Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

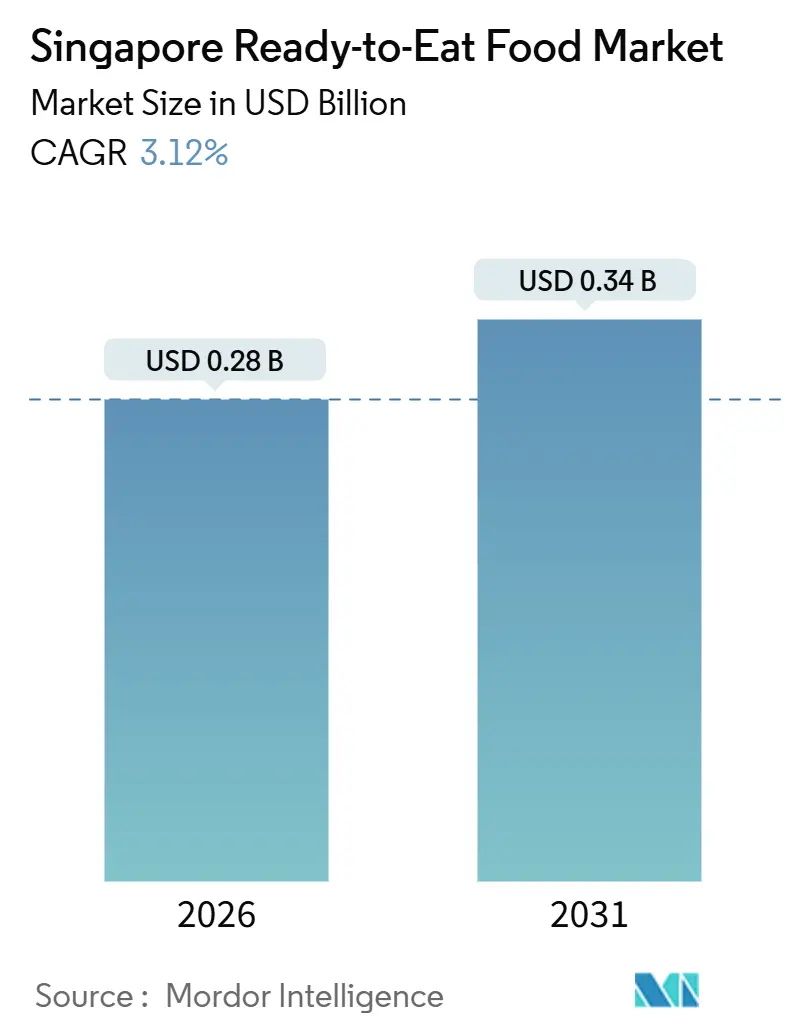

| Market Size (2026) | USD 0.28 Billion |

| Market Size (2031) | USD 0.34 Billion |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Singapore Ready-to-Eat Food Market Analysis by Mordor Intelligence

The Singapore ready-to-eat food market size is valued at USD 0.28 billion in 2026 and is projected to reach USD 0.34 billion by 2031, registering a 3.12% CAGR over the forecast period. Demand momentum rests on time-pressed urban households that are willing to pay for convenience even while the nation’s vibrant hawker culture continues to command habitual meal occasions. Dual-income families, growing e-commerce penetration, functional product upgrades, and packaging technologies that lengthen shelf life collectively sustain incremental volume gains. Private-label expansion by leading grocery chains is squeezing branded profit pools, prompting incumbents to use health claims, ethnic flavors, and alternative proteins to justify price premiums. Meanwhile, Singapore’s clear regulatory pathway for novel foods positions it as a regional launchpad for cultivated meat and precision-fermentation ingredients, further diversifying the offer set within the Singapore ready-to-eat food market.

Key Report Takeaways

- By product type, Ready Meals led with 38.28% of the Singapore ready-to-eat food market share in 2025, and Instant Soups and Snacks are projected to expand at a 4.28% CAGR through 2031.

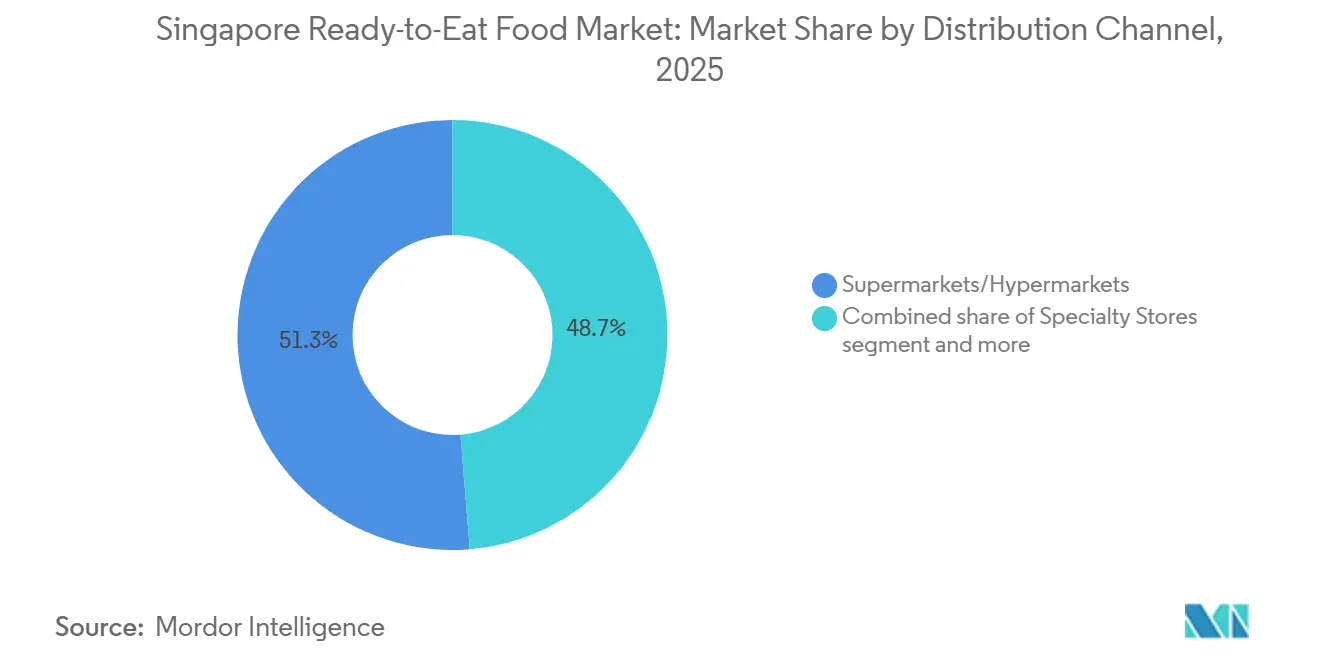

- By distribution channel, Supermarkets and Hypermarkets accounted for 51.27% share of the Singapore ready-to-eat food market size in 2025, and Online Retail is forecast to record a 5.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Ready-to-Eat Food Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of Western convenience foods | +0.6% | National, with higher penetration in expatriate-dense districts (Orchard, Marina Bay) | Medium term (2-4 years) |

| Dual-income households seeking time-efficient meals | +0.8% | National, concentrated in HDB estates and private condominiums | Long term (≥ 4 years) |

| Expansion of e-commerce and food delivery platforms | +0.7% | National, with early gains in central and eastern Singapore | Short term (≤ 2 years) |

| Health consciousness drives demand for organic, low-sugar, and plant-based RTE products | +0.5% | National, skewed toward higher-income segments and younger demographics | Medium term (2-4 years) |

| Cultural diversity spurs varied cuisine RTE options | +0.4% | National, reflecting Malay, Indian, Chinese, and fusion preferences | Long term (≥ 4 years) |

| Technological advances in packaging extend shelf life | +0.3% | National, with spillover benefits to regional export markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dual-Income Households Seeking Time-Efficient Meals

In Singapore, high labor-force participation rates and long working hours have resulted in a structural time deficit. RTE (Ready-to-Eat) suppliers are addressing this demand by offering portion-controlled, microwaveable options. Approximately 28% of Singaporean consumers report insufficient time to cook, exceeding the global average by 8 percentage points. Additionally, 49% of Singaporeans consume takeaway or ready-made meals at least once a week. Household expenditure surveys show a significant increase in spending on food-serving services, rising from SGD 404.1 (USD 299) in 1993 to SGD 965.7 (USD 715) in 2023. This 2.9% annual growth rate surpasses headline inflation, indicating a lasting shift toward convenience. Consumers in this demographic prioritize speed and minimal cleanup, often choosing RTE meals that replicate popular hawker dishes—such as chicken rice, laksa, and nasi lemak—packaged in single-serve trays. The Progressive Wage Model, which raised median monthly incomes for food-services workers to SGD 5,500 (USD 4,070) in 2024, has further constrained household time budgets, according to the Ministry of Manpower[1]Source: Ministry of Manpower, “Progressive Wage Model for Food Services,” Mom.gov.sg. With higher wages enabling greater spending on convenience, the motivation to cook from scratch has declined.

Expansion of E-Commerce and Food Delivery Platforms

In 2023, online food and beverage sales reached USD 2.31 billion, contributing approximately 25% to 27% of the total F&B revenue. Online grocery channels generated USD 1.4 billion in 2024 and are projected to grow to USD 2.3 billion by 2033. Around 68% of Singaporeans use food-delivery services daily, spending an average of SGD 108 (USD 80) per month. The platform has maintained high order volumes by partnering with ComfortDelGro taxis for last-mile delivery, enabling fulfillment within 2 hours in densely populated residential areas. Foodpanda's Pandamart dark stores, which stock over 40,000 SKUs, offer an average delivery time of 25 minutes. This effectively positions RTE products as on-demand meal solutions that compete on speed rather than price. These infrastructure advancements allow brands to bypass traditional retail negotiations and test limited-edition flavors or functional variants with minimal inventory risk. This has reduced product-development cycles from 18 months to under 6 months for digital-first launches.

Health Consciousness Drives Demand for Organic, Low-Sugar, and Plant-Based RTE Products

In 2023, Singapore's investment in alternative proteins climbed to USD 170 million, representing a significant rise from the USD 85 million invested in 2021. This increase is driven by both government-supported initiatives and private capital seeking regulatory clarity on novel ingredients. By mid-2024, the Singapore Food Agency had approved 16 cell-based and precision-fermentation products, establishing the city as a global hub for testing next-generation ready-to-eat (RTE) formulations. For instance, GOOD Meat's cultivated chicken will be available at SGD 7.20 (USD 5.33) for 120 grams at Huber's Butchery starting May 2024, as reported by GOOD Meat and the SFA[2]Source: Singapore Food Agency, “Novel Food Approvals and Regulations,” Sfa.gov.sg. Nestlé's partnership with KosmodeHealth to create high-protein, high-fiber noodles from upcycled barley grains—an initiative recognized as the "Most Transformational Collaboration" at the 2023 Singapore International Chamber of Commerce event—demonstrates the industry's shift toward circular-economy principles in mainstream RTE products. Moreover, the Health Promotion Board's Healthier Dining Programme, which mandates reduced sodium and sugar levels in participating outlets, is influencing retail RTE categories. Manufacturers are proactively reformulating their products to meet these evolving standards, reducing potential reputational risks from future regulatory actions.

Technological Advances in Packaging Extend Shelf Life

The Soup Spoon's high-pressure processing (HPP) technology has extended the shelf life of refrigerated soups from 14 days to 120 days and ready meals from 3 days to 28 days. This advancement enables nationwide distribution without the costs of a frozen supply chain and reduces retailer markdown losses by up to 40%. Active packaging, which includes oxygen scavengers and antimicrobial films, is becoming a standard feature in premium ready-to-eat (RTE) lines. Additionally, smart packaging with QR-code freshness indicators and time-temperature tags allows consumers to verify cold-chain integrity before purchasing, addressing trust concerns related to chilled convenience foods. In April 2024, the Nurasa Food Tech Centre, a 3,840-square-meter facility backed by Temasek, opened at Biopolis. This center provides co-manufacturing infrastructure for startups developing innovative barrier films and modified-atmosphere packaging, which can triple ambient shelf life without using synthetic preservatives. Singapore's position as a regional logistics hub enhances the strategic importance of these innovations. For example, extending shelf life by 30 days transforms Singapore into a viable export platform for RTE products destined for Malaysia, Indonesia, and other emerging ASEAN markets, turning a domestic technological advantage into a cross-border competitive edge.

Restraint Impact Analysis

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over preservatives, additives, and high sodium in processed RTE foods | -0.5% | National, with heightened scrutiny among health-conscious millennials and Gen Z | Long term (≥ 4 years) |

| Strict Singapore Food Agency regulations | -0.4% | National, affecting all RTE manufacturers and importers | Medium term (2-4 years) |

| Strong hawker culture and preference for fresh-cooked meals | -0.6% | National, particularly in mature estates with established hawker centers | Long term (≥ 4 years) |

| High operational costs from premium ingredients and advanced packaging | -0.3% | National, with spillover effects on export pricing competitiveness | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Hawker Culture and Preference for Fresh-Cooked Meals

Singapore's 114 hawker centers, managed by the National Environment Agency and comprising over 14,000 stalls, are central to the city's dining culture. Approximately 70% of residents visit these venues four or more times a week, reducing their dependence on packaged ready-to-eat (RTE) alternatives. Hawker meals, priced between SGD 3 and SGD 5 (USD 2.22 to USD 3.70) per serving, are more affordable than most chilled RTE products and are perceived as fresher. Additionally, the communal dining experience and direct vendor interactions add a social element, creating barriers to switching that extend beyond cost considerations. Government support, including subsidies for hawker-center construction and stall rentals, aligns with efforts to preserve Singapore's culinary heritage. These measures ensure fresh-cooked meals remain both accessible and affordable, effectively limiting the premium consumers are willing to pay for convenience. In response, RTE suppliers replicate hawker flavors and collaborate with celebrity hawkers to co-brand frozen versions of popular dishes. However, these products primarily target a niche audience, including consumers who are traveling, working late, or living in newer estates with fewer hawker options. The resilience of the hawker model suggests that RTE growth in Singapore will remain gradual, complementing rather than replacing existing options. Export markets with less developed fresh-food infrastructures may offer greater potential for higher returns on marketing investments.

Strict Singapore Food Agency Regulations

The Singapore Food Agency (SFA) implemented Novel Food Regulations requiring pre-market safety assessments for ingredients without a history of human consumption. This regulation has caused delays of 6 to 12 months for plant-based and cell-cultured ready-to-eat (RTE) product launches in Singapore compared to jurisdictions with less stringent rules. Moreover, the SS 672:2021 standard for RTE meal delivery in Singapore enforces compliance costs between SGD 15,000 and SGD 30,000 (approximately USD 11,100 to USD 22,200) per stock-keeping unit (SKU). These costs stem from requirements for temperature logging, traceability protocols, and microbial testing. Such financial demands discourage small-batch experimentation, giving an edge to larger players with dedicated quality-assurance teams. Additionally, strict labeling requirements—including allergens, nutritional content, and country-of-origin—reduce available packaging space. This limitation forces brands to choose between highlighting marketing claims or meeting regulatory disclosures. While these standards enhance public health and reinforce Singapore's reputation as a safe-food hub, they also create a two-tier market. Multinational corporations, capable of spreading compliance costs across regional portfolios, gain an advantage over local startups. These startups often rely on partnerships with contract manufacturers or face prolonged time-to-market challenges. By mid-2024, the SFA had approved 16 novel-food applications, indicating progress in the regulatory framework. However, the agency's non-transparent, case-by-case review process leaves applicants uncertain about approval timelines, complicating investor due diligence and product-launch planning.

Segment Analysis

By Product Type: Functional Claims Reshape Portfolio Mix

In 2025, Ready Meals accounted for 38.28% of the market, driven by dual-income households seeking convenience and portion control over traditional cooking. Instant Soups and Snacks, growing at a 4.28% CAGR through 2031, lead product category growth with functional benefits like high protein and plant-based broths. Instant Breakfast and Cereals gained traction with fortified oat blends and protein granolas, such as General Mills' 2024 launches targeting busy consumers. Baked Goods and Meat Products cater to niche occasions with shelf-stable croissants and vacuum-sealed sausages as bakery substitutes. Plant-Based Ready Meals, though emerging, are expanding, with Impossible Foods' products available in major retail outlets since 2020 and 2021.

Functional and Protein Snacks are reshaping indulgence by adding health benefits, such as Heal Nutrition's Protein Puffs, offering 20 grams of protein per pack in unique flavors. Other Product Types, including sauces, condiments, and meal kits, create cross-selling opportunities, like Prima Taste's sauce range and Hai's Chicken Rice Sauce Kit, enabling quick hawker-style meals. These products blur the line between ready-to-eat and home-cooked meals. The Singapore Food Agency's approval of Solar Foods' Solein protein powder and its 2024 incorporation into Fazer snack bars highlight regulatory acceptance of innovative ingredients. This development signals potential shifts in product boundaries during the forecast period.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channels: Private Label Pressures Branded Margins

In 2025, Supermarkets and Hypermarkets accounted for 51.27% of the distribution share, effectively utilizing promotional pricing, strategic end-cap placements, and private-label products to attract cost-conscious shoppers. In 2024, NTUC FairPrice's Own Brands portfolio generated over SGD 1 billion (USD 740 million) in revenue, contributing approximately 20% to the group's total sales. These products appeared in 70% of online grocery baskets, a penetration rate that pressures branded suppliers to innovate and justify premium pricing or risk being delisted. Convenience and Grocery Stores focus on quick top-up purchases and impulse buys. For example, 7-Eleven Singapore offers more than 300 ready-to-eat (RTE) SKUs, including plant-based burgers and ethnic meal trays, catering to late-night workers and transit hubs. Specialty Stores target affluent customers seeking organic, imported, or artisanal RTE options. A notable example is Huber's Butchery, which introduced GOOD Meat's cultivated chicken in May 2024 at SGD 7.20 (USD 5.33) per 120 grams, demonstrating how niche retailers test premium pricing before broader market adoption.

Online Retail channels are experiencing the fastest growth among distribution formats, with a 5.26% CAGR projected through 2031. This growth is driven by dark-store networks and 25-minute delivery windows, which minimize the gap between impulse purchases and order fulfillment. foodpanda's pandamart stocks over 40,000 items and ensures a 25-minute delivery time. Similarly, RedMart's collaboration with ComfortDelGro taxis enables same-day delivery slots for suburban areas that previously relied on weekly supermarket trips. Other Distribution Channels—such as vending machines, workplace canteens, and petrol-station marts—capitalize on micro-occasions where convenience outweighs price considerations. However, their combined market share remains small compared to the dominance of big-box retailers and e-commerce platforms. The shift to online ordering allows RTE brands to bypass slotting fees and achieve better margins through direct-to-consumer sales. At the same time, this transition exposes brands to algorithm-driven visibility challenges, where factors like search ranking and sponsored placements significantly impact sales performance alongside product quality.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Singapore, with its compact 734-square-kilometer footprint and a population of 5.9 million, serves as a hyper-urban laboratory where patterns of Ready-to-Eat (RTE) adoption emerge more swiftly than in the region's sprawling markets. However, this density also intensifies competition from hawker centers and restaurant deliveries. As a regional headquarters for multinational food giants like Nestlé, Unilever, and PepsiCo, Singapore often becomes a testing ground for product innovations. These innovations, once piloted locally, typically scale across Southeast Asia within a mere 12 to 18 months. This dynamic positions Singapore as a disproportionately influential test market, especially given its relatively modest revenue base. Highlighting this influence, Nestlé, in March 2025, announced an expansion of its R&D center in Singapore, with backing from the Economic Development Board. The focus is on alternative-protein formulations and sugar-reduction technologies, set to be deployed in neighboring countries like Malaysia, Indonesia, Thailand, and the Philippines.

Singapore's government, with its "30 by 30" initiative, aims to locally produce 30% of the nation's nutritional needs by 2030. This ambition is driving investments into vertical farms, aquaculture, and precision fermentation facilities. These facilities not only supply fresh inputs to RTE manufacturers but also aim to reduce the nation's dependency on imports and shorten the farm-to-fork cycle. In April 2024, the Nurasa Food Tech Centre, a 3,840-square-meter facility backed by Temasek and located at Biopolis, commenced operations. This center offers co-manufacturing infrastructure for startups experimenting with novel ingredients and packaging formats. By doing so, it effectively subsidizes early-stage R&D, which might have otherwise relocated to more cost-effective jurisdictions. Singapore's strategic position is further bolstered by its free-trade agreements and the cargo throughput of Changi Airport, which handled 7.4 million tonnes in 2019. This makes Singapore a prime re-export platform for RTE products aimed at ASEAN markets. Notably, advanced packaging techniques that extend shelf life by 30 days can facilitate distribution to tier-2 and tier-3 cities in these markets, which often lack cold-chain infrastructure, as highlighted by the CAAS[3]Source: Civil Aviation Authority of Singapore (CAAS) "Changi Airport Cargo Throughput Statistics." caas.gov.sg.

Cross-border e-commerce platforms are capitalizing on the "Made in Singapore" label, listing Singapore-manufactured RTE products in neighboring markets. This label acts as a quality signal, allowing these products to command a 10% to 15% price premium over locally produced alternatives in both Indonesia and Malaysia. In a testament to Singapore's growing influence in the RTE sector, Temasek Holdings made headlines with its March 2025 acquisition of a 10% stake in India's Haldiram's, valuing the company at a whopping USD 10 billion. Additionally, the firm's November 2024 regulatory nod to invest in Rebel Foods further underscores the appetite of Singaporean capital for scaling RTE platforms across South and Southeast Asia, with Singapore emerging as both a financial nucleus and an operational blueprint.

Competitive Landscape

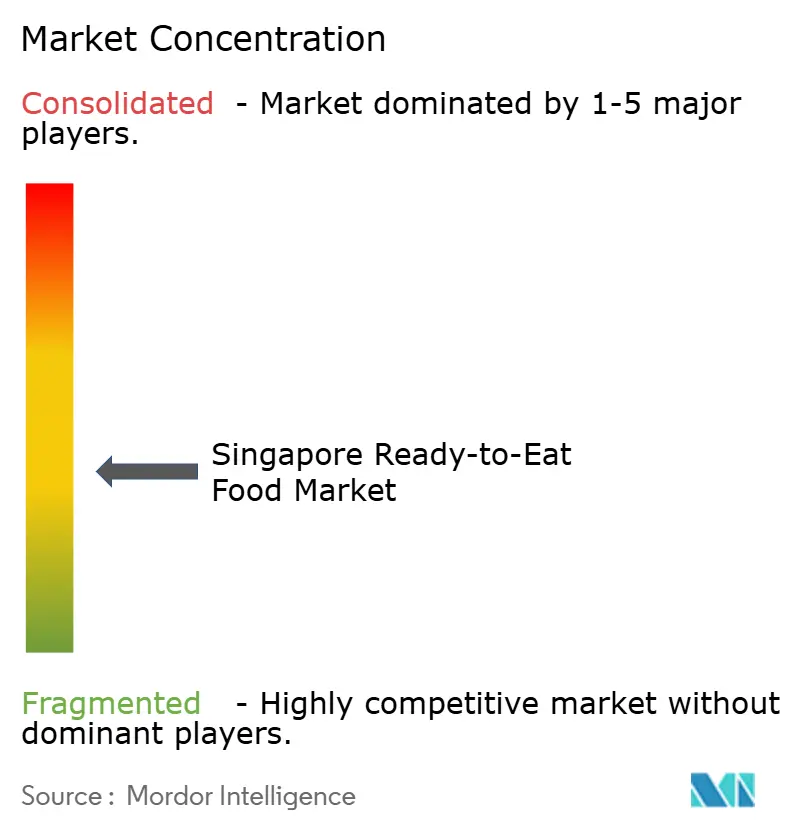

Singapore's ready-to-eat food market demonstrates moderate fragmentation, characterized by competition between established multinational companies like PepsiCo Inc., Nestle, Kellanova, and General Mills Inc. The fragmented market structure allows niche players to target specific consumer segments while creating opportunities for strategic consolidation. This dynamic is exemplified by the July 2024 partnership between SATS and Mitsui, which combines SATS' culinary expertise and production capabilities with Mitsui's global procurement and distribution network.

In Singapore, market leaders are capitalizing on the country's favorable regulatory environment and robust infrastructure to pilot products before rolling them out regionally. These companies benefit from Singapore's strategic position as a hub for innovation and testing, leveraging its well-established logistics network and supportive policies to refine their offerings before scaling operations across Southeast Asia. Meanwhile, smaller players are carving out a niche in premium segments, setting themselves apart through health-centric positioning, sustainability claims, and a nod to cultural authenticity, all in pursuit of fatter margins. Their focus on premiumization allows them to cater to a discerning consumer base willing to pay a premium for quality and value. Notably, the market is ripe with opportunities, especially in plant-based ready meals and functional foods, resonating with Singapore's wellness-centric trends and growing demand for healthier, convenient options.

Newer entrants are shunning traditional retail routes, opting instead for direct-to-consumer models. By harnessing the power of e-commerce platforms, these companies are tapping into the fastest-growing distribution channel in the ready-to-eat food sector. This approach enables them to connect with consumers swiftly, bypassing intermediaries and reducing costs. Additionally, it allows these businesses to gather real-time consumer insights, adapt to evolving tastes, and offer personalized experiences, further strengthening their market presence.

Singapore Ready-to-Eat Food Industry Leaders

-

Nestlé S.A.

-

General Mills Inc.

-

PepsiCo Inc.

-

Kellanova

-

Prima Limited

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Singapore’s leading clean snack brand, Hey! Chips has launched Hey! Fruit Bites, a first-of-its-kind freeze-dried snack that blends real fruit with science for a naturally crunchy treat.

- May 2025: Glico Singapore has introduced Pocky Milk, a wholesome biscuit snack made with premium Hokkaido milk, enriched with calcium and fibre.

- April 2025: Nissin Foods Pte Ltd introduced a limited-edition Mala Tang Cup Noodles in Singapore, translating the Sichuan street-food experience into an instant format.

- February 2025: SATS Ltd., Asia's leading food solutions provider, developed five halal-certified ready-to-eat (RTE) meals for Singapore's national emergencies, featuring no refrigeration needs, room-temperature consumption, and an eight-month shelf life achieved via retort sterilization without preservatives.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Singapore's ready-to-eat (RTE) food market as every pre-cleaned, pre-cooked meal or snack that shoppers can consume directly or after a short re-heating. Items arrive in sealed frozen, chilled, ambient, or shelf-stable packs and move through retail and e-grocery channels to households.

Scope exclusion: Pet meals, freshly prepared deli counters, catering trays, and food-delivery platform sales are set aside.

Segmentation Overview

-

By Product Type

- Ready Meals

- Instant Soups & Snacks

- Instant Breakfast/Cereals

- Baked Goods

- Meat Products

- Plant-Based Ready Meals

- Functional/Protein Snacks

- Other Product Types

-

By Distribution Channels

-

Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

-

Supermarkets/Hypermarkets

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured talks with brand managers, large grocery buyers, cold-chain operators, and nutrition consultants across Singapore and neighboring Malaysia and Indonesia. These interviews confirmed household basket shifts, average wastage, and the real uptake of Healthier Choice labeled SKUs, giving us confidence to fine-tune model assumptions.

Desk Research

We began by mapping retail values with help from the Singapore Department of Statistics monthly retail food series, Health Promotion Board nutrition surveys, and Singapore Customs import codes for prepared meals. World Bank household-spend datasets and UN Comtrade trade flows let us size import-heavy categories. Company filings, price lists, and store circulars filled average price gaps, while D&B Hoovers and Dow Jones Factiva supplied revenue splits for major producers. Inputs were cross-referenced with commentary from the Singapore Food Manufacturers' Association and patent counts obtained through Questel to judge innovation pace. The sources named are illustrative only; many other public records and specialist portals supported data checks.

Market-Sizing & Forecasting

We rebuilt 2024 spend using a top-down flow that links household food expenditure, category penetration, and average pack prices. Then, we verified totals through selective bottom-up supplier roll-ups and channel checks. Key levers include per-capita frozen meal uptake, dual-income household growth, scanner-based price trends, import volume of ready meals, Healthier Choice logo penetration, and supermarket e-commerce share. A multivariate regression of these drivers against historic sales delivers the 2025-2030 view, and scenario analysis layers inflation or policy shocks. Gaps in granular producer data were bridged by using peer group margins and import parity prices.

Data Validation & Update Cycle

Outputs travel through three analyst reviews, variance tests against trade receipts and tax filings, plus anomaly triggers whenever quarterly retail sales swing beyond two standard deviations. We refresh the model every twelve months, and we issue interim updates when regulation or demand shocks emerge, so clients always receive the latest picture.

Why Our Singapore Ready-to-Eat Food Baseline Earns Trust

Published estimates seldom match because firms pick dissimilar product baskets, mix foodservice with retail, apply different exchange rates, or refresh at uneven intervals.

According to Mordor Intelligence, our disciplined retail-only scope, yearly updates, and dual-track modeling mean stakeholders get a figure they can trace and replicate.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.25 bn (2025) | Mordor Intelligence | |

| USD 0.12 bn (2023) | Regional Consultancy A | Leaves out frozen ranges and keeps outdated exchange rates |

| USD 0.05 bn (2023) | Trade Journal B | Counts only chilled ready meals, omitting cereals and snacks |

| USD 3.43 bn (2024) | Global Consultancy C | Mixes retail, foodservice, and delivery GMV with no product filters |

These contrasts show that Mordor's clear scope choices, transparent variables, and regular refresh cadence create a balanced, dependable baseline for strategic decisions.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Singapore ready-to-eat food market?

The market is valued at USD 0.25 billion in 2025 and represents a single-city consumer base with high purchasing power.

What growth rate is forecast for the Singapore ready-to-eat food market through 2030?

Revenue is projected to rise to USD 0.29 billion by 2030, translating to a 3.06% CAGR over the period.

How are health trends shaping product innovation?

Brands reformulate with lower sodium, natural preservatives and plant-based proteins to address rising health awareness and comply with Nutri-Grade labeling.

Why is Singapore considered a regional launchpad for ready-to-eat products?

A compact geography, streamlined food-safety approvals and high expatriate diversity allow companies to test new flavors locally before scaling to wider ASEAN markets.