Solar Water Heater Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

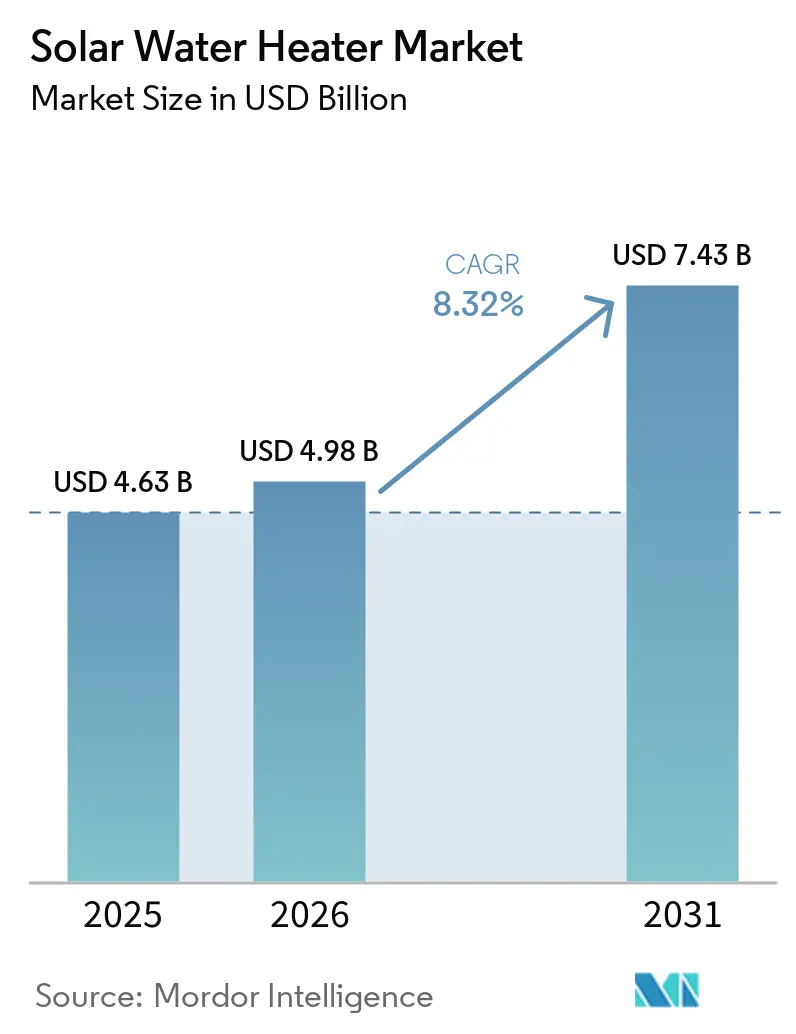

| Market Size (2026) | USD 4.98 Billion |

| Market Size (2031) | USD 7.43 Billion |

| Growth Rate (2026 - 2031) | 8.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solar Water Heater Market Analysis by Mordor Intelligence

The Solar Water Heater Market size was valued at USD 4.63 billion in 2025 and is estimated to grow from USD 4.98 billion in 2026 to reach USD 7.43 billion by 2031, at a CAGR of 8.32% during the forecast period (2026-2031).

Policy mandates, declining collector prices, hybrid-system retrofits, and industrial low-temperature process-heat demand are accelerating adoption across residential, commercial, and industrial settings. Glazed collectors, evacuated tubes, and flat plates benefit from improved selective coatings that boost winter efficiency, while vertical integration in China and India is compressing delivered costs for global buyers. Heat-pump/solar hybrids are redefining Europe’s renovation market as builders target Building Performance Directive thresholds. Commercial buyers, notably hotels and hospitals, are turning to solar thermal to decarbonize Scope-1 heat and secure green-building certifications. Regionally, Asia-Pacific leads on volume, Europe on hybrid innovation, and North America on code-driven multifamily retrofits.

Key Report Takeaways

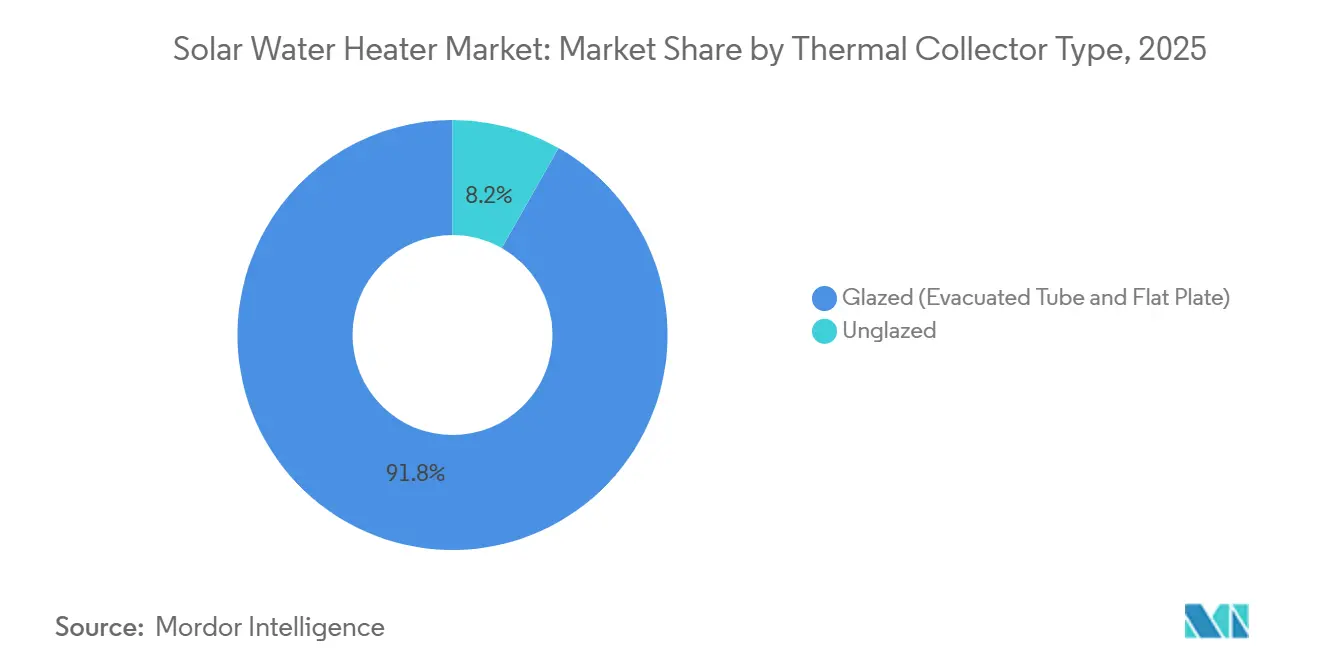

- By thermal collector type, glazed systems captured 91.8% of revenue in 2025 and are forecast to grow at an 8.8% CAGR through 2031.

- By system type, passive thermosiphon units held 62.5% of 2025 installations, while active pumped designs are poised for the fastest 10.2% CAGR to 2031.

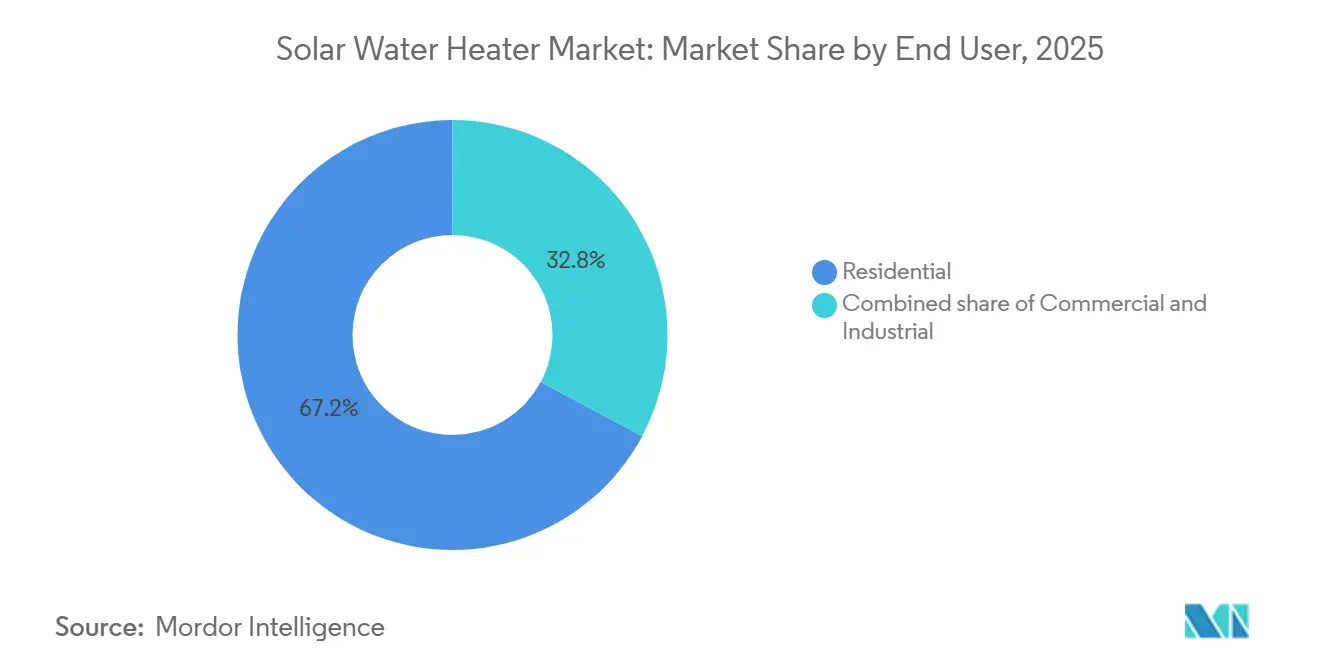

- By end user, residential installations delivered 67.2% of revenue in 2025, whereas commercial deployments are set to advance at 11.0% CAGR through 2031.

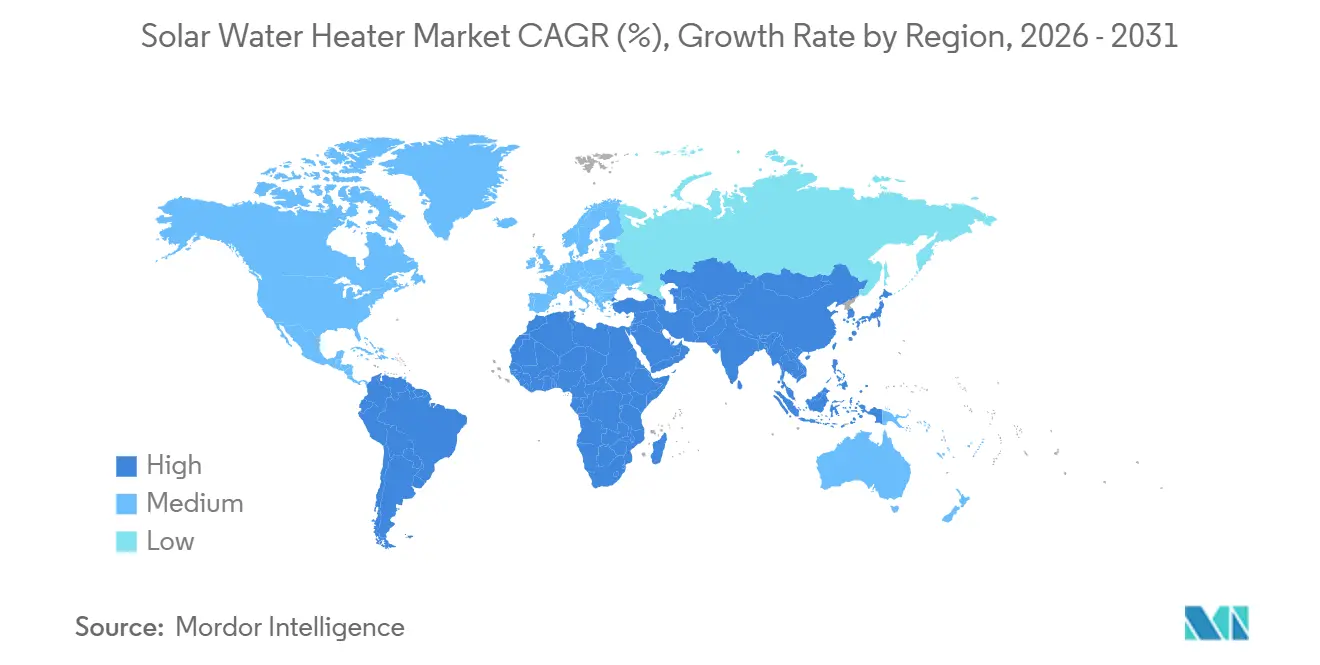

- By geography, Asia-Pacific led with 43.9% of the market in 2025; the region is set to advance at a 9.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Solar Water Heater Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream policy-driven rooftop mandates | +1.8% | China, India, Middle East | Medium term (2-4 years) |

| Declining collector costs in China & India | +1.5% | Global, strongest in Asia-Pacific and South America | Short term (≤ 2 years) |

| Heat-pump/solar hybrid retrofits in Europe | +0.9% | Germany, Spain, Nordic countries | Medium term (2-4 years) |

| Industrial low-temperature process-heat demand | +1.2% | Global, focused on Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Carbon-credit monetization of SWH installations | +0.7% | Europe, North America, select Asia-Pacific markets | Long term (≥ 4 years) |

| Corporate ESG procurement for Scope-1 heat | +0.6% | Global hospitality and healthcare networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mainstream Policy-Driven Rooftop Mandates

China’s Fourteenth Five-Year Plan extended solar-thermal obligations to 87 additional tier-2 and tier-3 municipalities, compelling new residential buildings below 12 stories to pre-install rooftop systems.[1]China National Energy Administration, “Solar Thermal Provisions in the 14th Five-Year Plan,” chinaenergyportal.org India raised capital subsidies to 30% for evacuated-tube units in 2025, aiming for 10 million m² of added collector area by 2027.[2]Ministry of New and Renewable Energy, “Capital Subsidy Scheme for Solar Water Heating,” mnre.gov.in Spain’s revised Building Technical Code now requires solar thermal to provide half of the domestic hot-water demand in all new homes, solidifying hybrid adoption over pure electric heaters. These rules reduce payback periods to fewer than three years in high-insolation zones, yet uneven incentives in several U.S. states still hinder contractor uptake despite federal tax relief.

Declining Collector Costs in China & India

Evacuated-tube prices have fallen 22% since 2023, reaching below USD 45 per square meter in export-grade batches as vertically integrated Chinese plants scale glass-melting and coating lines. India’s Production-Linked Incentive program attracted USD 180 million of fresh factory investment in 2024, trimming delivery lead times for domestic installers. Flat-plate prices track similar cost deflation through aluminum-extrusion automation and polymer glazing, while selective-coating advances narrow the winter efficiency gap between technologies. Affordable hardware is expanding access in Brazil, where residential solar-thermal uptake rose 34% year-on-year in 2025 as unsubsidized systems undercut electric shower-heads over a seven-year lifecycle. Quality variance persists: third-party audits in 2025 found 18% of low-cost evacuated tubes failed ISO 9806 benchmarks, prompting tighter customs inspection in key destinations.

Heat-Pump/Solar Hybrid Retrofits in Europe

Europe’s Building Performance Directive requires all dwellings to reach Energy Performance Certificate C or better by 2030. Hybrid retrofits that pair solar collectors with air-source heat pumps allow German homeowners to cut electricity use by 40% while meeting the rule’s renewable-heat threshold.[3]Bosch Thermotechnology, “Hybrid Solar-Heat-Pump Performance Report 2025,” bosch-thermotechnology.com Norway’s Enova grant now reimburses 35% of hybrid costs, lifting residential solar-thermal uptake 29% in 2025. Dutch hospital pilots showed a 52% reduction in compressor cycling when solar pre-heating was added, extending heat-pump service life and slashing operating expenses. Despite a 20% upfront premium over standalone systems, lower utility bills in high-power-price countries recoup the delta in under four years.

Industrial Low-Temperature Process-Heat Demand

Textile, dairy, and pharmaceutical processors are installing collectors to deliver 60–90 °C water where fossil boilers once dominated. India’s Perform Achieve Trade scheme drove 340,000 m² of collector additions in textiles during 2025. Australian dairies now achieve 55% solar fractions on pasteurization lines by pairing flat plates with heat recovery. A Zhejiang pharmaceutical plant posted a 3.1-year payback and 1,800 tCO₂ annual avoidance from its 2025 evacuated-tube array, even after adding storage tanks, levelized solar industrial heat costs of USD 0.03–0.05 per kWh undercut diesel and grid electricity in off-pipeline regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front capex vs. electric heaters | -0.7% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Competition from heat-pump water heaters | -0.9% | North America, Europe, temperate APAC regions (Japan, South Korea) | Medium term (2-4 years) |

| Supply-chain glass-tube fragility | -0.5% | Global, particularly affecting long-distance exports from China to Latin America and Africa | Short term (≤ 2 years) |

| Policy uncertainty for solar thermal vs. PV | -0.4% | North America, select European markets, emerging APAC economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Capex vs. Electric Heaters

A 300-liter residential solar array costs USD 1,200–1,800 installed versus USD 400–600 for a resistance tank, stretching paybacks to 8–10 years in U.S. states with low-power tariffs.[4]U.S. Department of Energy, “Residential Water Heating Fact Sheet 2026,” energy.gov Only 12% of American installers offered on-bill financing in 2025, hampering uptake relative to photovoltaic loans. European hybrids exceed EUR 5,000, and a 2025 German survey showed 61% of households underestimated lifecycle savings by more than 30%. Leasing models are emerging; Spain’s zero-down subscription launched in 2025, but tax clarity on asset ownership remains unsettled.

Competition From Heat-Pump Water Heaters

Variable-speed heat-pump heaters with COPs above 3.5 won 41% shipment growth in the United States during 2025 on the back of the Inflation Reduction Act incentives covering 30% of the installed cost. Japan’s CO₂-based Eco Cute units held 52% of 2025 sales thanks to compact indoor designs and utility rebates. Heat pumps need no rooftop penetrations, offer plug-and-play smart-home integration, and often carry lower installed costs than solar arrays in temperate zones. Solar vendors counter with hybrid packages and predictive controllers. Viessmann’s 2025 Vitosol line reached 67% renewable-heat fractions in German trials, yet the residential share battle remains intense.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Thermal Collector Type: Efficiency Powers the Glazed Advantage

In 2025, glazed evacuated-tube and flat-plate collectors captured 91.8% of revenue, and the segment is tracking toward an 8.8% CAGR to 2031 as policymakers demand year-round thermal efficiency. Evacuated tubes dominate China and India, where sub-10 °C winters prevail; their vacuum jackets keep annual efficiencies above 60% even with 20 °C ambient deltas. Flat plates find favor in Mediterranean and tropical climates where lower hardware costs and simpler mounts outweigh modest winter losses. The solar water heater market size for glazed collectors is projected to rise alongside selective-coating innovations that push absorptance beyond 0.95, closing the performance gap.

Technological convergence is accelerating: polymer glazing cuts flat-plate weight by 35% and shipping damage by 18% at the expense of shorter UV warranties, while heat-pipe evacuated tubes speed installation by 22%. Compliance with ISO 9806 and Solar Keymark is now mandatory for EU rebates, forcing low-cost exporters to upgrade quality controls. Unglazed polypropylene mats retain a small pool-heating niche but face saturation as cover-sheet solutions deliver passive gains at comparable cost.

By System Type: Active Pumps Edge Into Passive Territory

Passive thermosiphon units delivered 62.5% of 2025 shipments thanks to zero electricity use and mechanical simplicity prized in single-family homes across Asia-Pacific and Latin America. Yet active pumped architectures are forecast to post the fastest 10.2% CAGR through 2031, reflecting commercial retrofits that require basement tanks, precision temperature control, and digital monitoring. In Germany, the solar water heater market share of hybrids that blend active solar and heat pumps jumped to 34,000 units in 2025 after incentives rewarded renewable-heat percentages.

Active systems let engineers place 5,000-liter storage tanks below collectors, critical for multistory hotels and industrial plants lacking rooftop volume, while smart controllers modulate pump speed by isolation and tariff signals. New thermosiphon designs with integrated electric back-up heaters appeared in India during 2025, enhancing monsoon reliability without pumps. The solar water heater market size for active configurations is positioned to benefit from Ecodesign thresholds that indirectly favor advanced controls in the European Union.

By End User: Commercial Demand Accelerates

Residential users produced 67.2% of 2025 revenue as Chinese and Indian housing mandates institutionalized rooftop systems for low-rise buildings. However, hotels, hospitals, and schools are set to log the swiftest 11.0% CAGR to 2031 as owners chase Scope-1 decarbonization and green-building ratings. A European hotel study covering 120 properties documented 38% fossil-gas savings where solar served 50–70% of hot-water load, boosting asset values via BREEAM certifications.

Industrial low-temperature heat remains an untapped frontier: textiles, dairy, and pharmaceuticals together consumed 1.2 million TJ in India alone, yet solar currently supplies under 2%. A Brazilian dairy cooperative installing 1,200 m² of evacuated tubes in 2025 displaced 220,000 m³ of natural gas and generated 1,800 voluntary carbon credits. Space and storage constraints raise project capex by up to 30%, but modular industrial packages launched in 2025 by Bosch cut design-to-commissioning lead times by 55%, widening the addressable buyer pool.

Geography Analysis

Asia-Pacific retained 43.9% of 2025 revenue and is projected to expand at 9.1% CAGR through 2031, supported by China’s 18.5 million m² annual collector additions and India’s 30% capital subsidies for evacuated tubes. Export-grade tube prices below USD 45 per m² allowed Chinese makers to penetrate 87 countries, while India aims for 10 million m² of new capacity by 2027, lifting rural installations by 28% year-on-year in 2025. Japan’s mature but stable base of 47,000 annual installs is increasingly hybridized with CO₂ heat pumps where grid power tops JPY 30 per kWh.

Europe’s momentum stems from retrofit regulations and hybrid innovation. Germany clocked 112,000 installs in 2025 as Building Performance Directive targets pushed 78% of systems into solar-heat-pump combinations. Spain’s 2026 mandate for 50% solar contribution in new homes will add roughly 180,000 annual systems in Mediterranean zones with insolation above 1,800 kWh/m². Denmark’s district-heating hybrid field tied 5,000 m² of flat plates to a 10,000-m³ seasonal store, achieving 35% solar fraction in 2025.

North America, South America, and the Middle East form high-growth niches. California’s Title 24 code drove 18,000 multifamily pre-heat installations in 2025. Mexico’s CONAVI subsidies propelled a 22% residential jump, while Brazil’s hospital projects attained three-year paybacks and LEED Gold status. Saudi Arabia earmarked USD 120 million in 2025 for industrial solar-thermal rollouts under Vision 2030, bringing 70–90 °C process heat to petrochemical parks. South African aggregators monetize residential installations via voluntary carbon credits, keeping unsubsidized paybacks under four years even without grid-feed tariffs.

Competitive Landscape

Competitive Landscape

The top 10 manufacturers captured an estimated 48% of global revenue in 2025, indicating moderate consolidation. Vertically integrated Chinese leaders, including Himin Solar, Jiangsu Sunpower, and Zhejiang JiaDeLe, reduce end-to-end costs by 25–30% through captive borosilicate glass lines and automated coating plants, enabling aggressive entry into Latin America and Africa. Western incumbents, including Rheem, A.O. Smith, Bosch Thermotechnology, and Viessmann, are pivoting to premium hybrids, bundling AI-driven controllers, extended warranties, and remote diagnostics for commercial clients willing to pay 20–30% price premiums.

Innovation centers on shipping resilience and digital optimization. Bosch filed 14 polymer-composite tube patents in 2025 that cut freight breakage by 18% yet pass ISO 9806 tests, while Viessmann’s predictive algorithms time-shift solar, heat-pump, and resistance inputs to shave electricity peaks by 30% in field trials. India’s Production-Linked Incentive outlay of USD 180 million in 2024 seeded domestic capacity for V-Guard and Racold, shrinking import lead times, and diversifying global supply.

White-space opportunities persist in Europe’s hybrid retrofits and industrial low-temperature heat. Only 15% of European residential installs featured a heat-pump interface in 2025 despite lifecycle savings above 25% in high-power-price zones. Solar currently meets under 2% of global low-temperature process heat, even though levelized costs beat electric boilers by roughly 40% in 2025. Carbon-credit aggregators add a new competitive layer, with a South African firm monetizing 22,000 credits from 14,500 systems in 2025 at USD 12–18 tCO₂.

Solar Water Heater Industry Leaders

Himin Solar Energy Group

Ariston Thermo SpA (incl. Racold & Chromagen)

Rheem Manufacturing Co.

A. O. Smith Corp.

Bosch Thermotechnology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Oekoboiler Swiss AG, a Swiss manufacturer of energy-efficient hot water solutions, is pushing the boundaries of sustainable building technology. Their integrated heat pump and solar systems cater to both residential and commercial properties across Switzerland.

- January 2026: CyboEnergy announced advancements in the development and commercialization of its CyboInverter H solar PV water-heating solution. This technology allows standard electric water heaters to operate directly using solar power. The initiative aims to reduce energy costs, enhance grid independence, and promote the adoption of renewable water-heating technologies.

- October 2025: Enphase Energy, Inc. has expanded its IQ Energy Management capabilities to encompass select electric water heaters in Belgium, the Netherlands, and Switzerland. This update, driven by the Enphase IQ Energy Router, empowers homeowners to have greater control over their energy usage – spanning solar, batteries, electric vehicle (EV) chargers, heat pumps, and now, electric water heaters – all within a unified system.

- May 2025: Lennox and Ariston Group have teamed up in a joint venture, aiming to deliver a competitive range of residential water heaters to homeowners across the United States and Canada.

Global Solar Water Heater Market Report Scope

A Solar Water Heater generates hot water using solar heat energy. A solar collector attached to a water storage tank and positioned on the top of a building makes up a standard solar water heater. Solar water heaters are a significant step toward living more sustainably.

The Solar Water Heater Market is segmented by thermal collector type, system type, end-user, and geography. By thermal collector type, the market is segmented into glazed (evacuated tube and flat plate) and unglazed. By system type, the market is segmented into active/pumped and passive/thermosiphon. The end-user includes residential and commercial, and industrial. The report also covers the market size and forecasts for the solar water heater market across the major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Glazed (Evacuated Tube, and Flat Plate) |

| Unglazed |

| Active (Pumped) |

| Passive (Thermosiphon) |

| Residential |

| Commercial |

| Industrial |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Thermal Collector Type | Glazed (Evacuated Tube, and Flat Plate) | |

| Unglazed | ||

| By System Type | Active (Pumped) | |

| Passive (Thermosiphon) | ||

| By End User | Residential | |

| Commercial | ||

| Industrial | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast growth rate for global solar water heating between 2026 and 2031?

The segment is projected to register an 8.32% CAGR, taking revenue from USD 4.98 billion in 2026 to USD 7.43 billion by 2031.

Which collector type will lead installations through 2031?

Glazed collectors - evacuated tubes and flat plates - are set to maintain dominance, holding over 90% of revenue and growing at 8.8% CAGR.

Why are active pumped systems gaining popularity?

They accommodate basement tank placement, enable precision controls, and integrate seamlessly with heat-pump hybrids, making them attractive for multistory commercial projects.

Which region currently buys the most solar water heaters?

Asia-Pacific commanded 43.9% of global revenue in 2025, driven by China's municipal mandates and India's subsidy extensions.

How are solar water heaters financed in cost-sensitive markets?

Tools range from capital subsidies and tax credits to emerging carbon-credit monetization and zero-down leasing models, which collectively cut typical paybacks below four years in high-insolation zones.

What threat do heat-pump water heaters pose?

In temperate regions with inconsistent sun, variable-speed heat pumps offer lower upfront costs and ease of installation, taking share unless solar vendors bundle hybrid or smart-switching solutions.

Page last updated on: