Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2025 - 2031 |

| Market Size (2025) | USD 262.84 Million |

| Market Size (2031) | USD 405.19 Million |

| Growth Rate (2025 - 2031) | 7.48% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Travel Retail Market Analysis by Mordor Intelligence

The Singapore travel retail market size reached USD 262.84 million in 2025 and is projected to reach USD 405.19 million by 2031 at a 7.48% CAGR. The Singapore travel retail market is expanding as growth shifts from pure visitor volumes toward higher spending intensity per traveler, which supports premium and high-margin retail categories. Even with visitor numbers still normalizing, travelers are spending more on luxury, beauty, and premium alcohol, reinforcing the resilience of duty-free sales. This trend particularly benefits airport and cruise retail channels, where impulse and premium purchases remain strongest. Changi Airport’s recovery as a major global hub continues to anchor the market, providing consistently high passenger throughput that sustains retail demand. Market growth is further supported by Singapore’s positioning as a regional launchpad for luxury and global brands, which encourages experiential and discovery-led shopping. While shopping’s share of total tourism spending has moderated, the absolute value of high-quality duty-free transactions continues to rise due to premiumization. Retailers and brands are increasingly leveraging omnichannel strategies, digital engagement, and pre-travel targeting to stimulate demand before passengers arrive at the airport.

Key Report Takeaways

- By product type, Cosmetics & Fragrances led with 42.24% of the Singapore travel retail market share in 2025; Wines & Spirits is forecast to expand at an 8.11% CAGR through 2031.

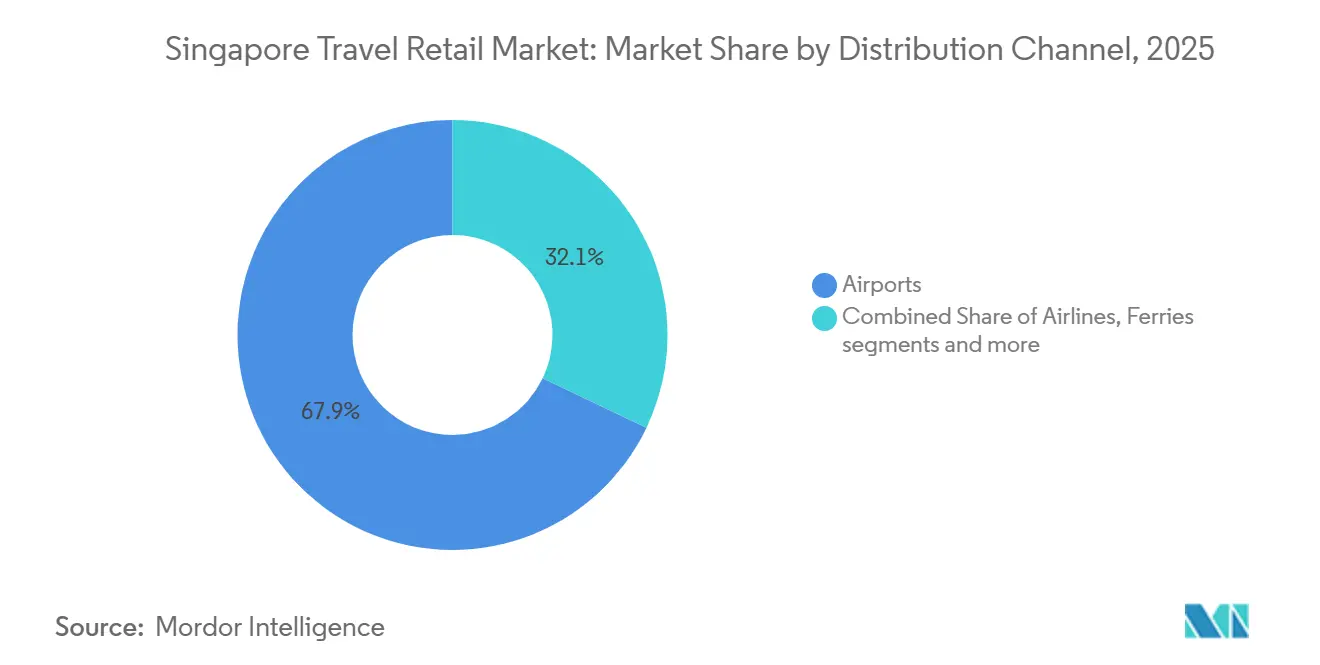

- By distribution channel, Airports held 67.90% of the Singapore travel retail market share in 2025, while the same channel is projected to grow at a 7.88% CAGR through 2031.

- By geography, the East Region accounted for 82.25% of the Singapore travel retail market share in 2025 and is set to grow at an 8.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Travel Retail Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Experiential retail-tainment boosting spend-per-passenger | +1.2% | Global, peak impact East Region (Changi Airport) | Medium term (2-4 years) |

| Omni-channel pre-order and click-and-collect at Changi | +0.9% | East Region (Changi ecosystem), expanding to Central/West via iShopChangi | Short term (≤ 2 years) |

| Surge in premium beauty and niche perfumes from Gen-Z tourists | +1.5% | Global, over-indexed by India, Southeast Asia, South Korea | Medium term (2-4 years) |

| Cruise-terminal expansion unlocking non-airport duty-free traffic | +0.7% | Central/South (Marina Bay), East (Tanah Merah) | Long term (≥ 4 years) |

| GST hike pulls forward high-ticket purchases | +0.4% | National, with early gains in the Central Region and East | Short term (≤ 2 years) |

| Pentarchy data-sharing lifting conversions | +1.1% | East Region (Changi partnerships), roll-out to Marina Bay cruise hub | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Experiential "Retail-tainment" Strategies Boosting Spend-Per-Passenger

Immersive activations across Changi and Jewel focus on turning dwell time into high-value purchases with multi-sensory formats and exclusive premieres. L’Oréal Travel Retail Asia Pacific’s “Beauty Shopper-tainment of the Future” and wide-scale, multi-terminal brand experiences illustrated how activation breadth increases reach and strengthens conversion among international travelers moving through multiple terminals[1]Source: Singapore Economic Development Board, “L’Oréal Showcases Travel Retail Beauty at TFWA 2025,” Singapore EDB, edb.gov.sg. SkinCeuticals’ first global travel retail presence at Terminal 3 introduces professional-grade skincare diagnostics into the airport setting, aligning premium skincare with unhurried transit moments that encourage consultation-led purchasing. Stronger spending intensity per traveler supports these high-end, experiential concepts even as overall visitor volumes continue to normalize. The East Region’s integrated retail ecosystem, led by Jewel, reinforces this dynamic through rising footfall and improving sales productivity. The Singapore travel retail market benefits from a flywheel where each high-profile activation reinforces brand discovery, compounding returns as passengers circulate across terminals and the Jewel precinct.

Omni-Channel Pre-Order & Click-and-Collect Adoption at Changi

Omnichannel pre-order and click-and-collect capabilities at Changi are a structural growth driver for the Singapore travel retail market, as they redefine when and how consumers engage with duty-free shopping. By shifting purchase decisions upstream to the planning phase of a journey, retailers capture intent earlier and reduce reliance on in-terminal impulse alone. The ability to serve both travelers and non-travelers through digital storefronts keeps assortments visible year-round rather than limited to airport dwell time. A fully integrated digital ecosystem aligns inventory, pricing, promotions, and content across physical and online channels, improving execution efficiency and minimizing lost sales from stockouts. Loyalty programs and data-enabled partnerships allow targeted engagement based on travel behavior, increasing conversion and basket size. Convenience, certainty of availability, and frictionless fulfillment strengthen consumer trust, particularly in premium beauty and liquor categories. Together, these omnichannel mechanics expand the effective selling window around each trip and create a more stable, scalable demand engine for travel retail[2]iShopChangi, “Shop Tax-Free Anytime, Anywhere,” iShopChangi, ishopchangi.com..

Cruise-Terminal Expansion Unlocking Non-Airport Duty-Free Traffic

Marina Bay and Singapore Cruise Centre together create a second growth leg by opening access to ferry and cruise passengers whose dwell times are typically longer than airport flows. The award of a long-term master duty-free and general merchandise concession at Singapore Cruise Centre to Lagardère Travel Retail in May 2025 established a broader footprint across HarbourFront Passenger Terminal and Tanah Merah Ferry Terminal, with operations slated to begin from July 2025 after phased upgrades. The Singapore travel retail market stands to gain as this concession brings consistent brand standards and category depth to sea terminals that connect directly to regional leisure corridors. Operator investments in refreshed layouts and convenience-led merchandising at ferry and cruise touchpoints work in tandem with airport activations to boost total traveler reach across gateways. As sea- and air-side programs align, the addressable audience expands to travelers who do not pass through air-side retail, lifting the ecosystem’s resiliency to seasonal air traffic swings. This structural expansion reduces concentration risk by adding non-airport duty-free nodes that are coordinated with airport promotions through shared loyalty and digital campaigns where feasible[3]Lagardère Travel Retail, “Lagardère Travel Retail Secures Long-Term Master Duty-Free & General Merchandise Concession at Singapore Cruise Centre,” Lagardère, lagardere.com..

GST Hike Pull-Forward of High-Ticket Purchases

The January 1, 2024, GST rate increases from 8% to 9% influenced pre-hike buying patterns for luxury goods and electronics, a common pull-forward dynamic when net payable tax rises year-on-year[4]Inland Revenue Authority of Singapore, “GST Rate Change for Consumers,” Inland Revenue Authority of Singapore, iras.gov.sg. Retailers prepared tactical promotions to smooth demand around the transition, while duty-free channels maintained category-specific concessions that preserved some price advantages relative to downtown retail. At the airport, this was complemented by omnichannel initiatives on iShopChangi that emphasize pre-order certainty and bundled offers to encourage conversion despite the rate change. Changi Airport’s FY2024/25 results signalled improved operating momentum supported by traffic recovery, even as global economic conditions tempered concession revenue growth in the period. The Singapore travel retail market has adapted to a higher GST baseline by leaning into differentiated experiences and duty-free allowances where permitted, keeping conversion strong for high-ticket categories where shoppers still value the combined benefits of convenience, authenticity, and curated exclusivity.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China's price convergence is eroding Singapore’s duty-free advantage | -1.3% | Global, acute for the East Region on beauty and spirits | Medium term (2-4 years) |

| Anti-daigou enforcement limiting bulk buys | -0.6% | National, disproportionate at Changi and Marina Bay checkpoints | Short term (≤ 2 years) |

| Rising concession and workforce costs | -0.8% | National, particularly the East and Central regions | Long term (≥ 4 years) |

| Health-driven curbs on tobacco and alcohol allowances | -0.4% | National, with periodic tightening by health authorities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

China Price Convergence Eroding Singapore’s Duty-Free Advantage

Regional price differentials have narrowed as offshore duty-free zones in China and upgraded airport retail offer competitive pricing and expanded allowances, reducing pure price-led arbitrage for mass prestige SKUs. This shift drives Singapore operators to emphasize exclusive products, early launches, and experiential formats that preserve differentiation when baseline prices converge. The Singapore travel retail market’s response is to focus on scarcity value and curated assortments that are difficult to replicate elsewhere, while amplifying the omnichannel pre-order model to lock in intent earlier in the journey. Singapore’s diversified source market mix, which includes China as a top visitation source in 2024, helps sustain category traffic even as relative price advantages ease. The net effect is a compositional shift from volume-driven cosmetics toward niche beauty, prestige spirits, and exclusive editions that better withstand price-based competition.

Anti-Daigou Enforcement Limiting Bulk Buys

Stricter enforcement against daigou and bulk-buy activities acts as a restraint on the Singapore travel retail market by limiting high-volume, repeat purchases intended for resale. Enhanced customs controls and clearer digital declaration processes have reduced opportunities for tax and duty arbitrage, discouraging purchases that previously inflated category volumes. As compliance becomes more rigorous, opportunistic bulk buying declines, particularly in categories prone to gray-market leakage. While this shift supports long-term brand equity and protects retail margins, it also reduces transaction throughput from high-frequency buyers. Retailers are therefore compelled to rebalance assortments toward premium products with higher single-item values and to focus on loyalty-driven, legitimate consumer demand rather than resale-oriented purchases.

Segment Analysis

By Product Type: Beauty Premiumization and Spirits Diversification Reshape Category Economics

Cosmetics & Fragrances commands 42.24% of the Singapore travel retail market share in 2025, while Wines & Spirits is projected as the fastest-growing category at an 8.11% CAGR through 2031. This divergence is driven by rising interest in niche fragrances and advanced skincare concepts that thrive on airport-led discovery and consultation, lifting spend per passenger even as visitor volumes continue to normalize. Changi Airport and Jewel reinforce beauty’s role as a first-look channel through exclusive launches and immersive counters, including professional-grade skincare formats that translate engagement into higher-value baskets.

The strong outlook for wines and spirits is underpinned by premiumization, curated assortments, and limited-edition offerings that appeal to travelers seeking rarity and storytelling rather than price arbitrage. Omnichannel previews and pre-travel engagement further support intent-building ahead of departure, enhancing conversion at the airport. Food and confectionery operators are increasingly emphasizing quality, provenance, and trusted labeling to appeal to discerning international travelers, while tobacco faces structural constraints from strict regulatory policies. As a result, space and investment continue to shift toward high-margin beauty and prestige spirits, with slower categories refined to protect overall profitability.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Airports Consolidate Dominance Through Omnichannel Integration and Infrastructure Expansion

Airports held a 67.90% share in 2025 and are projected to grow fastest at a 7.88% CAGR, with the channel benefiting from traffic normalization and the reach of iShopChangi as a digital extension of airport retail. Changi Airport continues to function as the primary sales engine, supported by ongoing terminal enhancements that sustain strong category breadth and premium shopping experiences. The integration of iShopChangi extends airport retail beyond physical dwell time, allowing travelers to engage with assortments before departure and outside peak travel windows. This omnichannel model shifts purchasing decisions earlier in the journey and improves conversion efficiency. As digital and physical activations become more synchronized, the airport channel’s influence on overall market growth continues to strengthen.

Beyond airports, complementary channels add depth to Singapore’s travel retail distribution ecosystem. Airlines play an important role in product discovery and impulse purchasing, particularly on long-haul routes where browsing time is longer and fulfillment can be seamlessly linked to airport collection. Ferry and cruise terminals are emerging as meaningful growth nodes as duty-free operations expand and store formats are refreshed to capture rising passenger flows. Downtown and border retail remain more limited in scale, but virtual downtown concepts anchored by airport marketplaces extend duty-free access to residents under defined conditions.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The East Region holds 82.25% share in 2025 and is forecast to grow at 8.32% CAGR through 2031, driven by the synergy between Changi Airport and Jewel, which together attract both travelers and residents. Jewel has become a destination in its own right, with strong footfall and increasing international visitor engagement validating its role as a hub for retail-led experiences. Changi’s traffic recovery further reinforces the region’s retail base, supporting anchor categories and a robust calendar of activations. The concentration of shoppers in the East enables sustained spend per passenger and strengthens the overall market ecosystem. Retail growth in this region is expected to continue as long as Changi remains the primary gateway and Jewel expands its attractions and experiences.

Long-term capacity growth is anchored by Terminal 5, which will significantly increase passenger throughput and strengthen the East Region’s retail potential. The “T5 In the Making” exhibition highlights design innovations and engages the public while linking visitors to on-terminal promotions, demonstrating how infrastructure development and retail programming are integrated. Planned expansions, including seamless transfers and multimodal access, reinforce the retail campus effect, encouraging repeat visits across multiple terminals. Retailers are aligning activation roadmaps with T5’s phased development to maximize engagement ahead of the terminal’s opening. This coordinated approach ensures shopper interest and market momentum are sustained even during the construction phase.

Other regions provide complementary opportunities but remain secondary to the East. The Central Region benefits from luxury shopping corridors, business hubs, and MICE-driven downtown retail, while cruise terminals create additional duty-free touchpoints for leisure travelers. North-East, North, and West regions see limited travel retail penetration due to fewer international gateways and smaller air- or seaside retail presence. Nationwide digital channels, including airport marketplace delivery services, help extend reach to residents and off-peak travelers. Across all regions, category depth, activation quality, and omnichannel convenience continue to shape how and where shoppers engage with the travel retail ecosystem.

Competitive Landscape

The Singapore travel retail market is highly concentrated, with a few leading players controlling most of the sector. Despite this, competitive intensity remains strong as experiential retail, premium activations, and omnichannel strategies raise the bar for conversion and loyalty. Airport-owned digital marketplaces, such as iShopChangi, extend retailers’ reach beyond terminal shoppers, engaging non-travelers through eligibility-based promotions and partnerships with airlines and banks. Brand-led campaigns and early product launches leverage the airport’s role as a showcase for international travelers, driving high-velocity sales and reinforcing premium positioning. While scale provides advantages, the gap in performance is increasingly determined by the ability to connect pre-trip intent with in-terminal engagement through data-driven strategies.

Strategic collaborations linking airlines, airports, payment networks, retailers, and brands are shaping integrated customer journeys, layering incentives without overburdening any single partner. Partnerships like Jewel Changi Airport and Mastercard illustrate the commercial power of coordinated campaigns that boost card transactions and cross-border spend among international visitors. Large-scale brand activations, such as those by L’Oréal Travel Retail Asia Pacific, demonstrate how multi-brand and single-brand experiences at terminal scale can drive visibility, engagement, and conversion across diverse traveler segments. The market increasingly rewards operators who can harness audience data to retarget travelers with timely, relevant offers. This partnership-driven approach strengthens incumbents’ competitive moat while allowing challenger brands to grow through targeted, event-led initiatives.

Expansion beyond airports into ferry and cruise terminals is diversifying traffic sources and complementing air-side retail flows. Programs such as Lagardère Travel Retail’s initiatives at HarbourFront and Tanah Merah Ferry Terminals bring unified brand standards, improving category depth and reducing fragmentation in non-airport nodes. Integration with airport promotions and loyalty mechanisms helps extend reach to travelers who bypass airside stores, enhancing overall market coverage. The competitive playbook now combines airport category leadership, omnichannel engagement via iShopChangi, and selective expansion into sea terminals to maximize retail team and inventory utilization. In this environment, innovation in activation, personalization, and experience delivery has become a key lever for sustaining growth and differentiation.

Singapore Travel Retail Industry Leaders

The Shilla Duty Free

Lotte Duty Free

Lotte Duty Free

Changi Airport Group

Lagardère Travel Retail

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: Changi Airport has launched an immersive public exhibition called “T5 In the Making” that showcases the vision, design, and innovations behind its upcoming Terminal 5, offering visitors an early glimpse into Singapore’s future aviation hub.

- October 2025: Jewel Changi Airport has renewed its strategic collaboration with Mastercard to continue boosting visitor engagement and spending through exclusive cardholder privileges across retail, dining, and leisure at Jewel.

- May 2025: Lagardère Travel Retail has secured the long‑term master duty‑free and general merchandise concession at Singapore Cruise Centre’s HarbourFront Passenger Terminal and Tanah Merah Ferry Terminal, marking a strategic expansion beyond airport retail.

- January 2025: Jewel Changi Airport announced plans to enhance its tenancy mix with close to 30 new brands in 2025, including a flagship concept store and several global debuts and F&B concepts, reinforcing the destination’s appeal to both overseas visitors and residents.

Singapore Travel Retail Market Report Scope

Travel retail is commonly used to describe the duty-free retail industry and all retail activities dedicated to travelers and tourists. A complete background analysis of the market, including the analysis of market size and forecast, market shares, industry trends, growth drivers, and vendors, is provided. The study also includes insights into market segmentation by product type and by distribution channel. Singapore's travel retail market is segmented by product type into beauty and personal care, wines and spirits, tobacco, edibles, fashion accessories and hard luxury, and other types. The distribution channel segments the market into airports, airlines, ferries, and other distribution channels.

The report offers market size and forecasts for Singapore's travel retail market in terms of value (in USD) for all the above segments.

By Product Type

| Fashion & Accessories |

| Jewelry & Watches |

| Wines & Spirits |

| Food & Confectionery |

| Cosmetics & Fragrances |

| Tobacco |

| Other Product Types (Stationery, Electronics, etc.) |

By Distribution Channel

| Airports |

| Airlines |

| Ferries |

| Other Channels (Railway Stations, Border Shops, Downtown) |

By Geography

| Central Region |

| East Region |

| North Region |

| North-East Region |

| West Region |

| By Product Type | Fashion & Accessories |

| Jewelry & Watches | |

| Wines & Spirits | |

| Food & Confectionery | |

| Cosmetics & Fragrances | |

| Tobacco | |

| Other Product Types (Stationery, Electronics, etc.) | |

| By Distribution Channel | Airports |

| Airlines | |

| Ferries | |

| Other Channels (Railway Stations, Border Shops, Downtown) | |

| By Geography | Central Region |

| East Region | |

| North Region | |

| North-East Region | |

| West Region |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and growth outlook for the Singapore travel retail market?

The Singapore travel retail market size was USD 262.84 million in 2025 and is projected to reach USD 405.19 million by 2031 at a 7.48% CAGR, supported by higher spend-per-passenger and the expansion of omnichannel models.

Which product categories are performing best within Singapore travel retail?

Cosmetics & Fragrances led in 2025 with 42.24% share, while Wines & Spirits is set to grow fastest at an 8.11% CAGR through 2031, reflecting premiumization and exclusive launches that raise basket values.

How critical are airports to Singapore’s travel retail performance?

Airports held a 67.90% share in 2025 and are projected to grow at a 7.88% CAGR, with Changi’s traffic recovery and iShopChangi’s pre-order and non-traveler services extending the effective selling window across the trip.

Why does the East Region dominate Singapore travel retail?

The East Region accounted for 82.25% in 2025 and is forecast at an 8.32% CAGR through 2031 due to the Changi-Jewel ecosystem’s combined footfall, destination retail, and strong activation pipeline supported by capacity expansion.

What role does data-sharing play in improving conversion in Singapore travel retail?

Ecosystem partnerships linking airlines, airports, brands, retailers, and payment networks enable targeted promotions, loyalty linkages, and live commerce pilots that increase pre-trip intent and in-terminal conversion.