| Study Period | 2019 - 2030 |

| Market Volume (2025) | 51.96 Million units |

| Market Volume (2030) | 87.60 Million units |

| CAGR | 11.01 % |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

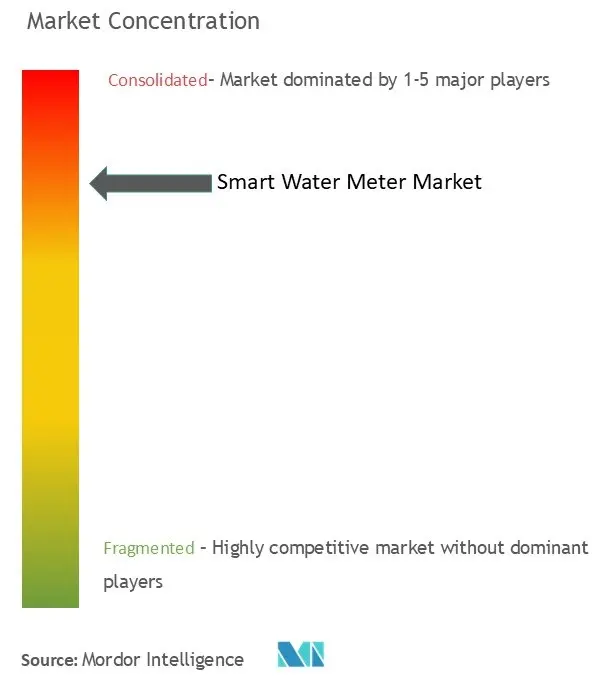

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Smart Water Meter Market Analysis

The Smart Water Meter Market size in terms of shipment volume is expected to grow from 51.96 million units in 2025 to 87.60 million units by 2030, at a CAGR of 11.01% during the forecast period (2025-2030).

The water utility industry is experiencing a significant transformation driven by increasing water consumption patterns and resource scarcity concerns. The United States leads global per capita water consumption at 2,842 cubic meters as of 2022, followed by Canada and New Zealand, highlighting the critical need for better water consumption monitoring and management. This escalating water usage, coupled with rapid urbanization trends, has pushed utilities to adopt more sophisticated monitoring solutions. According to UN-HABITAT projections, global urbanization is expected to reach 89% by 2050, creating unprecedented pressure on water infrastructure and management systems.

The integration of advanced technologies like IoT, AI, and machine learning is revolutionizing smart water management capabilities. Modern smart meters now offer comprehensive functionality beyond basic consumption measurement, including the ability to monitor water quality parameters, flow rates, and pH balance. These technological advancements are enabling real-time water leak detection, consumption pattern analysis, and automated billing systems, fundamentally changing how utilities and consumers interact with water resources. The Dubai Electricity and Water Authority demonstrated the growing adoption of such technologies, recording a 73.6% increase in smart water meters between 2018 and 2022.

Recent infrastructure modernization initiatives across major economies are accelerating the transition to smart water metering systems. In the United Kingdom, where water companies lose approximately 42% of water through leaking pipes, utilities are implementing aggressive smart meter deployment programs. Notable developments include Yorkshire Water's significant investment in smart meter technology in 2023 and Oxford's groundbreaking legislation making smart water meter installation mandatory for all residents, marking a shift toward compulsory adoption of smart metering solutions.

The industry is witnessing a surge in innovative product launches and technological partnerships aimed at enhancing meter capabilities and connectivity. In May 2023, Honeywell introduced its Next Generation Cellular Module, enabling the upgrade of legacy water meters to smart water meter systems without additional infrastructure investments. Similarly, Anglian Water's announcement in February 2023 to explore an 'end-to-end' smart metering delivery solution exemplifies the industry's move toward comprehensive digital transformation. These developments are complemented by rising consumer awareness about water conservation and the need for accurate billing, with Water UK reporting a significant 7.5% increase in typical water bills to GBP 448 annually from April 2023.

Smart Water Meter Market Trends

Supportive Government Regulations

Government initiatives and regulatory support have emerged as crucial drivers for smart water meter market adoption across global markets. The implementation of supportive policies and legislation is creating a strong foundation for market growth, with numerous governments providing financial incentives and mandating smart meter installations. For instance, in June 2022, a smart water meter joint venture initiative by Midcoast Council saw up to 40 large water users install smart water meters across their properties, resulting in savings of 169 million liters of water, equivalent to more than eight days of water supply for the entire region.

Recent regulatory developments have been particularly impactful in driving adoption. In August 2023, Water Corporation introduced Western Australia's most extensive smart water meter program, planning to install more than 16,000 digital smart meters at homes and businesses across Perth. Similarly, in March 2022, the Water and Sanitation Agency in Lahore signed an agreement to install 711,000 smart meters under a public-private partnership, demonstrating how government support is facilitating large-scale implementations. These initiatives are complemented by programs like the US Environmental Protection Agency's WaterSense partnership program, which awards utilities implementing smart water metering technologies.

Understand The Key Trends Shaping This Market

Download PDF

Need for Improvement in Water Utility Usage and Efficiency

The pressing need to enhance water utility management efficiency has become a significant market driver, particularly as utilities worldwide struggle with aging infrastructure and increasing operational costs. According to the American Society of Civil Engineers, nearly 6 billion gallons of treated water are lost daily in the United States due to water main breaks occurring every two minutes. This wastage of potable water is increasing operational costs for utilities, driving the adoption of smart metering solutions that can help identify and address these inefficiencies.

The drive for efficiency is reflected in substantial investment commitments from major utilities. Essential Utilities plans to invest USD 1.1 billion in 2023 and USD 3.3 billion through 2025 to improve water systems and enhance customer service through improved information technology. Similarly, California Water Service has allocated over USD 725 million in capital expenditure through 2024, while Middlesex Water plans to invest USD 266 million from 2023-2025. These investments are directly targeting efficiency improvements through smart metering technologies, which have demonstrated significant results. For instance, Dubai Electricity and Water Authority's alert service caught 1,327,583 leakages in water connections, 26,657 defects, and 13,172 cases of increased load, reducing CO2 emissions by 218,373 tons as of December 2022.

Increasing Demand to Reduce Non-revenue Water Losses

The critical challenge of non-revenue water (NRW) losses has emerged as a major driver for smart water meter market analysis globally. NRW, which includes water lost through leaks, theft, or metering errors, significantly impacts utility operations and financial sustainability. According to the Asian Development Bank, reducing NRW should be the primary focus for many cities when addressing low service coverage levels and increased demand for piped water supply, as expanding water networks without addressing water losses would only perpetuate inefficiency cycles.

The implementation of smart water analytics solutions has shown remarkable results in reducing NRW losses. For instance, by 2022, Maynilad's expanded network of 1.52 million service connections demonstrated significant improvements, serving 10 million people (a 64% improvement from 2007), with water service coverage rising to 95% and NRW reducing to 30.31%. This success has spurred increased investment in smart water infrastructure, exemplified by recent government initiatives. In April 2023, the Biden-Harris Administration announced nearly USD 585 million from the Bipartisan Infrastructure Law to repair aging water infrastructure, funding 83 projects across 11 states to increase drought resilience and improve water delivery systems. Similarly, in June 2023, the Tennessee Department of Environment and Conservation announced 131 grants totaling USD 300 million for drinking water, wastewater, and stormwater infrastructure improvements.

Segment Analysis: By Technology

Automatic Meter Reading Segment in Smart Water Meter Market

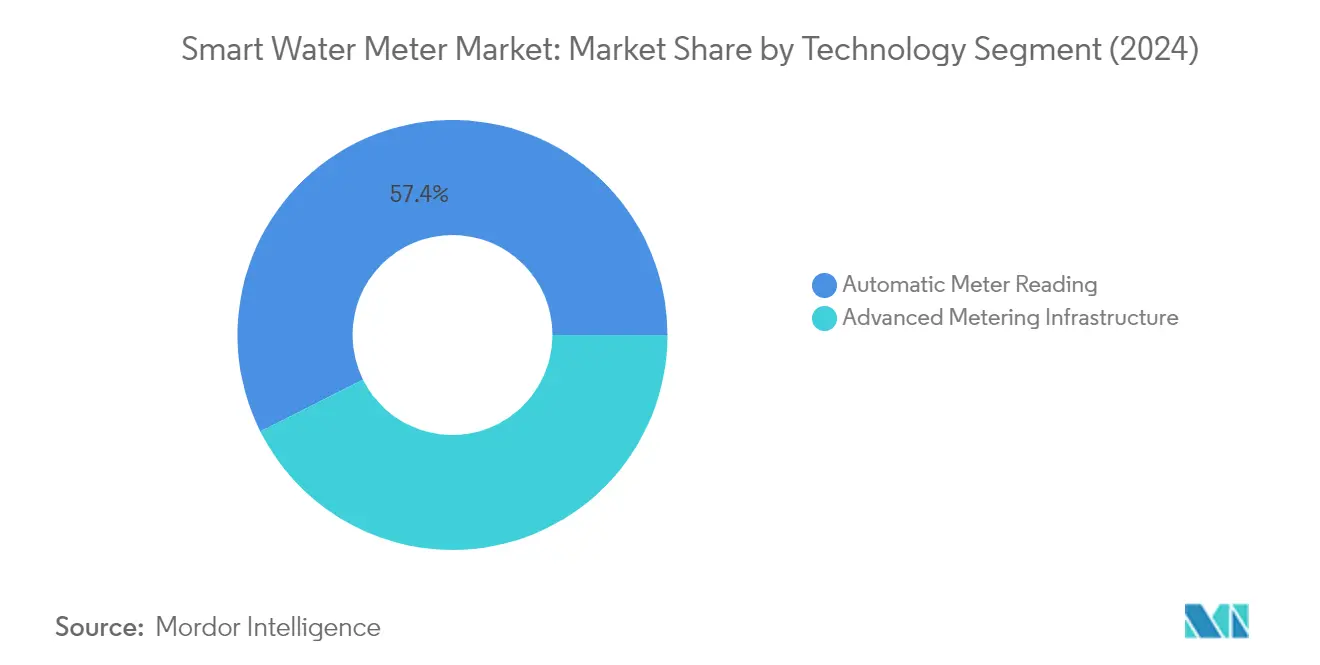

The AMR water meter segment continues to dominate the smart water meter market, holding approximately 57% market share in 2024. AMR technology has gained widespread adoption due to its cost-effective advantages and valuable resource- and time-saving benefits. A key advantage of the AMR water meter is its ability to be easily installed on existing meters, allowing for a seamless transition to a smart solution. The technology enables utilities to effectively monitor and analyze usage, troubleshoot concerns, and accurately bill customers based on actual consumption, eliminating the need for predictions that were previously necessary with bi-monthly or quarterly manual reads. AMR systems can be conducted through either walk-by or drive-by methods, where an endpoint connected to the meter's encoder register records water flow and alarm data, which utility personnel then collect by walking or driving with a data receiver near the device.

Advanced Metering Infrastructure Segment in Smart Water Meter Market

The AMI water meter segment is projected to witness the highest growth rate of approximately 18% during the forecast period 2024-2029. The AMI water meter represents the next evolution in smart water metering technology, offering a comprehensive solution that enables two-way communication between utilities and meters. This technology provides utilities with the capability to gather, measure, communicate, and assess data on water usage from treatment to customer delivery in real-time. AMI systems have integrated technology that generates continuous-use reports and leak detection alerts, with customizable parameters that can be set by water utilities. The technology also enables the quantification of water conservation achieved through leak repairs, efficiency initiatives, and conservation campaigns, while helping identify equipment programming errors such as incorrect irrigation scheduling.

Segment Analysis: By Application

Residential Segment in Smart Water Meter Market

The residential water meter segment continues to dominate the smart water meter market, commanding approximately 94% of the total market share in 2024. This substantial market presence is driven by the increasing adoption of residential water meter in homes and residential complexes for accurate consumption monitoring and billing. The technology enables homeowners to effectively track their water usage patterns, identify potential leaks, and implement water conservation measures. Smart water meters in residential applications provide valuable insights into individual household consumption patterns, helping utilities and consumers make informed decisions about water usage. The growing urbanization trends and improvements in water infrastructure across various regions have further strengthened the residential segment's position in the market. Additionally, several governments and authorities are actively promoting the use of smart water meters in their water conservation and sustainability efforts, with some regions implementing regulations that mandate the installation of smart water meters in new homes or renovations.

Commercial Segment in Smart Water Meter Market

The commercial water meter segment is emerging as the fastest-growing segment in the smart water meter market, with a projected growth rate of approximately 12% during 2024-2029. This accelerated growth is attributed to the increasing adoption of commercial water meter across various commercial establishments, including hotels, schools, hospitals, and public infrastructure facilities. The segment's growth is primarily driven by the need for efficient water management solutions that can help commercial building owners balance water demand and supply while reducing operational costs. Smart water meters enable more efficient meter reading and help reduce non-revenue water losses in commercial applications. The increased data transparency allows businesses to understand water usage patterns, identify billing discrepancies, and encourage water-saving behaviors. Furthermore, the rising investments in commercial real estate sectors across various regions are creating additional opportunities for smart water meter deployments in this segment.

Remaining Segments in Smart Water Meter Market

The industrial water meter segment plays a crucial role in the smart water meter market, serving various sectors including food and beverages, chemical, pharmaceutical, sewage treatment, and industrial utility management. This segment is particularly important for manufacturing facilities that require precise control of water consumption at different stages of their production processes. Smart water meters in industrial applications offer specialized features such as backflow detection and real-time leak identification, which are crucial for maintaining safe and efficient operations. The technology helps industries optimize their water usage, reduce wastage, and comply with environmental regulations while ensuring sustainable operations. The segment's impact on the overall market is significant as it drives innovation in high-capacity metering solutions and advanced monitoring capabilities.

Smart Water Meter Market Geography Segment Analysis

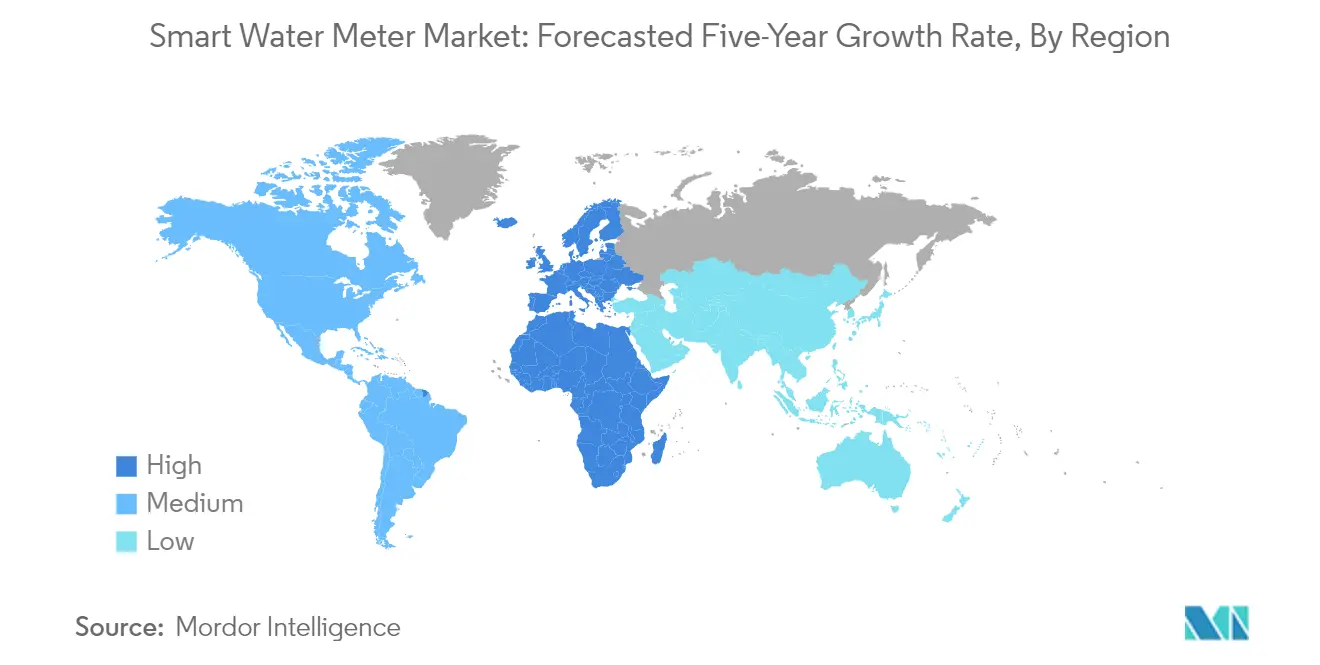

Smart Water Meter Market in North America

The North American smart water meter market holds approximately 24% of the global smart water meter market share in 2024, establishing itself as a crucial region in the global landscape. The market's growth is primarily driven by water scarcity challenges in the Western regions and aging infrastructure concerns in the Midwest and East, which have reinforced the need for efficient remote meter reading solutions. Water utilities across the United States are actively embracing innovative technologies to ensure adequate water supply, reduce operational costs, manage assets effectively, and support water conservation initiatives. The region's focus on infrastructure modernization, coupled with the growing emphasis on reducing non-revenue water losses, has created a strong foundation for market expansion. Advanced Metering Infrastructure (AMI) continues to gain significant traction, particularly in new and developing markets, while traditional technologies like Fixed Network and Powerline Communications maintain their dominance in the communicating meter segment. The presence of sophisticated communication networks and strong technical capabilities among utility providers further strengthens the region's market position.

Smart Water Meter Market in Europe

The European smart water meter market has demonstrated robust growth, achieving approximately a 12% growth rate during the period 2019-2024, driven by increasing government initiatives for better water management and mounting water scarcity concerns. The region's market dynamics are shaped by a strong emphasis on technological innovation and sustainability initiatives, particularly in countries like the United Kingdom, France, and Germany. European utilities are increasingly focusing on implementing advanced metering solutions to address water conservation challenges and improve operational efficiency. The market is characterized by a high level of technological adoption, with utilities actively pursuing digital transformation initiatives to enhance customer service and reduce operational costs. The presence of established manufacturers and ongoing research and development activities further strengthens the region's competitive position. Integration of smart water meters with existing infrastructure and the development of comprehensive water management system solutions remain key focus areas for market participants.

Smart Water Meter Market in Asia-Pacific

The Asia-Pacific smart water meter market is projected to grow at approximately 10% during the forecast period 2024-2029, positioning itself as a region with significant growth potential. The market is characterized by rapid urbanization, increasing water stress, and growing government initiatives to improve water infrastructure planning. China and Japan lead the regional market with their advanced technological capabilities and strong focus on smart city development. The region's growth trajectory is supported by increasing investments in water infrastructure modernization and the adoption of advanced metering technologies. Rising concerns about water scarcity, particularly in developing economies, are driving the implementation of smart water metering solutions. The market is witnessing a transformation with the integration of Internet of Things (IoT) technology and artificial intelligence in water metering systems, leading to improved efficiency and better resource management.

Smart Water Meter Market in Latin America

The Latin American smart water meter market is experiencing significant transformation driven by increasing urbanization and growing water conservation needs. The region faces unique challenges related to water infrastructure modernization and the need for efficient water management systems. Market growth is primarily supported by government initiatives aimed at reducing water losses and improving distribution efficiency. The adoption of smart water meters is gaining momentum as utilities seek to address issues such as non-revenue water losses and improve billing accuracy. The market is characterized by increasing investments in water infrastructure modernization and the implementation of advanced metering solutions. Growing awareness about water conservation and the need for sustainable water management practices continue to drive market expansion. The region's utilities are increasingly recognizing the benefits of smart water metering in improving operational efficiency and customer service.

Smart Water Meter Market in Middle East and Africa

The Middle East and African smart water meter market is emerging as a significant growth opportunity, driven by acute water scarcity concerns and increasing investments in water infrastructure. The region's unique challenges, particularly in the Middle East where groundwater availability is among the lowest globally, are driving the adoption of smart water management solutions. Governments across the region are implementing various initiatives to support water conservation and rationalize consumption patterns. The market is witnessing increased adoption of advanced metering infrastructure as utilities focus on reducing water losses and improving distribution efficiency. Growing urbanization and population growth are creating additional pressure on water resources, necessitating the implementation of smart water grid solutions. The market is characterized by increasing investments in desalination plants and water distribution infrastructure, creating opportunities for smart meter deployments.

Get Analysis on Important Geographic Markets

Download PDF

Smart Water Meter Market Overview

Top Companies in Smart Water Meter Market

The smart water meter market features established players like Itron, Landis+Gyr, Honeywell, Badger Meter, and Sensus (Xylem) leading technological innovation and market development. These smart water meter companies are heavily investing in research and development to advance their ultrasonic metering technologies, IoT integration capabilities, and communication protocols like LoRaWAN and NB-IoT. The industry demonstrates a strong focus on developing sustainable and recyclable products, with water meter companies like Landis+Gyr introducing biodegradable meters. Strategic partnerships with utilities and technology providers have become increasingly common, enabling enhanced data analytics and remote monitoring capabilities. Smart water meter manufacturers are also expanding their geographical presence through local manufacturing facilities and distribution networks, particularly in high-growth regions like Asia-Pacific and the Middle East.

Market Structure Shows Mixed Global-Local Dynamics

The smart water meter global market exhibits a complex competitive structure characterized by both global conglomerates and specialized regional players. Large multinational corporations like Honeywell and Xylem leverage their extensive resources and cross-industry expertise to maintain market leadership, while specialized players like Kamstrup and Arad Group focus on developing innovative water-specific solutions. The market demonstrates moderate consolidation, with established players maintaining strong positions in their respective regions while simultaneously expanding into emerging markets. The competitive landscape is further shaped by the presence of numerous medium-sized companies that maintain significant smart water meter market share in specific geographical regions or specialized product segments.

The industry has witnessed strategic acquisitions aimed at expanding technological capabilities and geographical reach. Companies are increasingly focusing on acquiring software and analytics firms to strengthen their smart metering solutions portfolio. Regional players are forming strategic alliances with technology providers to enhance their product offerings and compete with global players. The market also sees collaboration between meter manufacturers and communication technology providers to develop integrated solutions that address the growing demand for smart water infrastructure.

Innovation and Integration Drive Future Success

Success in the smart water meter industry increasingly depends on technological innovation and system integration capabilities. Companies must continuously invest in developing advanced metering technologies while ensuring compatibility with existing infrastructure and emerging communication standards. The ability to provide end-to-end solutions, including hardware, software, and analytics platforms, has become crucial for maintaining market position. Customer relationships and service quality are becoming increasingly important as utilities seek long-term partnerships rather than simple product suppliers. Smart water meter suppliers must also focus on developing cost-effective solutions while maintaining high accuracy and reliability standards to address the diverse needs of different market segments.

Market players need to navigate complex regulatory environments while adapting to evolving water management policies across different regions. The ability to provide customized solutions for specific regional requirements while maintaining economies of scale will be crucial for future success. Companies must also address growing cybersecurity concerns and data privacy requirements as smart meters become more connected. The development of user-friendly interfaces and value-added services will be essential for differentiation in an increasingly competitive market. Additionally, sustainability considerations and environmental compliance will play a larger role in product development and market acceptance.

Smart Water Meter Market Leaders

-

WaterTech S.p.A (Arad Group)

-

MOM Zrt

-

Apator SA

-

Arad Group

-

Axioma Metering

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Smart Water Meter Market News

- September 2023 - Honeywell announced the integration of quantum computing hardware encryption Keys on smart utility meters to protect the end user's data from increasing cyber threats. To help strengthen reliability and trust in a digitalized energy sector, the company will use the Quantum Origin technology of Quantinuum. To ensure that natural gas, water, and electricity infrastructures are maintained for residential and commercial purposes, the enhanced security utility meter establishes a new benchmark that protects against data breaches.

- June 2023 - Badger Meter has partnered with the city of Savannah to begin the first phase of the system-wide implementation of Advanced Metering Infrastructure (AMI) or "smart" meters for its water customers. In the first phase of system-wide implementation, a total of 10,000 water meters will be upgraded to AMI meters.

- May 2023 - Honeywell launched the Next Generation Cellular Module (NXCM), a solution that upgrades legacy meters into smart meters without requiring additional infrastructure, improving monitoring and analytics capabilities for utility providers.

Smart Water Meter Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Technology Snapshot for types of Smart Water Meter

- 4.5 ROI Analysis for Smart Meters

- 4.6 Prominent Protocols Used and their Comparison

- 4.7 Steps Involved in Implementing LoraWAN/Prominent Use-cases/Long-term Implications

- 4.8 Advantages/Digitalization Achieved by Utilities by Smart Meter Implementations

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Supportive Government Regulations

- 5.1.2 Need for Improvement in Water Utility Usage and Efficiency

- 5.1.3 Increasing Demand to Reduce Non-revenue Water Losses

-

5.2 Market Restraints

- 5.2.1 High Costs and Security Concerns

- 5.2.2 Integration Difficulties with Smart Meters

- 5.2.3 Utility Supplier Switching Costs

6. MARKET SEGMENTATION

-

6.1 By Technology

- 6.1.1 Automatic Meter Reading

- 6.1.2 Advanced Metering Infrastructure

-

6.2 By Application

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.3 Industrial

-

6.3 By Geography***

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Watertech S.P.A (Arad Group)

- 7.1.2 Mom Zrt

- 7.1.3 Apator SA

- 7.1.4 Arad Group

- 7.1.5 Axioma Metering

- 7.1.6 Badger Meter Inc.

- 7.1.7 Diehl Stiftung & Co. KG

- 7.1.8 Honeywell International Inc.

- 7.1.9 Suntront tech Co., Ltd.

- 7.1.10 Maddalena SPA

- 7.1.11 Waviot

- 7.1.12 Itron Inc.

- 7.1.13 BETAR Company

- 7.1.14 Kamstrup A/S

- 7.1.15 Landis+GYR Group AG

- 7.1.16 Integra Metering AG

- 7.1.17 G. Gioanola Srl

- 7.1.18 Sensus Usa Inc. (Xylem Inc.)

- 7.1.19 Zenner International Gmbh & Co. KG

8. INVESTMENT ANALYSIS

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

*** In the Final Report Asia, Australia and New Zealand will be Studied Together as 'Asia Pacific'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Smart Water Meter Market Industry Segmentation

Smart water meters are devices used to measure the quantity/volume of water passing through a supply pipeline/outlet, which may include the primary water supply pipeline for an entire facility or a sub-zone. Measurements can be done in units, including cubic feet or gallons, among others.

The smart water metering market is segmented by technology (automatic meter reading, advanced metering infrastructure), by application (residential, commercial, industrial), and by geography (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Technology | Automatic Meter Reading |

| Advanced Metering Infrastructure | |

| By Application | Residential |

| Commercial | |

| Industrial | |

| By Geography*** | North America |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Smart Water Meter Market Research FAQs

How big is the Smart Water Meter Market?

The Smart Water Meter Market size is expected to reach 51.96 million units in 2025 and grow at a CAGR of 11.01% to reach 87.60 million units by 2030.

What is the current Smart Water Meter Market size?

In 2025, the Smart Water Meter Market size is expected to reach 51.96 million units.

Who are the key players in Smart Water Meter Market?

WaterTech S.p.A (Arad Group), MOM Zrt, Apator SA, Arad Group and Axioma Metering are the major companies operating in the Smart Water Meter Market.

Which is the fastest growing region in Smart Water Meter Market?

Europe is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Smart Water Meter Market?

In 2025, the Asia Pacific accounts for the largest market share in Smart Water Meter Market.

What years does this Smart Water Meter Market cover, and what was the market size in 2024?

In 2024, the Smart Water Meter Market size was estimated at 46.24 million units. The report covers the Smart Water Meter Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Smart Water Meter Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Smart Water Meter Market Research

Mordor Intelligence provides comprehensive industry analysis and market insights for the smart water meter market, covering crucial aspects such as smart water management, water leak detection, and smart water infrastructure. Our research encompasses detailed market segmentation across residential and commercial applications, technology types including AMI water meters and smart water monitoring systems, and geographical markets with special focus on emerging opportunities. The report pdf delivers actionable intelligence on market size, growth forecasts, competitive landscape analysis of leading smart water meter companies, and technological innovations shaping the smart water metering industry.

Our consulting expertise extends beyond traditional market research to provide strategic insights for stakeholders in the smart water meter industry. We assist clients with technology scouting for advanced metering solutions, regulatory assessment of water utility frameworks, and comprehensive analysis of water consumption monitoring trends. Our capabilities include customer behavior analysis to understand adoption patterns of smart water meters, product positioning strategies for digital water meters, and competitive intelligence on water meter manufacturers. Through data aggregation and advanced analytics, we help businesses make informed decisions about market entry, product development, and strategic partnerships in the evolving smart water grid ecosystem.