Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

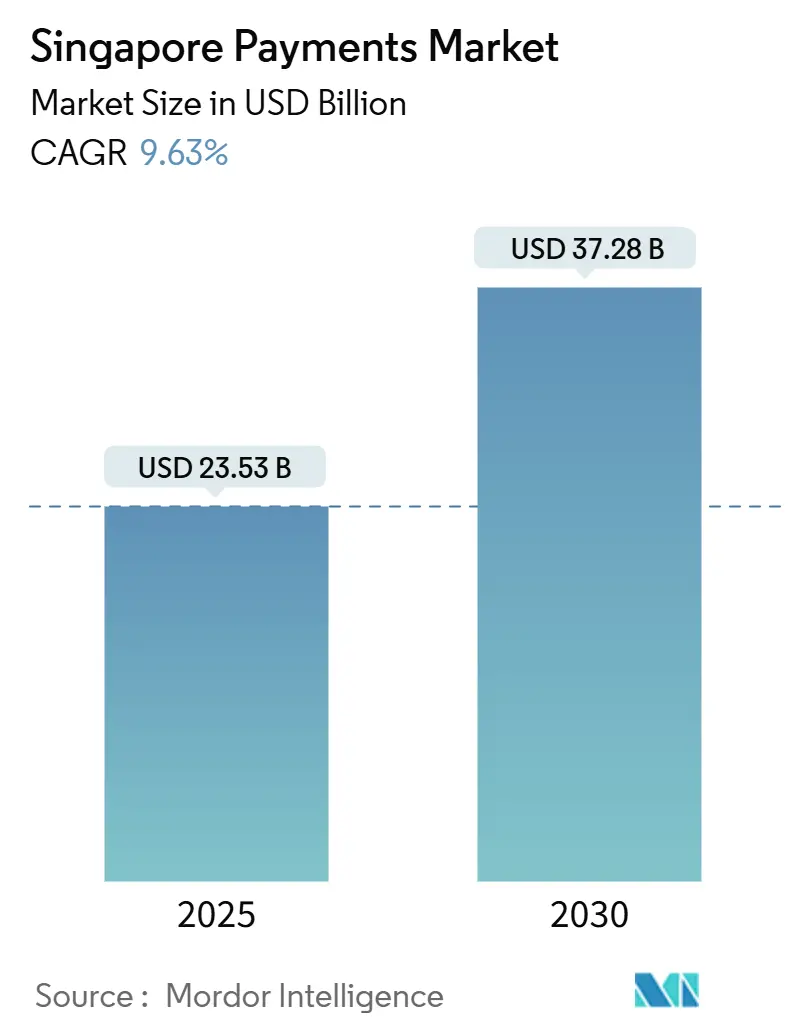

| Market Size (2025) | USD 23.53 Billion |

| Market Size (2030) | USD 37.28 Billion |

| Growth Rate (2025 - 2030) | 9.63% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Singapore Payments Market Analysis by Mordor Intelligence

Singapore’s payments market size stood at USD 23.53 billion in 2025 and, at CAGR of 9.63%, is expected to reach USD 37.28 billion by 2030, underscoring the dynamism of the Singapore payments market. Deep smartphone penetration, decisive public-sector modernisation programmes, and prolific fintech partnerships combine to create what executives increasingly recognise as the region’s reference payment environment.1Monetary Authority of Singapore, “MAS and ABS to Establish New Payments Entity to Position Singapore for Future Payments Growth,” mas.gov.sg Instant rails such as FAST and PayNow now underpin consumer, SME, and cross-border use cases, while unified QR acceptance through SGQR streamlines retail checkout. Intensifying cross-border ecommerce demand, particularly into neighbouring ASEAN corridors, is channelling incremental volumes onto the Singapore payments market as Project Nexus links five Southeast Asian schemes plus India in live pilots. Competitive behaviour centres on ecosystem integration: super-apps, digital banks, and incumbent card networks are racing to bundle payments with lending, wealth, and lifestyle propositions to retain throughput and data advantages.

Key Report Takeaways

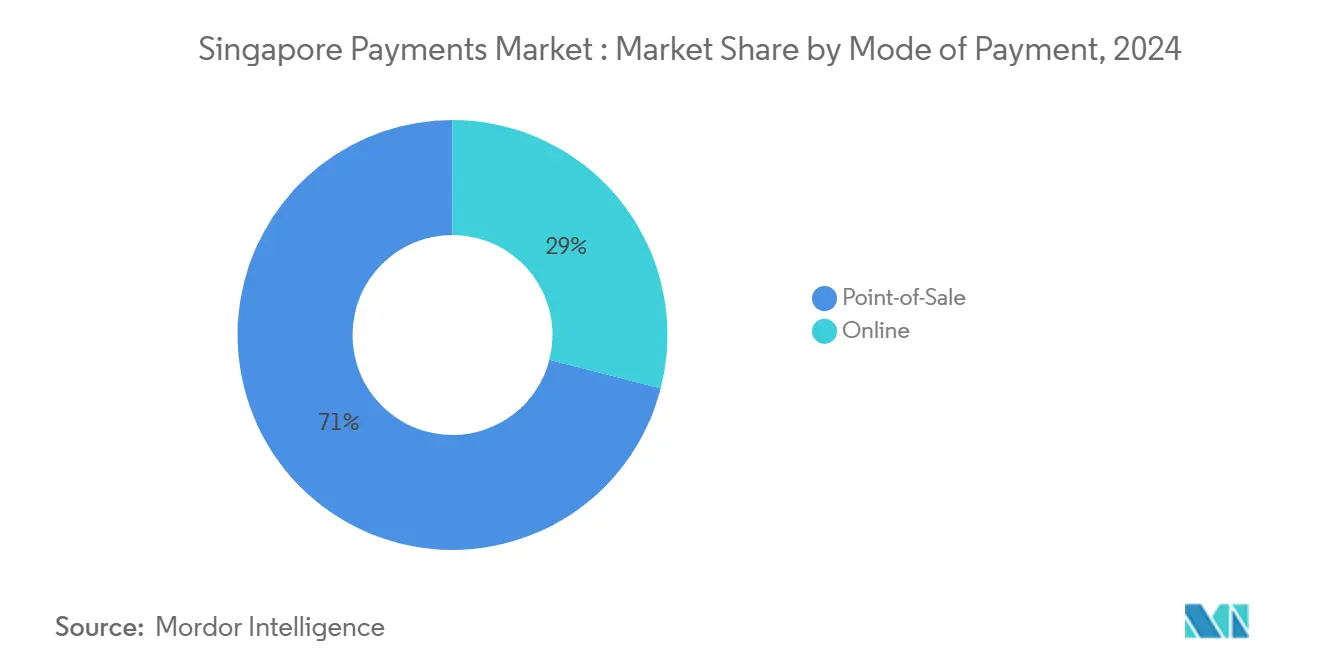

- By mode of payment, Point-of-Sale held 71% of Singapore payments market share in 2024, whereas online digital wallets and account-to-account transfers are projected to expand at a 12.3% CAGR through 2030.

- By interaction channel, point-of-sale transactions led with a 60% share of the Singapore payments market size in 2024, while ecommerce and m-commerce channels are forecast to grow at 11.5% CAGR to 2030.

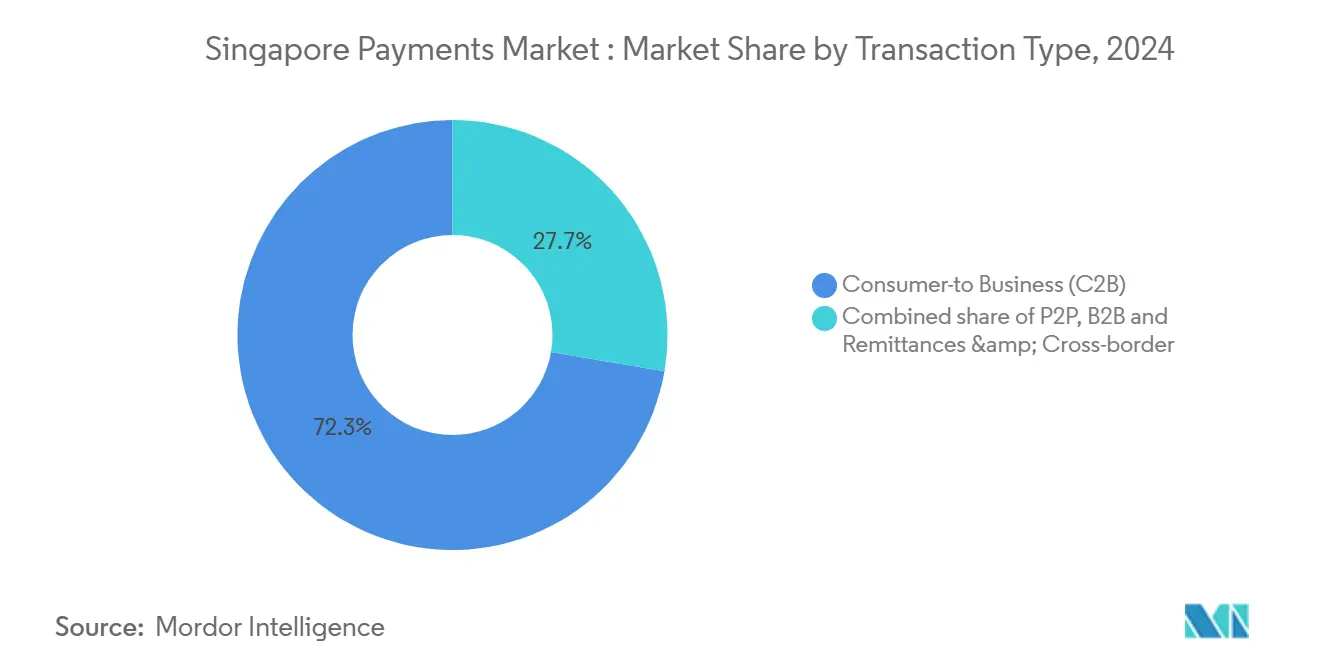

- By transaction type, consumer-to-business flows accounted for 72.3% of Singapore payments market share in 2024, whereas remittances and cross-border volumes are set to rise at a 13.7% CAGR to 2030.

- By end-user industry, retail captured 38% of the Singapore payments market size in 2024; healthcare is the fastest-growing vertical with a 13.9% CAGR projected to 2030.

Singapore Payments Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom and cross-border retail spend | +2.1% | Global, with concentration in ASEAN corridors | Medium term (2-4 years) |

| Government-led digital voucher & QR-code initiatives (SGQR) | +1.8% | Singapore national, with regional spillover effects | Short term (≤ 2 years) |

| Near-real-time Faster Payment rails (PayNow/FAST) reaching SMEs | +1.5% | Singapore domestic, expanding to ASEAN through Project Nexus | Medium term (2-4 years) |

| Super-app ecosystems bundling payments, ride-hailing & food delivery | +1.3% | Southeast Asia regional, led by Singapore and Indonesia | Long term (≥ 4 years) |

| Digital banks targeting underbanked gig-economy workers | +0.9% | Singapore national, with expansion to regional markets | Medium term (2-4 years) |

| Tokenized stored-value wallets embedded in wearables & IoT devices | +0.7% | Global technology adoption, early deployment in Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce boom and cross-border retail spend

Cross-border ecommerce flows surged from USD 500 million in 2024 to USD 1.2 billion projected for 2028, funnelling additional throughput onto the Singapore payments market as merchants tap six ASEAN countries via a single acceptance stack.2Visa Inc., “Visa Fiscal 2024 Annual Report,” visa.com Unified payment links reduce foreign-exchange friction, supporting buy-now-pay-later penetration that has reached 29% of local merchants. Digital wallet share already represents 39% of online payments, a base that positions the Singapore payments market for incremental cross-border volume once Project Nexus enters production. Integration of Alipay+ and similar schemes enables QR code acceptance for Chinese visitors, a priority tourist segment. The resulting scale effect accelerates network economics, improving merchant economics and reinforcing the city-state’s role as ASEAN’s payment clearing hub.

Government-led digital voucher & QR-code initiatives (SGQR)

The SGQR+ proof-of-concept delivered a 105% jump in transactions and 212% in value across 453 merchants during a one-month pilot, validating the case for national roll-out. Hawker subsidies that eliminate merchant discount rates accelerate acceptance among micro-retailers. Consolidation of FAST, PayNow, and SGQR under the new MAS-ABS entity fast-tracks decision-making and simplifies scheme participation for payment service providers. SGQR’s alignment with Alipay, WeChat Pay, and regional wallets provides foreign visitors a familiar checkout experience and supports tourism recovery. Strategic intent centres on elevating cash-light adoption while ensuring that domestic merchants remain connected to growing Chinese consumer spend.

Near-real-time PayNow/FAST rails reaching SMEs

SME registrations for PayNow Corporate spiked through 2024 on transaction-limit increases to SGD 200,000 (USD 149,000) per transfer via FAST, solving liquidity pain points for smaller enterprises.3UOB, “PayNow Corporate,” uob.com.sg Direct non-bank access to the rails opens gateway opportunities for fintech acquirers that can combine real-time settlement with value-added analytics. The Direct FAST Working Group’s API framework delivers plug-and-play connectivity, reducing onboarding friction. Monthly instant-payment volumes have climbed to 12.5 million, and Project Nexus provides a path to regional real-time corridors at sub-3% cost. Collectively, these factors entrench PayNow and FAST as baseline infrastructure within the Singapore payments market.

Super-app ecosystems bundling payments, ride-hailing & food delivery

Grab’s platform shows that 86% of users engage multiple verticals, driving a projected 27% gross merchandise value CAGR between 2024 and 2025. GrabPay controls 35.3% of local e-wallet share, illustrating payment stickiness once financial and lifestyle services converge. Super-apps are pivoting to high-margin embedded finance, including micro-loans and insurance, leveraging transaction data for risk analytics. Regulatory sandbox flexibilities let operators trial programmable money and smart contracts without compromising consumer safeguards. For incumbents, partnership or acquisition of super-app capabilities is becoming a prerequisite to defend relevance within the Singapore payments market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Merchant MDR cap pressures PSP profitability | -1.2% | Singapore national, with regional competitive effects | Short term (≤ 2 years) |

| Rising e-commerce fraud & social-engineering scams | -0.8% | Global cybersecurity challenge, acute in Singapore | Medium term (2-4 years) |

| Inter-wallet interoperability gaps for foreigners | -0.5% | Singapore national, affecting tourist and business visitor segments | Medium term (2-4 years) |

| Saturation of payment apps causing consumer fatigue | -0.3% | Singapore national, with spillover to urban ASEAN markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Merchant MDR cap pressures PSP profitability

Zero-interchange on instant payments compresses merchant-service margins, compelling PSPs to monetise analytics, lending, and loyalty rather than pure processing. Government hawker subsidies conditioned merchants to expect no-cost acceptance, further eroding fee tolerance. NETS, as master acquirer for many state programmes, heightens competitive pressure on private acquirers. International schemes must reconcile Singapore pricing caps with global profitability hurdles, risking under-investment. The strategic response pivots to differentiated value adds and cross-border corridors where fee structures remain intact.

Rising e-commerce fraud & social-engineering scams

Scam losses jumped 50% to SGD 652 million (USD 485 million) in 2024, triggering liability rules that push banks to deploy real-time AI screening or absorb losses.4BankInfoSecurity, “Singapore Requires Banks, Telecoms to Prevent Scams,” bankinfosecurity.com Mandatory 12-hour cooling-off windows for high-value transfers add friction that may dent user experience. Telecommunications firms must vet SMS sender IDs, a compliance burden that can inadvertently block legitimate cross-border notifications. Institutions escalate spend on biometrics and behavioural analytics, increasing cost-to-income ratios. Although necessary, these controls temper the headline growth narrative for the Singapore payments market by amplifying operating expense.

Segment Analysis

By Mode of Payment: Cards Maintain Scale, Wallets Gain Velocity

Cards anchored 55.2% of the Singapore payments market share in 2024, reflecting the entrenched security and rewards of established schemes. Overall, POS leads the segment with 71% share. Wallet-based and account-to-account instruments outpace at 12.3% CAGR through 2030, propelled by PayNow-to-ecommerce integrations and SGQR ubiquity. Cash persists only in narrow use cases such as traditional wet markets, where targeted digitisation subsidies are progressively shrinking share. Tokenised credentials on wearables introduce new micro-transaction classes that bypass plastic entirely. Convergence plays are visible as Mastercard’s Pay Local allows consumers to attach cards to local wallets for instant payment, blurring scheme lines.

The Singapore payments market size for wallet transactions is forecast to exceed USD 15 billion by 2030, aided by tourist QR acceptance. Hybrid checkout flows where a credit line is embedded in a PayNow push transfer appeal to merchants seeking lower fees without losing instalment attractiveness. BNPL, adopted by 29% of merchants, merges credit dynamics with wallet UX. The competitive frontier therefore moves from instrument type to value-added layers such as loyalty, instalments, and data insights. Providers that couple card acceptance with bank-rail payouts at checkout are best positioned to defend volume while compressing cost for merchants and consumers alike.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Interaction Channel: Physical Stays Relevant as Digital Commerce Accelerates

Point-of-sale accounted for 60% of transactions in 2024, sustaining volume through dense retail networks and QR code roll-outs at hawkers. The Singapore payments market size within ecommerce and m-commerce is projected to hit SGD 37.5 billion (USD 27.9 billion) by 2030, capturing nearly the entirety of online retail activity. SGQR+ enables merchants to unify physical and online acceptance, reducing channel siloing. Social-commerce and livestream sales inject payment moments directly into content, demanding real-time settlement rails to prevent cart abandonment. Consequently, interaction definitions blur as super-apps let consumers alternate between offline pick-up, in-app ordering, and QR payment in a single journey.

Mobile checkout conversion stands at 92% among leading merchants that integrate PayNow deep-links, far exceeding card redirect flows. For cross-border sellers, Project Nexus promises instant, capped-fee transfers that bypass traditional card rails, further tilting shares in the Singapore payments market. Physical retailers are adding cashier-less experiences, where computer-vision and tokenised wallets auto-debit upon exit. The strategic imperative for PSPs is omnichannel orchestration that recognises users across touchpoints and extends risk controls without compromising speed.

By Transaction Type: C2B Dominance, Cross-Border Volumes Scale Up

Consumer-to-business flows delivered 72.3% of 2024 throughput, aligning with Singapore’s service-oriented economy. Remittances and other cross-border payments, however, are the fastest growing slice at 13.7% CAGR, fuelled by instant corridors to Thailand, Malaysia, Indonesia, Vietnam, the Philippines, and India. Person-to-person volumes keep momentum as PayNow’s NRIC and mobile proxies entrench use for gifting and bill splitting. Business-to-business transactions modernise via PayNow Corporate and blockchain trade rails that compress settlement and documentary cycles.

Linkage with India’s UPI supercharges remittance pathways, connecting Singapore’s 350,000-strong Indian workforce to affordable transfers under USD 3 average fee. Multinationals leverage Singapore’s hub status to route intercompany settlements through local banks, positioning the Singapore payments market as a treasury centre for ASEAN operations. Government-to-person experimentation with programmable vouchers could create new volume categories once live. PSPs that layer FX hedging, compliance screening, and working-capital finance onto cross-border flows will unlock margin uplift beyond core processing.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Retail Leadership, Healthcare Upswing

Retail captured 38% of transaction value in 2024, supported by tourist expenditures and local discretionary spending. Healthcare transactions are pacing at 13.9% CAGR to 2030, catalysed by the Healthier SG programme’s emphasis on preventive digital care. Entertainment payments, including gaming and streaming, contribute high transaction frequency, while travel rebounded as border restrictions eased. Government service integration, notably digital tax and licence payments via PayNow, is gradually normalising cashless public-sector revenue collection.

The Singapore payments market size attributable to healthcare is set to triple by 2030 as telemedicine, pharmacy deliveries, and wearables integrate payments. IoT-enabled parking, tolling, and electric-vehicle charging add micro-payment volumes in mobility. Retailers exploit SGQR to converge in-store and online promotions, driving loyalty card consolidation inside wallets. PSPs that secure deep vertical integration, for instance through healthcare compliance modules or travel loyalty engines, will command premium yield despite MDR compression elsewhere.

Geography Analysis

Singapore’s domestic payments policy environment functions as an exportable template for Southeast Asia. The consolidation of FAST, PayNow, and SGQR governance under the MAS-ABS payments entity puts a single strategic nerve centre behind scheme evolution and cross-border alignment. Project Nexus institutionalises this stance, with Singapore acting as scheme operator for payment interlinking across five ASEAN peers plus India, positioning the Singapore payments market as the regional settlement engine. Bilateral PayNow-PromptPay connectivity already processes 300,000 monthly transfers, demonstrating consumer appetite for instant, low-fee cross-border payments.

Neighbouring ASEAN markets collectively posted USD 220 billion in electronic payments during 2024, representing the largest near-term addressable upside for Singaporean PSPs. Singapore provides regional headquarters to over 1,200 financial institutions, which pilot innovations—biometrics, tokenisation, programmable money—before scaling to Indonesia, the Philippines, and Vietnam. Visa’s June 2025 launch of Intelligent Commerce across Asia-Pacific selected Singapore as reference ground for AI-assisted routing, underlining the city-state’s test-bed advantage.

Global corridors are likewise expanding. Stablecoin start-up XWeave chose Singapore-Philippines as its first remittance route, seeking regulatory clarity and migrant-worker flow density. Wise’s deeper integration with Standard Chartered reinforces Singapore as the brand’s APAC liquidity node. Collectively, these developments embed the Singapore payments market inside both regional and global settlement fabrics, offering scale economics beyond its 6-million-population domestic base.

Competitive Landscape

Three universal banks—DBS, OCBC, and UOB—anchor the incumbent layer, leveraging current-account ubiquity and integrated super-wallets to capture everyday payments. DBS posted SGD 11.4 billion (USD 8.5 billion) net profit in 2024 while PayLah! logged 41.6 million monthly logins, equating to near-daily usage across its active user base. Network schemes Visa and Mastercard fortify positions via tokenisation and cross-border routing initiatives such as Pay Local. Grab and SeaMoney weaponise lifestyle ecosystems, embedding payments into ride-hailing, food delivery, and gaming flows.

Strategic plays now focus on ecosystem breadth rather than stand-alone processing. DBS links PayLah! to transit, utilities, and e-commerce, deepening data troves that feed credit algorithms. Visa’s Intelligent Commerce introduces AI-scoring at checkout, cutting issuer declines and lifting throughput. Grab deepens credit exposure through its GXS Bank, targeting underbanked micro-entrepreneurs. NETS channels state contracts to defend relevance against global schemes, while new digital banks such as Trust Bank court gig-workers with instant PayNow wage disbursements and micro-savings.

White-space is evident in cross-border SME payments and vertical-specific processing such as healthcare, where compliance complexity offers barriers. Patent activity in 3-D Secure nearly doubled to 8,172 filings in 2024, signalling a security arms race. Stablecoin rails may challenge correspondent banking if regulatory perimeter clarifies. Meanwhile, MDR caps tilt domestic economics toward ancillary services—data, lending, and subscription fintech APIs—that sustain profitability within the Singapore payments market.

Singapore Payments Industry Leaders

-

DBS Bank Ltd

-

PayPal Holdings, Inc.

-

Apple Inc.

-

Grab Holdings Ltd.

-

Fave (Pine Labs Pte Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Visa launched Intelligent Commerce across Asia-Pacific to provide AI-driven authorisation-optimisation and fraud-mitigation services. Strategy rationale: deepen issuer and merchant stickiness while positioning Visa as a tech platform beyond network processing.

- May 2025: XWeave secured USD 3 million seed funding to build stablecoin-based cross-border rails between Singapore and the Philippines, aiming to exploit migrant remittance demand and regulatory clarity for digital tokens.

- February 2025: MAS and ABS formed a new payments entity consolidating FAST, PayNow, and SGQR oversight, streamlining scheme governance to accelerate feature roll-out and international linkages.

- November 2024: Mastercard unveiled Pay Local, letting consumers attach cards to local wallets for real-time purchases, a hedge against bank-rail migration and QR proliferation in the Singapore payments market.

- November 2024: Wise partnered Standard Chartered to deliver instant multi-currency remittances, pairing fintech UX with bank liquidity to defend market share in the profitable cross-border segment.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Singapore payments market as the total value of transactions carried out by consumers at physical points of sale and on domestic e-commerce or travel platforms. The model counts card, account-to-account, and digital wallet flows settled in Singapore dollars or cross-border rails that terminate in Singapore merchants; cash usage is tracked only as a share driver, not as value.

Scope Exclusion. The framework omits motor vehicle and real estate purchases, utility or loan bill payments, and capital market trades.

Segmentation Overview

- By Mode of Payment

- Point-of-Sale

- Card (Debit, Credit, Pre-paid)

- Digital Wallets (Apple Pay, Google Pay, Interac Flash)

- Cash

- Other POS (Gift-cards, QR, Wearables)

- Online

- Card (Card-Not-Present)

- Digital Wallet and Account-to-Account (Interac e-Transfer, PayPal)

- Other Online (COD, BNPL, Bank Transfer)

- Point-of-Sale

- By Interaction Channel

- Point-of-Sale

- E-commerce/M-commerce

- By Transaction Type

- Person-to-Person (P2P)

- Consumer-to-Business (C2B)

- Business-to-Business (B2B)

- Remittances and Cross-border

- By End-user Industry

- Retail

- Entertainment and Digital Content

- Healthcare

- Hospitality and Travel

- Government and Utilities

- Other End-user Industries

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed acquiring banks, payment gateways, and large online merchants across Central, North, and East regions. These conversations let us stress test growth levers such as instant payment adoption and average ticket sizes, while short consumer pulse surveys clarified channel migration after PayNow rail expansions.

Desk Research

We began with datasets issued by the Monetary Authority of Singapore, the Infocomm Media Development Authority, and the Department of Statistics, which anchor transaction volumes, smartphone penetration, and household e-commerce outlay. Industry associations such as the Singapore Retailers Association and ASEAN+3 Macroeconomic Research Office supplied supplemental indicators on card circulation and regional remittance corridors. Our team next pulled company filings, investor decks, and press releases to track fee structures and wallet load value. Select modules from D&B Hoovers and Dow Jones Factiva helped us validate issuer revenue and news driven shocks. This list is illustrative, and many additional public and paid sources informed our desk work.

Market-Sizing & Forecasting

We reconstructed the 2025 baseline through a top down transaction value pool that layers MAS card switch data, FAST rail statistics, and estimated wallet balances, which are then cross checked with sampled average selling price × volume calculations at leading acquirers. Key drivers, smartphone penetration, e-commerce gross merchandise value, real time transfer share, credit card rewards intensity, and merchant QR acceptance feed a multivariate regression that projects demand to 2030. Bottom up supplier roll ups fill any channel gaps, and scenario analysis adjusts for regulatory fee caps.

Data Validation & Update Cycle

Outputs flow through variance checks against external benchmarks and prior editions. Senior analysts review anomalies before sign off, and we refresh every twelve months, with interim updates triggered by material policy or infrastructure changes.

Why Mordor's Singapore Payments Baseline Inspires Confidence

Published estimates often diverge because firms choose distinct scopes, currency conversions, or refresh cadences, and we acknowledge that upfront.

The most common gaps arise when broader studies fold in wholesale clearing totals or, conversely, study only card issuance revenue, while Mordor reports the consumer facing transaction pool supported by MAS data and annual model recalibration.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 23.53 B (2025) | Mordor Intelligence | |

| USD 120 B (2024) | Regional Consultancy A | Bundles peer to peer transfers and interbank settlement layers without de-duplication |

| USD 4.48 B (2024) | Industry Association B | Focuses solely on card issuer fee revenue and ignores wallet and A2A flows |

These comparisons show that, by selecting a balanced scope and validating every assumption through public statistics and first hand interviews, Mordor Intelligence delivers a dependable baseline that decision makers can trace back to transparent variables and repeatable steps.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of Singapore’s payments market and how fast is it growing?

The market is valued at USD 23.53 billion in 2025 and is projected to reach USD 37.28 billion by 2030, reflecting a 9.63% CAGR.

Which payment mode holds the largest share today?

Card transactions remain dominant, capturing 55.2% of total payment volume in 2024.

What segment is expanding the quickest?

Online digital wallets and account-to-account transfers lead growth with a 12.3% CAGR forecast through 2030.

How important are cross-border and remittance flows?

Remittances and other cross-border payments are the fastest-rising transaction type, advancing at a 13.7% CAGR on the back of Project Nexus connectivity.

Which end-user industry offers the strongest growth outlook?

Healthcare payments are set to expand at a 13.9% CAGR as digital health and telemedicine adoption accelerate.

What are the main risks that market participants should watch?

Margin pressure from zero-MDR instant payments and rising e-commerce fraud—scam losses reached SGD 652 million (USD 485 million) in 2024—are the key headwinds.

Page last updated on: