| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 2.21 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Smart Television & Set-Top Box Market Analysis

The Smart Television and Set-Top Box Market is expected to register a CAGR of 2.21% during the forecast period.

The Smart Television and set-top box market is experiencing significant transformation driven by industry consolidation and evolving consumer preferences. The market structure reflects a moderately consolidated landscape, with a few prominent companies controlling over 65% of the Smart TV Market share, including major players like Samsung, LG Electronics, Sony, and TCL. This concentration of market power has intensified competition, leading to accelerated innovation and strategic partnerships among key players to maintain their competitive edge. The industry has witnessed a notable shift in manufacturing strategies, with companies increasingly focusing on localizing production to ensure supply chain resilience and meet regional demand.

The convergence of traditional television and streaming services has become a defining characteristic of the market landscape. According to industry surveys, approximately 35% of industry professionals view set-top boxes as useful but not irreplaceable components in TV operators' propositions, reflecting the evolving nature of content delivery platforms. This transformation is further evidenced by the growing integration of streaming capabilities directly into Smart TVs, with Roku OS emerging as the leading Smart TV operating system in the United States according to NPD's Weekly Retail Tracking Service. The trend has prompted traditional pay-TV operators to adapt their strategies, incorporating OTT services and advanced features into their offerings.

Product innovation and technological advancement continue to reshape the market dynamics, with manufacturers focusing on developing more sophisticated and feature-rich devices. The integration of artificial intelligence, voice control capabilities, and enhanced user interfaces has become standard in premium offerings. Companies are increasingly investing in research and development to introduce advanced features such as 8K resolution, quantum dot technology, and improved gaming capabilities. This focus on innovation has led to the development of more sophisticated products that cater to evolving consumer preferences for seamless, integrated Smart Home Entertainment experiences.

The market is witnessing a significant shift in distribution strategies and retail partnerships. Major manufacturers are expanding their direct-to-consumer channels while maintaining strategic relationships with traditional retailers. The industry has seen an increase in exclusive partnerships between content providers and device manufacturers, creating unique value propositions for consumers. For instance, manufacturers are partnering with streaming services to offer integrated content solutions, while others are developing proprietary platforms to differentiate their offerings. These partnerships have become crucial in creating comprehensive entertainment ecosystems that combine hardware capabilities with content accessibility, further solidifying the role of Connected TV in the Smart TV Industry.

Smart Television & Set-Top Box Market Trends

High Levels of Technological Innovations

The set-top box and smart television market is witnessing significant technological advancements, particularly in artificial intelligence integration and enhanced audio-visual capabilities. The adoption of AI technology has revolutionized both picture quality optimization and voice control functionality, enabling more intuitive content navigation and improved user experiences. For instance, manufacturers are incorporating advanced processors to support heavy applications related to gaming, OTT platforms, and music streaming, ensuring smooth performance and enhanced viewer engagement. The integration of voice-enabled remote controls and AI-powered sound systems, exemplified by partnerships like SK Broadband's collaboration with Bang & Olufsen for AI Sound Max, demonstrates the industry's commitment to innovation.

The emergence of 4K UHD and 8K resolution technologies, coupled with advanced features like HDR (High Dynamic Range) and Dolby Vision support, has transformed the viewing experience. Leading manufacturers are continuously introducing innovative products, as evidenced by Sony Electronics' launch of the BRAVIA XR television series featuring Cognitive Processor XR and Mini LED backlight technology. These innovations extend beyond basic display capabilities to include advanced connectivity options such as Wi-Fi 6 integration, Bluetooth 5.0 compatibility, and enhanced storage capabilities with features like 2GB RAM and 8GB eMMC flash memory in modern set-top boxes. The integration of multiple technologies has enabled manufacturers to offer comprehensive entertainment solutions that combine traditional broadcasting with modern media streaming player capabilities.

Understand The Key Trends Shaping This Market

Download PDF

Growing Adoption in the Emerging Markets

Emerging markets are experiencing unprecedented growth in smart TV and set-top box adoption, driven by increasing internet penetration and the rising popularity of streaming services. The transformation is particularly evident in countries like India, where the market potential is amplified by over 200 million potential TV households that remain underpenetrated. The increasing affordability of smart televisions, coupled with growing consumer preference for internet-connected entertainment devices, has created a robust ecosystem for market expansion. This trend is further supported by the rising adoption of subscription video-on-demand (SVOD) services and the growing demand for high-quality content consumption on larger screens.

The market growth in emerging economies is further catalyzed by strategic partnerships between telecom operators and OTT platforms, creating comprehensive entertainment packages for consumers. For instance, telecommunications companies are increasingly collaborating with local and international OTT platforms to offer bundled services, enhancing the value proposition for consumers. The rural market penetration is showing promising growth, with significant increases in teledensity rates indicating the expanding reach of digital entertainment services. This expansion is complemented by the introduction of affordable smart TV models by various manufacturers, making advanced entertainment technology accessible to a broader consumer base in emerging markets.

Deployment of OS-Based Devices

The deployment of operating system-based devices has emerged as a crucial driver in the smart TV and set-top box market, with Android TV leading the transformation in consumer entertainment devices. The strong demand for Android TV box set-top boxes is attributed to their superior picture and sound quality, combined with seamless access to streaming content and applications. This is evidenced by significant market success stories, such as Sumitomo Electric's BS4K Android TV-powered set-top box achieving remarkable shipment milestones. The operating system's ability to support multiple applications while maintaining smooth performance has made it a preferred choice for both manufacturers and consumers.

The evolution of OS-based devices has enabled manufacturers to offer enhanced customization options and improved user interfaces, making content discovery and navigation more intuitive. Modern OS-based devices support advanced features such as universal search capabilities, voice control integration, and seamless connectivity with other smart home media devices. The integration of app stores, such as Google Play Store, provides users with access to a vast ecosystem of applications and content, while manufacturers continue to innovate with new features like far-field voice technology and improved content recommendation systems. This technological advancement has also facilitated the development of hybrid solutions that combine traditional broadcasting capabilities with modern digital television features, creating a more versatile entertainment platform for consumers.

Segment Analysis: By Technology

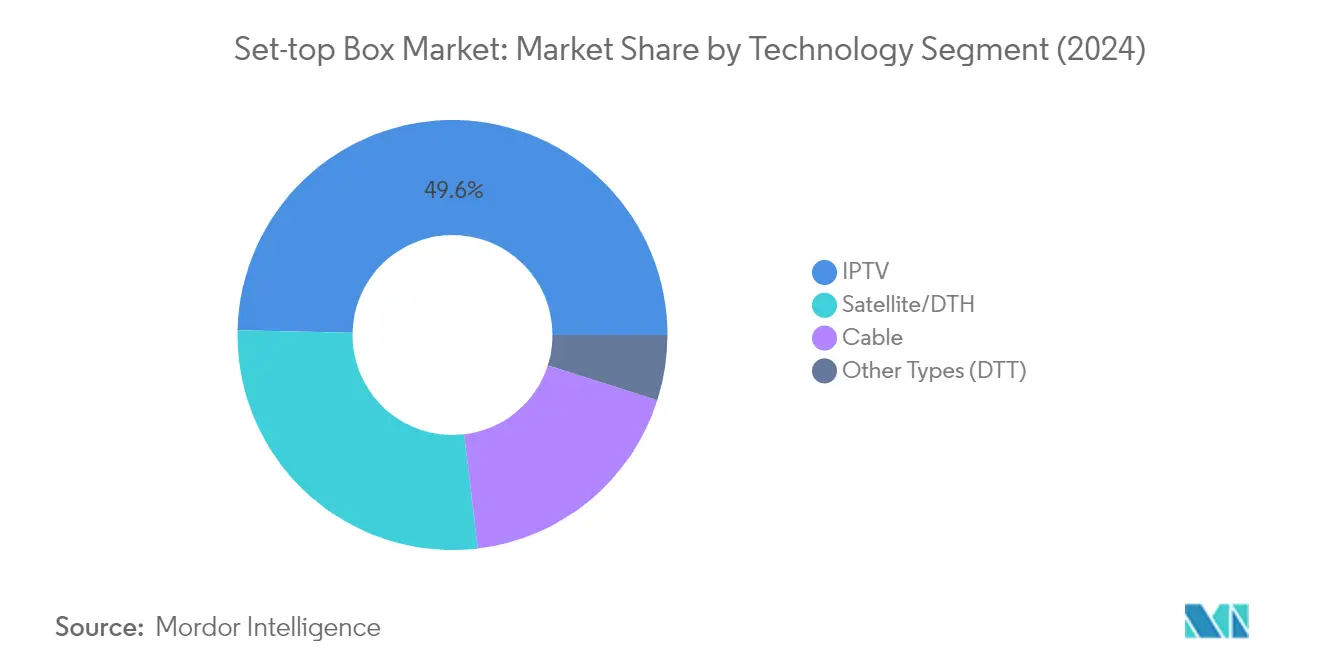

IPTV Segment in Set-top Box Market

The IPTV box segment has emerged as the dominant force in the global set-top box market, commanding approximately 50% market share in 2024. This significant market position is driven by the increasing adoption of internet-based television services and the growing demand for interactive features. IPTV set-top boxes enable seamless integration of traditional television programming with streaming services, providing users with a comprehensive entertainment experience. The segment's growth is further supported by the rising penetration of high-speed internet infrastructure and the increasing consumer preference for on-demand content. Major telecommunications companies and service providers are actively expanding their IPTV offerings, incorporating advanced features such as cloud DVR capabilities, multi-screen viewing, and personalized content recommendations. The segment is also benefiting from technological advancements in video compression and streaming technologies, enabling better quality of service and enhanced user experience.

Remaining Segments in Set-top Box Market Technology

The traditional segments of satellite TV box and cable TV box continue to play important roles in the set-top box market, particularly in regions with limited internet infrastructure. The Satellite/DTH segment maintains its relevance through its ability to reach remote areas and provide consistent service quality regardless of terrestrial infrastructure limitations. Cable set-top boxes remain significant in established markets with extensive cable network infrastructure, though facing increasing competition from IPTV solutions. The Digital Terrestrial Television (DTT) segment, while smaller, serves specific market needs in regions undergoing digital transition, particularly in emerging economies where governments are mandating the switch from analog to digital broadcasting. These segments continue to evolve through the integration of hybrid functionalities, combining traditional broadcasting with internet-based features to stay competitive in the changing media landscape.

Segment Analysis: By Resolution

4K Segment in Smart Television Market

The 4K resolution segment has emerged as the dominant force in the global smart television market, commanding approximately 52% market share in 2024. This substantial market position is driven by the increasing consumer demand for superior picture quality and immersive viewing experiences. The adoption of 4K TVs has been accelerated by the declining prices of these devices, making them more accessible to a broader consumer base. Television manufacturers are actively integrating advanced features like HDR (High Dynamic Range) and wide color gamut (WCG) into their 4K offerings, enhancing the overall viewing experience. The segment's growth is further supported by the expanding availability of 4K content across various streaming platforms and the increasing penetration of high-speed internet connectivity, enabling seamless streaming of high-resolution content.

8K Segment in Smart Television Market

The 8K resolution segment is experiencing remarkable growth in the smart television market, with an expected CAGR of approximately 13% during 2024-2029. This exceptional growth rate is driven by continuous technological advancements in display technology and increasing consumer demand for ultra-high-definition viewing experiences. Major television manufacturers are investing heavily in 8K technology development, introducing innovative features such as advanced AI upscaling capabilities and enhanced processing power. The segment's growth is also supported by the expanding ecosystem of 8K content creation and distribution, particularly in sports broadcasting and gaming applications. The increasing adoption of larger screen sizes, where 8K resolution provides noticeable benefits, is further accelerating the segment's expansion.

Remaining Segments in Resolution Segmentation

The HD/FHD segment continues to maintain a significant presence in the smart television market, particularly in emerging economies and price-sensitive markets. This segment offers a balanced combination of picture quality and affordability, making it an attractive option for budget-conscious consumers. The HD/FHD segment remains relevant in smaller screen sizes where the benefits of higher resolutions are less pronounced. Additionally, the segment serves as an entry point for first-time smart TV buyers and secondary television purchases, supported by the wide availability of HD content across broadcasting and streaming platforms.

Smart Television and Set-Top Box Market Geography Segment Analysis

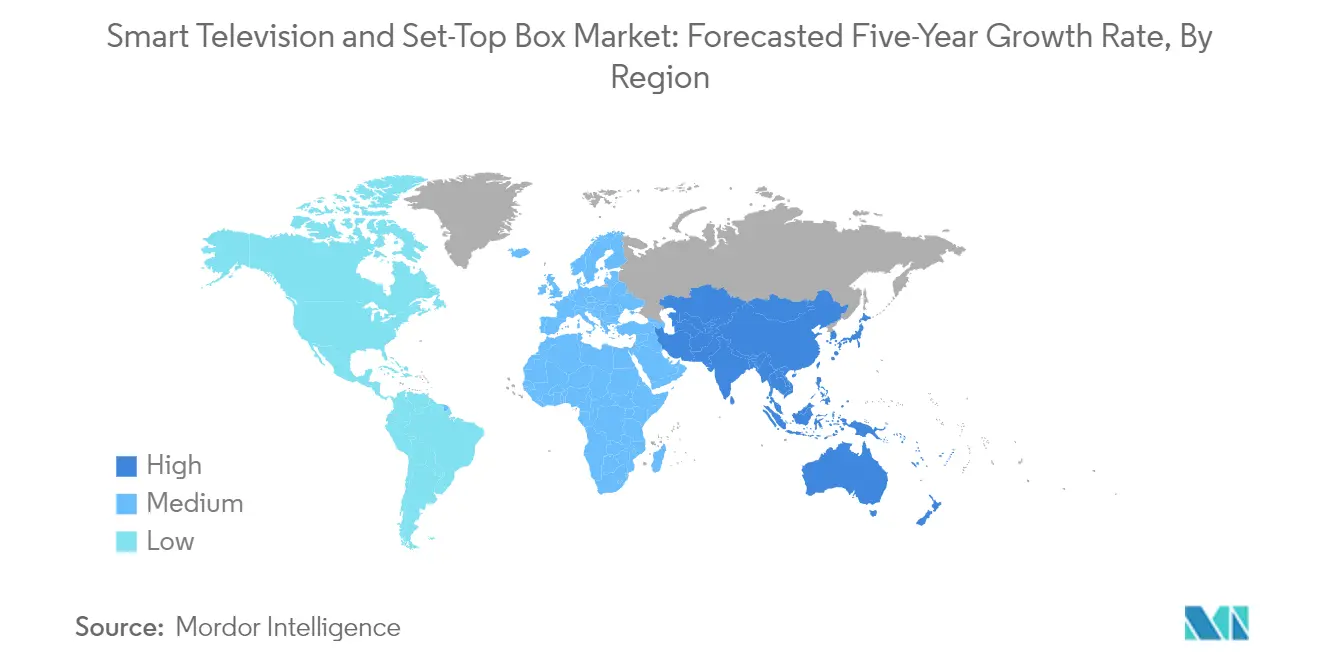

Smart Television and Set-Top Box Market in North America

The North American market continues to be at the forefront of technological adoption in the smart TV and set-top box industry, commanding approximately 22% of the global market share in 2024. The region demonstrates a strong inclination towards advanced features such as gateway abilities, security protocols, and enhanced HD functionality. The increasing consumption of OTT content has emerged as a major market driver, with connected TV manufacturers competing intensely on user interface innovations, content aggregation capabilities, and sophisticated application development. The market is characterized by a high penetration of smart devices and robust payment infrastructure, creating a conducive environment for premium content delivery. Consumer preferences in the region are increasingly shifting towards larger screen sizes and higher resolutions, particularly in the 4K UHD segment. The integration of voice-enabled controls and AI-powered features has become standard offerings, reflecting the region's sophisticated consumer base. The market also shows strong adoption of streaming media devices, with manufacturers focusing on built-in features that eliminate the need for additional set-top boxes.

Smart Television and Set-Top Box Market in Europe

The European market has demonstrated a consistent evolution pattern, recording approximately a 3% decline in market volume from 2019 to 2024. The region exhibits a mature market structure with significant variations across different countries, particularly between Western and Eastern European nations. The market is characterized by strong regulatory frameworks, particularly around energy efficiency and competition standards. Consumer preferences in Europe show a distinct trend towards smart TVs with integrated streaming capabilities, with a growing emphasis on local content delivery platforms. The region's market dynamics are shaped by the increasing adoption of IPTV services and the growing popularity of hybrid broadcast broadband TV (HbbTV) standards. European consumers demonstrate a strong preference for premium viewing experiences, driving demand for advanced display technologies and sophisticated user interfaces. The market also shows significant traction in the development of operator-tier Android TV solutions, reflecting the region's focus on standardized yet customizable platforms. The presence of established manufacturers and strong distribution networks continues to support market stability despite competitive pressures.

Smart Television and Set-Top Box Market in Asia-Pacific

The Asia-Pacific market is projected to experience a marginal decline of approximately 0.4% during the 2024-2029 period, though the region maintains its position as a crucial market for smart TV and set-top box manufacturers. The market landscape is characterized by diverse consumer preferences across different countries, ranging from premium segment demands in developed nations to value-segment requirements in emerging economies. The region demonstrates strong potential in terms of digital transformation initiatives and increasing internet penetration rates. Local manufacturing capabilities and cost-effective production hubs continue to attract global manufacturers to establish their presence in the region. The market shows particular strength in the adoption of Android-based smart TV platforms, with an increasing focus on localized content delivery and regional language support. Consumer preferences are evolving towards larger screen sizes and advanced features, particularly in urban areas. The competitive landscape is marked by the presence of both established global brands and emerging local players, creating a dynamic market environment.

Smart Television and Set-Top Box Market in Rest of the World

The Rest of the World market, encompassing Latin America, the Middle East, and Africa, presents unique opportunities and challenges in the digital television market and set-top box industry. These regions demonstrate varying levels of market maturity and digital infrastructure development, influencing adoption patterns and consumer preferences. The market is characterized by increasing urbanization rates and growing middle-class populations, particularly in major metropolitan areas. Consumer preferences show a strong inclination towards value-for-money propositions, with growing interest in smart entertainment system features and connectivity options. The market demonstrates significant potential for growth in DTH services, particularly in regions with limited broadband infrastructure. Regional content preferences and language requirements play a crucial role in shaping product offerings and marketing strategies. The competitive landscape is marked by strategic partnerships between global manufacturers and local distributors to enhance market penetration and service delivery capabilities. The market shows particular promise in the adoption of hybrid solutions that combine traditional broadcasting with emerging digital platforms.

Get Analysis on Important Geographic Markets

Download PDF

Smart Television & Set-Top Box Industry Overview

Top Companies in Smart Television and Set-Top Box Market

The market features prominent players like Samsung, LG Electronics, TCL, Hisense, and Xiaomi in smart TVs, while ARRIS (CommScope), Technicolor, and ZTE lead in set-top boxes. These companies demonstrate a strong commitment to product innovation through continuous R&D investments in advanced technologies like OLED, QLED, Mini LED displays, and Android TV integration. Operational agility is evident in their rapid adaptation to market demands, particularly in emerging markets where companies are establishing local manufacturing facilities and customizing products for regional preferences. Strategic partnerships with content providers, technology companies, and telecom operators have become crucial for expanding service offerings and market reach. Companies are increasingly focusing on developing integrated smart home ecosystems, incorporating AI capabilities, voice control features, and IoT connectivity to enhance user experience and maintain competitive advantage.

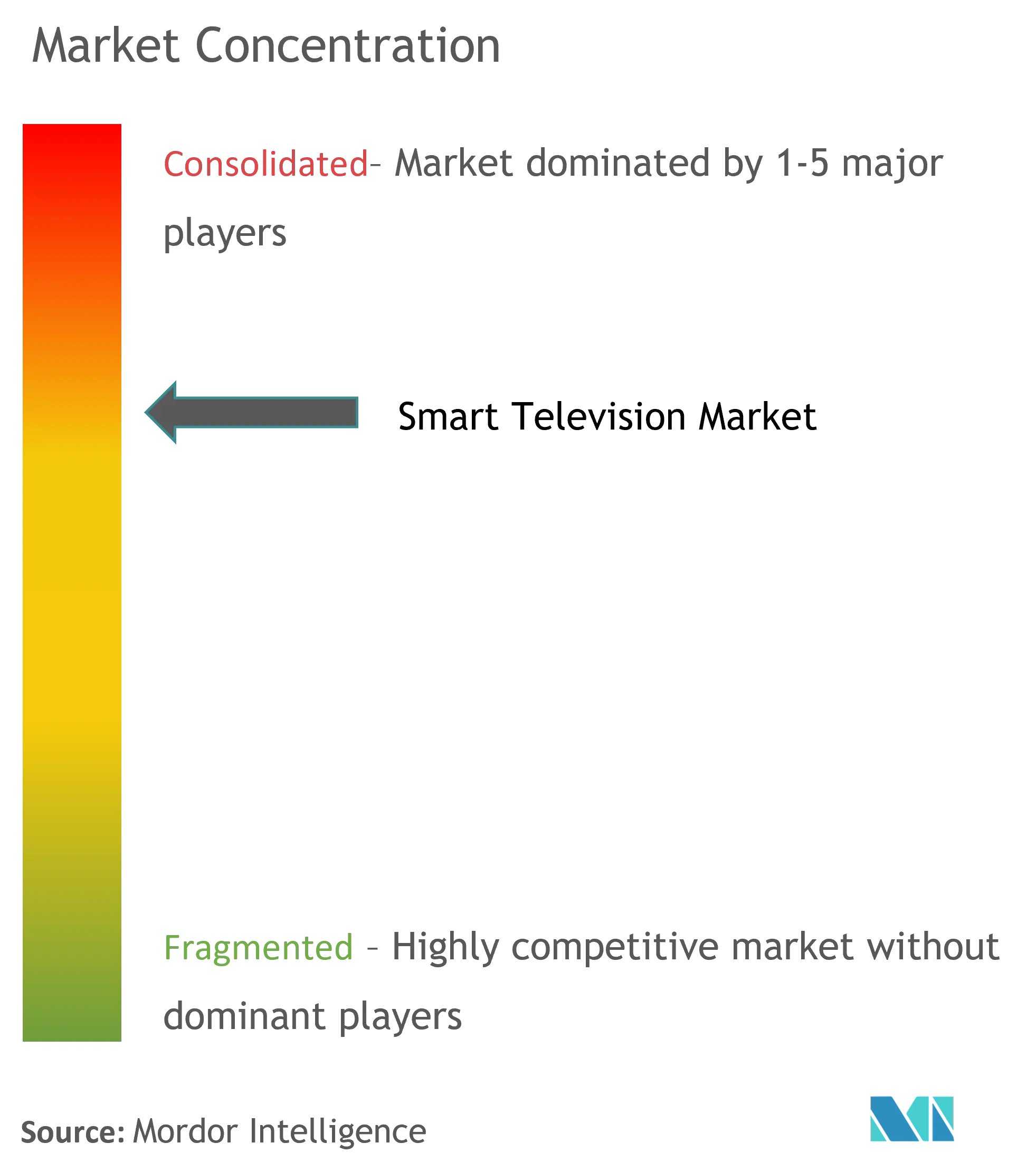

Dynamic Market Structure with Regional Variations

The smart television and set-top box market exhibits a moderately consolidated structure, with global conglomerates dominating the premium segments while regional specialists maintain strong positions in mid-range and entry-level segments. Major electronics manufacturers like Samsung and LG leverage their vertical integration capabilities, controlling everything from component manufacturing to distribution, while Chinese companies like TCL and Hisense have rapidly expanded their global presence through aggressive pricing and technological advancement. The set-top box segment shows higher fragmentation with specialized manufacturers competing alongside diversified technology companies, particularly in emerging markets where digitalization initiatives drive demand.

Market dynamics are characterized by strategic partnerships and collaborations rather than traditional M&A activities, as companies focus on building ecosystem capabilities through technology sharing and content partnerships. Regional variations play a significant role in market structure, with developed markets showing a preference for premium smart TV brands and OTT services, while emerging markets maintain strong demand for traditional set-top boxes alongside growing smart TV adoption. Local manufacturing initiatives and government regulations regarding digital transmission standards have led to increased collaboration between global and local players, creating a complex competitive landscape that varies significantly by region.

Innovation and Adaptability Drive Market Success

Success in this market increasingly depends on companies' ability to balance technological innovation with cost competitiveness while maintaining strong distribution networks and after-sales support. Incumbent players must focus on continuous R&D investment in display technologies, smart features, and user interface improvements while simultaneously optimizing their supply chains to maintain competitive pricing. The ability to create comprehensive ecosystems that integrate various smart home functions and content services has become crucial for maintaining market share, as consumers increasingly seek seamless connectivity and enhanced functionality beyond traditional viewing experiences.

For contenders looking to gain ground, the key lies in identifying and exploiting specific market niches while building strong partnerships with content providers and technology companies. The threat of substitution from mobile devices and streaming services necessitates a focus on value-added features and content integration. Regulatory factors, particularly regarding data privacy, content restrictions, and environmental standards, continue to shape market dynamics and create both challenges and opportunities for market participants. Success in this evolving landscape requires companies to maintain flexibility in their business models while ensuring compliance with varying regional requirements and consumer preferences. The digital media receiver market also plays a role in expanding the range of content delivery options available to consumers.

Smart Television & Set-Top Box Market Leaders

-

Samsung Electronics Co. Ltd

-

LG Electronics Inc.

-

TCL Electronics Holdings Limited

-

Hisense Group

-

Xiaomi Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Smart Television & Set-Top Box Market News

- August 2022 - Samsung announced to launch of Samsung OLED in Australia, thereby expanding its 2022 TV line-up. The TV features over 8 million self-lit pixels partnered with Quantum Dot Technology that can deliver brighter, more accurate highlights and realistic colors.

- February 2022 - ZTE Corporation, a major international provider of telecommunications, enterprise and consumer technology solutions for the mobile internet, announced that it will launch a new-generation 5G media gateway set-top box (STB) ZXV10 B960GV1 powered by Android TV at the upcoming Mobile World Congress (MWC) 2022 in Barcelona, Spain.

- September 2021 - Technicolor deployed next-generation Android TV set-top boxes (STBs) for TIM to provide Italian households with access to premium services offered by broadcasters and over-the-top (OTT) providers, including Netflix, Amazon, Infinity, Disney+, and DAZN. The STBs are based upon Technicolor Connected Home's JADE platform, which includes Wi-Fi 6 and Android 10, as well as ready-to-add-on accessories such as personal video recorders or far-field voice. As part of this deployment, Technicolor Connected Home will also roll out a software upgrade to enable access to new services for existing customers in TIM's current installed base.

Smart Television & Set-Top Box Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study (Set-top Box Market)

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Market

-

4.5 Technology Snapshot

- 4.5.1 Evolution of Set-top Boxes

- 4.5.2 Key Collaborations

- 4.5.3 Ongoing Technological Developments

5. MARKET DYNAMICS

-

5.1 Drivers

- 5.1.1 High Levels of Technological Innovations

- 5.1.2 Growing Adoption In The Emerging Markets

- 5.1.3 Deployment Of OS-based Devices

-

5.2 Restraints

- 5.2.1 Growing Production Costs and Vendor Consolidation

6. SET-TOP BOX MARKET SEGMENTATION

-

6.1 By Technology

- 6.1.1 Satellite/DTH

- 6.1.2 IPTV

- 6.1.3 Cable

- 6.1.4 Other Types (DTT)

-

6.2 By Resolution

- 6.2.1 SD

- 6.2.2 HD

- 6.2.3 Ultra-HD And Higher

-

6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Rest of the World

7. TELEVISION MARKET SEGMENTATION

-

7.1 By Resolution

- 7.1.1 HD/FHD

- 7.1.2 4K

- 7.1.3 8K

-

7.2 By Display Size (in Inches)

- 7.2.1 32 And Below

- 7.2.2 39-43

- 7.2.3 48-50

- 7.2.4 55-60

- 7.2.5 65 And Above

-

7.3 By Technology

- 7.3.1 LCD

- 7.3.2 OLED

- 7.3.3 QLED

-

7.4 By Geography

- 7.4.1 North America

- 7.4.2 Europe

- 7.4.3 Asia Pacific

- 7.4.4 Rest of the World

8. VENDOR MARKET SHARE ANALYSIS

- 8.1 Vendor Market Share - Set-top Box Market

- 8.2 Vendor Market Share - Smart Television Market

9. COMPETITIVE LANDSCAPE

-

9.1 Company Profiles - Set-top Box

- 9.1.1 Arris International PLC (commscope Holding Company, Inc)

- 9.1.2 Technicolor SA

- 9.1.3 Intek Digital Inc.

- 9.1.4 Humax Holdings CO. Ltd

- 9.1.5 ZTE Corporation

- 9.1.6 Shenzhen Skyworth Digital Technology CO., Ltd

- 9.1.7 Sagemcom SAS

- 9.1.8 Gospell Digital Technology CO. Limited

- 9.1.9 Kaonmedia CO. Ltd

- 9.1.10 Shenzhen Coship Electronics CO. Ltd

- 9.1.11 Evolution Digital LLC

- 9.1.12 Shenzhen SDMC Technology CO. Ltd

-

9.2 Company Profiles - Smart Television

- 9.2.1 Samsung Electronics CO., Ltd

- 9.2.2 LG Electronics Inc.

- 9.2.3 TCL Electronics Holdings Limited

- 9.2.4 Hisense Group

- 9.2.5 Xiaomi Corporation

10. INVESTMENT ANALYSIS

11. FUTURE OF THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Smart Television & Set-Top Box Industry Segmentation

The scope of the study focuses on the market analysis of Smart TVs and Set-top Boxes across the globe, and market sizing encompasses the revenue generated by these products sold by various market players. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyzes the overall impact of COVID-19 on the ecosystem. The report's scope encompasses market sizing and forecast for technology, Resolution, and geography segmentation for the Set-top box market. The report's scope also encompasses market sizing and forecast for Resolution, Display Size, Technology, and Geography for the Smart TV Market.

| By Resolution | HD/FHD |

| 4K | |

| 8K | |

| By Display Size (in Inches) | 32 And Below |

| 39-43 | |

| 48-50 | |

| 55-60 | |

| 65 And Above | |

| By Technology | LCD |

| OLED | |

| QLED | |

| By Geography | North America |

| Europe | |

| Asia Pacific | |

| Rest of the World |

Need A Different Region or Segment?

Customize Now

Smart Television & Set-Top Box Market Research FAQs

What is the current Smart Television and Set-Top Box Market size?

The Smart Television and Set-Top Box Market is projected to register a CAGR of 2.21% during the forecast period (2025-2030)

Who are the key players in Smart Television and Set-Top Box Market?

Samsung Electronics Co. Ltd, LG Electronics Inc., TCL Electronics Holdings Limited, Hisense Group and Xiaomi Corporation are the major companies operating in the Smart Television and Set-Top Box Market.

Which is the fastest growing region in Smart Television and Set-Top Box Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Smart Television and Set-Top Box Market?

In 2025, the Asia-Pacific accounts for the largest market share in Smart Television and Set-Top Box Market.

What years does this Smart Television and Set-Top Box Market cover?

The report covers the Smart Television and Set-Top Box Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Smart Television and Set-Top Box Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Smart Television and Set-Top Box Market Research

Mordor Intelligence provides a comprehensive analysis of the smart tv and digital television landscape. We leverage our extensive expertise in connected tv technologies and smart home entertainment systems. Our detailed research covers the entire ecosystem. This includes android tv box solutions and IPTV box implementations. We offer deep insights into digital tv box technologies and streaming media player innovations. The report examines emerging trends in OTT box development and internet tv box adoption. It also explores the evolution of digital media player technologies across global markets.

Stakeholders gain valuable insights through our analysis of streaming device adoption patterns and cable tv box integration within connected home device ecosystems. The report, available as an easy-to-download PDF, explores the transformation of television streaming device technologies and their impact on smart home media consumption. Our research encompasses satellite tv box systems and digital media receiver innovations. It also identifies emerging trends in the smart entertainment system space, providing actionable intelligence for industry participants. The analysis covers both established players in the digital television industry and innovative startups disrupting the smart tv market. It offers comprehensive insights into market dynamics and growth opportunities.