| Study Period | 2019 - 2030 |

| Market Volume (2025) | 2.16 Terawatt |

| Market Volume (2030) | 6.03 Terawatt |

| CAGR | 22.01 % |

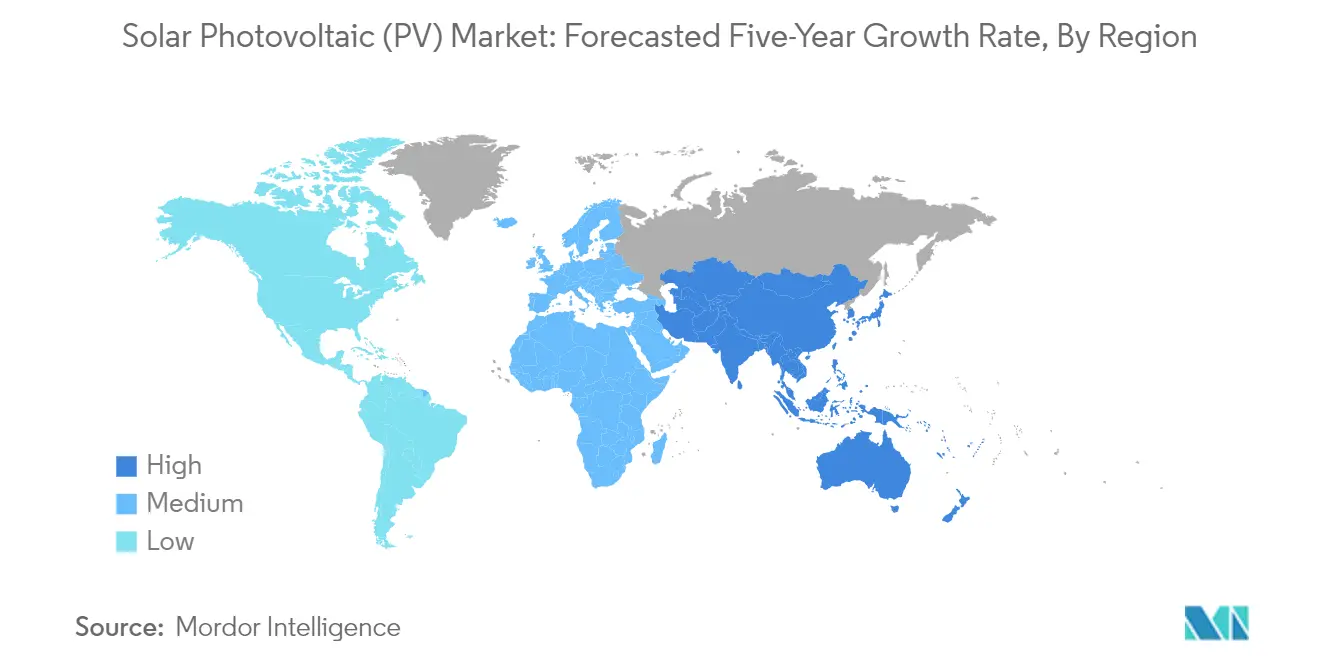

| Fastest Growing Market | Middle-East and Africa |

| Largest Market | Asia Pacific |

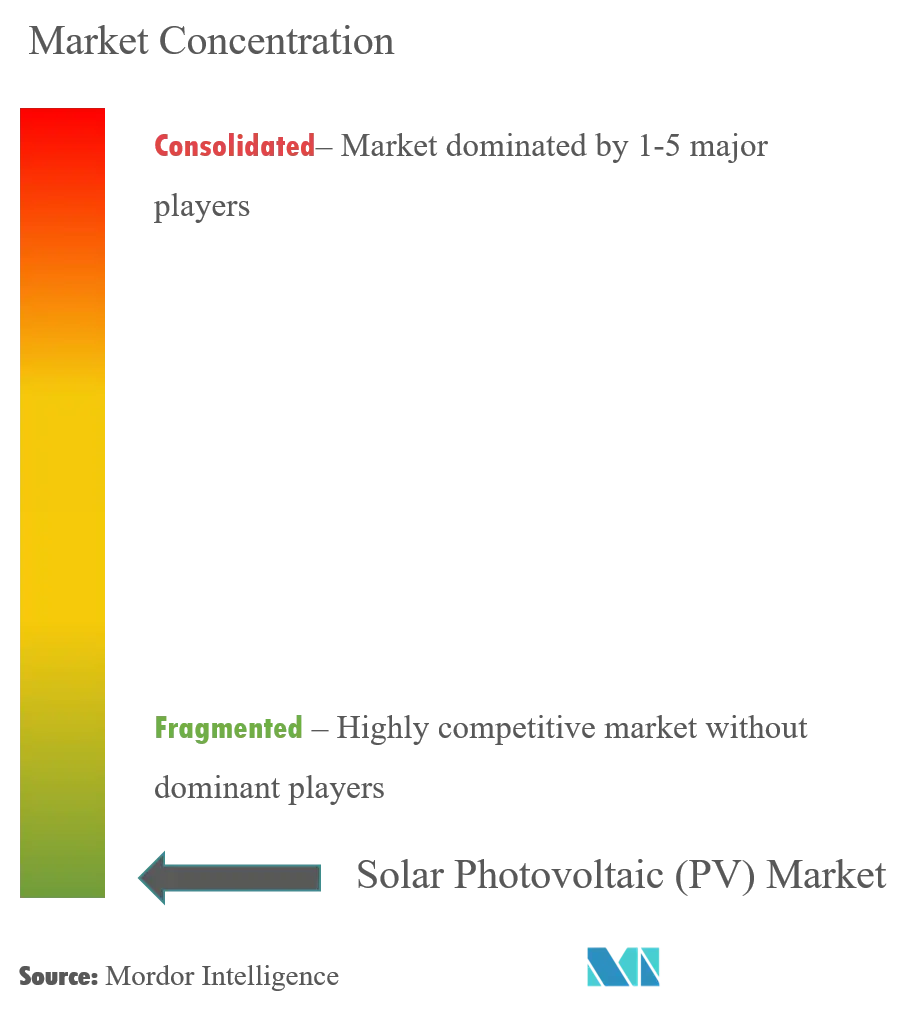

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Market Size")

Solar Photovoltaic Market Analysis

The Solar Photovoltaic Market size is estimated at 2.16 Terawatt in 2025, and is expected to reach 6.03 Terawatt by 2030, at a CAGR of 22.01% during the forecast period (2025-2030).

The global solar photovoltaic industry has witnessed remarkable technological advancements and efficiency improvements, transforming the renewable energy landscape. Solar PV generation demonstrated substantial growth, increasing by 270 TWh (up 26%) in 2022 to reach almost 1300 TWh, highlighting the technology's increasing adoption and effectiveness. The continuous evolution of solar cell technology has led to higher conversion efficiencies and improved performance under various environmental conditions. Manufacturing processes have become more sophisticated, resulting in better quality control and reduced production costs, while innovations in module design have enhanced durability and lifetime performance.

The industry has experienced significant shifts in solar manufacturing capabilities and supply chain dynamics, particularly in key markets. China continues to dominate the solar manufacturing landscape, with solar panel installations rising by 59% to 87.4 GW in 2022, demonstrating the country's manufacturing prowess and market leadership. The emergence of new manufacturing hubs in various regions has begun to diversify the global supply chain, reducing dependency on single-source markets. This transformation has been accompanied by substantial investments in research and development, leading to breakthrough technologies in cell architecture and module design.

Technological innovation in the solar PV industry has reached new heights, with mono-crystalline silicon technology gaining unprecedented market share. According to the National Renewable Energy Laboratory (NREL), in 2022, 96% of total solar module shipments were of mono-Si technology, compared to 35% in 2015, indicating a clear industry preference for higher efficiency solutions. The industry has also witnessed remarkable progress in bifacial technology, tracking systems, and smart monitoring solutions, enhancing overall system performance and reliability while reducing maintenance requirements.

Corporate investments and utility-scale projects have reached unprecedented levels, with several landmark developments in 2023. Notable projects include Total Energies' commencement of commercial operations of the 380 MW Myrtle Solar facility in Houston, featuring approximately 705,000 ground-mounted photovoltaic panels. Additionally, Ørsted's announcement of the One Earth Solar Farm project with a capacity of 740 MW demonstrates the increasing scale of solar installations. The industry has also seen innovative partnerships, such as BELECTRIC Solar Ltd UK and NextEnergy Solar Fund's framework agreement for more than 150 MWp in O&M, highlighting the growing emphasis on operational efficiency and long-term asset management.

Solar Photovoltaic Market Trends

Favorable Government Policies and Increasing Adoption of Solar PV Systems

The solar photovoltaic market has witnessed substantial growth driven by increasingly supportive government policies and regulations worldwide. In 2023, governments have introduced more aggressive renewable energy targets and financial incentives to accelerate solar PV adoption. For instance, in August 2022, the US government signed the landmark Inflation Reduction Act, allocating nearly USD 400 billion in direct funding and tax credits for clean energy development, which has had a profound impact on America's path to net-zero emissions. Similarly, the UK government has set ambitious targets to raise the country's solar capacity to 70 gigawatts by 2035, demonstrating the global push towards solar energy adoption through policy frameworks.

The effectiveness of government support is evident in the remarkable growth of solar PV generation, which increased by 270 TWh (up 26%) in 2022, reaching almost 1300 TWh globally. This growth has been further catalyzed by continuous improvements in the economic attractiveness of solar PV, massive development in the supply chain, and increasing policy support, especially in major economies. For example, in September 2022, India allocated a total capacity of 39.6 GW of domestic solar PV module manufacturing capacity to 11 companies, with a total outlay of INR 14,007 crore under the Production Linked Incentive Scheme. Such initiatives have created a favorable environment for both manufacturers and consumers, driving increased adoption across residential, commercial, and utility sectors.

Understand The Key Trends Shaping This Market

Download PDF

Soaring Electricity Prices Incentivized Installing Solar PV Systems for Self-Consumption

The dramatic surge in global electricity prices has emerged as a powerful catalyst for solar PV adoption, particularly in the residential and commercial sectors. In 2022, electricity prices witnessed unprecedented increases, with the United States recording a 10.7% rise in residential electricity prices, creating a compelling economic case for solar installation. This trend has been particularly significant as businesses and households seek to mitigate the impact of rising energy costs through self-generation capabilities. The installation costs for solar PV systems have simultaneously decreased, with residential solar installation prices in British households declining by 13% in the six months leading to March 2023, making the technology increasingly accessible to a broader range of consumers.

The economic benefits of solar self-consumption have been further enhanced by innovative policies and market structures. For instance, in Germany, the government reduced the surcharge on solar energy electricity bills by 43% in 2021, and further decreased it to 3.7 cents from 6.5 cents in 2022, making solar power more economically attractive for end-users. The cost-effectiveness of solar PV systems has improved significantly, with the cost of producing one kilowatt-hour using solar panels reaching as low as 3.7 cents in some regions. This economic advantage, coupled with the ability to reduce dependency on grid electricity, has led to a notable increase in solar PV installations, particularly in the residential sector, where the United States alone witnessed a 23% year-over-year growth in 2022, reaching 5.08 GW of installed capacity.

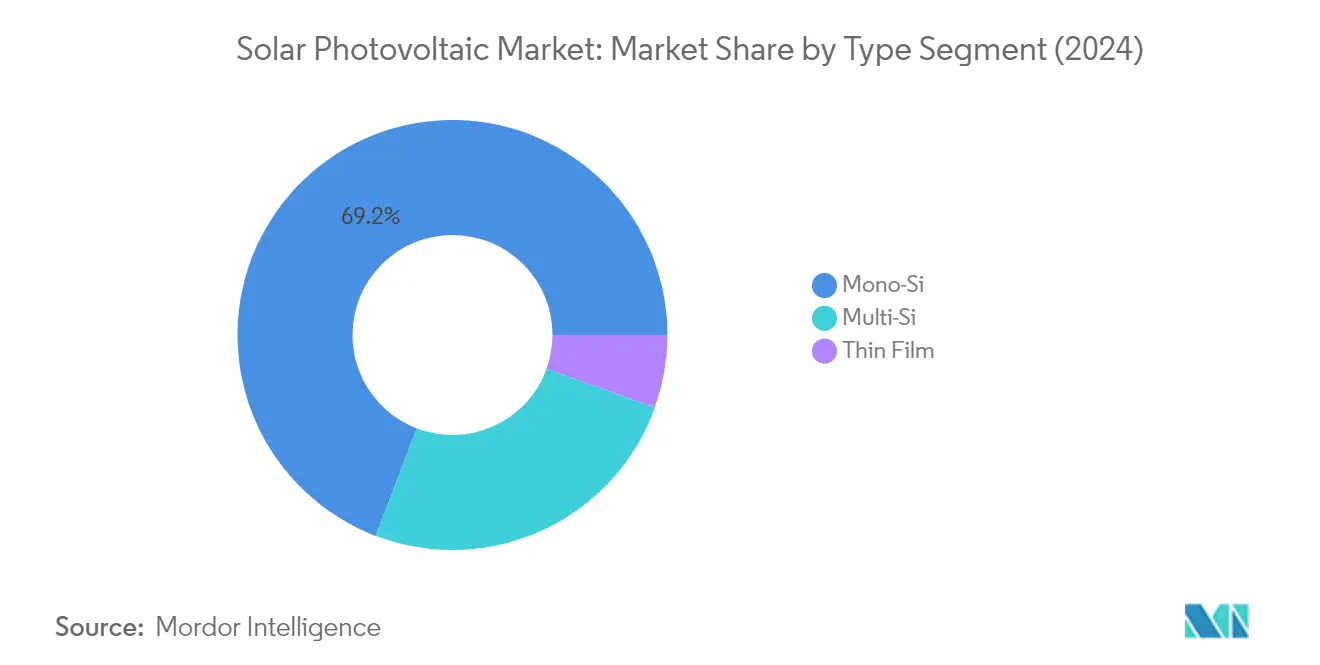

Segment Analysis: By Type

Mono-Si Segment in Solar Photovoltaic (PV) Market

The mono-crystalline silicon (Mono-Si) segment dominates the global solar photovoltaic market, commanding approximately 69% market share in 2024. This dominance can be attributed to the superior efficiency and performance characteristics of mono-crystalline technology. Mono-Si panels are characterized by their high power output rating and superior efficiency levels reaching up to 23%. The segment's growth is driven by continuous technological advancements, improving manufacturing processes, and increasing demand from utility-scale solar power generation projects. Major manufacturers are focusing on expanding their Mono-Si production capacities and developing more efficient products to meet the growing demand. The segment particularly benefits from its suitability for space-constrained installations, making it popular in both residential and commercial applications where maximum power output per unit area is crucial.

Thin Film Segment in Solar Photovoltaic (PV) Market

The thin film segment is emerging as the fastest-growing segment in the solar PV market, with projections indicating robust growth between 2024 and 2029. This growth is primarily driven by technological advancements that have improved the efficiency and reduced production costs of thin-film modules. The segment is witnessing increased adoption due to its versatility in various applications, particularly in building-integrated photovoltaics (BIPV) and large-scale utility projects. Thin-film technology offers several advantages, including better performance in high-temperature conditions and low-light situations, making it particularly attractive for regions with varying weather conditions. Manufacturers are investing heavily in research and development to further enhance the efficiency and reduce the production costs of thin-film modules, which is expected to drive continued growth in this segment.

Remaining Segments in Solar PV Market by Type

The multi-crystalline silicon (Multi-Si) segment continues to play a significant role in the solar PV market, offering a balance between cost and performance. Multi-Si technology remains popular in price-sensitive markets and large-scale utility projects where cost per watt is a crucial factor. The segment benefits from established manufacturing processes and a mature supply chain, making it an attractive option for many solar installations. While facing competition from Mono-Si technology in terms of efficiency, Multi-Si modules continue to find applications in various projects where their cost-effectiveness outweighs the slight efficiency disadvantage. The segment maintains its relevance through continuous improvements in manufacturing processes and cell efficiency, though at a more modest pace compared to other technologies.

Segment Analysis: End-User

Utility Segment in Solar Photovoltaic (PV) Market

The utility segment continues to dominate the global solar photovoltaic market, commanding approximately 61% of the total market share in 2024. This significant market position is primarily driven by the increasing development of large-scale solar farms and utility-scale projects worldwide. The segment's dominance is further strengthened by declining technology costs, improved grid integration capabilities, and supportive government policies promoting utility-scale solar installations. Major utility-scale projects are being developed across key regions including China, India, the United States, and Europe, with many countries focusing on expanding their utility-scale solar capacity to meet renewable energy targets. The segment's growth is also supported by the increasing adoption of power purchase agreements (PPAs) and innovative financing models that make large-scale solar projects more economically viable.

Residential Segment in Solar Photovoltaic (PV) Market

The residential solar segment is emerging as the fastest-growing sector in the solar PV market, with projections indicating robust growth between 2024 and 2029. This exceptional growth is driven by increasing consumer awareness of renewable energy benefits, declining installation costs, and improved energy storage solutions for residential applications. Government incentives and subsidies specifically targeting residential solar installations have played a crucial role in accelerating adoption rates. The segment's growth is further supported by innovative financing options, including solar leasing and power purchase agreements, making solar installations more accessible to homeowners. Additionally, the integration of smart home technologies and the rising trend of energy independence among residential consumers are contributing to the segment's rapid expansion. The increasing focus on sustainable living and rising electricity costs in many regions are also key factors driving residential solar PV adoption.

Remaining Segments in End-User Segmentation

The commercial solar segment represents a significant portion of the solar PV market, serving as a crucial bridge between utility-scale and residential installations. This segment encompasses a diverse range of applications including solar installations on commercial buildings, industrial facilities, schools, hospitals, and government buildings. The commercial sector's growth is driven by businesses seeking to reduce operational costs, meet sustainability goals, and comply with corporate environmental responsibilities. The segment benefits from the availability of roof space on commercial buildings, making it ideal for solar PV installations. Additionally, the commercial segment often serves as a testing ground for new solar technologies and innovative business models before they are scaled to utility-level or adapted for residential use.

Segment Analysis: By Deployment

Ground-mounted Segment in Solar Photovoltaic Market

Ground-mounted solar PV installations continue to dominate the global solar photovoltaic market, accounting for approximately 57% of the total installed capacity in 2024. This dominance is primarily driven by utility-scale projects that benefit from economies of scale, lower installation costs, and higher operational efficiencies. The segment's growth is particularly strong in emerging economies such as China, India, and Brazil, where large tracts of land are available for solar farm development. Ground-mounted installations are preferred for utility-scale projects due to their ability to optimize panel orientation and tracking systems, resulting in higher energy yields. The segment has also benefited from technological advancements in mounting structures, improved land utilization techniques, and innovative bifacial module technologies that enhance overall system performance. Additionally, the increasing adoption of advanced tracking systems and smart monitoring solutions has further boosted the efficiency and reliability of ground-mounted installations.

Rooftop Solar Segment in Solar Photovoltaic Market

The rooftop solar segment is experiencing remarkable growth and is projected to expand at approximately 24% annually from 2024 to 2029. This accelerated growth is driven by several factors, including favorable government policies, declining installation costs, and increasing awareness of sustainable energy solutions among residential and commercial consumers. The segment is witnessing significant technological innovations, particularly in terms of lightweight panels, improved mounting systems, and integrated solar tiles that enhance aesthetic appeal while maintaining high performance. The commercial and industrial sectors are increasingly adopting rooftop solar solutions to reduce operational costs and meet corporate sustainability goals. Furthermore, the development of smart energy management systems, coupled with energy storage solutions, has made rooftop solar installations more attractive to property owners. The segment is also benefiting from streamlined installation processes, improved financing options, and enhanced grid integration capabilities that make rooftop solar more accessible to a broader range of consumers.

Solar Photovoltaic (PV) Market Geography Segment Analysis

Solar Photovoltaic Market in North America

The North American solar photovoltaic market demonstrates robust growth driven by supportive government policies, technological advancements, and increasing adoption across residential, commercial, and utility sectors. The United States leads the regional market with significant installations across multiple states, particularly in California, Texas, and Florida. Canada follows with its own ambitious renewable energy targets and implementation of various incentive programs. The region benefits from well-developed infrastructure, strong research and development capabilities, and increasing corporate commitments to renewable energy adoption.

Solar Photovoltaic Market in United States

The United States dominates the North American solar photovoltaic market landscape through comprehensive federal and state-level support mechanisms, including tax incentives and renewable portfolio standards. The country has witnessed substantial growth in utility-scale installations while maintaining steady expansion in residential and commercial segments. With approximately 91% photovoltaic market share in North America as of 2024, the U.S. market is characterized by diverse applications ranging from large solar farms to residential rooftop installations. The country's solar industry benefits from declining technology costs, improving efficiency rates, and increasing grid integration capabilities.

Solar Photovoltaic Market Growth Trajectory in United States

The United States continues to demonstrate strong growth potential in the solar photovoltaic sector, with an expected growth rate of approximately 17% during 2024-2029. The growth is supported by the Inflation Reduction Act, which provides significant incentives for solar installations across all segments. The country's commitment to clean energy transition is evident through numerous utility-scale projects under development, expanding manufacturing capabilities, and innovative financing mechanisms. Technological advancements in energy storage integration and smart grid solutions further enhance the market's growth prospects.

Solar Photovoltaic Market in Asia-Pacific

The Asia-Pacific region represents the largest and most dynamic solar photovoltaic market globally, characterized by rapid technological advancement and significant manufacturing capabilities. China leads the regional market with extensive manufacturing infrastructure and ambitious installation targets, followed by Japan's mature market and India's rapidly expanding solar sector. The region benefits from strong government support, decreasing technology costs, and increasing energy demands that drive both utility-scale and distributed solar installations.

Solar Photovoltaic Market in China

China maintains its position as the dominant force in the Asia-Pacific solar photovoltaic market through comprehensive policy support and extensive manufacturing capabilities. With approximately 58% photovoltaic market share in the Asia-Pacific region as of 2024, China's market is characterized by large-scale utility projects and growing distributed generation segments. The country's solar industry benefits from integrated supply chains, technological innovation, and strong domestic demand for renewable energy solutions.

Solar Photovoltaic Market Growth Trajectory in India

India emerges as the fastest-growing market in the Asia-Pacific region, with an expected growth rate of approximately 29% during 2024-2029. The country's solar sector is driven by ambitious renewable energy targets, supportive government policies including the Production Linked Incentive scheme, and increasing private sector participation. India's solar market benefits from abundant solar resources, decreasing technology costs, and growing emphasis on domestic manufacturing capabilities.

Solar Photovoltaic Market in Europe

The European solar photovoltaic market demonstrates a strong commitment to renewable energy transition through comprehensive policy frameworks and technological innovation. Germany leads the regional market with significant installations and mature market infrastructure, while countries like France, Italy, and the United Kingdom contribute to the region's diverse solar landscape. The market benefits from strong environmental policies, technological advancement, and increasing focus on energy independence.

Solar Photovoltaic Market in Germany

Germany maintains its leadership position in the European solar photovoltaic market through well-established support mechanisms and strong technical expertise. The country's market is characterized by balanced growth across residential, commercial, and utility segments, supported by comprehensive feed-in tariff programs and increasing focus on energy storage integration.

Solar Photovoltaic Market Growth Trajectory in Germany

Germany continues to demonstrate strong growth potential in the solar photovoltaic sector, driven by ambitious renewable energy targets and supportive regulatory frameworks. The country's commitment to energy transition is evident through continuous technological innovation, growing energy storage integration, and increasing focus on sector coupling between electricity, heating, and transport sectors.

Solar Photovoltaic Market in South America

The South American solar photovoltaic market shows increasing momentum driven by abundant solar resources and growing energy demands. Brazil emerges as both the largest and fastest-growing market in the region, followed by Argentina's developing solar sector. The region demonstrates significant potential through expanding utility-scale projects, increasing distributed generation, and supportive regulatory frameworks that encourage solar adoption across various segments.

Solar Photovoltaic Market in Middle East & Africa

The Middle East & Africa region presents significant growth opportunities in the solar photovoltaic market, driven by excellent solar resources and increasing focus on energy diversification. Saudi Arabia emerges as the fastest-growing market while the United Arab Emirates represents the largest market in the region. The region benefits from decreasing technology costs, ambitious renewable energy targets, and increasing investments in utility-scale solar projects.

Get Analysis on Important Geographic Markets

Download PDF

Solar Photovoltaic Industry Overview

Top Companies in Solar Photovoltaic (PV) Market

The global solar PV market is characterized by intense innovation and strategic expansion initiatives from leading players, including First Solar, JinkoSolar, Canadian Solar, LONGi Green Energy, and SunPower Corporation. Companies are heavily investing in research and development to improve solar cell efficiency and develop next-generation technologies like high-efficiency tandem devices and perovskite cells. Operational agility is demonstrated through vertical integration strategies and the establishment of manufacturing facilities across multiple geographies to ensure supply chain resilience. Strategic moves include significant capacity expansions, particularly in emerging markets, alongside investments in advanced solar manufacturing capabilities for newer technologies like N-type modules and TOPCon cells. Market leaders are also focusing on developing comprehensive solution offerings that combine solar modules with energy storage and smart monitoring systems to provide integrated energy solutions.

Market Dominated by Global Manufacturing Giants

The photovoltaic industry exhibits a moderately consolidated structure dominated by large-scale manufacturers with significant production capabilities, particularly from China and other Asian countries. These major players leverage their economies of scale, established distribution networks, and technological expertise to maintain their market positions, while regional specialists focus on specific market segments or geographical areas. The industry has witnessed substantial vertical integration, with many leading companies expanding across the value chain from wafer production to module manufacturing and project development.

The market has experienced considerable consolidation through strategic mergers and acquisitions, particularly focused on expanding geographical presence and acquiring technological capabilities. Companies are actively pursuing partnerships and collaborations to strengthen their market position, with a notable trend of established players acquiring innovative technology startups to enhance their product portfolios. Joint ventures and strategic agreements, especially in emerging markets, have become common as companies seek to navigate local regulations and establish a manufacturing presence in key growth regions.

Innovation and Efficiency Drive Market Success

Success in the solar PV market increasingly depends on companies' ability to balance technological innovation with cost optimization. Incumbent players must focus on continuous improvement in module efficiency, manufacturing processes, and supply chain optimization to maintain their competitive edge. Investment in research and development, particularly in emerging technologies like bifacial modules and advanced cell architectures, remains crucial. Companies also need to develop strong project development capabilities and establish robust distribution networks to effectively serve diverse market segments.

Market contenders can gain ground by focusing on specialized market segments, developing innovative financing solutions, and establishing strong local partnerships. The industry's future success factors include the ability to navigate evolving regulatory landscapes, particularly regarding local content requirements and environmental standards. Companies must also address the growing end-user demand for integrated energy solutions and enhanced product warranties. The risk of substitution remains relatively low due to solar PV's established position in the renewable energy mix, but companies must continue to improve cost competitiveness and efficiency to maintain their market position against other renewable technologies.

Solar Photovoltaic Market Leaders

-

SunPower Corporation

-

JinkoSolar Holding Co. Ltd

-

Canadian Solar Inc.

-

Trina Solar Ltd

-

JA Solar Holdings Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Solar Photovoltaic Market News

- May 2023: State-owned SJVN Ltd. bagged a 100 MW solar power project worth USD 73.24 Million from Rajasthan Urja Vikas Nigam Ltd. SJVN Green Energy Ltd (SGEL), a wholly-owned subsidiary of SJVN, participated in an open competitive tariff bidding process followed by e-Reverse Auction (e-RA) organized by Rajasthan Urja Vikas Nigam Ltd (RUVNL).

- November 2022: European Energy, a Danish-based developer of solar parks, was set to build a 128.5 MW solar park near Helsingborg in southern Sweden. The plant is expected to produce 175 GWh of electricity annually. Production is scheduled to begin in 2024 after the completion of the project by 2023.

Solar Photovoltaic (PV) Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Solar Photovoltaic (PV) Installed Capacity and Forecast, till 2030

- 4.3 Annual Solar PV Shipments in GW, till 2024

- 4.4 Share of Solar PV Shipments (%), by Technology, 2024

- 4.5 Average Selling Price of Solar PV Modules in USD/W, till 2024

- 4.6 Utility-Scale Solar PV Installation Cost in USD/kW, by Major Countries, 2024

- 4.7 Solar PV Average Electricity Cost, by Major Countries, 2024

- 4.8 Information on Key Projects

- 4.9 Recent Trends and Developments

- 4.10 Government Policies and Regulations

-

4.11 Market Dynamics

- 4.11.1 Drivers

- 4.11.1.1 Favorable Government Policies and Increasing Adoption of Solar PV Systems

- 4.11.1.2 Soaring Electricity Prices Incentivized Installing Solar PV Systems for Self-Consumption

- 4.11.2 Restraints

- 4.11.2.1 The Growth of Other Renewable Technologies Such as Wind and Bioenergy

- 4.12 Supply Chain Analysis

-

4.13 Porter's Five Forces Analysis

- 4.13.1 Bargaining Power of Suppliers

- 4.13.2 Bargaining Power of Consumers

- 4.13.3 Threat of New Entrants

- 4.13.4 Threat of Substitute Products and Services

- 4.13.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Type

- 5.1.1 Thin film

- 5.1.2 Multi-Si

- 5.1.3 Mono-Si

-

5.2 End-User

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Utility

-

5.3 Deployment

- 5.3.1 Ground-mounted

- 5.3.2 Rooftop Solar

-

5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Asia-Pacific

- 5.4.2.1 China

- 5.4.2.2 India

- 5.4.2.3 Japan

- 5.4.2.4 Rest of Asia-Pacific

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East & Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted and SWOT Analysis by Leading Players

-

6.3 Company Profiles

- 6.3.1 First Solar Inc.

- 6.3.2 Sharp Corporation

- 6.3.3 Suntech Power Holding Co. Ltd.

- 6.3.4 JinkoSolar Holding Co. Ltd.

- 6.3.5 JA Solar Holdings Co. Ltd.

- 6.3.6 Trina Solar Ltd.

- 6.3.7 Hanwha Q Cells Co. Ltd.

- 6.3.8 Acciona SA

- 6.3.9 Canadian Solar Inc.

- 6.3.10 SunPower Corporation

- 6.3.11 LONGi Green Energy Technology Co. Ltd.

- *List Not Exhaustive

- 6.4 List of Other Prominent Players

- 6.5 Market Ranking/Share Analysis

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Efforts by Several Governments Across the Emerging Nations in the Regions Like Africa and Southeast Asia to Provide 100% Electricity Access

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Solar Photovoltaic Industry Segmentation

Photovoltaic solar energy is a clean, renewable energy source that uses solar radiation to produce electricity. It is based on the so-called photoelectric effect, by which certain materials can absorb photons (light particles) and release electrons, generating an electric current.

The Solar Photovoltaic (PV) Market is segmented by product type, end-user, deployment and geography. By product, the market is segmented by thin film, multi-si, and mono-si. By end-user, the market is segmented by residential, commercial, and utility. By deployment, the market is segmented into ground-mounted and rooftop solar. The report also covers the market size and forecasts for the solar photovoltaic (PV) market across major regions. The market sizing and forecasts for each segment have been done based on installed capacity.

| Type | Thin film | ||

| Multi-Si | |||

| Mono-Si | |||

| End-User | Residential | ||

| Commercial | |||

| Utility | |||

| Deployment | Ground-mounted | ||

| Rooftop Solar | |||

| Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Rest of Asia-Pacific | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| South Africa | |||

| Rest of Middle East & Africa | |||

Need A Different Region or Segment?

Customize Now

Solar Photovoltaic (PV) Market Research Faqs

How big is the Solar Photovoltaic (PV) Market?

The Solar Photovoltaic (PV) Market size is expected to reach 2.16 terawatt in 2025 and grow at a CAGR of 22.01% to reach 6.03 terawatt by 2030.

What is the current Solar Photovoltaic (PV) Market size?

In 2025, the Solar Photovoltaic (PV) Market size is expected to reach 2.16 terawatt.

Which is the fastest growing region in Solar Photovoltaic (PV) Market?

Middle-East and Africa is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Solar Photovoltaic (PV) Market?

In 2025, the Asia Pacific accounts for the largest market share in Solar Photovoltaic (PV) Market.

What years does this Solar Photovoltaic (PV) Market cover, and what was the market size in 2024?

In 2024, the Solar Photovoltaic (PV) Market size was estimated at 1.68 Terawatt. The report covers the Solar Photovoltaic (PV) Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Solar Photovoltaic (PV) Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Solar Photovoltaic (PV) Industry Report

Mordor Intelligence provides a comprehensive analysis of the solar photovoltaic and renewable energy industries. We leverage decades of expertise in clean energy market research. Our detailed report covers the entire PV industry. This includes solar power generation, solar manufacturing, and key technologies such as solar cells, solar modules, and solar inverters. The analysis encompasses both residential solar and commercial solar segments. We pay particular attention to rooftop solar applications and utility-scale solar farms.

Stakeholders benefit from our thorough examination of photovoltaic price trends and PV industry growth projections. These are available in an easy-to-download report PDF format. The report provides valuable solar PV industry insights. It covers solar technology advancements, solar equipment developments, and solar installation trends. Our analysis includes detailed PV market forecasts, solar power market size assessments, and comprehensive solar energy industry trends. This enables businesses to make informed decisions in the rapidly evolving solar power industry.