Solar Photovoltaic Glass Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

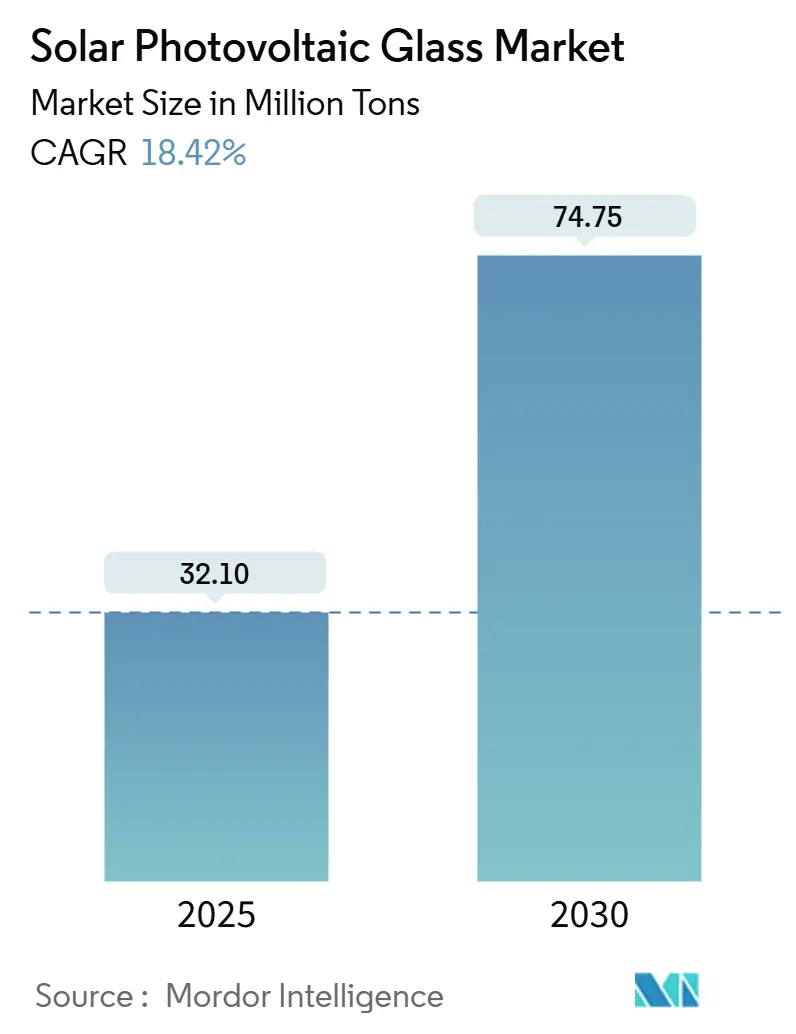

| Market Volume (2025) | 32.10 Million tons |

| Market Volume (2030) | 74.75 Million tons |

| Growth Rate (2025 - 2030) | 18.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solar Photovoltaic Glass Market Analysis by Mordor Intelligence

The solar photovoltaic glass market size reached 32.10 million tons in 2025 and is forecast to reach 74.75 million tons by 2030, advancing at an 18.42% CAGR between 2025 and 2030. This sustained expansion reflects policy-driven installation targets, rapid cost deflation across the module supply chain, and aggressive capacity additions in ultra-low-iron float lines. Transparent conductive oxide (TCO) glass is scaling quickly as next-generation cell architectures demand both high light transmission and surface conductivity. Meanwhile, Asia-Pacific maintains manufacturing leadership, accounting for 62% of global output, yet new capacity in the Middle East and North Africa (MENA) is broadening geographic diversity. Competitive strategies range from Chinese producers expanding commodity capacity to Western incumbents investing in circularity, low-carbon furnaces, and specialty coatings. These shifts together position the solar photovoltaic glass market for resilient growth throughout the decade.

Key Report Takeaways

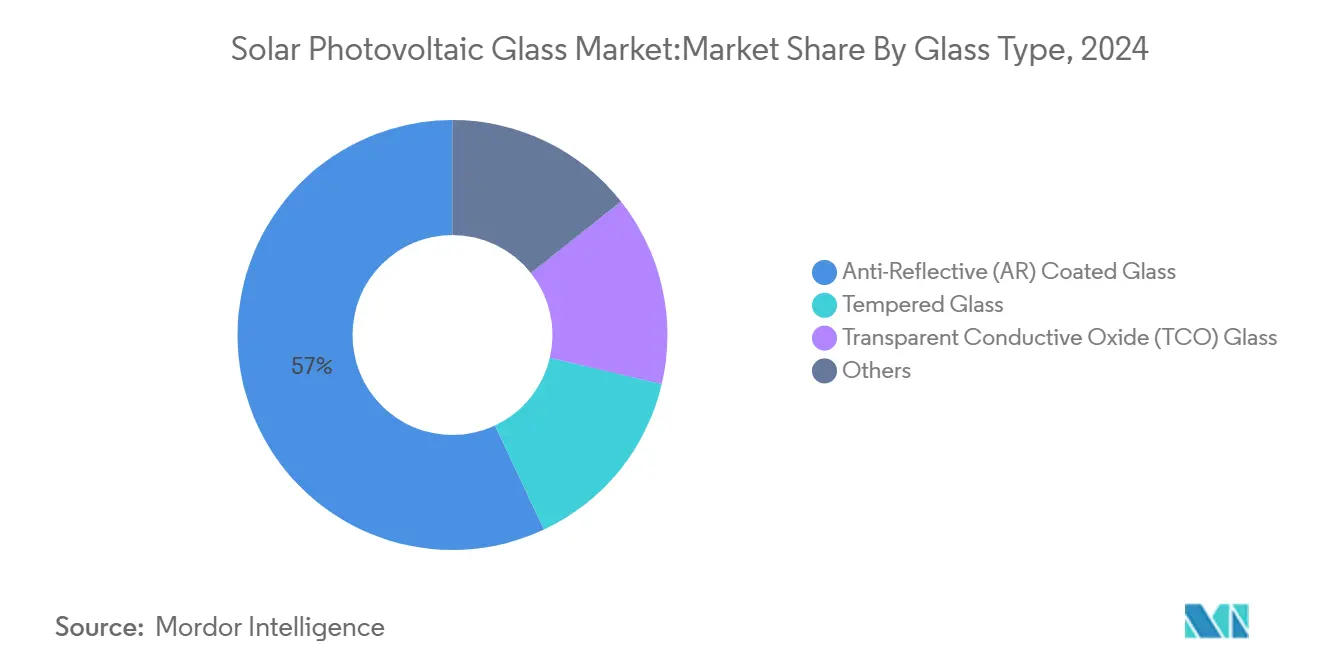

- By glass type, anti-reflective coatings led with a 57% solar photovoltaic glass market share in 2024, while TCO glass is projected to expand at 22.46% CAGR through 2030.

- By manufacturing process, float lines delivered 68% of 2024 volume; rolled glass is forecast to post a 19.70% CAGR to 2030.

- By solar technology, crystalline silicon held 91% share of the solar photovoltaic glass market size in 2024, whereas CIGS cells are expected to grow at 23.61% CAGR between 2025 and 2030.

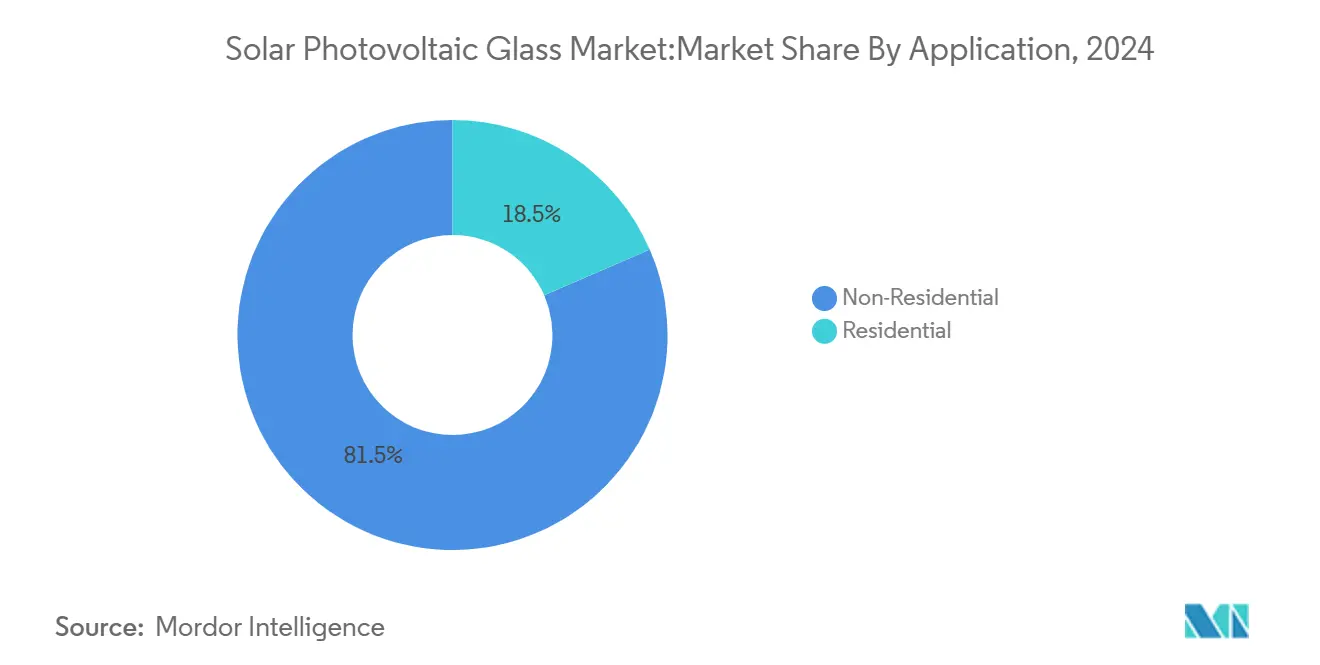

- By application, non-residential installations accounted for 81.5% of 2024 demand and are advancing at an 18.90% CAGR to 2030.

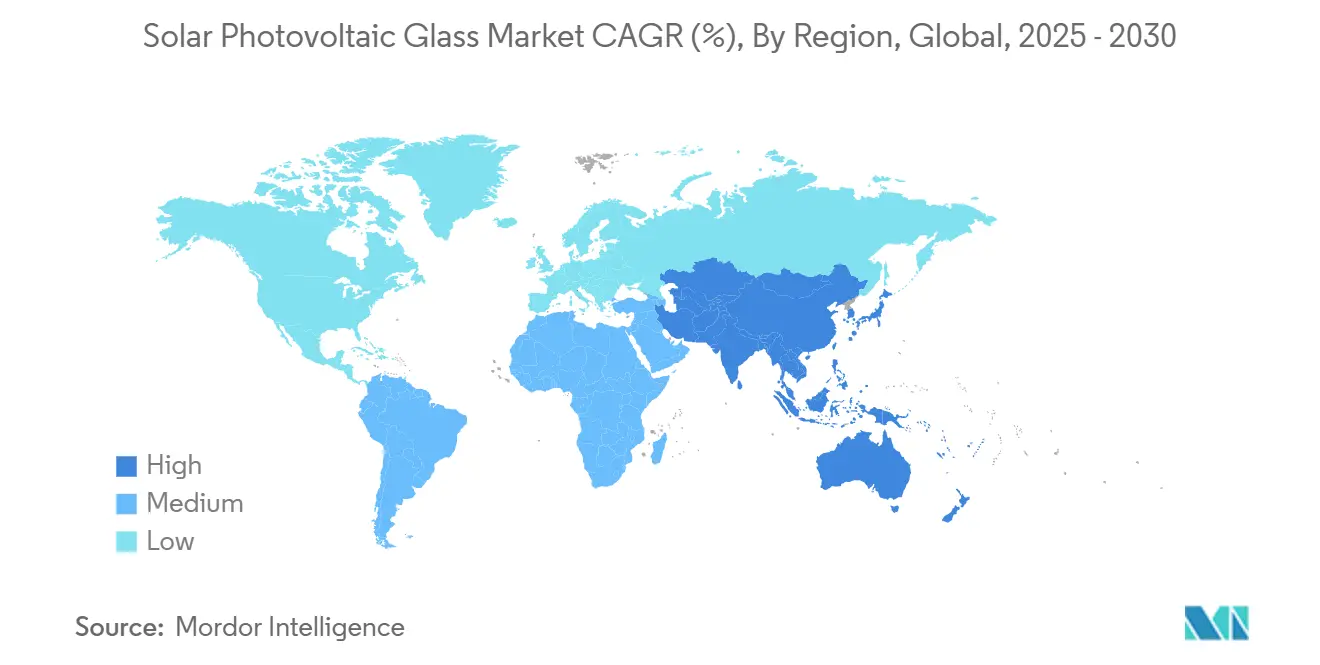

- By geography, Asia-Pacific captured 62% of 2024 volume; the region also commands the highest forecast growth at 19.90% CAGR to 2030.

Global Solar Photovoltaic Glass Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Mandated Solar-Glass Quotas in Asia | +5.20% | Asia-Pacific, spillover global | Medium term (2-4 years) |

| Rapid Capacity Build-outs of Ultra-Low-Iron Float Lines in MENA | +3.10% | MENA core, spillover to Europe | Medium term (2-4 years) |

| Declining Solar Panel Costs | +4.80% | Global | Short term (≤ 2 years) |

| Increasing Adoption of Renewable Energy | +4.50% | Global | Long term (≥ 4 years) |

| Supportive Government Policies across US, Europe and Asia | +2.90% | US, Europe, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-mandated solar-glass quotas in Asia

Wider and stricter installation mandates across China, India, Indonesia, and Israel have established predictable demand that underpins new furnace projects. China’s 2024 guidelines raise efficiency thresholds for solar manufacturing, favoring producers of premium glass with superior optical properties. India’s local-content rules take effect in mid-2026, redirecting procurement toward domestic factories and triggering an estimated 20–30% boost in national output. Indonesia’s phased rooftop quotas aim for 5.75 GW capacity by 2028, while Israel now requires solar panels on all new roofs, lifting residential glass demand by 15-20% annually. The cumulative effect secures baseline offtake, lowering investment risk for greenfield and brownfield expansions across the solar photovoltaic glass market.

Rapid capacity build-outs of ultra-low-iron float lines in MENA

Egypt, Morocco, and the Gulf states are adding premium float capacity to localize supply chains and leverage abundant solar resources. Egypt’s USD 172 million silicon complex in New Alamein will integrate upstream, capturing value from metallurgical-grade silicon to polysilicon and specialty glass[1]Sohaila Khaled, “Egypt constructing silicon complex in New Alamein at $172 mln total investments,” Ahram Online, english.ahram.org.eg . United Solar Holding’s polysilicon factory underscores first-mover advantage in the region, while Morocco’s Noor and Egypt’s Benban projects assure stable downstream consumption. Proximity to Europe shortens lead times and underpins interest from European module makers seeking diversification from Asia. These dynamics accelerate a more balanced global footprint for the solar photovoltaic glass market.

Declining solar panel costs

Spot prices for high-purity quartz sand, a key raw material, collapsed while global module prices plateaued at historic lows despite sluggish demand. China’s 650–750 GW cell capacity expansion created structural oversupply, translating into a deflationary environment that spurs installations in price-sensitive economies. Cheaper modules lift project viability, thereby raising throughput for glass producers even as margins tighten. Manufacturers now compete on scale, logistics efficiency, and coating innovation to defend profitability in the solar photovoltaic glass market.

Increasing adoption of renewable energy

Cumulative solar capacity reached 1.6 TWdc in 2023, up 89% on 2022, while building-integrated photovoltaics (BIPV) gained momentum. Tandem perovskite-organic cells achieved record 25.7% efficiency, pushing module developers to seek glass substrates with higher durability and UV resistance. As corporates set carbon-neutrality goals, non-residential rooftops and carports add significant megawatts, converting warehouses and logistic hubs into power assets. The breadth of applications broadens order visibility across size classes, bolstering long-term growth for the solar photovoltaic glass market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soda-Ash & Energy Cost Volatility Squeezing Glass Margins | -2.30% | Global, acute in Europe | Short term (≤ 2 years) |

| Capital-Intensive Furnace Conversions to Low-Carbon Fuels | -3.50% | Global, acute in OECD | Long term (≥ 4 years) |

| Competition from Alternative Energy Sources | -1.20% | Regions with diverse mixes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soda-ash and energy cost volatility

Soda ash spot prices rose 5–8% in 2024, while European natural-gas costs swung ±15–20%, inflating production expenditure by up to 6% and squeezing margins in an industry already competing on price. Producers respond with long-term supply contracts, efficiency upgrades, and onsite renewables, yet the pass-through to module OEMs remains limited in a surplus market. This mismatch between rising input prices and flat selling prices restricts reinvestment budgets, slowing furnace upgrades in the solar photovoltaic glass market[2]Alex Scott, “Can synthetic soda ash survive?” Chemical & Engineering News, cen.acs.org .

Capital-intensive furnace conversions to low-carbon fuels

Electric melting or hydrogen-ready furnaces cost USD 50–100 million per line and require multi-year downtime, creating revenue gaps and financing hurdles. Early movers such as AGC and Saint-Gobain allocate substantial capex to meet voluntary and regulatory decarbonization targets, but laggards with legacy natural-gas lines retain lower cost bases. Uneven adoption risks price distortions unless carbon-adjustment measures equalize competitive conditions across borders. The resulting uncertainty defers investment decisions and tempers the growth trajectory of the solar photovoltaic glass market.

Segment Analysis

By Glass Type: AR coatings hold sway as TCO gains momentum

In 2024, anti-reflective coatings commanded 57% of the solar photovoltaic glass market, supported by entrenched float infrastructure and proven light-capture gains. The segment’s dominance is reinforced by standardized recipes and high yields, especially for commodity mono-perc modules. Nonetheless, TCO glass is scaling at a 22.46% CAGR thanks to its dual role as conductive layer and encapsulant interface, which reduces manufacturing steps for heterojunction and tandem cells. A surge in research on p-type transparent conductors and indium-free formulations accelerates commercialization prospects, even though uniform deposition at industrial width remains a technical barrier. Cross-licensing deals and sputtering-target alliances are therefore proliferating as firms seek secure supply[3]Woods-Robinson et al., “From design to device: challenges and opportunities in computational discovery of p-type transparent conductors,” arXiv, arxiv.org .

The competitive shift encourages AR-focused producers to upgrade lines with duplex coatings that merge anti-reflective and hydrophobic properties, safeguarding share while raising average selling price. Tempered substrates continue serving high-wind and hail markets, and patterned or ultra-clear variants gain traction in BIPV façades where aesthetics drive decisions. Overall, diverging performance criteria across module architectures are broadening the solution set, sustaining multiproduct strategies inside the solar photovoltaic glass market.

Note: Segment shares of all individual segments available upon report purchase

By Manufacturing Process: Rolled lines complement float dominance

Float production delivered 68% of output in 2024 because of superior flatness that maximizes light throughput and ensures tight thickness tolerances. These attributes underpin bankability for utility-scale projects, which rely on long-term performance warranties. Rolled lines, however, are advancing 19.70% CAGR through 2030, lifted by lower capital cost and recent quality gains from advanced calendaring and polishing. Emerging exporters in Southeast Asia and the Middle East embrace rolled technology to accelerate market entry without the complexity of float furnaces.

Hybrid tempering and laser-texturing solutions now let rolled glass approximate float optical standards while retaining price advantages. Concurrently, investments in upgraded furnace insulation and oxy-fuel firing improve float energy efficiency, narrowing the gap in operating cost. The interplay of these advancements enables project developers to tailor glass selection to climate, loading, and cost targets, enriching choice within the solar photovoltaic glass market.

By Solar Technology: CIGS accelerates within a silicon world

Crystalline silicon maintained 91% share of the solar photovoltaic glass market size in 2024, a reflection of its mature ecosystem and declining wafer prices. Yet Copper-Indium-Gallium-Diselenide modules are growing fastest at 23.61% CAGR, propelled by lab efficiency and inherent flexibility that suits lightweight designs. CIGS adoption is further spurred by space-constrained rooftops in high-rise urban zones, where lighter loads ease permitting. Cadmium-Telluride technology, championed by First Solar, retains an edge in ultra-low-carbon footprints, attracting utility-scale buyers bound by scope-3 emissions targets. Bifacial CdTe prototypes with hierarchical transparent back contacts highlight ongoing R&D aimed at energy-yield gains.

Amorphous silicon remains niche, but its roll-to-roll compatibility may find new relevance in agrivoltaic greenhouses and vehicle-integrated solar where diffuse light is abundant. Taken together, technology pluralism stabilizes demand across glass thicknesses, coatings, and form factors, anchoring multi-year order books for diverse suppliers inside the solar photovoltaic glass market.

By Application: Commercial and utility users shape demand

The non-residential domain represented 81.50% of 2024 volume and continues leading at an 18.90% CAGR as corporates deploy rooftop arrays to offset carbon and hedge power prices. Warehouse, data-center, and shopping-mall owners increasingly monetize unused roof space, locking in predictable cash flows backed by power-purchase agreements. Utility-scale parks remain central to climate-policy targets, with developers favoring large-format glass to reduce balance-of-system cost per watt. The solar photovoltaic glass market share thus skews toward heavy-duty tempered panels that tolerate extreme wind and sand.

Residential demand benefits from net-metering reforms and declining hardware costs, but growth is steady rather than explosive. Building-integrated photovoltaics could catalyze future step-changes once standardized façade elements enter mass production. Meanwhile, specialty uses such as floating solar, agrivoltaics, and transportation noise barriers introduce niche specifications—anti-soiling coatings, high mechanical load resistance, or specific translucency—that spur product innovation and embed optionality across the solar photovoltaic glass market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific dominates the solar photovoltaic glass market with 62% of global volume in 2024 and is set to expand at 19.90% CAGR to 2030. China’s investment guidelines, finalized in late 2024, reward high-efficiency manufacturing and sustainability compliance, incentivizing upgrades to larger float baths and plasma sputtering lines. India’s antidumping duties on imported solar glass shift procurement to local mills, while Southeast Asia capitalizes on trade tensions by hosting module assembly clusters that consume rising tonnage of regional glass. Beyond manufacturing, rooftop quotas in Indonesia and mandatory installations in Israel strengthen end-market growth, anchoring the regional demand curve.

North America is experiencing a renaissance after the Inflation Reduction Act, with more than 280 GW of announced module assembly, cell, and wafer projects. Federal subsidies now extend to glass substrates, and the administration’s 2025 tariffs on Southeast Asian imports aim to nurture domestic supply chains. New float and rolled lines in Georgia, Ohio, and Texas shorten lead times and de-risk logistics for utility-scale projects. These moves gradually reduce reliance on imports and stimulate technology partnerships between U.S. glassmakers and cell integrators intent on localized content.

Europe retains a strong position owing to binding climate targets and deep refurbishment cycles across its building stock. The European Solar Charter bolsters regional manufacturing, while recycling mandates drive closed-loop collaborations such as AGC with ROSI. Energy-price volatility post-2022 reinforces the economics of onsite solar for industrial users, lifting panel demand and thus glass consumption. The MENA region, meanwhile, turns into a strategic manufacturing node and power exporter. Egypt and Morocco host integrated complexes that feed both domestic gigawatt pipelines and export corridors into Europe, diluting Asia’s historic dominance and adding resilience to the solar photovoltaic glass market.

Competitive Landscape

The global solar photovoltaic glass market is moderately consolidated: the five largest producers command about 64% of melting capacity, yet regional pockets exhibit differing dynamics. Chinese leaders Xinyi Solar and Flat Glass Group deploy scale as their chief weapon, targeting 32,200 tonnes per day of combined capacity by end-2024. They leverage integrated sand mining, float lines, and module assembly to extract cost efficiencies difficult for smaller peers to match. Price leadership from these firms keeps commodity AR-coated panels affordable in emerging markets.

Western incumbents AGC, Saint-Gobain, and NSG Group pursue premium positioning built around low-carbon, high-performance products. AGC’s Low-Carbon Glass and circularity partnership with ROSI highlight its commitment to life-cycle impact reduction. Saint-Gobain’s acquisition of CSR in Australia expands downstream reach in fast-growing construction segments, linking façade products with BIPV glass. NSG’s new U.S. solar line secures domestic customers seeking supply-chain security in the wake of geopolitical and logistics upheavals. These moves collectively tilt Western portfolios toward value-added niches rather than pure volume.

Emerging challengers differentiate through sustainability and regional proximity. SOLARCYCLE is building the first U.S. facility to remake solar-grade glass from retired modules, sourcing low-carbon soda ash under a multi-year contract with Genesis Alkali. Smaller MENA producers market ultra-low-iron output tied to renewable-powered furnaces, positioning for future carbon border adjustments. This layered competitive structure encourages partnership models, whereby cell and module makers lock in supply with off-take agreements, reinforcing stability across the solar photovoltaic glass market.

Solar Photovoltaic Glass Industry Leaders

Xinyi Solar Holdings Limited

Flat Glass Group Co. Ltd.

AGC Inc.

Saint-Gobain

Guardian Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: AGC Glass Europe and ROSI have partnered to recycle photovoltaic cover glass into high-purity feedstock for float production. The collaboration combines ROSI's separation technology with AGC's furnace infrastructure, ensuring a stable cullet supply at consistent pricing while reducing raw sand usage.

- January 2025: NSG Group has commenced operations of a new solar glass production line in the United States, strengthening its position in the solar photovoltaic glass market. This development is expected to enhance the supply of high-quality solar glass, supporting the growing demand in the renewable energy sector.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the solar photovoltaic glass market as low-iron glass sheets that encapsulate or replace conventional module covers and simultaneously function as the light-harvesting surface in crystalline-silicon, CdTe, CIGS, or other PV modules. According to Mordor Intelligence, sizing is expressed in metric tons of new PV-grade glass shipped to module makers or directly integrated in building façades.

Scope exclusion: patterned solar control glass without integrated photovoltaic functionality, automotive smart glass, and any post-consumer recycled volume are outside this study.

Segmentation Overview

- By Glass Type

- Tempered Glass

- Anti-Reflective (AR) Coated Glass

- Transparent Conductive Oxide (TCO) Glass

- Others

- By Manufacturing Process

- Float Glass

- Rolled Glass

- By Solar Technology

- Crystalline Silicon

- Cadmium-Telluride (CdTe) Thin Film

- Amorphous Silicon (a-Si)

- Copper-Indium-Gallium-Diselenide (CIGS)

- Other Technologies

- By Application

- Residential

- Non-Residential

- Commercial

- Industrial/Institutional

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Egypt

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed manufacturing engineers from float-line operators, procurement managers at module assemblers across Asia, Europe, and North America, and EPC contractors active in utility-scale projects. These conversations confirmed average melt-tank utilizations, real-world wastage, and anticipated AR-coating adoption, allowing us to close data gaps flagged during desk research and to triangulate cost progression assumptions.

Desk Research

We began with structured pulls from public bodies such as the International Renewable Energy Agency, the International Energy Agency PVPS database, China's National Energy Administration, and Eurostat trade codes for HS-700719. These sources outlined installed PV capacity additions and cross-border flows of low-iron rolled glass, which anchored regional supply-demand balances. Our team then layered insights from company 10-Ks, investor decks, SolarPower Europe installation trackers, and customs-level shipment analytics retrieved through Volza and D&B Hoovers to refine conversion factors for glass per watt ratios. The indicative sources listed are not exhaustive; many additional open datasets and press releases were referenced for validation.

Market-Sizing & Forecasting

A top-down production and trade reconstruction established 2025 demand, after which regional supplier roll-ups and sampled average selling price multiplied by weight served as cross-checks. Key variables fed into the model include national installation targets, square meters of module glass per watt, float-line capacity pipelines, glass conversion yield, and quarterly ASP shifts. Multivariate regression paired with scenario analysis projects volume to 2030, while an ARIMA overlay smooths cyclical fluctuations in module build rates. Where bottom-up estimates diverged, we recalibrated coefficients through iterative back-testing against historical shipments.

Data Validation & Update Cycle

Outputs pass a two-level analyst review that flags anomalies versus independent indicators such as polysilicon drawdowns and EVA sheet sales. Reports refresh annually, with mid-cycle updates triggered by capacity announcements, trade policy shifts, or greater than 5 percent variance in quarterly installations.

Why Mordor's Solar Photovoltaic Glass Baseline Earns Trust

Published numbers often differ because firms mix solar control glass with PV grades, apply disparate ASP progressions, or convert currencies at outdated rates.

Key gap drivers lie in scope breadth, unit of account, and refresh cadence. We report physical tons tied to module production schedules, whereas many publishers release blended dollar values or include non-PV architectural glass, which inflates totals. Others project aggressive CAGR paths without reconciling them against float-line construction lead times or ethylene-vinyl-acetate supply constraints.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 32.10 Mn tons (2025) | Mordor Intelligence | - |

| USD 53.5 Bn (2024) | Global Consultancy A | Mixes PV and solar control glass, value basis, broader product scope |

| USD 17.3 Bn (2024) | Industry Journal B | Excludes China's captive glass output, relies on installation-led revenue multiples |

| USD 10.08 Bn (2024) | Regional Consultancy C | Uses static ASP, limited primary checks, last update greater than 18 months ago |

Taken together, the comparison shows that Mordor's disciplined, annually refreshed tonnage model grounded in verified production and trade data offers clients the most reproducible baseline for strategic planning.

Key Questions Answered in the Report

What is the current size of the solar photovoltaic glass market?

The solar photovoltaic glass market size stood at 32.10 million tons in 2025 and is projected to reach 74.75 million tons by 2030.

Which glass type commands the largest share today?

Anti-reflective coated glass leads with 57% of global volume due to its proven ability to maximize light transmission.

Why is TCO glass growing so quickly?

TCO glass provides both transparency and electrical conductivity, which aligns with heterojunction and tandem cell designs, driving a 22.46% CAGR through 2030.

Which region dominates production?

Asia-Pacific held 62% of 2024 global output and continues to expand capacity, especially in China and India.

What is the outlook for CIGS technology?

CIGS modules are expected to grow at 23.61% CAGR to 2030, making them the fastest-expanding technology segment.