Smart Water Management Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

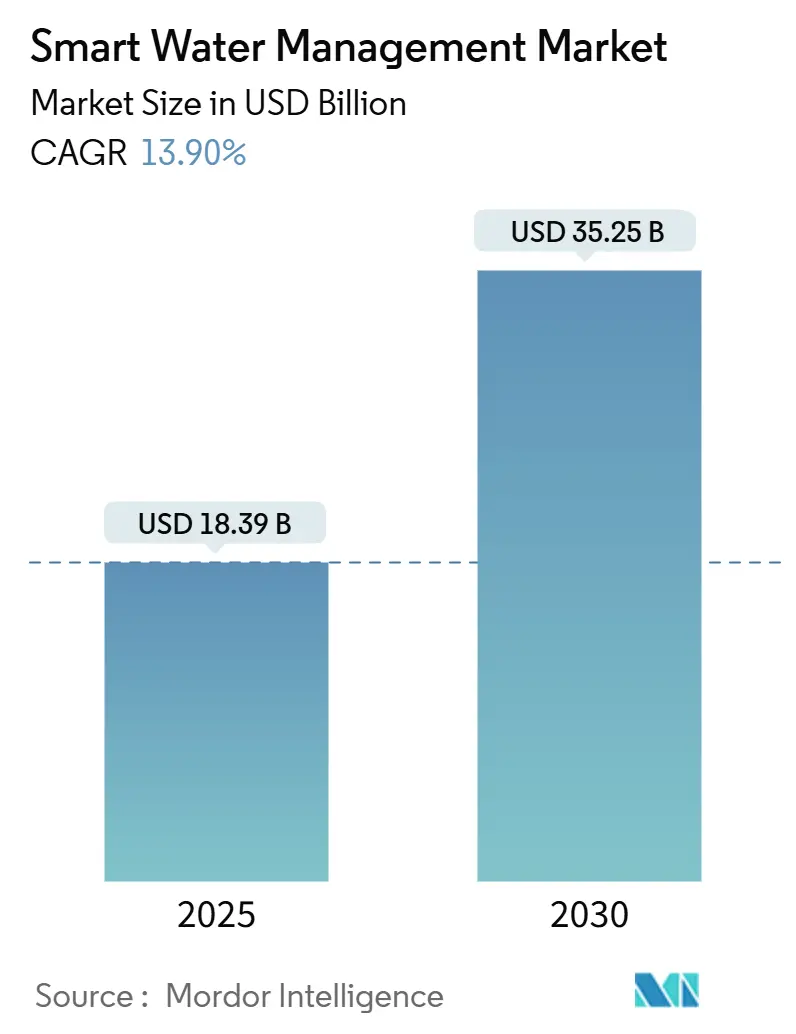

| Market Size (2025) | USD 18.39 Billion |

| Market Size (2030) | USD 35.25 Billion |

| Growth Rate (2025 - 2030) | 13.90% CAGR |

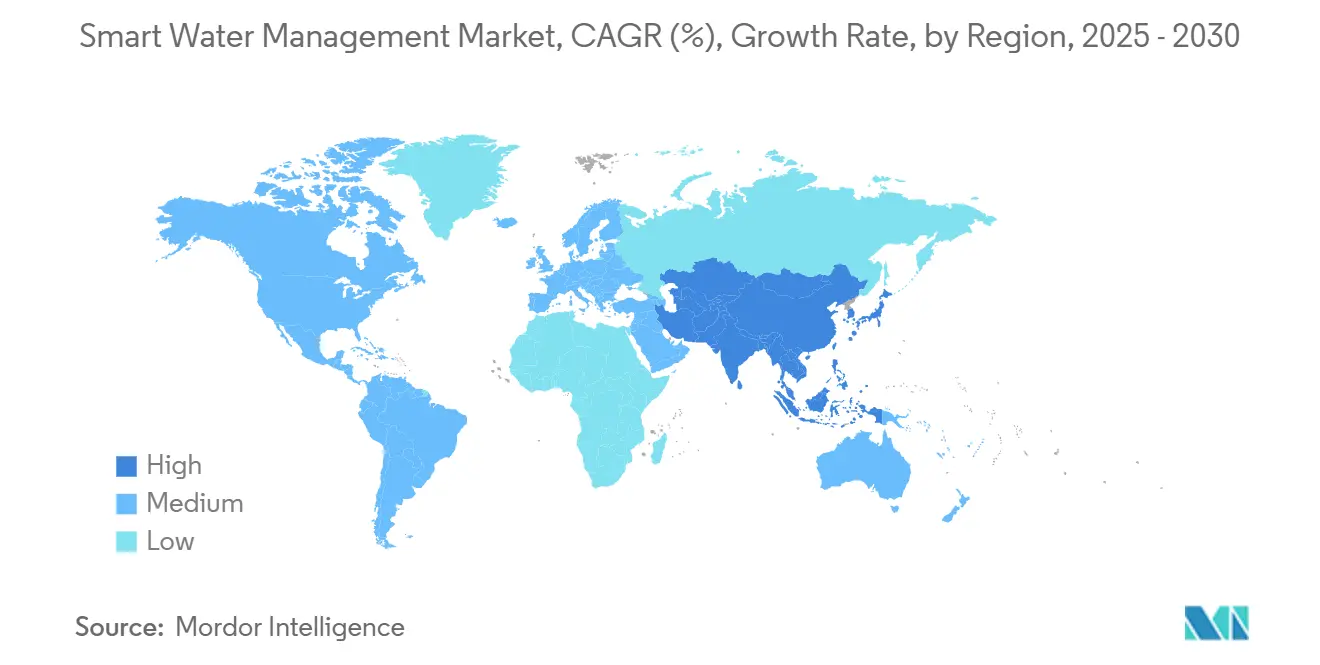

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Smart Water Management Market Analysis by Mordor Intelligence

The smart water management market size is estimated at USD 18.39 billion in 2025 and is forecast to reach USD 35.25 billion by 2030, advancing at a 13.9% CAGR during the period. Rapid scale-up reflects utilities’ shift from incremental leak reduction to data-driven efficiency programs that counter rising water stress and tighter environmental mandates. Utilities now favor integrated monitoring, analytics, and control platforms that transform legacy distribution networks into predictive, self-optimizing systems. Investment momentum is reinforced by the maturation of LPWAN connectivity, proven digital-twin applications, and sizeable government stimulus packages that earmark funds for digital water infrastructure. Traditional metering and SCADA frameworks, once considered adequate, are therefore giving way to end-to-end, cloud-enabled architectures that can document measurable performance improvements.

Key Report Takeways

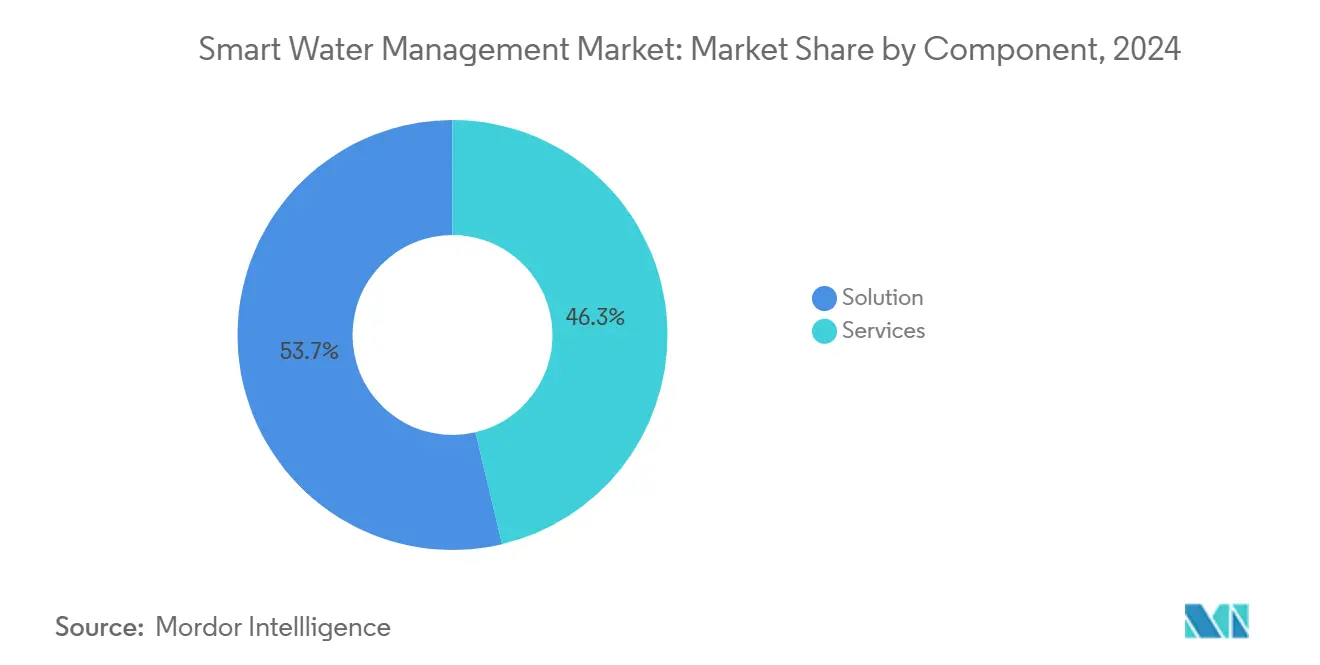

- By component, solutions accounted for 53.7% revenue in 2024; services post the fastest growth at a 16.2% CAGR through 2030.

- By end user, the residential segment held 47.2% of the smart water management market share in 2024 and is on track for a 14.3% CAGR to 2030.

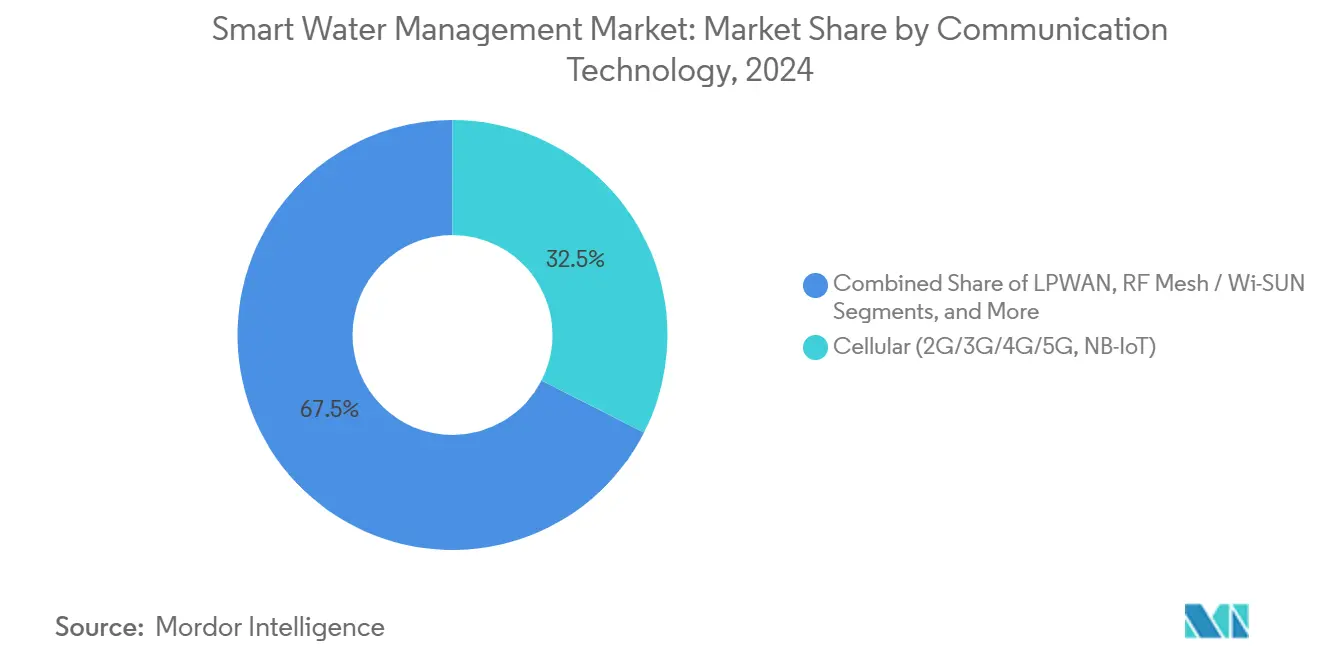

- By communication technology, cellular networks retained 32.5% of the smart water management market size in 2024, while LPWAN is expanding at 15.7% CAGR.

- By geography, North America led with 27.9% revenue share in 2024; APAC represents the fastest-growing region at a 14.3% CAGR to 2030.

Global Smart Water Management Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing need to manage increasing global water demand | +3.2% | Global with acute impact in MENA and Western US | Long term (≥ 4 years) |

| Rising pressure to curb Non-Revenue Water losses | +2.8% | Europe and North America | Medium term (2-4 years) |

| Government smart-city and sustainability mandates | +2.5% | North America, EU, Asia-Pacific core markets | Medium term (2-4 years) |

| Rapid adoption of LPWAN connectivity | +2.1% | Europe and APAC | Short term (≤ 2 years) |

| Digital-twin platforms for predictive pipe failure | +1.8% | North America, Northern Europe, developed Asia-Pacific | Long term (≥ 4 years) |

| US and EU stimulus funds for digital water | +1.4% | North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Need to Manage Increasing Global Water Demand

Severe drought cycles push utilities to treat real-time consumption optimization as mission-critical infrastructure. France recorded 30% precipitation deficits in 2025, prompting usage restrictions across 14 departments—more than double the 2024 count . Greater Lyon responded by installing 5,500 leak sensors and 10,000 connected meters, saving 33,000 m³ per day.[1]Veolia, “Veolia Environnement Press Releases,” veolia.comSourceThese results underscore how predictive analytics turn conservation from public messaging into verifiable supply-demand balancing. Regions with chronic scarcity, especially the Western US and parts of the Mediterranean, now regard digital water platforms as prerequisites for service continuity, cementing long-run demand for the smart water management market.

Rising Pressure to Curb Non-Revenue Water (NRW) Losses

Mounting regulatory scrutiny converts NRW reduction into a survival metric for utilities. Orange County utilities recovered more than USD 4 million annually after smart meter roll-outs, while Jacksonville identified 1 billion gallons of losses previously undetected . In Europe, certain French networks still lose over 50% of transported water, triggering compliance deadlines.[2]Le Monde, “Les fuites d’eau en France,” lemonde.frSource AI-enabled systems such as Siemens’ SIWA Leak Finder helped Sweden’s VA SYD cut NRW from 10% to 8%, proving immediate operational returns. Financial penalties and performance-based rate structures make leak analytics adoption non-discretionary, fueling steady expansion of the smart water management market.

Government Smart-City and Sustainability Mandates

Policies increasingly oblige municipalities to incorporate digital water infrastructure before receiving public funding. Japan’s Ministry of Land, Infrastructure, Transport and Tourism (MLIT) embedded smart-water criteria into its DX Technology Catalog, reshaping procurement norms. Prefectures including Tokushima, Wakayama, and Kumamoto have launched coordinated residential meter pilots, confirming top-down momentum . Comparable directives in the EU tie operating licenses to quantified efficiency gains. By converting digital upgrades from optional to mandatory, regulators shorten adoption cycles and enlarge the global smart water management market.

Rapid Adoption of LPWAN Connectivity (LoRaWAN, NB-IoT)

Advances in LPWAN underpin large-scale, low-power metering roll-outs. SUEZ and Vodafone aim to connect 2 million meters via NB-IoT by 2030, removing utilities’ need to build private networks.[3]SUEZ Group, “SUEZ and Vodafone partnership announcement,” suez.comSouth Africa plans to monitor 15 million meters through Sigfox, validating LPWAN’s national-level scalability . Battery lives exceeding 15 years and deep-indoor penetration cut lifetime ownership costs, giving LPWAN a compelling edge over bandwidth-heavy cellular options and enlarging its role within the smart water management market.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-intensive nature of metering and network upgrades | -2.10% | Developing markets most exposed | Medium term (2-4 years) |

| Interoperability gaps across legacy OT/IT systems | -1.80% | North America and Europe | Long term (≥ 4 years) |

| Cyber-security vulnerabilities in converged water networks | -1.50% | Global | Short term (≤ 2 years) |

| Tariff-driven cost inflation for IoT components | -1.20% | US and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Nature of Metering and Network Upgrades

Full-scale smart water deployments require substantial capital outlays that can exceed smaller utilities’ borrowing capacity. Thames Water signed a GBP 50 million framework to deploy 1 million smart meters by 2030, illustrating the upfront spend needed for broad coverage. Where political sensitivities keep tariffs low, long payback periods hinder board approvals, particularly in emerging economies lacking concessional finance. These budget constraints fragment uptake rates and temper the smart water management market’s near-term growth.

Interoperability Gaps Across Legacy OT/IT Systems

Utilities operating decades-old SCADA installations face costly rip-and-replace choices or middleware work-arounds when integrating IoT platforms. Mixed-vendor protocols create lock-in and raise lifetime support bills, stalling procurement cycles. Integration complexity is especially acute across North American and European utilities with extensive sunk investments, adding risk premiums that slow the smart water management market’s expansion trajectory.

Segment Analysis

By Component: Solutions Dominate Platform Consolidation

Solutions held 53.7% revenue in 2024 as utilities gravitated toward unified suites that span metering, leak detection, analytics, and control. Professional services, managed services, and outcome-based contracts now grow at 16.2% CAGR because utilities realize technology value only when data science and change-management skills are embedded. Enterprise asset management modules integrate with hydraulic modeling engines to predict pipe failures well ahead of visible leaks, reducing emergency repair spend. Distribution network monitoring overlays geospatial analytics onto SCADA data, letting operators prioritize capital projects according to risk scores instead of age alone.

Vendor roadmaps converge around cloud-native architectures that support application marketplaces and low-code customization, which lowers future integration cost. As a result, the smart water management market sees utilities negotiating multi-year platform agreements that bundle licensing with guaranteed operational improvements. Smaller operators embrace managed services to offset talent shortages, while larger counterparts co-develop algorithms with vendors to protect intellectual property advantages. These trends cement solutions as the economic anchor of the smart water management market.

By End User: Residential Drives Adoption and Growth

The residential segment captured 47.2% revenue in 2024 and is expanding at a 14.3% CAGR on the back of mass smart meter programs. Standardized household meter installations allow utilities to amortize deployment costs quickly, accelerating roll-outs across dense urban districts. Japan’s coordinated pilots spanning Tokushima, Kumamoto, and Kyoto highlight national-level commitment to household demand optimization . Dynamic pricing enabled by interval data helps shift consumption away from peak hours, cutting treatment and pumping costs.

Commercial and industrial users push vendors toward granular analytics that benchmark facilities against peer sites, informing corporate ESG disclosures. Public utility campuses adopt digital twins to predict sewer overflows during storm events, unlocking insurance discounts. These diverse requirements enlarge service revenue streams and reinforce the centrality of the residential cohort within the smart water management market.

By Communication Technology: Cellular Leadership Faces LPWAN Challenge

Cellular, including NB-IoT, commanded 32.5% of 2024 revenues, leveraging ubiquitous towers and proven QoS for mission-critical telemetry. The smart water management market size for cellular networks is projected to grow steadily but cede relative share as LPWAN adoption accelerates. LoRaWAN and Sigfox, posting 15.7% CAGR, outperform on battery life and module cost, making them ideal for remote meters and buried installations where maintenance visits are costly. RF mesh remains favored for confined campus networks needing low latency, while satellite backhaul secures data from isolated reservoirs and desert pipelines.

Technology choices now hinge on lifetime economics rather than raw throughput. Utilities often deploy hybrid architectures, running NB-IoT meters downtown and LoRaWAN in suburbs to optimize total cost of ownership. Vendor ecosystems mature accordingly; for instance, Actility partners with meter manufacturers to preload LoRaWAN firmware, trimming integration timelines. This diversification reshapes connectivity spending patterns inside the smart water management market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America generated 27.9% of 2024 revenue, large municipal utilities swiftly issue tenders for meter data management, edge analytics, and cyber-security hardening. Schneider Electric’s plan to inject USD 700 million into US facilities by 2027 reflects expectations of sustained procurement pipelines . Canada’s prairie provinces accelerate leak analytics to counter irrigation-driven withdrawals, while Mexico’s northern states pilot LPWAN networks to reduce theft and illegal tapping. Mature telecom backbones and a deep integrator base minimize deployment risk, reinforcing regional leadership in the smart water management market.

APAC is the fastest-growing territory at 14.3% CAGR, propelled by China’s mandate that every national-level smart city include end-to-end digital water supervision . Provincial grants subsidize cloud platforms that link urban drainage models with real-time rainfall feeds, blending flood prevention with consumption management. Japan’s MLIT catalog hard-codes performance benchmarks, ensuring funding flows only to utilities that deploy interoperable meter-to-analytics stacks . Australia increases desalination reliance and thus prizes early leak detection to lower energy intensity, while India rolls out prepaid meters in drought-prone Madhya Pradesh under public-private partnerships. This policy mosaic keeps the smart water management market on an accelerated trajectory across APAC.

Competitive Landscape

The vendor ecosystem is moderately concentrated. Incumbents such as Xylem, Itron, ABB, Siemens, and Schneider Electric leverage global service fleets and diversified product sets to lock in multi-year contracts. Acquisition remains their preferred path to capability expansion: Badger Meter purchased SmartCover for USD 185 million, folding sewer monitoring into its BlueEdge suite badgermeter.com, while Xylem took a majority stake in Idrica to deepen analytics offerings . These moves elevate platform breadth and raise customer switching costs, consolidating share inside the smart water management market.

Meanwhile, AI-first challengers such as FIDO AI, SewerAI, and Kando have secured funding rounds between USD 10 million and USD 15 million, reflecting investor conviction that machine-learning models will redefine leak detection and wastewater intelligence . Their cloud-native algorithms detect acoustic anomalies or chemical signatures that legacy hardware misses, enabling utilities to prevent bursts before service interruptions. Partnerships bridge incumbents and disruptors: Siemens collaborates with KETOS to embed robotics-sourced sensor data into its SIMATIC platform, marrying operational depth with analytical sophistication.

Smart Water Management Industry Leaders

-

Xylem Inc. (incl. Sensus)

-

Itron Inc.

-

ABB Ltd.

-

ABB Ltd.

-

Schneider Electric SE (+AVEVA)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Veolia acquired CDPQ’s remaining 30% stake in Water Technologies and Solutions for USD 1.75 billion, targeting EUR 90 million in additional synergies by 2027.

- April 2022: Global Omnium, Telefónica Tech, and Google Cloud formed an AI alliance to monitor Mediterranean Posidonia meadows and optimize utility operations.

- March 2025: Daupler raised USD 15 million in Series B funding led by Aqualateral to automate incident response for utilities.

- March 2025: LeakZon secured USD 5 million Series A capital from Peal Holdings to expand its WEAD leak-analytics platform into the US market.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the smart water management market as connected hardware, software, and managed services that collect, transmit, and analyze data from water networks so utilities, industries, and households can detect leaks, cut energy use, and optimize distribution in near-real time.

Scope Exclusions: Conventional treatment equipment that operates without digital sensing or two-way communication is kept outside the boundary.

Segmentation Overview

- By Component

- By Solution

- Enterprise Asset Management

- Distribution Network Monitoring

- Supervisory Control and Data Acquisition (SCADA)

- Meter Data Management (MDM)

- Analytics

- Other Solutions

- By Services

- Professional Services

- Managed Services

- By Solution

- By End User

- Residential

- Commercial

- Industrial / Public Utilities

- By Communication Technology

- Cellular (2G/3G/4G/5G, NB-IoT)

- LPWAN (LoRaWAN, Sigfox)

- RF Mesh / Wi-SUN

- Satellite and Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts next interviewed distribution engineers at municipal utilities across North America, Europe, and Asia Pacific, plus solution integrators and metering OEMs. These conversations confirmed adoption rates, average sensor lifetimes, and service mark-ups that were only partially visible in secondary sources, letting us adjust key assumptions with field insight.

Desk Research

We began by mapping published data from leading open sources such as the United Nations FAO AQUASTAT, the International Water Association, Eurostat's water statistics, and US EPA Smart Utility reports. We then cross-checked infrastructure funding figures from World Bank project sheets. Company 10-Ks, investor decks, and utility tariff filings gave us cost curves and roll-out schedules. Subscriber tools inside D&B Hoovers and Dow Jones Factiva supplied revenue splits for listed meter makers and platform vendors. This list is illustrative; many other public repositories were tapped to fill smaller gaps.

Market-Sizing & Forecasting

A top-down build started with regional water utility spending and non-revenue-water loss values, which are then paired with smart meter penetration ratios, communication module attach rates, and typical annual service charges. Select bottom-up checks, supplier revenue roll-ups and sampled ASP × unit shipments, validated totals. Critical model drivers include leak incidence, utility digitization budgets, IoT module costs, regulatory grant disbursements, and residential billing reforms. Multivariate regression linked these drivers to historic spend, allowing five-year forecasts. Scenario analysis handled policy or climate shocks. Data voids in the bottom-up layer were bridged by calibrated ratios guided by expert interviews.

Data Validation & Update Cycle

Before sign-off, outputs pass anomaly tests and peer review inside Mordor. Material variances trigger re-contact with sources. Models refresh every twelve months, with interim tweaks if major funding, drought, or policy events shift the baseline.

Why Mordor's Smart Water Management Baseline Commands Reliability

Published estimates often differ because studies track unlike scopes, currencies, and refresh cadences. Mordor's disciplined boundary setting, annual refresh, and dual-path modeling keep our numbers dependable for planners.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 18.39 billion (2025) | Mordor Intelligence | - |

| USD 20.08 billion (2025) | Global Consultancy A | Emphasizes meter hardware, lighter on platform and service revenue, limited geographic weighting |

| USD 16.6 billion (2023) | Industry Association B | Older base year, linear escalation, excludes managed services |

| USD 17.53 billion (2025) | Regional Consultancy C | Utility-only scope, omits commercial estates and updates bi-annually |

In sum, Mordor Intelligence roots every figure in clearly stated scope choices, multi-source data, and repeatable checks, giving decision-makers a balanced, transparent baseline they can trace back to public metrics and on-ground voices.

Key Questions Answered in the Report

What is the current size of the smart water management market?

The market is valued at USD 18.39 billion in 2025 and is projected to reach USD 35.25 billion by 2030.

Which component segment grows the fastest?

Services, encompassing professional and managed offerings, is forecast to expand at 16.2% CAGR through 2030.

Why are utilities adopting LPWAN for water metering?

LPWAN delivers 15-year battery life and strong signal penetration, cutting lifetime operating costs compared with high-bandwidth cellular options.

Which region leads revenue and which region grows the fastest?

North America leads with a 27.9% share in 2024, while APAC registers the fastest growth at a 14.3% CAGR.

Page last updated on: