Market Size of Global Single Use Plastic Packaging Industry

| Study Period | 2019 - 2029 |

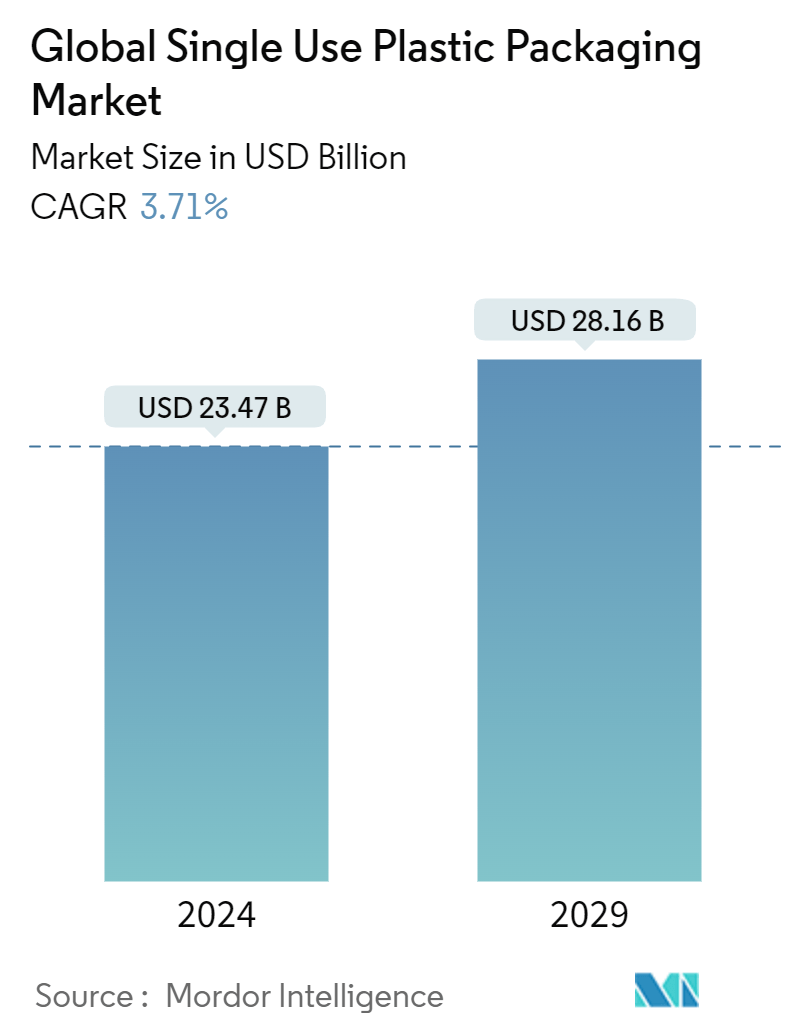

| Market Size (2024) | USD 23.47 Billion |

| Market Size (2029) | USD 28.16 Billion |

| CAGR (2024 - 2029) | 3.71 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order |

Single Use Plastic Packaging Market Analysis

The Global Single Use Plastic Packaging Market size is estimated at USD 23.47 billion in 2024, and is expected to reach USD 28.16 billion by 2029, growing at a CAGR of 3.71% during the forecast period (2024-2029).

- The expanding urban population drives the demand for prepared and ready-to-eat food products, significantly influencing food service packaging trends. This trend is expected to increase the demand for single-use plastic packaging solutions during the forecast period. Consumers in urban areas often have busier lifestyles and less time for meal preparation, leading to a greater reliance on convenience foods that require efficient packaging.

- The rise of food delivery services and takeaway options in cities has further amplified this demand. In key regions, urbanization, lifestyle changes, adaptation to fast-paced work environments, and increased reliance on online food platforms rapidly transform the foodservice industry dynamics, further boosting the demand for single-use plastic packaging solutions. These factors collectively contribute to a growing market for packaging that prioritizes convenience, portability, and food preservation, characteristics often associated with single-use plastic packaging in the foodservice industry.

- The growth of end users, including quick-service restaurants, full-service restaurants, coffee shops, snack outlets, and institutional facilities, drives the demand for convenient packaging solutions. This trend is expected to increase the production of single-use packaging formats. The shift from rigid to flexible packaging is gaining momentum as consumers seek convenience and adapt to changing lifestyles, particularly in smaller households. Consequently, single-use plastic packaging is experiencing increased popularity across various food service segments.

- The rapid expansion of fast-food franchises and quick-service restaurants drives the market's growth, responding to changing demographics, employment patterns, and lifestyles. Fast food's affordability and quick preparation times align with consumers' demand for convenient meal options. This global increase in fast food consumption directly supports the growth of single-use plastic packaging in the food service industry.

- The growing demand for consumer convenience is a crucial factor driving the single-use plastic packaging market. Manufacturers adapt to evolving customer preferences by offering packaging solutions catering to these changing needs. The busy lifestyles of working professionals have increased the demand for convenient food packaging options. Additionally, producers are now considering post-use disposal, leading to the development of packaging items that can be easily discarded.

- Regulations on single-use plastics and the growing preference for sustainable packaging alternatives, such as fiber and paper-based products, challenge the market's growth. These regulations aim to reduce plastic waste and promote environment-friendly packaging solutions. The shift towards sustainable alternatives is driven by both consumer demand and governmental policies.

- Increasing consumer awareness about the environmental impact of single-use plastics and unsustainable practices has led to demands for higher development standards with positive ecological outcomes. This awareness has prompted many consumers to actively seek out products with eco-friendly packaging, putting pressure on companies to adapt their packaging strategies. As a result, businesses across various industries are investing in research and development of innovative, sustainable packaging solutions to meet these evolving consumer expectations and comply with regulatory requirements.

Single Use Plastic Packaging Industry Segmentation

Single-use plastic packaging refers to disposable containers, wrappers, and other packaging materials made from plastic designed to be used only once before being discarded or recycled. These items are typically used for food, beverages, consumer goods, and various other products, serving the purpose of protection, preservation, and convenience during transportation and storage. Single-use plastic packaging encompasses many products, including plastic bags, food containers, beverage bottles, cutlery, straws, and packaging films. These materials are often lightweight, cost-effective, and provide excellent barrier properties against moisture, oxygen, and contaminants.

The single-use plastic packaging market is segmented by material (polylactic acid [PLA], polyethylene terephthalate [PET], polyethylene [PE], and other material types), product type (bottles, bags and pouches, clamshells, trays, cups and lids, and other product types), end user (quick-service restaurants, full-service restaurants, institutional, retail, and other end users), and geography (North America [United States, Canada], Europe [Germany, United Kingdom, France, Italy, and Rest of Europe], Asia-Pacific [China, Japan, India, Australia and New Zealand, and Rest of Asia-Pacific], Latin America [Brazil, Mexico, Columbia, and Rest of Latin America], Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Material | |

| Polylactic Acid (PLA) | |

| Polyethylene Terephthalate (PET) | |

| Polyethylene (PE) | |

| Other Material Types |

| By Product Type | |

| Bottles | |

| Bags and Pouches | |

| Clamshells | |

| Trays, Cups, and Lids | |

| Other Product Types |

| By End User | |

| Quick Service Restaurants | |

| Full Service Restaurants | |

| Institutional | |

| Retail | |

| Other End Users |

| By Geography*** | ||||||

| ||||||

| ||||||

| ||||||

| ||||||

|

Global Single Use Plastic Packaging Market Size Summary

The global single-use plastic packaging market is experiencing a notable expansion, driven by the increasing demand for convenience and utility in packaging solutions. The COVID-19 pandemic significantly impacted consumer behavior, leading to a surge in demand for single-use packaging, particularly in the food and beverage sector. This demand was further fueled by the rise in online food delivery services, which rely heavily on single-use packaging for efficiency and hygiene. Despite environmental concerns, the lightweight and durable properties of single-use plastics continue to make them a preferred choice for many industries. However, the market is also witnessing a shift as companies explore alternatives, such as natural fiber-based packaging, in response to regulatory pressures and changing consumer preferences.

The market is characterized by a high level of competition, with key players like Dart Container Corporation, Georgia-Pacific LLC, and Graphic Packaging International, Inc. dominating the landscape. These companies are actively engaging in strategic partnerships and innovations to enhance their market presence and address environmental challenges. The use of polyethylene terephthalate (PET) remains predominant due to its versatility and recyclability, although the effectiveness of recycling initiatives varies by region. Government regulations and initiatives, such as the EU's Single-Use Plastic Directive and the US Department of Energy's funding for advanced recycling technologies, are influencing market dynamics, potentially leading to a more sustainable future for single-use packaging.

Global Single Use Plastic Packaging Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Consumers

-

1.2.3 Threat of New Entrants

-

1.2.4 Threat of Substitutes

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Industrial Value Chain Analysis

-

-

2. MARKET SEGMENTATION

-

2.1 By Material

-

2.1.1 Polylactic Acid (PLA)

-

2.1.2 Polyethylene Terephthalate (PET)

-

2.1.3 Polyethylene (PE)

-

2.1.4 Other Material Types

-

-

2.2 By Product Type

-

2.2.1 Bottles

-

2.2.2 Bags and Pouches

-

2.2.3 Clamshells

-

2.2.4 Trays, Cups, and Lids

-

2.2.5 Other Product Types

-

-

2.3 By End User

-

2.3.1 Quick Service Restaurants

-

2.3.2 Full Service Restaurants

-

2.3.3 Institutional

-

2.3.4 Retail

-

2.3.5 Other End Users

-

-

2.4 By Geography***

-

2.4.1 North America

-

2.4.1.1 United States

-

2.4.1.2 Canada

-

-

2.4.2 Europe

-

2.4.2.1 Germany

-

2.4.2.2 United Kingdom

-

2.4.2.3 France

-

2.4.2.4 Italy

-

-

2.4.3 Asia-Pacific

-

2.4.3.1 China

-

2.4.3.2 Japan

-

2.4.3.3 India

-

2.4.3.4 Australia and New Zealand

-

-

2.4.4 Latin America

-

2.4.4.1 Brazil

-

2.4.4.2 Mexico

-

2.4.4.3 Columbia

-

-

2.4.5 Middle East and Africa

-

2.4.5.1 United Arab Emirates

-

2.4.5.2 Saudi Arabia

-

2.4.5.3 South Africa

-

-

-

Global Single Use Plastic Packaging Market Size FAQs

How big is the Global Single Use Plastic Packaging Market?

The Global Single Use Plastic Packaging Market size is expected to reach USD 23.47 billion in 2024 and grow at a CAGR of 3.71% to reach USD 28.16 billion by 2029.

What is the current Global Single Use Plastic Packaging Market size?

In 2024, the Global Single Use Plastic Packaging Market size is expected to reach USD 23.47 billion.