| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 11.81 Billion |

| Market Size (2030) | USD 19.35 Billion |

| CAGR (2025 - 2030) | 10.38 % |

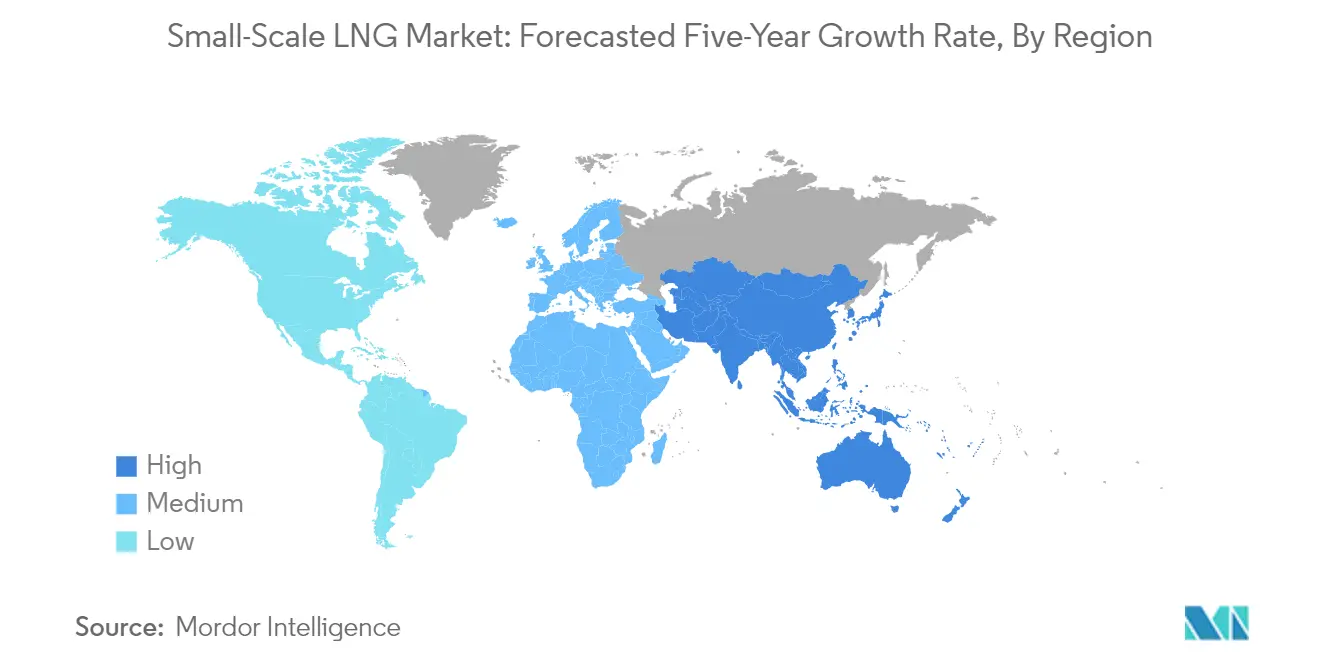

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

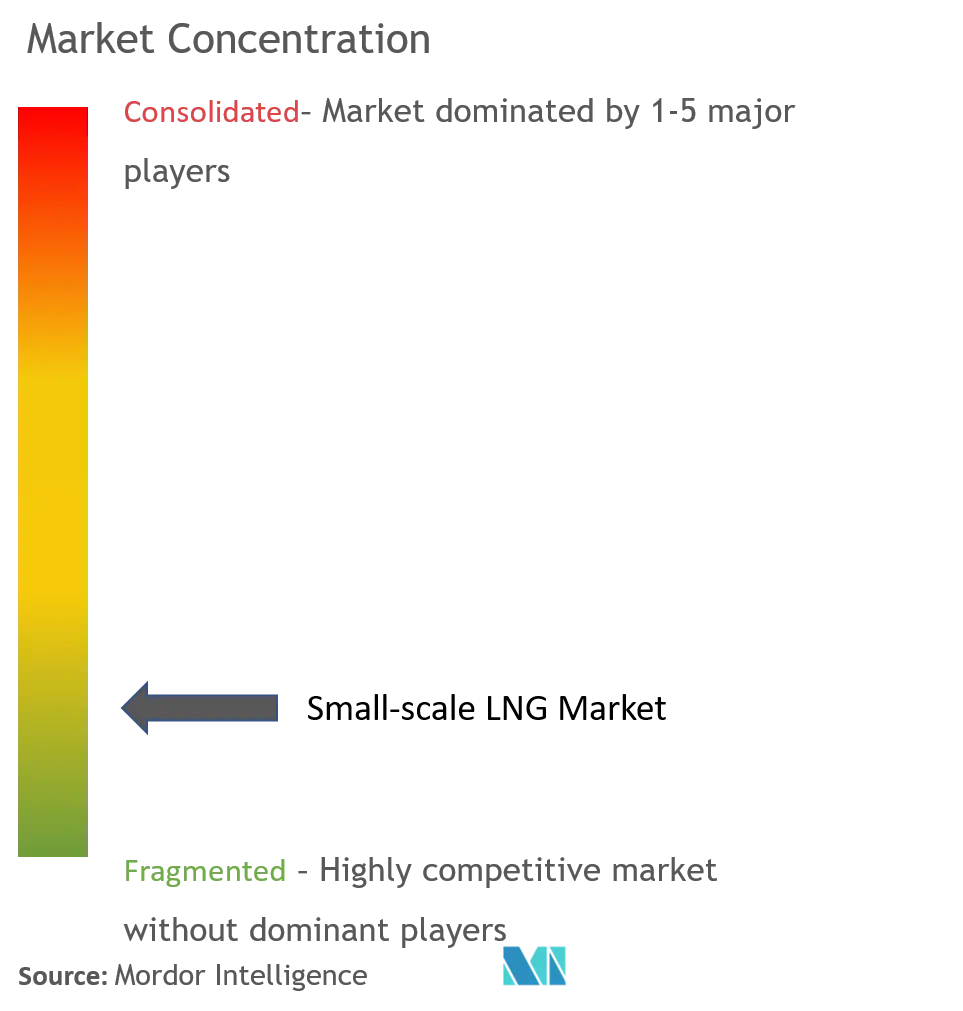

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Small-scale LNG Market Analysis

The Small-scale LNG Market size is estimated at USD 11.81 billion in 2025, and is expected to reach USD 19.35 billion by 2030, at a CAGR of 10.38% during the forecast period (2025-2030).

The small-scale LNG industry is experiencing significant transformation driven by evolving global energy dynamics and environmental regulations. The implementation of IMO 2020 regulations has fundamentally altered the marine fuel landscape, pushing shipping companies to adopt cleaner fuel alternatives. This shift has catalyzed investments in LNG bunkering infrastructure across major ports worldwide. Shell, a major player in the industry, currently operates approximately 90 LNG carriers, representing about 20% of the global LNG shipping fleet, demonstrating the scale of infrastructure development in the sector. The industry is witnessing increased collaboration between energy companies and port authorities to develop comprehensive LNG supply networks.

The market is characterized by strategic partnerships and infrastructure developments aimed at expanding small-scale LNG accessibility. In 2023, Pavilion Energy Trading & Supply Pte. Ltd. established a significant agreement with Hangjiaxin to supply small-scale LNG from Singapore, committing to deliver up to 0.5 million TPY of LNG. This trend of cross-border partnerships is reshaping the industry's supply chain dynamics. Companies are increasingly focusing on developing modular LNG solutions to serve diverse end-user requirements, from industrial applications to marine bunkering.

Technological advancements in LNG liquefaction and regasification processes are enabling more efficient small-scale operations. In June 2022, GAIL placed an order for two small-scale liquefaction skids capable of producing LNG on a pilot basis, demonstrating the industry's move toward more compact and versatile solutions. These developments are particularly significant for remote locations and off-grid applications, where traditional pipeline infrastructure is not economically viable. The industry is seeing increased adoption of innovative solutions like truck-to-ship bunkering and mobile LNG facilities.

The market is witnessing a geographical shift in trade patterns and infrastructure development. Qatar, maintaining its position as a major LNG exporter with 77 million tons in 2021, is investing in small-scale infrastructure to serve diverse market segments. China's emergence as the world's largest LNG importer, reaching 79 million tons in 2021, has spurred the development of small-scale LNG terminals and distribution networks. The industry is also seeing significant developments in terminal operations, exemplified by Gas Vitality's successful completion of its first loading operation at the Fos Cavaou LNG terminal in late 2021, initiating new small-scale LNG loading services with 50 loading slots per year for vessels up to 40,000 m³.

Small-scale LNG Market Trends

Growing Demand for LNG in Transportation Sector

The transportation sector has emerged as a significant driver for the small-scale LNG market, particularly in marine and heavy-duty road transport applications. According to Shell LNG Outlook 2024, there were 469 LNG-fueled vessels in operation and 537 LNG-fueled vessels on order as of 2023, demonstrating the robust adoption of LNG as a marine fuel. This trend is further exemplified by recent developments like Venture Global LNG's March 2024 initiative to construct nine new LNG-powered vessels, including six vessels with 174,000 m3 cargo capacity and three with 200,000 m3 capacity in South Korea.

The inherent advantages of LNG as a transportation fuel have been instrumental in driving its adoption. LNG's non-corrosive and non-toxic properties can extend vehicle life by up to three times compared to conventional fuels. Additionally, LNG's extremely low boiling point requires minimal heat for conversion to gaseous form at high pressure, resulting in negligible mechanical energy consumption and making it an exceptionally efficient fuel for transportation. These characteristics, combined with its economic and environmental benefits compared to diesel and fuel oil, have made LNG particularly attractive for commercial fleet operators and shipping companies looking to optimize their operations while meeting stringent environmental regulations. The establishment of LNG fueling stations is pivotal in supporting this growth, facilitating the expansion of LNG transportation networks.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Focus on Clean Energy and Environmental Regulations

Stringent environmental regulations and clean energy initiatives have become major catalysts for small-scale LNG market growth. The European Green Deal, introduced by the European Commission in 2019, has set ambitious targets for achieving carbon neutrality by 2050, specifically emphasizing the role of LNG in reducing emissions from trucks and marine vessels. These policy initiatives have created a strong regulatory framework that encourages the adoption of LNG as an alternative fuel, particularly in the transportation sector where emissions reduction is a critical priority.

The implementation of international environmental standards, such as IMO 2020 regulations, has further accelerated the transition toward LNG as a marine fuel. These regulations have placed strict limits on sulfur emissions from marine vessels, making LNG an attractive alternative due to its significantly lower emissions profile. Similarly, regional emission control standards like China VI have created additional momentum for LNG adoption in the road transport sector. The alignment of these regulations with the environmental benefits of LNG - including reduced greenhouse gas emissions and virtually zero sulfur emissions - has created a strong regulatory environment supporting the growth of small-scale LNG infrastructure. The development of LNG logistics systems is essential to ensure efficient LNG distribution in compliance with these regulations.

Rising Demand from Remote Areas and Industrial Applications

The growing need for reliable energy supply in remote areas and industrial applications has emerged as a crucial driver for the small-scale LNG market. This is particularly evident in regions lacking traditional pipeline infrastructure, where small-scale LNG offers a viable solution for energy distribution. A prime example is India's recent initiatives, including the March 2024 launch of the country's first small-scale LNG unit by GAIL at Vijaipur in Madhya Pradesh, demonstrating the increasing focus on developing small-scale LNG infrastructure to serve remote locations.

The industrial sector's demand for cleaner and more efficient fuel sources has also contributed significantly to market growth. Small-scale LNG facilities provide a flexible solution for industrial users requiring reliable energy supply in areas not connected to traditional gas pipeline networks. This is exemplified by GAIL Limited's initiative to establish small liquefaction facilities specifically targeting areas without pipeline connectivity, supporting India's broader goal of increasing natural gas's share in its energy mix to 15% by 2030. The ability of small-scale LNG to serve as both an industrial feedstock and power generation fuel has made it an increasingly attractive option for industrial users looking to optimize their energy consumption while meeting environmental objectives. The concept of LNG virtual pipeline systems and containerized LNG solutions further enhances the accessibility and distribution of LNG in these challenging environments.

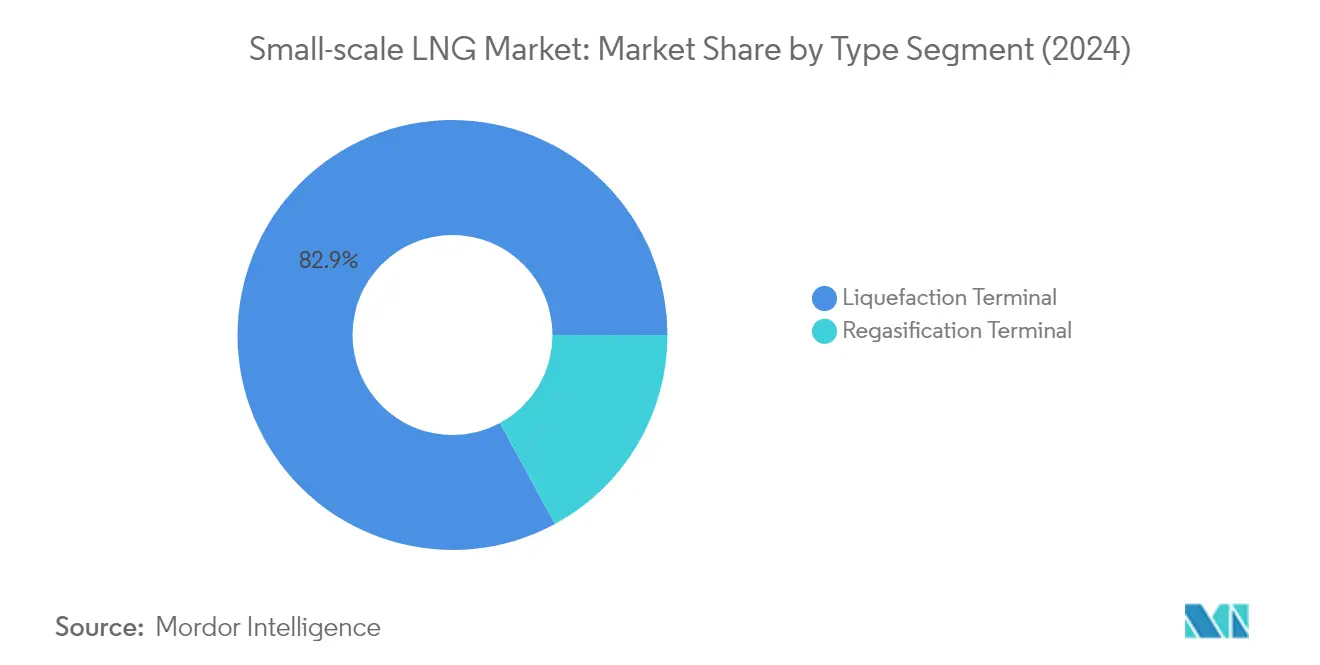

Segment Analysis: Type

Liquefaction Terminal Segment in Small-scale LNG Market

The liquefaction terminal segment dominates the small-scale LNG market, holding approximately 83% market share in 2024. This significant market position is driven by the increasing adoption of small-scale liquefaction facilities in remote areas and regions without traditional pipeline infrastructure. The segment's growth is particularly strong in Asia-Pacific, where countries like China are developing numerous small-scale liquefaction facilities to serve specific markets with production capacities under 0.5 million tons per year. These terminals are proving to be more cost-effective than large-scale facilities, with lower overall CAPEX and OPEX, shorter kick-off timelines, and reduced pay-off periods. The segment is also benefiting from the rising demand for LNG peak shaving applications in power plants and the increasing need for distributed LNG production business models.

Regasification Terminal Segment in Small-scale LNG Market

The regasification terminal segment is emerging as the fastest-growing segment in the small-scale LNG market, with a projected growth rate of approximately 19% during 2024-2029. This remarkable growth is primarily attributed to the increasing demand for clean energy solutions in remote industrial sectors and the rising adoption of LNG as a marine fuel. The segment is witnessing significant developments in Europe, where countries are expanding their small-scale LNG infrastructure to comply with stricter emission regulations. The growth is further supported by the increasing number of small-scale regasification facilities being developed near ports and industrial clusters, offering flexible and efficient solutions for LNG distribution. These terminals are particularly gaining traction in regions with limited pipeline infrastructure, providing a viable solution for meeting localized energy demands.

Segment Analysis: Mode of Supply

Truck Segment in Small-Scale LNG Market

The truck segment dominates the small-scale LNG market, holding approximately 53% market share in 2024. This segment's prominence is driven by its flexibility in transporting LNG to areas without pipeline infrastructure and its cost-effectiveness for small-scale distribution. Modern LNG transport trucks are equipped with double-walled containers featuring internal stainless steel containment and external carbon or stainless steel walls, significantly reducing volume losses from heat transfer. These advanced trailers can store LNG for up to 45 days without requiring venting for pressure management. The segment's growth is further supported by increasing demand from remote industrial consumers, power generation facilities, and the expanding network of LNG fueling stations across major transportation routes. In regions like Europe and Asia-Pacific, truck-based LNG transportation has become particularly crucial for supporting the growing network of LNG stations and industrial users in areas not connected to traditional gas infrastructure.

Remaining Segments in Mode of Supply

The transshipment and bunkering segment represents a significant portion of the small-scale LNG market, playing a crucial role in marine applications and ship-to-ship transfers. This segment has gained importance due to stringent environmental regulations in the maritime sector and the increasing adoption of LNG as a marine fuel. The pipeline and rail segment, while smaller in market share, offers unique advantages in specific geographical contexts where established rail networks can efficiently connect LNG terminals to demand nodes. This segment is particularly relevant in regions with developed rail infrastructure and where pipeline construction might be challenging due to geographical or economic constraints. Both segments continue to evolve with technological advancements and infrastructure development, contributing to the overall growth of the small-scale LNG market.

Segment Analysis: Application

Transportation Segment in Small-Scale LNG Market

The transportation segment has emerged as both the dominant and fastest-growing segment in the small-scale LNG market, holding approximately 53% market share in 2024. This segment's prominence is primarily driven by the increasing adoption of LNG as a cleaner alternative fuel for heavy-duty vehicles and marine vessels. The implementation of stringent emission regulations, particularly IMO 2020 for maritime transport, has significantly boosted the demand for LNG as a marine fuel. China, the United States, and Europe have already made substantial progress in deploying LNG-powered trucks, especially for long-distance freight carriage, supported by government policies and regulations on decarbonization and emission control. According to industry data, there were 137 LNG-fueled ships in operation and 350 LNG-fueled ships on order as of early 2024, demonstrating the rapid growth in this sector. The segment's growth is further supported by the development of LNG bunkering market infrastructure in major ports and the expansion of LNG fueling stations for heavy vehicles.

Remaining Segments in Small-Scale LNG Market Applications

The industrial feedstock segment represents a significant portion of the small-scale LNG market, serving various industries through captive power plants and as a reactant in industrial processes. This segment has gained traction due to the increasing need for reliable and cleaner energy sources in remote industrial locations. The power generation segment has established itself as a crucial application, particularly in areas without access to natural gas pipeline infrastructure, providing a flexible backup to variable renewable sources. Small-scale LNG power generation has proven especially valuable in remote residential and industrial sectors, offering an economical solution for peak shaving and emergency backup power. Other applications, including mining and rail activities, though smaller in market share, play an important role in specific sectors where traditional energy infrastructure is limited or where environmental regulations drive the transition to cleaner fuels.

Small-scale LNG Market Geography Segment Analysis

Small-scale LNG Market in North America

North America has emerged as a significant player in the small-scale LNG market, driven by technological improvements and the need for natural gas supplies to reach remote areas. The region's market is characterized by a robust infrastructure network, particularly in the United States and Canada. The presence of established LNG terminal facilities, coupled with growing demand for cleaner fuel alternatives in marine and transportation sectors, has created a favorable environment for small-scale LNG development. The region's strategic focus on reducing greenhouse gas emissions and improving fuel efficiency has further accelerated market growth.

Small-scale LNG Market in the United States

The United States dominates the North American small-scale LNG market, holding approximately 24% of the global market share in 2024. The country's leadership position is supported by its extensive network of small-scale facilities, including peak shaving units, satellite facilities, and marine terminals. The United States Department of Transportation's Pipeline and Hazardous Materials Safety Administration oversees numerous small-scale LNG facilities across the country, serving various applications from power sector operations to marine bunkering. The country's strategic location and well-developed infrastructure network have enabled efficient distribution of LNG to otherwise untapped markets.

Small-scale LNG Market in Canada

Canada represents the fastest-growing market in North America, with a projected growth rate of approximately 10% from 2024 to 2029. The country's growth is primarily driven by increasing demand for LNG in remote communities and the marine sector. Canada's focus on reducing diesel consumption in remote areas has led to increased investment in small-scale LNG infrastructure. The government's initiatives to promote cleaner energy sources and provide reliable power supply to remote communities have created significant opportunities for market expansion. The country's strategic position and abundant natural gas resources further support its rapid market growth.

Small-scale LNG Market in Europe

Europe has established itself as a pioneer in small-scale LNG infrastructure development, with several countries implementing innovative solutions for LNG distribution and bunkering. The region's commitment to reducing carbon emissions and meeting stringent environmental regulations has driven significant investments in small-scale LNG facilities. Countries like Norway, the Netherlands, and Spain have taken leading roles in developing LNG bunkering infrastructure and promoting LNG as a marine fuel. The European Union's supportive policies and regulations have created a favorable environment for market growth.

Small-scale LNG Market in Norway

Norway leads the European small-scale LNG market, commanding approximately 22% of the regional market share in 2024. The country's early adoption of LNG technology and comprehensive value chain development has established it as a market leader. Norway's success is supported by government initiatives such as the NOx fund, which provides financial support for LNG-fueled ships. The country's extensive coastline and strategic location have enabled it to develop a robust small-scale LNG infrastructure serving both domestic and international markets.

Small-scale LNG Market in Spain

Spain demonstrates the highest growth potential in Europe, with an expected growth rate of approximately 11% from 2024 to 2029. The country's strategic geographical location and extensive coastline have positioned it as a key player in the small-scale LNG market. Spain's well-developed LNG infrastructure, including multiple terminals with truck loading facilities, supports its rapid market expansion. The country's commitment to developing LNG bunkering services and promoting LNG as a transportation fuel has created significant growth opportunities.

Small-scale LNG Market in Asia-Pacific

The Asia-Pacific region represents the largest and most dynamic small-scale LNG market globally, characterized by rapid industrialization and increasing demand for cleaner energy solutions. Countries across the region are investing heavily in small-scale LNG infrastructure to support various applications, from power generation to marine transport. The region's diverse energy needs and growing focus on environmental sustainability have created significant opportunities for market expansion. The presence of major LNG importers and exporters has facilitated the development of comprehensive small-scale LNG value chains.

Small-scale LNG Market in China

China stands as the dominant force in the Asia-Pacific small-scale LNG market. The country's extensive network of small-scale liquefaction plants, particularly in the northwestern and central provinces, demonstrates its market leadership. China's commitment to reducing carbon emissions and promoting natural gas as a cleaner fuel alternative has driven significant investments in small-scale LNG infrastructure. The country's robust transportation sector and growing industrial demand continue to support market expansion.

Small-scale LNG Market in India

India emerges as the fastest-growing market in the Asia-Pacific region. The country's ambitious plans to increase the share of natural gas in its energy mix have created substantial opportunities for small-scale LNG development. India's focus on developing LNG infrastructure for transportation and industrial applications, coupled with government initiatives to reduce carbon emissions, has accelerated market growth. The country's expanding network of LNG stations and growing demand from various sectors continue to drive market expansion.

Small-scale LNG Market in South America

South America's small-scale LNG market is characterized by emerging opportunities and growing infrastructure development. The region's diverse energy needs and geographical challenges have created significant potential for small-scale LNG solutions. Brazil emerges as both the largest and fastest-growing market in the region, driven by its extensive coastline and increasing demand from industrial and power generation sectors. Peru and Panama also contribute significantly to the regional market, particularly in developing LNG infrastructure for remote areas and maritime applications. The region's focus on reducing dependence on traditional fuels and improving energy access has created favorable conditions for market growth.

Small-scale LNG Market in Middle East & Africa

The Middle East & Africa region presents unique opportunities in the small-scale LNG market, driven by diverse energy needs and growing infrastructure development. Qatar leads the regional market as both the largest and fastest-growing country, leveraging its position as a major LNG producer. The United Arab Emirates, South Africa, and Algeria also play significant roles in shaping the regional market landscape. The region's focus on developing LNG bunkering facilities and supporting industrial applications has created substantial growth opportunities. The increasing adoption of LNG as a cleaner fuel alternative and growing investments in small-scale infrastructure continue to drive market expansion.

Get Analysis on Important Geographic Markets

Download PDF

Small-scale LNG Industry Overview

Top Companies in Small-Scale LNG Market

The small-scale LNG market is dominated by major energy conglomerates, including Shell PLC, Linde PLC, PJSC Gazprom, and Engie SA, who leverage their extensive infrastructure and technological capabilities. Companies across the sector are focusing on developing proprietary technologies for liquefaction and regasification processes, with significant investments in modular and scalable solutions. Operational excellence is being pursued through digital transformation initiatives and the automation of terminal operations. Strategic partnerships and joint ventures are becoming increasingly common, particularly for expanding into emerging markets and developing bunkering infrastructure. Market leaders are also emphasizing sustainability through investments in bio-LNG capabilities and carbon capture technologies, while simultaneously expanding their small-scale LNG terminal networks across strategic locations to capture growing demand from industrial and transportation sectors.

Diverse Players Shape Dynamic Market Structure

The small-scale LNG market exhibits a moderately consolidated structure with distinct player categories, including integrated energy majors, specialized technology providers, and regional terminal operators. Global energy conglomerates maintain significant market presence through their established gas supply chains and extensive infrastructure networks, while specialized players like Chart Industries and Baker Hughes have carved out strong positions in technology provision and equipment manufacturing. The market is witnessing increased participation from regional players, particularly in Asia-Pacific and Europe, who focus on developing localized distribution networks and customer-specific solutions.

The industry is characterized by strategic alliances and collaborative ventures, particularly in emerging markets where local expertise is crucial for market entry and expansion. Merger and acquisition activities are primarily focused on technology acquisition and geographic expansion, with larger players acquiring specialized technology providers and regional operators to enhance their service offerings. The market is also seeing the emergence of new entrants, particularly in the marine bunkering and truck loading segments, though high capital requirements and technical expertise create significant barriers to entry.

Innovation and Flexibility Drive Future Success

Success in the small-scale LNG market increasingly depends on technological innovation, operational flexibility, and strategic positioning along the value chain. Incumbent players must focus on developing cost-effective and scalable solutions while expanding their geographic presence through strategic partnerships and investments in key markets. The ability to offer integrated solutions, from liquefaction to end-user delivery, while maintaining operational efficiency and environmental compliance, will be crucial for maintaining market leadership. Companies must also invest in developing sustainable solutions and alternative fuel options to address growing environmental concerns and regulatory requirements.

Market contenders can gain ground by focusing on specialized market segments and developing innovative solutions for specific end-user applications. Success factors include building strong relationships with local stakeholders, developing efficient distribution networks, and offering flexible contract terms to attract customers. The increasing focus on environmental regulations and emission standards presents opportunities for companies offering cleaner energy solutions and advanced technologies. Additionally, the ability to adapt to changing market dynamics, including end-user preferences and regulatory requirements, while maintaining cost competitiveness, will be crucial for long-term success in the market. Companies involved in LNG logistics and those operating LNG terminals are particularly well-positioned to capitalize on these trends.

Small Scale LNG Market Leaders

-

Shell PLC

-

Linde plc

-

PJSC Gazprom

-

Engie SA

-

Wartsila Oyj ABP

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Small-scale LNG Market News

- April 2024: the Indian Gas Exchange announced the contracts for small-scale liquefied natural gas on its platform after receiving approval from the Petroleum and Natural Gas Regulatory Board.

- November 2023: Elengy, a unit of Engie’s GRTgaz, established a new small-scale LNG carrier loading service at its Fos Tonkin terminal on France’s Mediterranean coast.

- May 2023: The National Gas Company of Trinidad and Tobago Limited signed a MoU with Globus Energy Group Trinidad Limited, Corban Energy Group, and Chester LNG LLC to identify and screen technologies for micro- and small-scale LNG development projects in the Caribbean.

Small Scale LNG Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

-

4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Investment in LNG Infrastructure

- 4.5.1.2 Rising Demand for LNG in Bunkering, Road Transportation, and Off-grid Power

- 4.5.2 Restraints

- 4.5.2.1 Lack of Supporting Infrastructure in the Regions such as the Middle East and Africa

- 4.6 Supply Chain Analysis

-

4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Type

- 5.1.1 Liquefaction Terminal

- 5.1.2 Regasification Terminal

-

5.2 Mode of Supply

- 5.2.1 Truck

- 5.2.2 Transshipment and Bunkering

- 5.2.3 Pipeline and Rail

-

5.3 Application

- 5.3.1 Transportation

- 5.3.2 Industrial Feedstock

- 5.3.3 Power Generation

- 5.3.4 Other Applications

-

5.4 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 France

- 5.4.2.3 United Kingdom

- 5.4.2.4 Russia

- 5.4.2.5 Spain

- 5.4.2.6 NORDIC

- 5.4.2.7 Italy

- 5.4.2.8 Turkey

- 5.4.2.9 Rest of the Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Vietnam

- 5.4.3.6 Malaysia

- 5.4.3.7 Indonesia

- 5.4.3.8 Australia

- 5.4.3.9 Rest of the Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Qatar

- 5.4.5.6 Nigeria

- 5.4.5.7 Rest of the Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Small-scale LNG Technology Providers

- 6.3.1.1 Linde PLC

- 6.3.1.2 Wartsila Oyj ABP

- 6.3.1.3 Baker Hughes Company

- 6.3.1.4 Honeywell UoP

- 6.3.1.5 Chart Industries Inc.

- 6.3.1.6 Black & Veatch Holding Company

- 6.3.2 Small-scale LNG Marine Transporter

- 6.3.2.1 Anthony Veder Group NV

- 6.3.2.2 Engie SA

- 6.3.2.3 Evergas AS

- 6.3.3 Small-scale LNG Operators

- 6.3.3.1 Shell PLC

- 6.3.3.2 Eni SpA

- 6.3.3.3 PJSC Gazprom

- 6.3.3.4 TotalEnergies SE

- 6.3.3.5 Gasum Oy

- 6.3.4 Market Ranking/Share (%) Analysis

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Development of Cost-efficient Small-scale LNG Infrastructure

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Small-scale LNG Industry Segmentation

Small-scale LNG (SSLNG) is defined as the liquefaction, regasification, and import terminals at plants with a capacity of less than 1 MTPA, according to the International Gas Union (IGU), and with applications in power generation, transportation, industrial feedstock, and other applications. SSLNG carriers are vessels with an LNG storage capacity of less than 30,000 cubic meters (m³) for transportation. The typical range of SSLNG storage capacity is between 500 m³ and 5,000 m³. Other elements of SSLNG include LNG bunkering facilities for LNG-fueled vessels, LNG satellite stations, and infrastructure to supply LNG as fuel for road vehicles.

The small-scale LNG market is segmented by type, mode of supply, application, and geography. By type, the market is segmented into liquefaction terminals and regasification terminals. By mode of supply, the market is segmented into truck, transshipment and bunkering, and pipeline and rail. By application, the market is segmented into transportation, industrial feedstock, power generation, and other applications. The report also covers the market size and forecasts for the small-scale LNG market across major regions. For each segment, the market sizing and forecasts were made based on revenue (USD).

| Type | Liquefaction Terminal | ||

| Regasification Terminal | |||

| Mode of Supply | Truck | ||

| Transshipment and Bunkering | |||

| Pipeline and Rail | |||

| Application | Transportation | ||

| Industrial Feedstock | |||

| Power Generation | |||

| Other Applications | |||

| Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)}) | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Russia | |||

| Spain | |||

| NORDIC | |||

| Italy | |||

| Turkey | |||

| Rest of the Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Vietnam | |||

| Malaysia | |||

| Indonesia | |||

| Australia | |||

| Rest of the Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| South Africa | |||

| Egypt | |||

| Qatar | |||

| Nigeria | |||

| Rest of the Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Small Scale LNG Market Research FAQs

How big is the Small-scale LNG Market?

The Small-scale LNG Market size is expected to reach USD 11.81 billion in 2025 and grow at a CAGR of 10.38% to reach USD 19.35 billion by 2030.

What is the current Small-scale LNG Market size?

In 2025, the Small-scale LNG Market size is expected to reach USD 11.81 billion.

Who are the key players in Small-scale LNG Market?

Shell PLC, Linde plc, PJSC Gazprom, Engie SA and Wartsila Oyj ABP are the major companies operating in the Small-scale LNG Market.

Which is the fastest growing region in Small-scale LNG Market?

North America is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Small-scale LNG Market?

In 2025, the Asia-Pacific accounts for the largest market share in Small-scale LNG Market.

What years does this Small-scale LNG Market cover, and what was the market size in 2024?

In 2024, the Small-scale LNG Market size was estimated at USD 10.58 billion. The report covers the Small-scale LNG Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Small-scale LNG Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Small-scale LNG Market Research

Mordor Intelligence provides a comprehensive analysis of the small-scale LNG market, utilizing our extensive expertise in energy sector consulting. Our detailed report covers the entire ecosystem. This includes LNG terminal infrastructure, LNG bunkering operations, LNG fueling station networks, and LNG regasification facilities. The analysis also examines modular LNG solutions, LNG transportation systems, and emerging LNG logistics frameworks. These insights are crucial for stakeholders and are available in an easy-to-read report PDF format for download.

Our research benefits industry participants by offering a detailed examination of LNG power generation applications, LNG peak shaving capabilities, and LNG satellite station implementations. The report explores containerized LNG solutions, LNG storage facility development, and LNG distribution networks. It also includes LNG virtual pipeline systems. Stakeholders gain valuable insights into mini LNG operations, LNG retail opportunities, and the expanding market for LNG terminals. This is supported by comprehensive data on LNG bunkering market trends and regional growth patterns.