, and knee airbags, which reduce lower-extremity injuries by cushioning the driver's knees against the instrument panel. BMW's iX, tested by Euro NCAP in 2021, demonstrated the efficacy of a centre airbag (deployed between front-seat occupants) in mitigating far-side impacts, a design now being adapted for the X3 platform assembled in Rosslyn. Curtain airbags require longer inflator tubes and larger gas volumes than frontal systems, which raises bill-of-materials costs by 18–22%. However, OEMs are absorbing this premium to achieve five-star Global NCAP ratings, a marketing differentiator in South Africa's competitive SUV segment.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Platinum-Group Metal Prices Elevating Inflator Costs | -1.3% | National, with acute impact on Gauteng and Eastern Cape suppliers | Short term (≤ 2 years) |

| Intermittent Load-Shedding Disrupting Tier-2 Suppliers | -0.9% | National, most severe in Gauteng, KwaZulu-Natal, and Eastern Cape | Short term (≤ 2 years) |

| Slow Adoption of Aftermarket Replacement Airbags | -0.6% | National, concentrated in informal repair networks in townships | Medium term (2–4 years) |

| Cost Sensitivity in Entry-Level Vehicles Limiting Advanced Airbag Penetration | -0.5% | National, affecting budget segments in Gauteng, Western Cape, and KwaZulu-Natal | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Slow Adoption of Aftermarket Replacement Airbags

South Africa's aftermarket for airbag replacement remains underdeveloped, with an estimated 60–70% of deployed airbags never replaced following a collision. This stems from three factors: high replacement costs (ZAR 8,000–15,000, or USD 430–810, for a driver-side module), limited insurance penetration (only 35% of vehicles carry comprehensive coverage), and a cultural preference for cosmetic repairs over safety-system restoration. Informal repair networks in townships often bypass airbag replacement entirely, reinstalling the steering wheel without a functional module to reduce costs.

Cost Sensitivity in Entry-Level Vehicles Limiting Advanced Airbag Penetration

Entry-level passenger cars, defined as models priced below ZAR 250,000 (approximately USD 13,500), account for a significant share of new-vehicle sales in South Africa, a segment where OEMs compete primarily on affordability. These models typically feature a single driver's airbag and, in some cases, a passenger airbag, but omit side-curtain, knee, or center airbags to keep the bill-of-materials costs down. Adding a full six-airbag suite (dual frontal, dual side-curtain, dual side-thorax) raises vehicle cost by ZAR 6,000–9,000 (USD 320–485), equivalent to 2.4–3.6% of the base price, a premium that budget-conscious buyers are unwilling to pay. This cost sensitivity is most acute in rural provinces such as Limpopo and Mpumalanga, where median household incomes are 30–40% below the national average and vehicle purchase decisions prioritize fuel economy and maintenance costs over safety features.

Segment Analysis

By Airbag Type: Driver Airbags Cement Leadership in SUVs

Driver airbags dominate the market with a 38.07% share, while curtain airbags are forecasted to grow at a 9.84% CAGR, the highest among all types in the airbag systems market. Knee airbags, though only a small percentage of volume, gain steady traction among fleet buyers who seek to curb workers ' compensation claims.

Centre and pedestrian airbags still hold niche positions but benefit from export programs demanding full occupant-protection suites. The Toyota Hilux now sells domestically with the same six-airbag set as export variants, signaling a convergence that should lift the airbag systems market share of supplemental devices during 2027–2031. BMW’s iX platform, assembled in Rosslyn, demonstrates how centre airbags prevent occupant-to-occupant contact and is expected to influence future SUV offerings.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Inflator Type: Hybrid Designs Accelerate

Pyrotechnic inflators accounted for 64.12% of the airbag systems market in 2025, primarily favored for frontal airbags that require millisecond inflation. Hybrid units, which combine modest pyrotechnic charges with compressed gas, are projected to grow at 12.43% annually, driven by lower rhodium dependency and readiness for multi-stage deployment.

Electric-vehicle growth in South Africa—helped by a 150% tax deduction effective March 2026—favors hybrid inflators because battery-disconnect safety logic integrates seamlessly with staged inflation. Denso and ZF have both added hybrid capacity near East London, cutting import lead times to under 30 days and strengthening their bids for the next Ranger and X3 refresh cycles.

By Vehicle Type: Commercial Fleets Close the Safety Gap

Passenger cars represented 73.56% of installations in 2025, yet their growth is moderating as baseline dual-airbag fitment nears saturation. Commercial vehicles will advance 7.62% yearly through 2031, driven by logistics operators that quantify downtime and injury-related costs. A Johannesburg freight trial found a 22% drop in driver-injury severity after retrofitting frontal airbags, prompting a fleet-wide rollout by 2027.

Heavy trucks lag at 15% airbag penetration but face rising Euro-5-equivalent emissions rules in 2027 that align cab safety with environmental upgrades. Module suppliers that offer robust, vibration-tolerant designs stand to capture this late-cycle demand and lift the airbag systems market size tied to commercial platforms.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Aftermarket Emerges from a Small Base

OEM factory-fit held 92.08% of 2025 volume, yet the aftermarket CAGR of 15.27% will inch share upward as the 2015–2020 vehicle cohort ages. Insurance-approved body shops are spreading beyond Gauteng and Western Cape, expanding addressable demand for genuine replacement modules. Proposed regulatory inspections could compel the replacement of non-functional airbags, materially lifting the airbag systems market size attached to the aftermarket from 2027 onward.

Still, the channel faces hurdles: proprietary ECU algorithms limit entry to OEM-branded parts, keeping price points elevated. Tier-1 suppliers are lobbying for standardized diagnostic protocols, which would enable independent repairers to verify proper deployment logic post-installation and accelerate market acceptance.

Geography Analysis

Gauteng accounted for an estimated 58% of the airbag systems market in 2025 owing to its dense cluster of OEM assembly lines. The co-location of Autoliv, ZF, and Joyson module plants within a 30 km radius sustains inventory turns and supports export logistics through OR Tambo International Airport. Yet the same density magnifies disruption risk when Stage 4 load-shedding halts multiple plants simultaneously, pressing suppliers to install battery storage and diesel gensets that add 2–3 percentage-point cost to margins.

The Eastern Cape, anchored by Volkswagen’s Kariega plant and expanding light-commercial assembly, held 18% share. Although local tier-2 depth remains thin, ongoing inflator sub-assembly investments are reducing over-the-road lead times from Gauteng by two days. Western Cape’s 14% share is driven less by production and more by aftermarket demand emanating from Cape Town’s high insurance penetration and dense collision-repair infrastructure.

KwaZulu-Natal contributed 7%, benefiting from Toyota’s Prospecton output and the port of Durban for component imports. The remaining provinces combine for 3%, largely through independent workshops servicing older vehicles with low airbag content. Export-driven convergence of domestic and foreign specifications suggests that the Eastern Cape share will rise modestly by 2031 as new SUV derivatives roll off its lines with full six-airbag suites, nudging the national distribution toward a more balanced provincial footprint.

Competitive Landscape

Autoliv, ZF Friedrichshafen, and Joyson Safety Systems collectively held a significant portion of South African OEM volume in 2025. Competition is sharpest in curtain airbags, where Autoliv pushes hybrid inflators and ZF leans on lighter stored-gas units to shave grams for fuel-economy targets.

Technology sits at the heart of differentiation. Bosch and Continental embed secure boot and over-the-air update capability in their ECUs, while Teijin leverages aramid-fiber leadership to backward-integrate into module assembly, targeting local OEMs that seek domestic content credits. Autoliv’s USD 2.5 billion share repurchase announced July 2025 demonstrates confidence that next-generation connected-safety modules will offset commodity price swings.

Cybersecurity has become a bid-qualification criterion; suppliers that meet ISO 21434 standards on cyber risk win preferred status for 2027 model launches. Local tier-2 firms with less than USD 50 million in sales struggle to fund the software and validation expertise now required, making strategic partnerships with global majors increasingly common.

Leaders of Airbag Systems Market In South Africa

-

Autoliv Inc.

-

Continental AG

-

Robert Bosch GmbH

-

Joyson Safety Systems

-

ZF Friedrichshafen AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: Stellantis South Africa has reiterated its ongoing Takata airbag recall, urging owners of vehicles from Citroën, DS, Chrysler, Jeep, Opel, Peugeot, and legacy Chevrolet brands to check their recall status immediately. The company emphasized that defective Takata inflators pose a serious risk of injury or death if deployed, and all affected units can be replaced free of charge at authorized service centers.

- December 2025: The National Consumer Commission (NCC) announced a safety recall affecting over 18,600 Kia vehicles and 323 Jeep Wrangler units, citing potential airbag circuit faults that may prevent proper deployment in the event of a crash. Owners have been advised to visit dealerships for free inspections and repairs to ensure compliance with safety standards.

Scope of Report on Airbag Systems Market In South Africa

The South Africa Airbag Systems Market covers the current and upcoming trends with recent technological developments. The report will provide a detailed analysis of various areas of the market by type, application and technology. The market share of significant automotive sensor manufacturing companies and country level analysis will be provided in the report.

By Airbag Type

| Driver Airbag |

| Passenger Airbag |

| Curtain Airbag |

| Knee Airbag |

| Others |

By Inflator Type

| Pyrotechnic |

| Stored Gas |

| Hybrid |

By Vehicle Type

| Passenger Cars |

| Commercial Vehicles |

By Distribution Channel

| OEM Factory-Fit |

| Aftermarket Replacement |

| By Airbag Type | Driver Airbag |

| Passenger Airbag | |

| Curtain Airbag | |

| Knee Airbag | |

| Others | |

| By Inflator Type | Pyrotechnic |

| Stored Gas | |

| Hybrid | |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| By Distribution Channel | OEM Factory-Fit |

| Aftermarket Replacement |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the airbag systems market in South Africa today?

The airbag systems market size stands at USD 217.23 million in 2026 and is projected to reach USD 272.46 million by 2031.

What is the expected growth rate for airbag systems through 2031?

The market is forecast to register a 4.72% CAGR, driven by stricter UNECE regulations and the SUV sales mix.

Which airbag type is expanding quickest?

Curtain airbags are advancing at a 9.84% CAGR as SUVs gain share and insurers reward vehicles fitted with side-impact protection.

Why are hybrid inflators gaining traction?

Hybrid inflators curb platinum-group-metal exposure and enable multi-stage deployment, supporting a forecast 12.43% CAGR through 2031.

What challenges does load-shedding pose to suppliers?

Stage 4 power outages spoil climate-sensitive inflator production, forcing firms to invest in costly battery storage or lose delivery reliability.