| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 389.14 Billion |

| Market Size (2030) | USD 619.34 Billion |

| CAGR (2025 - 2030) | 9.74 % |

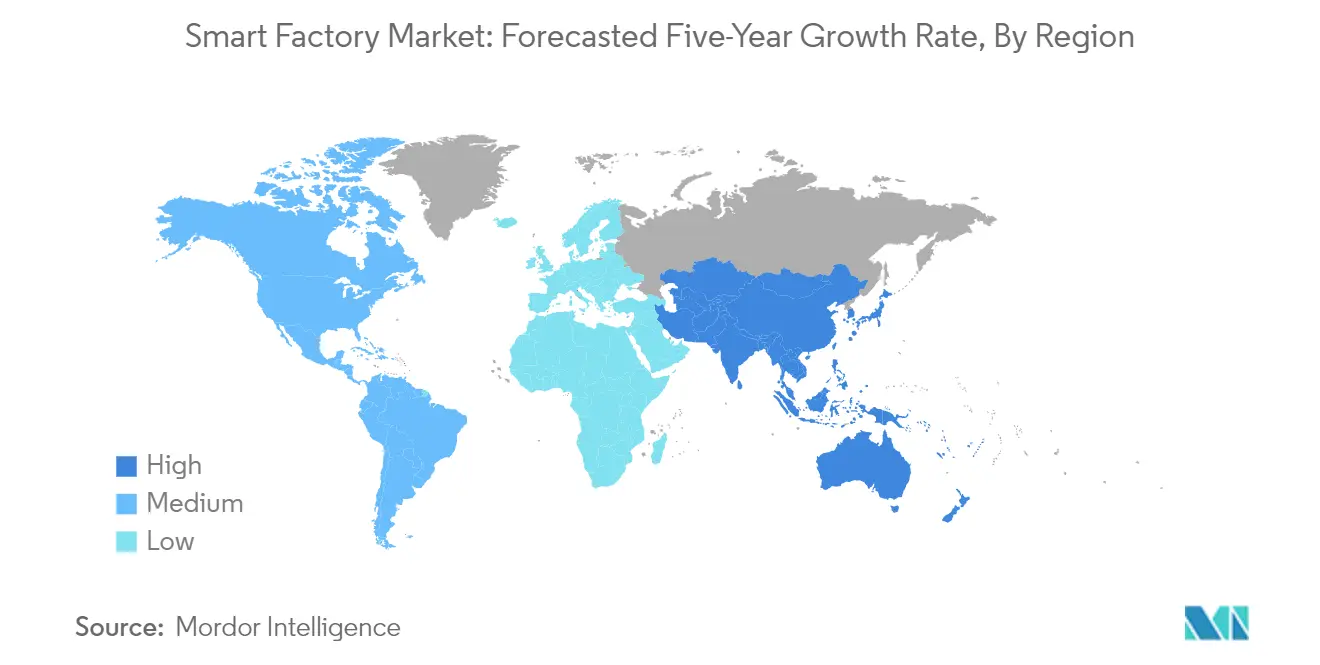

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

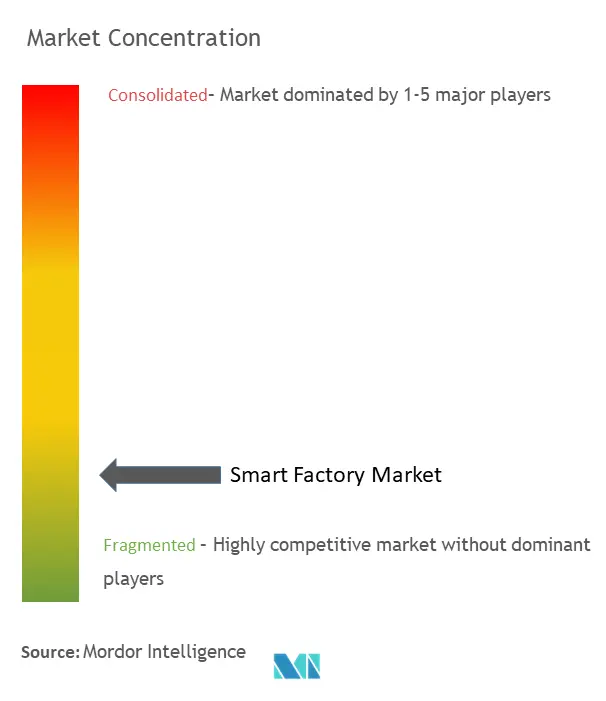

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Smart Factory Market Analysis

The Smart Factory Market size is estimated at USD 389.14 billion in 2025, and is expected to reach USD 619.34 billion by 2030, at a CAGR of 9.74% during the forecast period (2025-2030).

The smart factory landscape is undergoing a fundamental transformation driven by Industry 4.0 initiatives and the increasing integration of advanced technologies across manufacturing processes. Industrial system architects, integrators, and machine builders are leveraging advances in connected computing to help manufacturing facilities function more efficiently through research and development. According to estimates from Maryville University, by 2025, over 180 trillion gigabytes of data will be created worldwide annually, with a significant portion generated by IIoT-enabled industries. This massive volume of data is enabling manufacturers to refine complex processes and manage supply chains more effectively through advanced analytics and machine learning capabilities.

The convergence of artificial intelligence, machine learning, and automation technologies is revolutionizing traditional manufacturing methods. Manufacturing companies are increasingly adopting AI-enabled smart cameras and sensors to improve safety, quality, and operator efficiency. These technologies are replacing inefficient, labor-intensive operations with greater reliability and productivity. A survey by Industrial IoT company Microsoft Corporation found that 85% of companies have at least one IIoT use case project, with approximately 95% of respondents having implemented IIoT strategies by 2022, demonstrating the rapid pace of technological adoption.

The manufacturing sector is witnessing significant advancements in robotics and industrial automation capabilities, particularly in quality control and inspection processes. Machine vision systems equipped with AI algorithms are being deployed for defect identification, ensuring product quality, avoiding mix-ups during packaging, verifying labeling print, and performing color recognition. These systems are particularly crucial in industries such as pharmaceuticals, automotive, and electronics manufacturing, where precision and consistency are paramount. The integration of collaborative robots (cobots) with advanced sensing capabilities is enabling safer human-robot interactions and more flexible manufacturing processes.

The evolution of smart factories is driving a fundamental shift in workforce requirements and skill development. The traditional engineering skillset lifecycle has compressed from 15 years to 3-5 years, necessitating continuous upskilling to keep pace with technological advancement. According to Cisco's projections, machine-to-machine (M2M) connections supporting Industrial IoT applications now account for more than half of the world's 28.5 billion connected devices, highlighting the growing importance of digital literacy and technical expertise in manufacturing operations. This transformation is creating new roles focused on data analytics, robotics maintenance, and systems integration, while traditional manufacturing jobs are being augmented with digital tools and automation support.

Smart Factory Market Trends

Growing Adoption of Internet of Things (IoT) Technologies Across the Value Chain

The industrial landscape is witnessing a transformative shift with the widespread adoption of Internet of Things (IoT) technologies across manufacturing value chains. According to Maryville University estimates, by 2025, over 180 trillion gigabytes of data will be created worldwide annually, with a significant portion generated by Industrial IoT (IIoT)-enabled industries. This massive data generation is enabling manufacturers to leverage real-time monitoring, predictive maintenance, and advanced analytics to optimize their production processes. A survey by Industrial IoT giant Microsoft Corporation revealed that 85% of companies have at least one IIoT use case project, with 94% of respondents planning to implement IIoT strategies, demonstrating the growing confidence in industrial IoT technologies.

The integration of IoT in smart factory environments is revolutionizing traditional manufacturing methods through enhanced connectivity and data utilization. For instance, Panasonic's launch of the Miraie Profactory platform, an Industrial IoT/Smart Factory solution, demonstrates how manufacturers are leveraging IoT to digitize factory operations. These smart factory solutions are helping businesses optimize production efficiency, improve quality control, diagnose issues more effectively, and reduce downtime through real-time monitoring and analytics. The Semiconductor Industry Association reported that semiconductor sales reached USD 580.13 billion worldwide in 2022, with a year-on-year growth rate of 4.4%, indicating the growing demand for IoT-enabled smart manufacturing solutions that rely heavily on semiconductor components.

Understand The Key Trends Shaping This Market

Download PDF

Rising Demand for Energy Efficiency

The increasing focus on energy efficiency has become a crucial driver for smart factory adoption, as manufacturers seek to optimize their operations while reducing environmental impact. According to the Victorian Government's Compressed Air System Guide, compressed air alone accounts for 10% of industrial power usage across Australian industrial sectors, while the manufacturing industry as a whole accounts for 18% of the country's energy consumption. This significant energy usage has prompted manufacturers to implement smart factory solutions that can monitor and optimize energy consumption in real-time. The implementation of international standards on Environmental Management Systems (EMSs), particularly the ISO 50001 standard, has shown that companies can achieve initial energy savings of 10% or more through factory digitalization.

The European Commission's 2030 Energy Strategy has set ambitious targets, including achieving energy efficiency improvements of 30%, a 40% reduction in greenhouse gas emissions compared to 1990 levels, and ensuring at least 27% energy savings. These regulatory pressures, combined with the potential for substantial cost savings, are driving manufacturers to invest in industrial automation technologies. The U.S. Department of Energy's findings indicate that energy management efforts by large American manufacturers have saved nearly USD 2.4 billion in the past five years, demonstrating the significant financial benefits of implementing smart energy management systems. Industrial automation in smart factories is incorporating advanced technologies such as IEEE's new Wi-Fi standard 802.11ax, which uses both 2.4GHz and 5.0GHz wireless frequencies to provide better access points with greater capacity and improved energy efficiency over previous Wi-Fi standards.

Segment Analysis: By Product

Sensors Segment in Smart Factory Market

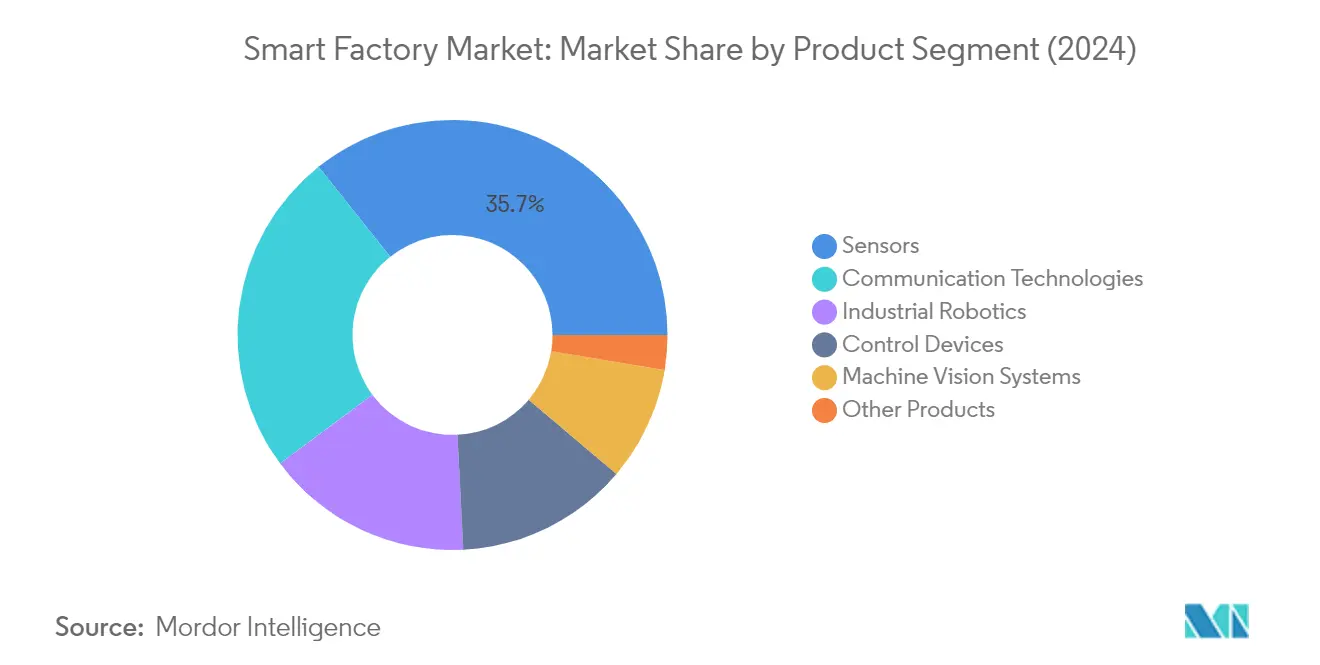

The sensors segment dominates the smart factory market, commanding approximately 36% market share in 2024, driven by the increasing adoption of IoT technologies across manufacturing value chains. These sensors play a crucial role in monitoring manufacturing conditions, with major companies like Royal Dutch Shell deploying over 50,000 sensors in single facilities to generate hundreds of thousands of measurements per minute for equipment and operating conditions monitoring. The segment's dominance is further strengthened by the growing implementation of proximity sensors in robotics applications, particularly in the automotive sector, where they are essential for determining the exact relative placement of products and automated robot operations.

Machine Vision Systems Segment in Smart Factory Market

The machine vision systems segment is projected to witness the highest growth rate of approximately 13% during 2024-2029, driven by increasing demand for quality inspection and automated manufacturing processes. This growth is supported by continuous technological advancements in cameras, processors, and machine vision software, enabling more sophisticated applications in automated assembly systems. The segment's expansion is further fueled by the integration of artificial intelligence and deep learning capabilities, allowing for more complex inspection tasks and improved decision-making capabilities in manufacturing processes. The adoption of AI-enabled smart cameras is particularly accelerating, as they help improve safety, quality, and operator efficiency while enabling automated monitoring and inspection in hazardous environments.

Remaining Segments in Smart Factory Market by Product

The other significant segments in the smart factory market include communication technologies, industrial robotics, and control devices, each serving distinct but complementary functions in industrial automation. Communication technologies facilitate seamless data exchange and network connectivity, while industrial robotics focus on automated manufacturing processes through various robot types including articulated, cartesian, and collaborative robots. Control devices, including relays, switches, and servo motors, provide the fundamental control mechanisms for automated systems. These segments collectively contribute to the comprehensive automation ecosystem required for modern smart factories, with each playing a vital role in enabling efficient, flexible, and intelligent manufacturing operations.

Segment Analysis: By Technology

Product Lifecycle Management (PLM) Segment in Smart Factory Market

The Product Lifecycle Management (PLM) segment dominates the smart factory technology market, holding approximately 33% market share in 2024. PLM's prominence stems from its crucial role in streamlining resources throughout the product manufacturing cycle by consolidating production information efficiently and cost-effectively. The software system enables enterprises to manage information through the entire lifecycle of products, offering features like data quality management, enterprise product record, enterprise visualization, customer need management, product cost and quality management, and materials and equipment management. PLM has redefined the value of data in manufacturing by providing a good return on investment, with employees becoming more efficient when all information is readily available. The integration of PLM with ERP systems has become particularly important for companies expanding their manufacturing capabilities across different geographic regions, helping maintain consistent product quality throughout their production facilities.

Manufacturing Execution System (MES) Segment in Smart Factory Market

The manufacturing execution systems (MES) segment is projected to experience the fastest growth rate of approximately 11% during 2024-2029. MES systems are increasingly being recognized as strategic elements for flexible and integrated production, combining all tasks of modern production management into a comprehensive software system. The growth is driven by manufacturing organizations facing challenges in increasing manufacturing profitability, obtaining higher return on assets, lowering business risk, and enhancing customer relationship processes. The integration of MES with ERP systems enables manufacturers to coordinate work orders and other resource needs effectively, helping make manufacturing leaner with real-time production adjustments, accurate demand forecasts, just-in-time deliveries, the ability to avoid rush orders, and seamless change orders. End users are increasingly investing in MES software to help drive value chain connectivity, interoperability, and collaboration.

Remaining Segments in Smart Factory Technology Market

The smart factory technology market encompasses several other significant segments including Human Machine Interface (HMI), Enterprise Resource Planning (ERP), Distributed Control System (DCS), Supervisory Control and Data Acquisition (SCADA), and Programmable Logic Controller (PLC). DCS plays a vital role in providing high-performance control capabilities for complex industrial processes, while SCADA systems enable comprehensive monitoring and control of industrial operations. PLC systems form the backbone of industrial automation by providing reliable control functions. HMI systems facilitate effective human-machine interactions and process monitoring, while ERP systems ensure seamless integration of business processes with manufacturing operations. Each of these technologies contributes uniquely to the overall smart factory ecosystem, enabling different aspects of automation, control, and optimization of manufacturing processes.

Segment Analysis: By End-User Industry

Oil & Gas Segment in Smart Factory Market

The oil and gas industry dominates the smart factory market, commanding approximately 19% of the total market share in 2024. This significant market position is driven by the increasing adoption of automation and control systems in critical operations such as remote monitoring of oil wells, pipeline management, and refinery operations. The industry's focus on operational efficiency, safety compliance, and the need for real-time monitoring of critical processes has led to substantial investments in smart factory solutions. Major oil and gas companies are implementing advanced technologies like IIoT-based equipment monitoring, energy efficiency solutions, and predictive maintenance systems to optimize their operations and reduce operational costs while ensuring regulatory compliance and environmental sustainability.

Semiconductor Segment in Smart Factory Market

The semiconductor segment is emerging as the fastest-growing sector in the smart factory market, with a projected growth rate of approximately 13% during 2024-2029. This remarkable growth is primarily attributed to the increasing demand for automated material handling systems and the need for more sophisticated process integration in semiconductor fabrication plants. The industry's push toward advanced technologies like AI-driven simulation, machine learning algorithms, and integrated IT/OT solutions is driving the adoption of smart factory solutions. Semiconductor manufacturers are increasingly focusing on implementing fully automated smart factories to improve throughput, enhance quality control, and reduce operational costs while maintaining the precision and consistency required in semiconductor production.

Remaining Segments in End-User Industry

The smart factory market encompasses several other significant industry segments including automotive, chemical and petrochemical, pharmaceutical, aerospace and defense, food and beverage, and mining sectors. The automotive sector is witnessing substantial transformation through the integration of robotics and factory automation systems in manufacturing processes. The chemical and petrochemical industry is focusing on process automation and safety systems, while the pharmaceutical sector is implementing smart factory solutions for quality control and regulatory compliance. The aerospace and defense industry is leveraging smart factory solutions for precision manufacturing and quality assurance, while the food and beverage sector is adopting automation for improved food safety and production efficiency. The mining sector is implementing smart technologies for enhanced operational safety and resource optimization.

Smart Factory Market Geography Segment Analysis

Smart Factory Market in North America

North America represents one of the most advanced markets for smart factory solutions, driven by early technology adoption and a strong manufacturing base. The United States and Canada are leading the implementation of Industry 4.0 technologies, with significant investments in automation, artificial intelligence, and the Industrial Internet of Things (IIoT). The region's growth is supported by a robust ecosystem of technology providers, system integrators, and end-users across the automotive, semiconductor, and aerospace industries. Manufacturing companies in both countries are increasingly focusing on digital transformation to improve operational efficiency and maintain a competitive advantage in the global smart factory industry.

Smart Factory Market in United States

The United States dominates the North American smart factory market landscape with approximately 82% market share in 2024, establishing itself as the regional powerhouse. The country's leadership position is reinforced by its strong industrial base, technological innovation capabilities, and the presence of major automation solution providers. American manufacturers are increasingly adopting advanced manufacturing technologies, particularly in the automotive, semiconductor, and aerospace sectors. The government's initiatives to revitalize the manufacturing sector through Industry 4.0 adoption, coupled with significant private sector investments in factory automation, continue to drive market growth. The presence of major technology companies and research institutions further strengthens the country's position in developing and implementing cutting-edge smart manufacturing solutions.

Smart Factory Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 10% from 2024-2029. The country's smart factory market is experiencing rapid expansion driven by increasing automation in its manufacturing sector, particularly in the automotive and electronics industries. Canadian manufacturers are actively embracing digital transformation, supported by government initiatives promoting Industry 4.0 adoption. The country's strong focus on research and development, coupled with its skilled workforce, is facilitating the implementation of advanced manufacturing technologies. Canadian companies are particularly focusing on implementing collaborative robots, artificial intelligence, and advanced analytics to enhance their manufacturing capabilities and global competitiveness.

Smart Factory Market in Europe

Europe stands as a crucial market for smart factory solutions, characterized by its strong industrial heritage and technological innovation. The region encompasses key manufacturing economies, including Germany, France, and the United Kingdom, each contributing significantly to the market's development. European manufacturers are at the forefront of Industry 4.0 implementation, particularly in the automotive, chemical, and discrete manufacturing sectors. The region's growth is supported by strong government initiatives, including Industry 4.0 programs and digital transformation strategies, along with collaboration between industry stakeholders and research institutions.

Smart Factory Market in Germany

Germany maintains its position as Europe's largest smart factory market, commanding approximately 26% of the regional market share in 2024. The country's leadership is built on its strong manufacturing base, particularly in the automotive and industrial equipment sectors. German manufacturers are recognized globally for their advanced manufacturing capabilities and early adoption of Industry 4.0 concepts. The country's robust ecosystem of automation solution providers, research institutions, and industrial companies continues to drive innovation in smart manufacturing technologies. German industries are particularly focused on implementing cyber-physical systems, industrial IoT, and advanced robotics solutions.

Smart Factory Market in France

France emerges as Europe's fastest-growing smart factory market, with a projected growth rate of approximately 10% from 2024-2029. The country's manufacturing sector is undergoing rapid digital transformation, supported by government initiatives and private sector investments. French manufacturers are increasingly adopting advanced automation solutions, particularly in the aerospace, automotive, and food processing industries. The country's focus on developing smart manufacturing capabilities is complemented by its strong research and development infrastructure and growing ecosystem of technology startups. French industries are particularly emphasizing the implementation of artificial intelligence, machine learning, and advanced analytics in their manufacturing processes.

Smart Factory Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for smart factory solutions, characterized by rapid industrialization and technological advancement. Countries like China, India, and Japan are driving significant growth in smart manufacturing adoption. The region's manufacturing sector is undergoing substantial digital transformation, with increasing investments in automation, robotics, and Industrial IoT solutions. The diversity of manufacturing capabilities across the region, from advanced electronics in Japan to large-scale manufacturing in China and emerging industrial capabilities in India, creates varied opportunities for smart factory solutions implementation.

Smart Factory Market in China

China stands as the dominant force in the Asia-Pacific smart factory market, leveraging its massive manufacturing base and aggressive industrial modernization initiatives. The country's manufacturing sector is undergoing rapid digital transformation, supported by national initiatives like Made in China 2025. Chinese manufacturers are increasingly adopting advanced automation solutions, particularly in the electronics, automotive, and machinery sectors. The country's robust ecosystem of technology providers and strong government support continues to drive innovation in smart manufacturing technologies.

Smart Factory Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, driven by its rapidly evolving manufacturing sector and increasing focus on digital transformation. The country's smart manufacturing initiatives are supported by government programs like Make in India and Industry 4.0 adoption across various sectors. Indian manufacturers are increasingly implementing advanced automation solutions, particularly in the automotive, electronics, and pharmaceutical industries. The country's growing technology ecosystem and skilled workforce are facilitating the adoption of smart factory solutions.

Smart Factory Market in Latin America

Latin America represents an emerging market for smart factory solutions, with Brazil, Mexico, and Argentina leading the regional adoption. The region's manufacturing sector is gradually embracing digital transformation, driven by the need to improve productivity and competitiveness. Brazil emerges as the largest market in the region, while Mexico shows the fastest growth rate, supported by its strong automotive and electronics manufacturing sectors. The region's adoption of smart factory solutions is particularly notable in the automotive, consumer goods, and food and beverage industries, with an increasing focus on automation and Industrial IoT implementation.

Smart Factory Market in Middle East & Africa

The Middle East & Africa region demonstrates growing potential in the smart factory market, with the United Arab Emirates and Saudi Arabia leading the adoption of smart manufacturing technologies. The region's industrial sector is increasingly focusing on digital transformation, particularly in the oil and gas, chemical, and manufacturing industries. The United Arab Emirates emerges as the largest market in the region, while Saudi Arabia shows the fastest growth rate, driven by its Vision 2030 initiative and increasing investments in industrial automation. The region's adoption of smart factory solutions is supported by government initiatives promoting industrial diversification and technological advancement.

Get Analysis on Important Geographic Markets

Download PDF

Smart Factory Industry Overview

Top Companies in Smart Factory Market

The smart factory market features prominent players like ABB, Siemens, Schneider Electric, Emerson Electric, Rockwell Automation, Honeywell International, and Yokogawa Electric Corporation. These companies are driving innovation through significant investments in research and development, particularly focusing on Industrial Internet of Things (IIoT), artificial intelligence, machine learning, and advanced automation solutions. Strategic partnerships and collaborations have become increasingly common as companies seek to enhance their technological capabilities and expand their market presence. Companies are actively pursuing product portfolio expansion through both internal development and strategic acquisitions, especially in emerging technologies like cloud computing, edge computing, and 5G integration. Operational agility is being achieved through vertical integration of manufacturing processes and the development of comprehensive end-to-end smart factory solutions that can be customized for different industries.

Consolidated Market with Strong Global Players

The smart factory market is characterized by the dominance of large multinational conglomerates that possess extensive resources, established distribution networks, and comprehensive product portfolios. These major players have built their market positions through decades of experience, strong brand recognition, and the ability to provide integrated solutions across multiple industrial automation segments. The market shows a moderate level of consolidation, with the top players holding significant market share while competing intensely through technological differentiation and industry-specific expertise. Regional players and specialists maintain their presence by focusing on niche applications or specific geographical markets where they can leverage local knowledge and relationships.

The market has witnessed active merger and acquisition activity as established players seek to strengthen their technological capabilities and expand their geographical footprint. Companies are particularly targeting acquisitions in emerging technologies like artificial intelligence, machine vision, and advanced robotics to enhance their smart manufacturing offerings. Strategic partnerships between technology providers and industrial automation companies have become increasingly common, creating ecosystems that combine domain expertise with cutting-edge digital capabilities. This trend is expected to continue as companies seek to address the growing complexity of smart manufacturing solutions and the need for seamless integration across different platforms and protocols.

Innovation and Integration Drive Market Success

Success in the smart factory market increasingly depends on the ability to provide comprehensive, integrated solutions that address the entire manufacturing value chain. Incumbent players are focusing on developing modular, scalable platforms that can be easily customized for different industries while maintaining compatibility with existing systems. Companies are investing heavily in building strong service capabilities, including remote monitoring, predictive maintenance, and digital twin technologies. The ability to demonstrate clear return on investment through improved operational efficiency, reduced downtime, and enhanced quality control has become crucial for maintaining market position. Vendors are also strengthening their cybersecurity capabilities and ensuring compliance with evolving industrial standards to address growing concerns about data security and system reliability.

For contenders looking to gain market share, specialization in specific industry verticals or technological niches offers a viable path to growth. Success factors include developing strong domain expertise, building strategic partnerships with established players, and focusing on innovative solutions that address specific customer pain points. The market shows relatively low substitution risk due to high switching costs and the critical nature of automation systems in manufacturing processes. However, companies must navigate increasingly complex regulatory requirements, particularly around data privacy, environmental compliance, and worker safety. The concentration of end-users varies by industry segment, with automotive, electronics, and process industries showing higher levels of concentration, requiring vendors to develop industry-specific expertise and solutions.

Smart Factory Market Leaders

-

ABB Ltd

-

Cognex Corporation

-

Siemens AG

-

Schneider Electric SE

-

Yokogawa Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Smart Factory Market News

- February 2023: Emerson combined its extensive power expertise and renewable energy capabilities into the OvationTM Green portfolio to help power generation companies meet the needs of their customers as they transition to green energy generation and storage. Emerson has broadened its power-based control architecture by integrating newly acquired Mita-Teknik software and technology with its industry-leading Ovation automation platform, extensive renewable energy knowledge base, cybersecurity solutions, and remote management capabilities.

- January 2023: Siemens Digital Industries Software announced the launch of eXplore live at Wichita's The Smart Factory. The smart factory contains a fully experiential lab and an active product line for developing and exploring innovative smart manufacturing capabilities. The Siemens Xcelerator portfolio is used in eXplore Live at Deloitte's The Smart Factory in Wichita to help companies experience the power of digitalization and the future of smart manufacturing.

- October 2022: ABB entered into a strategic collaboration with U.S.-based startup Scalable Robotics to improve its portfolio of user-friendly robotic welding techniques. Through 3D vision and implanted process understanding, the Scalable Robotics technology enables users to quickly program welding robots without coding.

Smart Factory Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of Macroeconomic Trends on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Growing Adoption of Internet of Things (IoT) Technologies Across the Value Chain

- 5.1.2 Rising Demand for Energy Efficiency

-

5.2 Market Restraints

- 5.2.1 Huge Capital Investments for Transformations

- 5.2.2 Vulnerable to Cyberattacks

6. MARKET SEGMENTATION

-

6.1 By Product Type

- 6.1.1 Machine Vision Systems

- 6.1.1.1 Cameras

- 6.1.1.2 Processors

- 6.1.1.3 Software

- 6.1.1.4 Enclosures

- 6.1.1.5 Frame Grabbers

- 6.1.1.6 Integration Services

- 6.1.1.7 Lighting

- 6.1.2 Industrial Robotics

- 6.1.2.1 Articulated Robots

- 6.1.2.2 Cartesian Robots

- 6.1.2.3 Cylindrical Robots

- 6.1.2.4 SCARA Robots

- 6.1.2.5 Parallel Robots

- 6.1.2.6 Collaborative Industry Robots

- 6.1.3 Control Devices

- 6.1.3.1 Relays and Switches

- 6.1.3.2 Servo Motors and Drives

- 6.1.4 Sensors

- 6.1.5 Communication Technologies

- 6.1.5.1 Wired

- 6.1.5.2 Wireless

- 6.1.6 Other Product Types

-

6.2 By Technology

- 6.2.1 Product Lifecycle Management (PLM)

- 6.2.2 Human Machine Interface (HMI)

- 6.2.3 Enterprise Resource and Planning (ERP)

- 6.2.4 Manufacturing Execution System (MES)

- 6.2.5 Distributed Control System (DCS)

- 6.2.6 Supervisory Controller and Data Acquisition (SCADA)

- 6.2.7 Programmable Logic Controller (PLC)

- 6.2.8 Other Technologies

-

6.3 By End-user Industry

- 6.3.1 Automotive

- 6.3.2 Semiconductors

- 6.3.3 Oil and Gas

- 6.3.4 Chemical and Petrochemical

- 6.3.5 Pharmaceutical

- 6.3.6 Aerospace and Defense

- 6.3.7 Food and Beverage

- 6.3.8 Mining

- 6.3.9 Other End-user Industries

-

6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 ABB Ltd

- 7.1.2 Cognex Corporation

- 7.1.3 Siemens AG

- 7.1.4 Schneider Electric SE

- 7.1.5 Yokogawa Electric Corporation

- 7.1.6 KUKA AG

- 7.1.7 Rockwell Automation Inc.

- 7.1.8 Honeywell International Inc.

- 7.1.9 Robert Bosch GmbH

- 7.1.10 Mitsubishi Electric Corporation

- 7.1.11 Fanuc Corporation

- 7.1.12 Emerson Electric Co.

- 7.1.13 FLIR Systems Inc. (Teledyne Technologies Incorporated)

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific' and Latin America and Middle East and Africa will be considered together as 'Rest of the World'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Smart Factory Industry Segmentation

Smart factory refers to the different fully integrated automation solutions adopted for manufacturing buildings. Such integration helps streamline the material flow during all the procedures involved in manufacturing. Big Data analytics allows factories to use smart solutions in their functions within its premises to shift from reactionary practices to predictive ones. This change targets enhanced efficiency of the process and product performance.

The studied market is segmented by different product types, such as machine vision systems, industrial robotics, control devices, sensors, and communication technologies, among other technologies. The study also considers various end-user industries and multiple geographies. The impact of macroeconomic trends on the market and impacted segments is also covered under the scope of the study. Further, the disturbance of the factors affecting the market's evolution in the near future has been covered in the study concerning drivers and restraints.

The market sizes and forecasts regarding value in (USD) for all the above segments are provided.

| By Product Type | Machine Vision Systems | Cameras | |

| Processors | |||

| Software | |||

| Enclosures | |||

| Frame Grabbers | |||

| Integration Services | |||

| Lighting | |||

| Industrial Robotics | Articulated Robots | ||

| Cartesian Robots | |||

| Cylindrical Robots | |||

| SCARA Robots | |||

| Parallel Robots | |||

| Collaborative Industry Robots | |||

| Control Devices | Relays and Switches | ||

| Servo Motors and Drives | |||

| Sensors | |||

| Communication Technologies | Wired | ||

| Wireless | |||

| Other Product Types | |||

| By Technology | Product Lifecycle Management (PLM) | ||

| Human Machine Interface (HMI) | |||

| Enterprise Resource and Planning (ERP) | |||

| Manufacturing Execution System (MES) | |||

| Distributed Control System (DCS) | |||

| Supervisory Controller and Data Acquisition (SCADA) | |||

| Programmable Logic Controller (PLC) | |||

| Other Technologies | |||

| By End-user Industry | Automotive | ||

| Semiconductors | |||

| Oil and Gas | |||

| Chemical and Petrochemical | |||

| Pharmaceutical | |||

| Aerospace and Defense | |||

| Food and Beverage | |||

| Mining | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Asia | China | ||

| India | |||

| Japan | |||

| Australia and New Zealand | |||

| Latin America | Brazil | ||

| Argentina | |||

| Mexico | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| South Africa | |||

Need A Different Region or Segment?

Customize Now

Smart Factory Market Research Faqs

How big is the Smart Factory Market?

The Smart Factory Market size is expected to reach USD 389.14 billion in 2025 and grow at a CAGR of 9.74% to reach USD 619.34 billion by 2030.

What is the current Smart Factory Market size?

In 2025, the Smart Factory Market size is expected to reach USD 389.14 billion.

Who are the key players in Smart Factory Market?

ABB Ltd, Cognex Corporation, Siemens AG, Schneider Electric SE and Yokogawa Electric Corporation are the major companies operating in the Smart Factory Market.

Which is the fastest growing region in Smart Factory Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Smart Factory Market?

In 2025, the Asia-Pacific accounts for the largest market share in Smart Factory Market.

What years does this Smart Factory Market cover, and what was the market size in 2024?

In 2024, the Smart Factory Market size was estimated at USD 351.24 billion. The report covers the Smart Factory Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Smart Factory Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Smart Factory Market Research

Mordor Intelligence provides a comprehensive analysis of the smart factory landscape. We leverage our extensive expertise in industrial automation and Industry 4.0 research. Our detailed report examines how digital manufacturing technologies, IIoT implementations, and manufacturing execution systems are transforming traditional facilities into connected factory environments. The analysis covers key developments in factory automation and intelligent manufacturing, highlighting the evolution toward the factory of the future.

Stakeholders gain valuable insights into smart factory solutions and industrial digital twin applications through our detailed market analysis. This information is available as an easy-to-download report PDF. The research explores emerging trends in manufacturing digitization, factory digitalization, and advanced manufacturing technologies. It also provides comprehensive coverage of smart manufacturing initiatives and industrial automation control systems. Our analysis helps decision-makers understand the complex ecosystem of smart factory technology and its impact on connected manufacturing. This enables informed strategic planning and implementation.