Smart Kitchen Market Size

| Study Period | 2019 - 2029 |

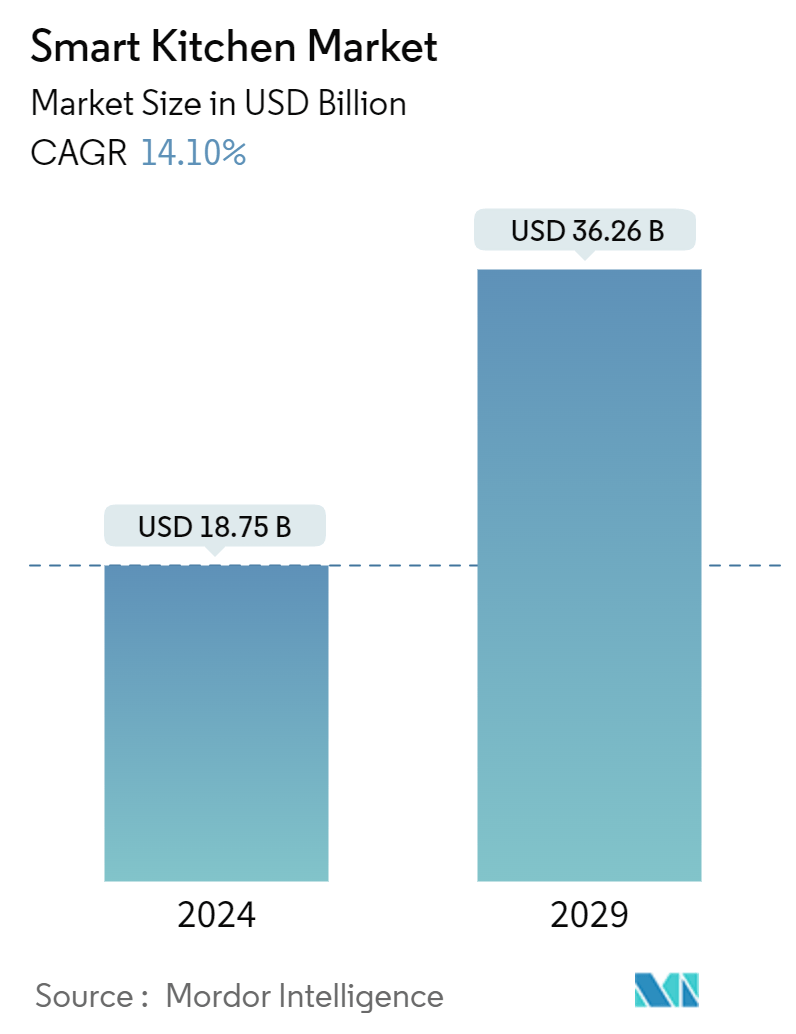

| Market Size (2024) | USD 18.75 Billion |

| Market Size (2029) | USD 36.26 Billion |

| CAGR (2024 - 2029) | 14.10 % |

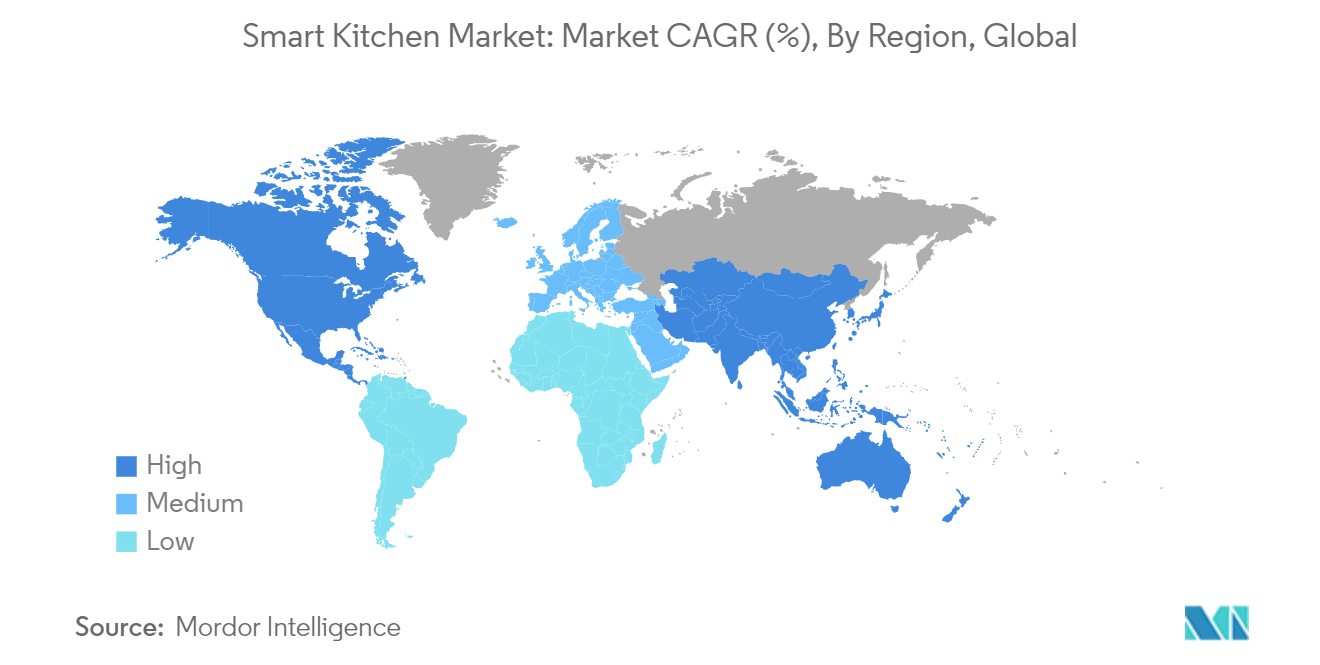

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Smart Kitchen Market Analysis

The Smart Kitchen Market size is estimated at USD 18.75 billion in 2024, and is expected to reach USD 36.26 billion by 2029, growing at a CAGR of 14.10% during the forecast period (2024-2029).

- Smart kitchen appliances and devices prioritize energy efficiency, outpacing their traditional counterparts. With features like smart sensors, energy-efficient compressors, and advanced power management systems, these appliances not only optimize energy usage but also contribute to reduced electricity bills and a diminished carbon footprint. As awareness grows, both consumers and businesses are actively pursuing these energy-efficient solutions to lessen their environmental impact.

- Many smart kitchen solutions are equipped with features that promote responsible waste separation and disposal. These innovations, such as smart trash cans with automated sorting and connections to municipal waste management systems, actively encourage users to recycle and manage kitchen waste responsibly.

- Government regulations and policies in certain regions are promoting the use of energy-efficient and eco-friendly kitchen appliances, boosting the demand for smart kitchen solutions. Over the next three years, the Bureau of Energy Efficiency (BEE) plans to mandate energy labeling for products like LPG stoves, microwave ovens, and induction hobs, which were previously voluntary. According to the BEE’s impact assessment report, energy efficiency measures led to substantial consumer savings of INR 54,323 crore (~USD 6.6 billion) in the fiscal year 2022-23.

- As urban areas become increasingly populated, the global trend of rapid urbanization is driving the demand for smart kitchen solutions. Urban dwellers, being diverse and health-conscious, are turning to smart kitchen technologies. These technologies offer personalized recipe recommendations, track ingredients, and automate cooking, catering to specialized dietary needs. Consequently, solutions that assist with meal planning, ingredient management, and customized cooking are witnessing heightened interest in urban locales.

- The intricate electronic components, sensors, and connectivity features of smart kitchen appliances often come with high repair or replacement costs. Moreover, specialized replacement parts for these devices might not only be scarce but also pricier than their standard counterparts. Such factors contribute to elevated maintenance expenses, potentially deterring consumers wary of the long-term financial commitment of owning and maintaining smart kitchen appliances.

- The fluctuating inflation rate escalates the costs associated with raw materials, components, and manufacturing processes for smart kitchen appliances and devices. As production costs surge, manufacturers find themselves under pressure, often compelled to transfer these increased expenses to consumers through price hikes. Similarly, retailers grapple with heightened procurement and operational costs, which could either inflate prices for consumers or squeeze profit margins.

Smart Kitchen Market Trends

Residential End-User Segment is Expected to Hold Significant Market Share

- Homeowners are turning to smart kitchen technologies for enhanced convenience, efficiency, and personalization in their cooking and food preparation. Residential consumers are increasingly favoring features such as voice-controlled appliances, automated meal planning, and recipe recommendation systems. These innovations promise a more seamless and tailored cooking experience. For instance, a smart oven that preheats and adjusts cooking times based on user preferences significantly streamlines meal preparation for busy households.

- Smart home technologies, including voice assistants, home automation platforms, and connected devices, are propelling the adoption of smart kitchen appliances in residential settings. Consumers are keen on embedding their kitchen appliances into the larger smart home ecosystem, facilitating centralized control, monitoring, and automation of diverse household functions. For example, a smart refrigerator that interacts with a home's voice assistant to update a shopping list or place grocery orders resonates with homeowners aiming for streamlined household management.

- Further, as individuals grow older, they frequently encounter physical and cognitive hurdles, making conventional kitchen appliances and tools harder to navigate. These challenges include diminished mobility, reduced dexterity, and waning cognitive abilities. Smart kitchen technologies equipped with voice-controlled interfaces, automated functionalities, and tailored settings significantly boost accessibility for seniors. This advancement empowers older adults to maintain their independence in cooking and other kitchen activities.

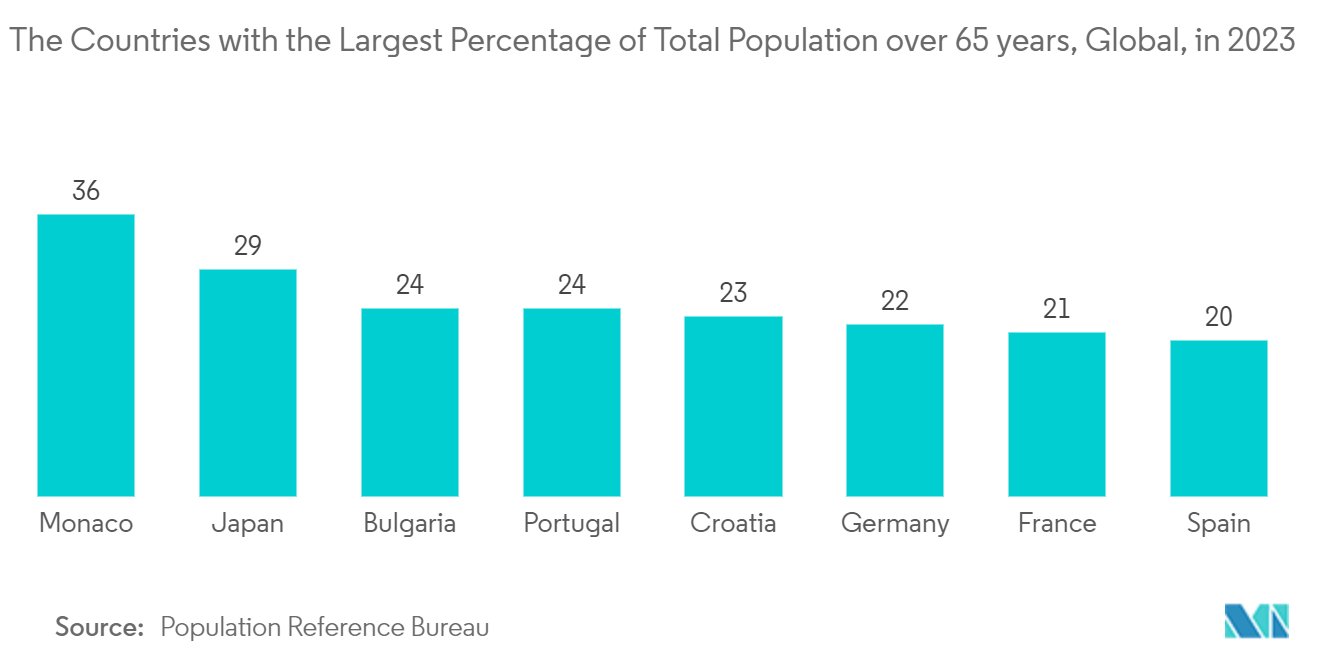

- According to the Population Reference Bureau, in 2023, Monaco led developed countries with 36% of its population aged 65 and older. Japan followed with 29%, while Portugal and Bulgaria each had 24%. The increasing elderly population, along with a rise in disabilities, is expected to drive demand for smart kitchen technologies. These technologies enhance accessibility and promote independent living for homeowners. Consequently, this segment of the residential market is expected to drive further growth and innovation in the smart kitchen technology sector.

North America is Expected to Hold Significant Market Share

- North America's affluent consumers, particularly in the United States, boast significant disposable incomes. This financial capability drives their preference for premium, innovative, and tech-savvy kitchen appliances and smart home solutions, all aimed at enhancing their convenience. For instance, data from BEA highlights a surge in US personal income, at USD 22,952 billion, underscoring the robust purchasing power available for smart kitchen investments. This elevated purchasing power facilitates a quicker adoption of smart kitchen technologies among North American consumers.

- North America boasts a concentration of top-tier home appliance and smart kitchen manufacturers, including industry giants like GE Appliances, Whirlpool, etc. These companies are in charge of crafting and rolling out cutting-edge smart kitchen products, directly addressing the surging consumer appetite in the region. Their established presence and brand clout in North America significantly bolster the uptake and integration of smart kitchen solutions.

- In the United States, a favorable regulatory landscape fosters the growth and acceptance of smart kitchen technologies. Programs like Energy Star, championing energy-efficient appliances, have heightened consumer interest in smart kitchen solutions that prioritize energy efficiency and sustainability. Government rebates and incentives for energy-efficient home upgrades, encompassing smart kitchen appliances, further motivate consumers. For example, in April 2024, the Inflation Reduction Act introduced rebates for new electric appliances, such as cooktops, ranges, and wall ovens, underscoring potential savings for consumers replacing kitchen appliances.

- In addition, the region's tech-savvy population quickly adopts new technologies, including smart home devices and appliances. This readiness propels a growing demand for innovative smart kitchen solutions, particularly in urban and suburban areas. Consumers are increasingly prioritizing convenience, efficiency, and time-saving features in their kitchen choices. Technologies like connected ovens, refrigerators, and dishwashers cater to this demand, offering features such as remote control, automated scheduling, and enhanced energy management. This push for a more streamlined and advanced kitchen experience is propelling the adoption of smart kitchen solutions across North America.

Smart Kitchen Industry Overview

The smart kitchen market is highly competitive, with several global and local industry players. These significant players are establishing their positions by extending their product portfolios. In addition, they opt for strategic initiatives like partnerships and collaborations to remain competitive. Some of the key players in the market are Electrolux, LG Electronics, Samsung Electronics, Haier Inc. (GE Appliances), and Whirlpool Corporation.

- April 2024: Samsung Electronics America Inc. unveiled new 4-Door Flex refrigerator models and a revamped line of premium slide-in ranges, including the Bespoke Slide-in Induction Range, as part of its expanded Bespoke kitchen appliance portfolio. These latest offerings uphold Bespoke's tradition of elegant design and cutting-edge features and introduce AI-driven technology, simplifying meal planning and cooking. The new models boast interchangeable door panels customizable in 11 colors and two finishes and are available in Stainless Steel or White Glass.

- February 2024: At the 2024 Kitchen & Bath Industry Show, LG Electronics unveiled its latest lineup of kitchen appliances, seamlessly integrating intelligent functionality and sleek design. LG's 29-cubic-foot Smart InstaView Standard-Depth MAX 4-Door French Door Refrigerator with the new MyColor feature and Full-Convert Drawer (models LF29S8365 and LH29S8365) makes a colorful design statement. LG STUDIO Essence White products offer a timeless look with a matte-white finish, and the 1.3-cubic-foot Smart Low-Profile Over-the-Range Microwave (MVEF1337F) boasts a sleek low-profile design with maximum interior height for tall items.

Smart Kitchen Market Leaders

-

Electrolux

-

LG Electronics

-

Samsung Electronics

-

Haier Inc. (GE Appliances)

-

Whirlpool Corporation

*Disclaimer: Major Players sorted in no particular order

Smart Kitchen Market News

- January 2024: At CES 2024, Fresco and Panasonic unveiled their broadened collaboration. These two industry frontrunners are set to introduce a groundbreaking AI-driven cooking assistant for Panasonic's kitchen devices, kicking off with the HomeCHEF 4-in-1 multi-oven. Integrated within the Panasonic app, Fresco's AI assistant empowers home chefs to tailor recipes to their dietary needs, swap ingredients based on pantry stock, and effortlessly modify serving sizes and cooking parameters.

- August 2023: GE Appliances (GEA), a subsidiary of Haier, and Google Cloud unveiled an expansion of their collaboration, aiming to elevate and tailor consumer experiences through generative AI. GEA's SmartHQ consumer app introduces a novel feature, Flavorly AI, enabling users to craft personalized recipes based on their kitchen ingredients, leveraging Google Cloud's Vertex AI platform. The SmartHQ Assistant, an AI-driven conversational interface, will leverage Google Cloud's generative AI to respond to questions about the operation and upkeep of connected home appliances.

Smart Kitchen Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Threat of New Entrants

4.2.2 Bargaining Power of Buyers

4.2.3 Bargaining Power of Suppliers

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

4.4 An Assessment of Macroeconomic Trends on the Market

4.5 Technology Snapshot (Wi-Fi-enabled, Bluetooth-enabled, etc.)

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Awareness toward Energy-Efficiency and Environmental Impact Drives the Market Demand

5.1.2 Surge in Urban Population and Interest toward Convenient Lifestyle Drives the Market Growth

5.2 Market Restraints

5.2.1 High Initial Cost of Smart Kitchen Appliances with High Cost of Maintenance

5.2.2 Privacy and Security Concerns

6. MARKET SEGMENTATION

6.1 By Product Type

6.1.1 Smart Refrigerators

6.1.2 Smart Oven

6.1.3 Smart Dishwashers

6.1.4 Smart Cooktops

6.1.5 Other Product Types

6.2 By End-user Industry

6.2.1 Residential

6.2.2 Commercial

6.3 By Geography***

6.3.1 North America

6.3.2 Europe

6.3.3 Asia

6.3.4 Australia and New Zealand

6.3.5 Latin America

6.3.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 Dacor Holdings Inc.

7.1.2 Electrolux

7.1.3 LG Electronics

7.1.4 Samsung Electronics

7.1.5 Haier Inc. (GE Appliances)

7.1.6 Panasonic Corporation

7.1.7 Whirlpool Corporation

7.1.8 Miele & Cie. KG

7.1.9 Groupe SEB

7.1.10 BSH Hausgeräte GmbH

7.1.11 Midea Group

7.1.12 Frigidaire

7.1.13 Liebherr Group

7.1.14 Brava Home Inc.

7.1.15 Spinn Inc.

7.1.16 Tovala

7.1.17 Meater (Apption Labs Limited)

7.1.18 Cosori

7.1.19 COWAY CO. LTD

7.1.20 Gourmia Inc.

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

Smart Kitchen Industry Segmentation

A smart kitchen leverages advanced technology and automation to enhance the cooking experience. This entails utilizing connected appliances and devices, often powered by artificial intelligence, which can be remotely controlled. A smart kitchen can range from a fully automated system that cooks meals and cleans up afterward to one equipped with smart appliances like smart fridges and smart cookers. The study monitors the revenue from selling internet, Wi-Fi, or Bluetooth-connected kitchen appliances seamlessly integrating into smart homes. The study also tracks the growth trends and macroeconomic factors impacting the market.

The smart kitchen market segments its offerings by product type (smart refrigerators, smart ovens, smart dishwashers, smart cooktops, and other product types), end-user industry (residential and commercial), and geography (North America, Europe, Asia, Australia and New Zealand, Latin America, and the Middle East and Africa). This report provides market forecasts and valuations (USD) for each segment.

| By Product Type | |

| Smart Refrigerators | |

| Smart Oven | |

| Smart Dishwashers | |

| Smart Cooktops | |

| Other Product Types |

| By End-user Industry | |

| Residential | |

| Commercial |

| By Geography*** | |

| North America | |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Smart Kitchen Market Research FAQs

How big is the Smart Kitchen Market?

The Smart Kitchen Market size is expected to reach USD 18.75 billion in 2024 and grow at a CAGR of 14.10% to reach USD 36.26 billion by 2029.

What is the current Smart Kitchen Market size?

In 2024, the Smart Kitchen Market size is expected to reach USD 18.75 billion.

Who are the key players in Smart Kitchen Market?

Electrolux, LG Electronics, Samsung Electronics, Haier Inc. (GE Appliances) and Whirlpool Corporation are the major companies operating in the Smart Kitchen Market.

Which is the fastest growing region in Smart Kitchen Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Smart Kitchen Market?

In 2024, the North America accounts for the largest market share in Smart Kitchen Market.

What years does this Smart Kitchen Market cover, and what was the market size in 2023?

In 2023, the Smart Kitchen Market size was estimated at USD 16.11 billion. The report covers the Smart Kitchen Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Smart Kitchen Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Smart Kitchen Industry Report

Statistics for the 2024 Smart Kitchen market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Smart Kitchen analysis includes a market forecast outlook for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

Smart Kitchen Market Report Snapshots