Skin Cancer Therapeutics Market Size and Share

Market Overview

| Study Period | 2021 - 2030 |

|---|---|

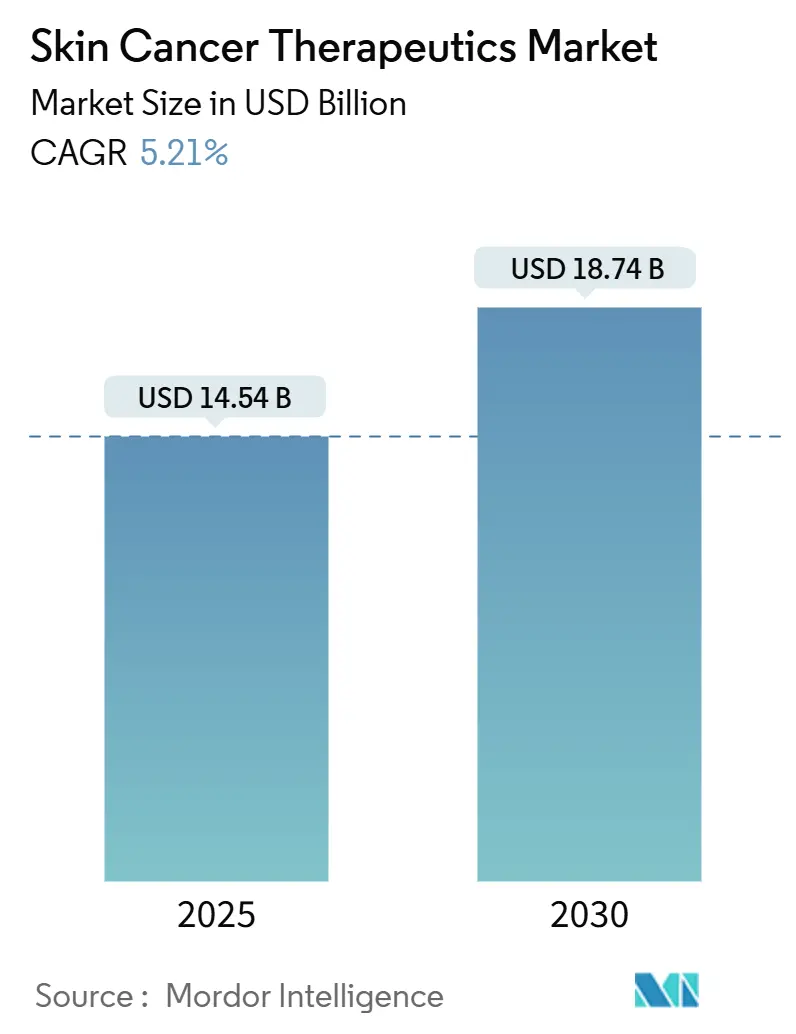

| Market Size (2025) | USD 14.54 Billion |

| Market Size (2030) | USD 18.74 Billion |

| Growth Rate (2025 - 2030) | 5.21% CAGR |

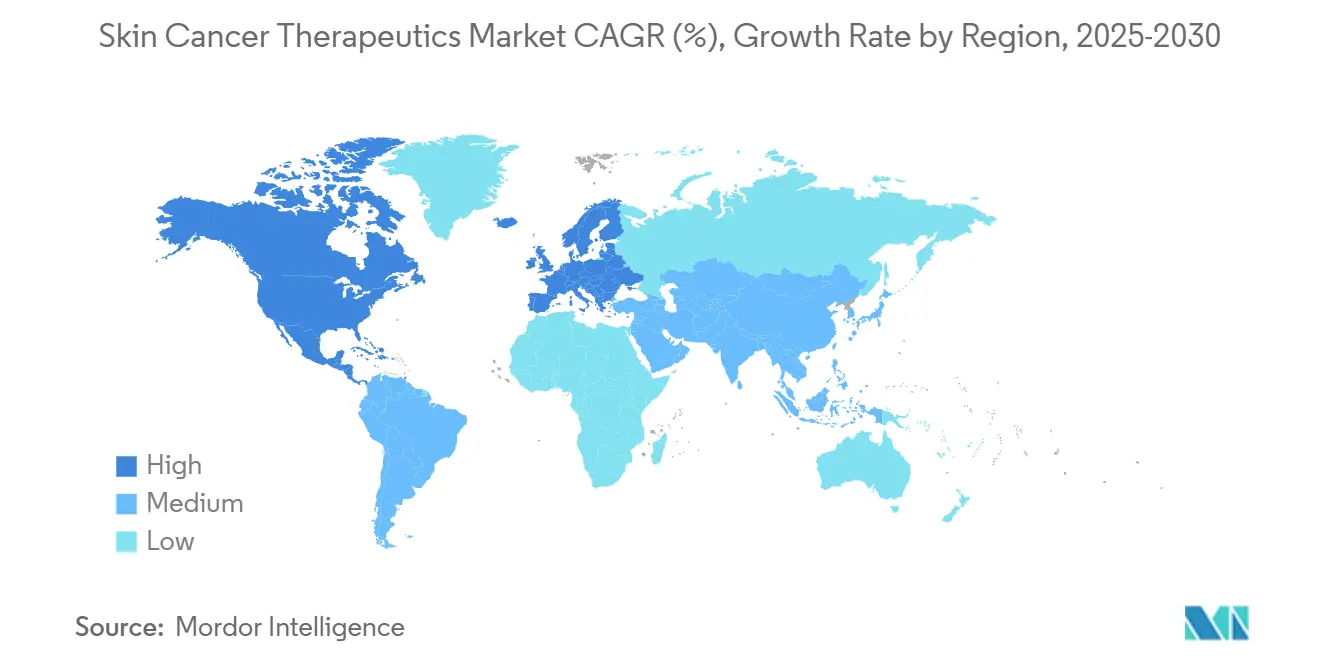

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Skin Cancer Therapeutics Market Analysis by Mordor Intelligence

The skin cancer therapeutics market reached USD 14.54 billion in 2025 and is forecast to advance to USD 18.74 billion by 2030, registering a 5.21% CAGR. The adoption of precision medicine, real-time molecular tests, and artificial-intelligence (AI) decision support is moving care away from stand-alone surgery and toward data-guided therapy selection. AI diagnostic platforms now match specialist performance, posting 96% sensitivity, while mRNA-based vaccines have cut melanoma recurrence rates by 49% in late-stage studies.[1]American Cancer Society, “Cancer Facts & Figures 2025,” cancer.org Regulators are fast-tracking novel agents, payers are broadening reimbursement for tele-dermatology, and investors are funding outpatient delivery models that lower procedure costs. Supply-side dynamics are equally important: pharmaceutical alliances combining checkpoint inhibitors with personalized vaccines, manufacturers embedding AI into therapeutics, and practice consolidations backed by private equity are together reshaping competitive positioning.

Key Report Takeaways

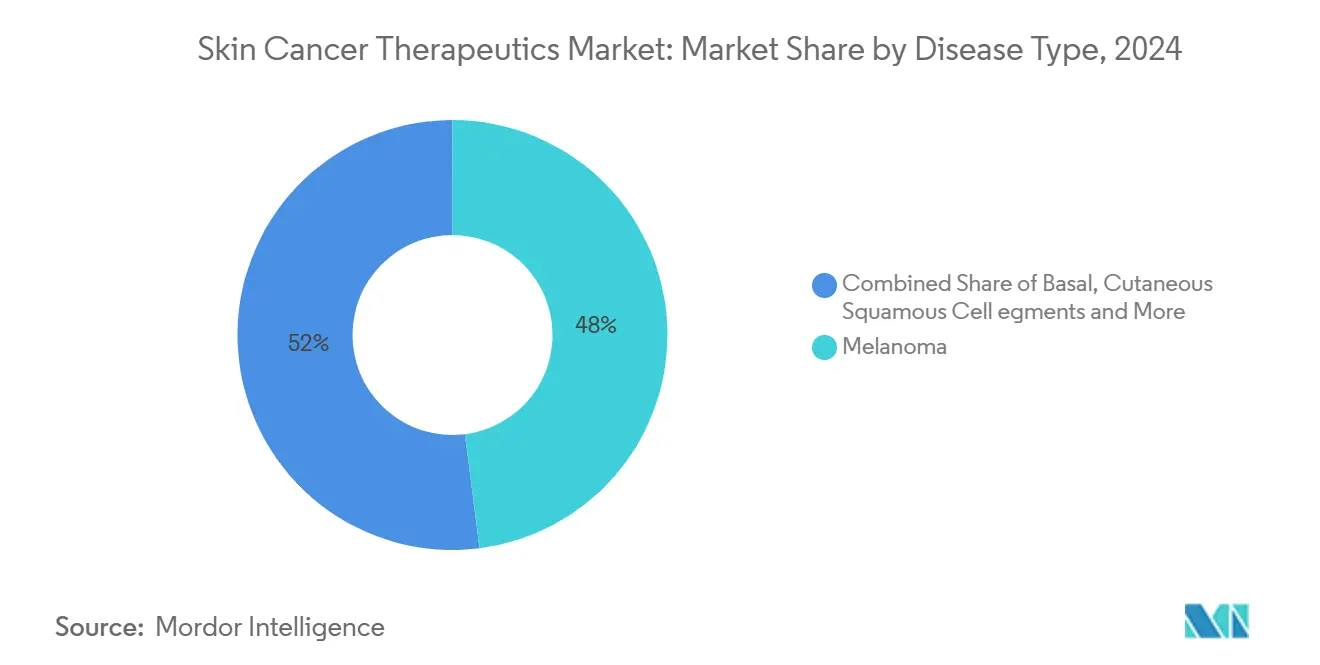

- By disease type, melanoma held 48.0% of the skin cancer therapeutics market share in 2024, while Merkel cell and other rare cancers are projected to expand at a 13.4% CAGR through 2030.

- By treatment modality, immunotherapy led with a 42.3% revenue share in 2024; mRNA-immunotherapy combinations are forecast to grow at a 21.8% CAGR to 2030.

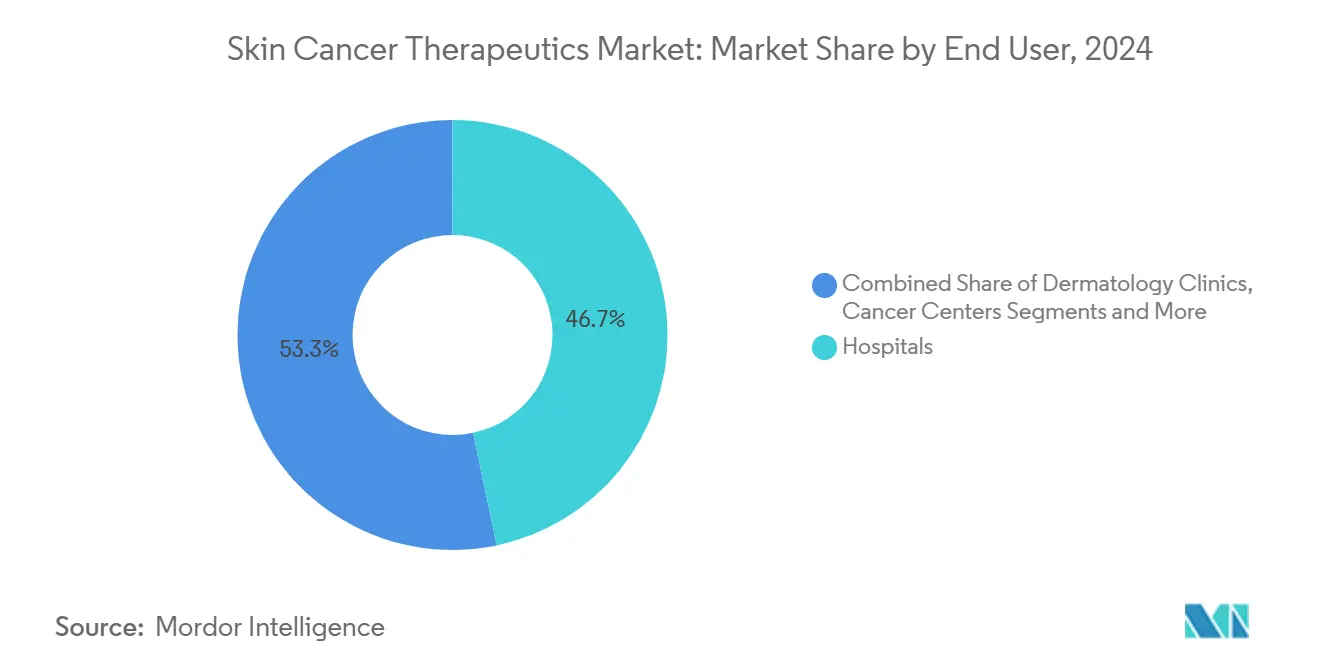

- By end-user, hospitals accounted for 46.7% share of the skin cancer therapeutics market size in 2024; ambulatory surgical centers are advancing at an 11.2% CAGR through 2030.

- By geography, North America commanded a 40.1% share in 2024, while Asia Pacific is set to climb at a 10.3% CAGR to 2030.

Global Skin Cancer Therapeutics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Incidence of Skin Cancer | +1.20% | Global; highest influence in Australia and North America | Long term (≥ 4 years) |

| Growing Approvals of Immune-Oncology Drugs | +2.90% | North America and EU; extending to Asia Pacific | Medium term (2-4 years) |

| Expansion of Targeted BRAF/MEK Inhibitor Therapies | +1.10% | North America, EU, and Asia Pacific precision-medicine hubs | Medium term (2-4 years) |

| Rising Adoption of Hedgehog Pathway Inhibitors in Advanced BCC | +1.20% | North America and EU; uptake beginning in high-income APAC | Short term (≤ 2 years) |

| Emergence of Personalized Neoantigen Cell Therapies | +1.40% | United States and Western Europe; pilot programs in Japan | Medium term (2-4 years) |

| Breakthrough Therapy Designations for Topical Oncolytic Patches | +1.60% | North America and EU dermatology centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Incidence of Skin Cancer

Melanoma cases rose 42% from 2015 to 2025, confirming that aging populations, lifestyle shifts, and environmental pollutants jointly heighten disease burden.[2]U.S. Food and Drug Administration, “Subcutaneous Nivolumab Approved for Solid Tumors,” fda.gov Urban pollution hotspots show unexpectedly high incidence, hinting that airborne carcinogens add to ultraviolet exposure risks. Earlier detection through high-resolution imaging increases case counts yet improves survival, sustaining demand for both diagnostics and therapy. Emerging economies now mirror Western sun-exposure patterns, assuring that the skin cancer therapeutics market will keep expanding even as prevention campaigns intensify.

Growing Approvals of Immune-Oncology Drugs

Regulators accelerate access to novel agents. In 2024, the FDA cleared subcutaneous nivolumab for all solid tumors, the first PD-1 inhibitor delivered outside an infusion suite.[3]U.S. Food and Drug Administration, “Subcutaneous Nivolumab Approved for Solid Tumors,” fda.gov China’s nod for toripalimab as frontline melanoma therapy illustrates regulatory harmonization with Western standards. The ten-year survival of 43% for the nivolumab–ipilimumab doublet sustains premium pricing. Broader indications and simplified dosing support continued uptake across the skin cancer therapeutics market.

Rapid Uptake of Combination mRNA–IO Vaccines

Merck and Moderna’s mRNA-4157, combined with pembrolizumab, cut recurrence risk by 49% and distant metastasis by 62% at nearly three-year follow-up. BioNTech’s BNT111 produced meaningful responses in PD-1-refractory patients, extending benefit to previously untreatable populations. Manufacturing personalization requires robust cold chains and rapid sequencing, but FDA breakthrough designation speeds U.S. review. Platform versatility hints at multi-cancer applications, positioning mRNA technology as a future growth engine for the skin cancer therapeutics market.

Emergence of Personalized Neoantigen Cell Therapies

Personalized neoantigen cell therapies bring precision medicine and immunotherapy together in a single, patient-specific treatment for advanced skin cancer. In February 2024, the FDA cleared Amtagvi (lifileucel), the first tumor-infiltrating lymphocyte therapy for a solid tumor, after it delivered a 31.5% objective response rate in heavily pre-treated melanoma patients. The approach involves harvesting a patient’s own immune cells, expanding the cells in a laboratory, then reinfusing them so they can target that individual’s cancer mutations. Building these “living drugs” demands sophisticated facilities and highly trained staff, which both limit new market entrants and support premium pricing that currently exceeds USD 100,000 per course of therapy.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Therapy & Device Capital Cost | -0.70% | Global; acute in emerging markets | Long term (≥ 4 years) |

| Severe Immune-Related Adverse Events | -0.50% | Global; regulatory focus in developed markets | Medium term (2-4 years) |

| Global Shortage of Trained Dermatologists | -0.40% | Worldwide; most acute in rural regions | Long term (≥ 4 years) |

| AI-Algorithm Racial Bias & Data-Privacy Gaps | -0.30% | Global; under strict scrutiny in the United States & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Therapy & Device Capital Cost

Checkpoint inhibitors exceed USD 23,000 per dose, while tumor-infiltrating lymphocyte therapy can run USD 100,000 per course. MOH's surgery costs climbed even as U.S. Medicare reimbursement fell 46% in real terms from 2007 to 2024. In low-income nations, these prices dwarf annual health budgets, limiting adoption and dragging on the skin cancer therapeutics market. Practice consolidation creates operational savings but can raise patient fees as investors seek returns.

Severe Immune-Related Adverse Events

Combination regimens trigger grade-3/4 toxicities in nearly half of treated patients, including pneumonitis and colitis that demand expensive management. Community oncologists need new training, and hospitals must staff rapid-response teams. Biomarker-based selection mitigates risk but amplifies diagnostic costs. Progress on predictive tests is essential to balance efficacy with safety in the skin cancer therapeutics market.

Segment Analysis

By Disease Type: Melanoma Drives Premium Value Creation

Melanoma controlled 48.0% of the skin cancer therapeutics market in 2024, a commanding position given that the tumor accounts for only 1% of overall cases. Premium drug prices and multidisciplinary management underpin that share. Combination nivolumab–ipilimumab costs exceed USD 100,000 per patient year, reinforcing revenue concentration. Rare entities such as Merkel cell carcinoma are forecast to rise to 13.4% CAGR as diagnostic awareness improves and targeted agents enter the pipeline. Basal cell carcinoma maintains growth through sheer volume, while cutaneous squamous cell carcinoma gains from newly approved antibodies that post 47.4% response rates.

Precision-biopsy tests shrink unnecessary surgery. Castle Biosciences’ DecisionDx-Melanoma guides sentinel-node decisions, cutting morbidity without impairing control. Neoadjuvant therapy trials and mRNA vaccines widen the treatable population to earlier stages. Collectively, these advances protect melanoma’s revenue importance even as other subtypes accelerate.

Note: Segment shares of all individual segments available upon report purchase

By Treatment Modality: Immunotherapy Dominance Faces mRNA Disruption

Immunotherapy contributed 42.3% of 2024 revenue, yet the fastest-growing modality, like mRNA-immunotherapy combinations, will expand at 21.8% CAGR to 2030. Surgery retains a core role, now enhanced by AI-guided imaging that sharpens margin control. Near-infrared photo-immunotherapy blends optical precision with immune activation, lessening collateral tissue damage. Targeted therapy uptake grows as biomarker panels refine patient eligibility, while chemotherapy use retreats.

Algorithm-driven treatment sequencing matches agent choice to evolving tumor biology, cutting unnecessary toxicity. This dynamic keeps the skin cancer therapeutics market fluid, with each modality’s competitive weight shifting as supporting evidence matures.

By End-user: Hospitals Lead While ASCs Accelerate

Hospitals generated 46.7% revenue in 2024, fueled by advanced infusion suites and intensive-care backup. Yet ambulatory surgical centers (ASCs) are growing quickly at an 11.2% CAGR, propelled by minimally invasive devices and payer incentives for lower-cost sites. Dermatology clinics extend their reach with teledermatology triage, while cancer centers focus on high-complexity immunotherapy.

ASCs leverage lean staffing and rapid turnover to lower per-procedure cost, drawing routine excisions and even some Mohs surgeries out of hospitals. Therapeutics in primary care feed ASCs with confirmed cases, making outpatient settings an increasingly important node in the skin cancer therapeutics market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America retained a 40.1% share in 2024 through early technology adoption, dense specialist networks, and favorable reimbursement. Europe follows with harmonized rules and universal-care funding mechanisms.

Asia Pacific records the fastest 10.3% CAGR: China’s NMPA accepted toripalimab for first-line melanoma, and Japan is pioneering boron neutron capture therapy, treating more than 500 patients to date, nature.com.

The Middle East and Africa rely on medical-tourism corridors, while South America benefits from rising public-health budgets. Supply chains are localizing: Chinese contract manufacturers now produce PD-1 antibodies, and Indian device firms supply dermoscopy units. These shifts highlight regional self-sufficiency trends within the skin cancer therapeutics market, even as global companies drive technology transfer alliances.

Competitive Landscape

Market structure is moderately fragmented but tilting toward consolidation. Bristol Myers Squibb, Merck, and Pfizer remain central, anchored by broad immunotherapy portfolios and globally distributed trial networks.

Partnerships redefine boundaries: Moderna and Merck co-develop personalized mRNA vaccines, while Sanofi placed EUR 300 million with Orano Med to access alpha-emitting radioligands. Private-equity funds now back 10-15% of dermatology practices, integrating diagnostics, surgery, and infusion under a single operating umbrella.

Disruptors focus on precision and automation. Castle Biosciences posted 51% revenue growth on molecular tests that address a USD 540 million U.S. opportunity. AI platform vendors secure FDA clearances yet face commercialization risk, as shown by DermTech’s 2024 Chapter 11 filing despite differentiated technology. Competitive advantage increasingly hinges on digital pathology, robotics, and genome-informed therapy design. These assets will decide future share in the skin cancer therapeutics market.

Skin Cancer Therapeutics Industry Leaders

Amgen Inc.

Bristol-Myers Squibb Company

Merck & Co., Inc.

Sun Pharmaceutical Industries Ltd.

Sanofi SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Newcastle University scientists reported that adding the anti-CD30 agent brentuximab vedotin to anti-PD-1 therapy lifted median overall survival by 24% in patients with metastatic melanoma who had failed earlier immunotherapy, offering a hopeful option for a hard-to-treat population.

- May 2025: Dubai-based start-up Medicus secured approval from the UAE Department of Health to launch a basal-cell-carcinoma study, highlighting the Middle East’s growing role in cutting-edge skin-cancer research.

- April 2025: The FDA cleared Sanofi and Regeneron’s Dupixent for a broader range of skin disorders, demonstrating how a blockbuster biologic can extend its reach well beyond atopic dermatitis.

- December 2024: : The FDA authorized subcutaneous nivolumab for all of its current solid-tumour indications, the first time a PD-1 inhibitor can be given outside the infusion chair—an advance expected to ease pressure on oncology clinics while preserving a 24.2% response rate.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the global skin cancer therapeutics market captures all prescription drugs and biologics used to treat melanoma, basal cell carcinoma, cutaneous squamous cell carcinoma, and other rare malignant skin tumors, generating USD 14.54 billion in 2025.

Scope exclusion: diagnostic tests, cosmetic dermatology procedures, radiotherapy equipment, and over-the-counter topicals are outside this study.

Segmentation Overview

- By Disease Type

- Melanoma

- Basal Cell Carcinoma

- Cutaneous Squamous Cell Carcinoma

- Other Rare Skin Cancers

- By Treatment Modality

- Surgery

- Chemotherapy

- Immunotherapy

- Targeted Therapy

- Photodynamic Therapy

- Others

- By End-user

- Hospitals

- Dermatology Clinics

- Cancer Centers

- Ambulatory Surgical Centers

- Research & Academic Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts completed interviews with oncologists, dermatology surgeons, hospital pharmacists, payers, and medical-affairs specialists across multiple countries. Their insights refined real-world dosing patterns, line-of-therapy splits, and expected uptake of next-wave checkpoint inhibitors, enabling strong triangulation with desk findings.

Desk Research

We screened authoritative open sources such as the World Health Organization, SEER, Eurostat cancer registries, and national formularies. We tracked product approvals in the US FDA Orange Book and the EMA database, parsed brand-level sales from 10-K filings via D&B Hoovers, and reviewed news archives on Dow Jones Factiva for launch pricing and competitive signals. Many additional reputable datasets informed our analysis beyond the examples listed here.

Market-Sizing & Forecasting

A top-down incidence-to-treated-patient model converts registry counts into drug-eligible cohorts and values them using weighted average selling prices. Sampled manufacturer revenues and selective channel audits provide bottom-up cross-checks that calibrate totals. Core variables include incidence growth, therapy penetration, biosimilar price erosion, approval cadence, and median course intensity. A multivariate regression projects values through 2030, with scenario overlays for breakthrough approvals.

Data Validation & Update Cycle

Outputs pass anomaly scans, senior analyst reviews, and client-facing sanity checks. Models refresh annually, with mid-cycle revisions whenever landmark approvals or epidemiological shifts materially impact assumptions.

Why Mordor's Skin Cancer Therapeutics Baseline Commands Reliability

Published figures differ because publishers choose distinct therapy baskets, geographies, and price assumptions, creating wide swings in reported values. Mordor's disciplined scope alignment, yearly refresh, and cross-method validation limit such drifts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.54 Bn (2025) | Mordor Intelligence | |

| USD 10.30 Bn (2025) | Global Consultancy A | counts only small-molecule drugs and omits biologics that dominate first-line therapy |

| USD 11.10 Bn (2024) | Trade Journal B | rolls forward historic sales without adjusting for accelerating immunotherapy uptake |

| USD 10.61 Bn (2024) | Regional Consultancy C | excludes emerging Asia-Pacific markets and applies fixed 2023 exchange rates |

These contrasts show that Mordor's wider therapy scope, dynamic price modeling, and timely refresh produce the most dependable baseline for strategic planning.

Key Questions Answered in the Report

What is the current size of the skin cancer therapeutics market?

The skin cancer therapeutics market stood at USD 14.54 billion in 2025 and is projected to reach USD 18.74 billion by 2030.

Which segment holds the largest revenue share?

Melanoma accounted for 48.0% of 2024 revenue, underscoring its premium pricing and high mortality despite low case volume.

How fast is the ambulatory surgical center segment growing?

Ambulatory surgical centers are forecast to expand to an 11.2% CAGR from 2025 to 2030 due to lower procedural costs and minimally invasive technology.

Why is Asia Pacific the fastest-growing region?

Asia Pacific benefits from rising middle-class demand, improved infrastructure, and regulatory moves like China’s approval of toripalimab, resulting in a 10.3% CAGR outlook.

What innovations are likely to shape future therapeutic strategies?

Personalized mRNA vaccines combined with checkpoint inhibitors, AI-guided dermoscopy, and radioligand therapy platforms are expected to redefine standard care pathways over the next five years.

Page last updated on: