Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

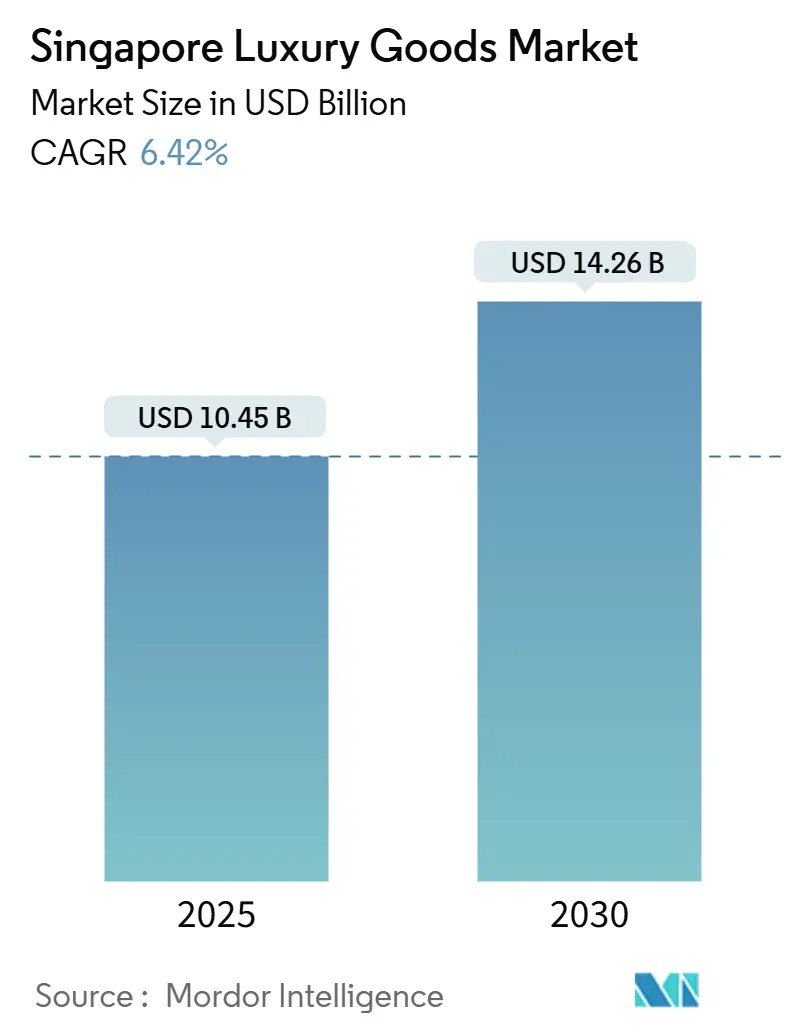

| Market Size (2025) | USD 10.45 Billion |

| Market Size (2030) | USD 14.26 Billion |

| Growth Rate (2025 - 2030) | 6.42% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Singapore Luxury Goods Market Analysis by Mordor Intelligence

The Singapore luxury goods market, valued at USD 10.45 billion in 2025, represents a critical segment within the global luxury goods industry. It is projected to grow significantly, reaching USD 14.26 billion by 2030, with a robust CAGR of 6.42% during the forecast period of 2025-2030. This growth is driven by several key factors, including rising disposable incomes, an increasing inclination toward premium and high-quality products, and the strong presence of global luxury brands in the country. Singapore's strategic position as a global financial hub and a premier tourist destination further bolsters the market, attracting affluent consumers from both domestic and international markets. The market is also witnessing a shift in consumer behavior, with a growing emphasis on personalized shopping experiences and sustainable luxury. The younger demographic, particularly millennials and Gen Z, is emerging as a significant consumer base, driving demand for innovative and exclusive luxury products. Furthermore, the rapid adoption of digital platforms and e-commerce has revolutionized the way luxury goods are purchased, offering greater accessibility and convenience to consumers.

Key Report Takeaways

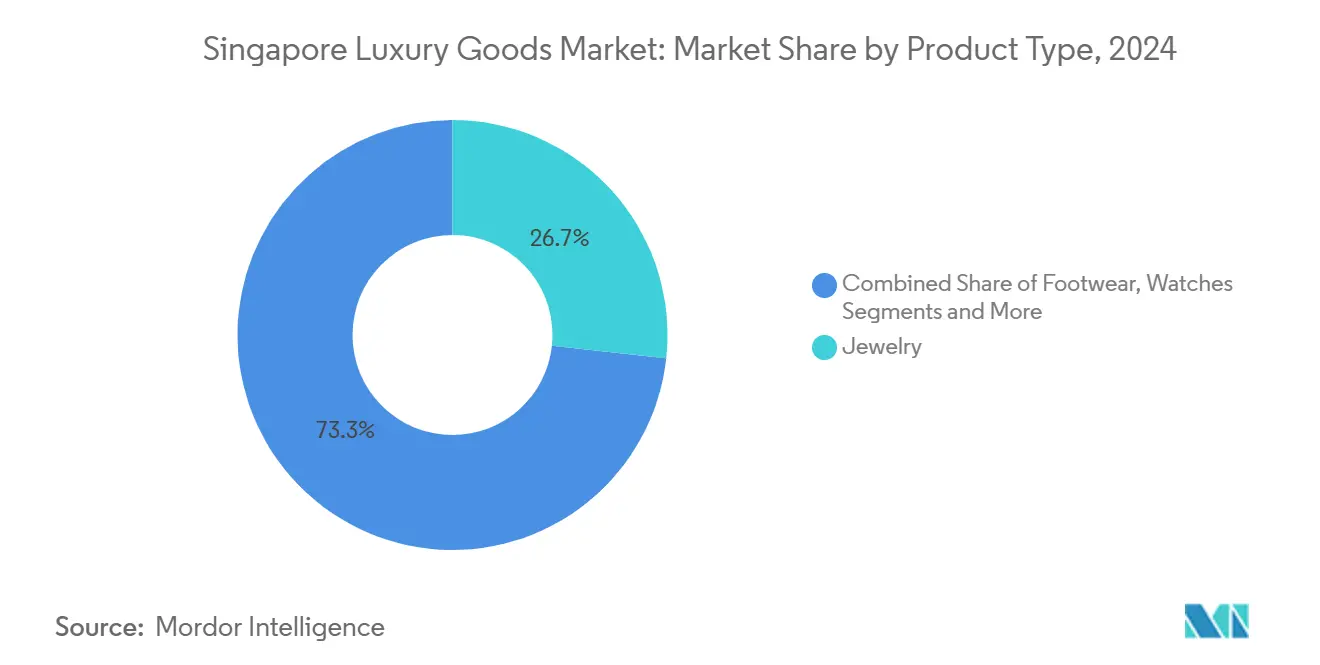

- By product type, jewelry captured 26.72% of Singapore luxury goods market share in 2024; watches are projected to post the fastest 7.18% CAGR through 2030.

- By end user, women accounted for 56.43% of the Singapore luxury goods market in 2024, whereas men represent the quickest-growing cohort with a 7.96% CAGR to 2030.

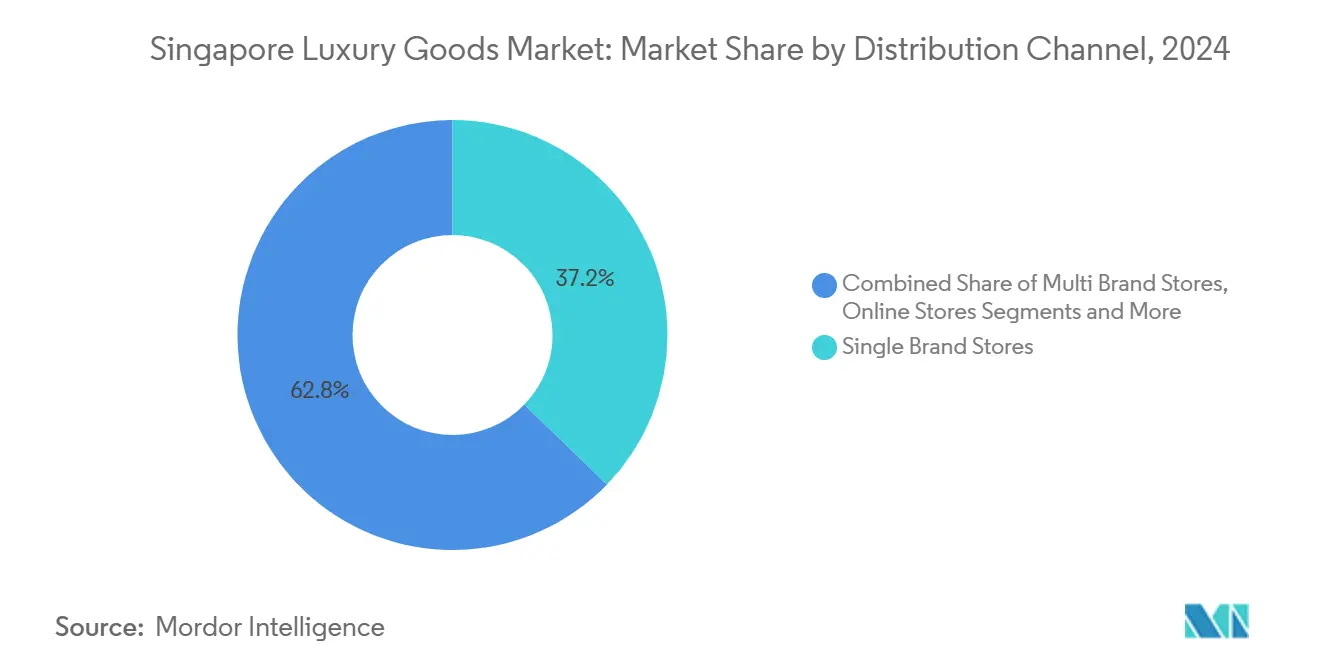

- By distribution channel, single-brand stores held 37.24% of 2024 revenue; online stores are forecast to record a 7.74% CAGR during 2025-2030.

Singapore Luxury Goods Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising wealth and HNWIs population | +1.8% | Singapore core, spillover to Southeast Asia | Medium term (2-4 years) |

| Influence of social media and celebrity endorsements | +1.2% | Singapore urban centers | Short term (≤ 2 years) |

| Expansion of luxury e-commerce platforms | +1.5% | Singapore national, regional hub effect | Medium term (2-4 years) |

| Affluent younger demographic | +0.9% | Singapore urban centers, regional influence | Long term (≥ 4 years) |

| Consumer inclination towards limited edition products | +0.6% | Singapore premium districts, tourist zones | Short term (≤ 2 years) |

| Globalization of luxury brands | +0.7% | Singapore as regional gateway to Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising wealth and HNWIs population

Growing affluence and an increasing population of high-net-worth individuals (HNWIs) are significant drivers of the Singapore luxury goods market. The rise in disposable income and wealth accumulation among individuals has led to a higher demand for premium and luxury products. According to the Credit Suisse Research Institute, in 2024, Singapore is home to 330,752 high-net-worth (HNW) individuals and 1,739 ultra-high-net-worth (UHNW) individuals [1]Source: Credit Suisse Research Institute, "Global Wealth Report 2025", www.smartwealth.sg. This substantial concentration of wealth not only boosts the consumption of luxury goods but also encourages the entry of global luxury brands into the market to cater to this affluent demographic. Singapore, being a global financial hub, attracts a significant number of HNWIs and UHNWIs, further fueling the market's growth. Additionally, the country's stable economy, favorable tax policies, and robust retail infrastructure create an ideal environment for the luxury goods market to thrive. The presence of high-end shopping districts, luxury boutiques, and exclusive retail experiences further enhances the appeal of luxury goods among affluent consumers, solidifying Singapore's position as a key market for luxury products in the Asia-Pacific region.

Influence of social media and celebrity endorsements

Social media and celebrity endorsements significantly drive the Singapore luxury goods market. The widespread use of social media platforms has transformed how consumers discover and engage with luxury brands. Platforms like Instagram, Facebook, and TikTok serve as key channels for showcasing luxury products, enabling brands to reach a broader audience and create aspirational value. Celebrity endorsements further amplify this influence by leveraging the credibility and appeal of well-known personalities. Celebrities often act as trendsetters, and their association with luxury brands enhances brand perception and desirability among consumers. In Singapore, where social media penetration is high, and consumers are highly brand-conscious, these endorsements play a pivotal role in shaping purchasing decisions. According to the Department of Singapore Statistics, the mobile penetration rate in Singapore was observed to be 165% in 2024 [2]Source: Department of Singapore Statistics, "InfoComm and Media", www.singstat.gov.sg, highlighting the extensive reach of digital platforms. Additionally, the integration of influencer marketing, where social media influencers promote luxury goods, has become a critical strategy for brands. Influencers with a strong following and niche appeal can effectively target specific consumer segments, driving engagement and sales.

Expansion of luxury e-commerce platforms

The expansion of luxury e-commerce platforms is a significant driver of the Singapore luxury goods market. These platforms are increasingly catering to the growing demand for premium products by offering a seamless online shopping experience. Enhanced digital infrastructure, coupled with the rising penetration of smartphones and internet connectivity, has enabled luxury brands to reach a broader audience. Additionally, features such as personalized recommendations, virtual try-ons, and exclusive online collections are attracting affluent consumers. The convenience of shopping from home, combined with secure payment options and efficient delivery services, further fuels the growth of luxury e-commerce in Singapore. This trend is reshaping consumer behavior and driving the market forward. Furthermore, collaborations between luxury brands and e-commerce platforms are creating exclusive partnerships, offering limited-edition products and unique experiences to online shoppers. The growing influence of social media and digital marketing strategies also plays a crucial role in promoting luxury goods through these platforms.

Affluent younger demographic

The wealthy youth demographic serves as a significant driver for the Singapore luxury goods market. In 2024, over 40% of Singaporeans are aged between 15 and 39, as reported by the Singapore Department of Statistics [3]Source: Singapore Department of Statistics, "Key Annual Indicators on Population", www.singstat.gov.sg. This substantial proportion of the population represents a key consumer base for luxury goods, as individuals in this age group are often characterized by higher disposable incomes and a strong inclination toward premium products. Younger consumers in Singapore are increasingly drawn to luxury brands due to their desire for exclusivity, status, and superior quality. Their tech-savviness and active engagement on digital platforms and social media further amplify their exposure to luxury trends, making them more likely to adopt and invest in high-end products. Moreover, this demographic's preference for personalized and unique experiences has prompted luxury brands to innovate and tailor their offerings to meet these evolving demands. As a result, the spending habits and preferences of this influential group are shaping the strategies of luxury brands, driving growth and competition within the market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating prime-retail rents | -0.8% | Singapore Orchard Road, Marina Bay premium districts | Short term (≤ 2 years) |

| Intense market competition | -0.6% | Singapore national, regional competitive spillover | Medium term (2-4 years) |

| Availability of counterfeit products | -0.4% | Singapore borders, regional supply chains | Medium term (2-4 years) |

| Sustainability-driven shift from new goods to resale | -0.7% | Singapore urban centers, environmentally conscious segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intense market competition

Fierce competition dominates the market landscape, acting as a significant restraint in the Singapore Luxury Goods Market. The presence of numerous established players and new entrants intensifies the rivalry, making it challenging for companies to differentiate their offerings. This competitive environment often leads to aggressive pricing strategies, promotional activities, and innovation races, which can strain profit margins. Additionally, the high level of competition compels businesses to invest heavily in marketing and branding efforts to maintain their market position, further increasing operational costs. Such dynamics create a challenging environment for market players, impacting their growth potential and overall market performance. Furthermore, the market's saturation with luxury brands and products makes it difficult for new entrants to establish a foothold, while existing players face the constant pressure of retaining customer loyalty. The evolving preferences of consumers, who increasingly seek personalized and unique experiences, further complicate the competitive landscape.

Availability of counterfeit products

The availability of counterfeit products poses a significant restraint in the Singapore Luxury Goods Market. Counterfeit goods, often sold at a fraction of the price of genuine luxury items, undermine the exclusivity and perceived value of luxury brands. This issue not only impacts the revenue of legitimate manufacturers and retailers but also erodes consumer trust in the market. The proliferation of counterfeit products is facilitated by advancements in technology, which make it easier to produce high-quality replicas, and by the rise of online platforms, which provide a convenient channel for their distribution. Additionally, the presence of counterfeit goods can dilute brand equity and create challenges for companies in maintaining their premium positioning. Counterfeit products also create a highly competitive environment for legitimate players, as consumers seeking lower-priced alternatives may opt for fake goods, further affecting the sales of authentic luxury items. The issue is compounded by the difficulty in distinguishing counterfeit products from genuine ones, especially for consumers who lack the expertise to identify subtle differences. Addressing this issue requires stringent regulatory measures, increased consumer awareness, and robust anti-counterfeiting strategies by market players.

Segment Analysis

By Product Type: Jewelry Dominance Meets Watch Innovation

In 2024, jewelry maintained its dominance in the Singapore luxury goods market, securing a commanding 26.72% share of the overall industry. This leadership position underscores Singapore’s role as a regional hub for luxury trade, drawing both local consumers and international buyers. The city-state’s strategic location and strong financial infrastructure make it an ideal gateway for precious metals and high-value products. Beyond trade dynamics, jewelry also carries deep cultural importance across Asia, where gold and other precious metals symbolize security, prosperity, and long-term wealth preservation. For many affluent consumers in Singapore and the surrounding region, jewelry purchases are not only seen as lifestyle choices but also as investments that hold intrinsic financial value.

The watches category is projected to be the fastest-growing segment, expanding at a CAGR of 7.18% through 2030. This growth trajectory reflects shifting consumer preferences, as high-net-worth individuals increasingly view luxury timepieces as both status symbols and collectible assets. Global demand for rare and limited-edition watches has surged, and Singapore’s luxury retail ecosystem positions it well to capture this momentum. The city’s reputation for authenticity, transparency, and access to leading Swiss and European brands enhances consumer trust in high-value purchases. Additionally, younger affluent buyers are showing keen interest in luxury watches, reflecting expanding aspirational consumption alongside traditional investment-driven purchases.

Note: Segment shares of all individual segments available upon report purchase

By End User: Women Lead While Men Accelerate

In 2024, women accounted for the largest share of the Singapore luxury goods market, commanding 56.43% of total sales. This dominance is closely tied to traditional consumption patterns in the luxury sector, where women have historically represented the primary consumer base for categories such as jewelry, apparel, handbags, and personal accessories. Cultural norms, coupled with long-established marketing practices, reinforce the centrality of female consumers in luxury retail strategies. Furthermore, women in Singapore and the broader Asian region often view luxury goods as both lifestyle enhancements and expressions of social identity, contributing to sustained demand across categories. Influenced by generational wealth transfers and rising female affluence, women continue to drive premium purchases in both established and emerging luxury segments.

In contrast, the men’s luxury segment is emerging as the fastest-growing category, projected to grow at a 7.96% CAGR through 2030. This rapid growth signals a fundamental shift in gender-based purchasing behavior, reflecting how male consumers are embracing luxury through new avenues beyond traditional categories. While watches and automobiles remain cornerstone purchases, today’s male consumers in Singapore are increasingly drawn to self-care products, high-end fashion, and accessories that emphasize individuality and personal expression. The evolving perception of masculinity among affluent men has paved the way for broader luxury participation, driven by aspirational consumption and investment-minded purchasing. Younger generations, in particular, are seeking out luxury as a statement of identity, lifestyle sophistication, and financial discernment.

By Distribution Channel: Single Brand Stores Anchor Digital Growth

In 2024, single-brand stores held the largest share of the Singapore luxury goods market, commanding 37.24% of overall sales. This dominance highlights the continued importance of exclusive and controlled retail environments within the luxury sector. Luxury brands rely heavily on curated physical spaces to deliver immersive experiences, build strong emotional connections, and maintain brand prestige among affluent consumers. For many buyers, the in-store journey from personalized service to sensory engagement is as critical as the product itself. Singapore’s position as a global shopping destination reinforces the relevance of single-brand boutiques, which are often strategically placed in high-end retail districts to cater to both local and international clientele. This enduring strength demonstrates that even in an era of rapid digitalization, physical stores remain the cornerstone of luxury retail strategies and consumer trust.

In contrast, online luxury retail is emerging as the fastest-growing distribution channel, projected to expand at a CAGR of 7.74% through 2030. This acceleration is driven by the digital transformation of consumer engagement models and the growing comfort of high-net-worth individuals with e-commerce transactions. Advancements in secure payment systems, virtual try-on technologies, and curated online experiences are reshaping how luxury brands connect with their audiences. Younger consumers, in particular, are spearheading this digital adoption, valuing convenience, exclusivity, and personalized recommendations in their online shopping journeys. Moreover, brands are strategically investing in direct-to-consumer platforms to retain control over pricing, authenticity, and customer relationships while scaling global reach. As a result, online stores are not only expanding rapidly but are also redefining the balance between traditional luxury retail environments and digital-first strategies in Singapore.

Geography Analysis

The Singapore luxury goods market stands out in Southeast Asia for its unique combination of strong local demand, significant tourist spending, and its status as a wealth management and retail hub. Singapore’s affluent resident base—bolstered by one of the highest concentrations of millionaires in Asia—drives consistent domestic consumption of high-end products, from designer apparel and luxury watches to jewelry and fine leather goods. The city’s reputation for safety, stability, and cosmopolitan lifestyle further cultivates a tendency towards discretionary luxury purchases, making it an attractive market for both global brands and local distributors looking to launch flagship stores or exclusive offerings.

Tourism plays a pivotal role in amplifying Singapore’s luxury market performance. As a renowned destination for international travelers, especially from China, Indonesia, and Malaysia, Singapore benefits from high tourist footfall in luxury retail districts like Orchard Road, Marina Bay Sands, and Changi Airport’s Jewel. Tourism-driven sales experienced a robust rebound following travel recovery in the post-pandemic era, contributing a substantial share to overall market revenues. The presence of luxury hotels and world-class shopping malls creates a seamless integration of premium experiences, further stimulating sales across categories such as fashion, watches, jewelry, and high-end beauty products.

Geographically, Singapore’s compact urban landscape allows for highly concentrated and dynamic retail zones, enabling luxury brands to maximize visibility and operational efficiency. Areas such as Orchard Road and Marina Bay act as flagship corridors for leading global luxury houses, providing immersive retail experiences and frequent opportunities for exclusive launches and pop-up events. Meanwhile, expanding e-commerce penetration and omnichannel strategies allow luxury brands to reach affluent consumers island-wide, including repeat customers and younger luxury buyers in residential neighborhoods. This unique geography—urban, accessible, and intensely commercial—solidifies Singapore’s role as a benchmark luxury goods market, not just in ASEAN but globally.

Competitive Landscape

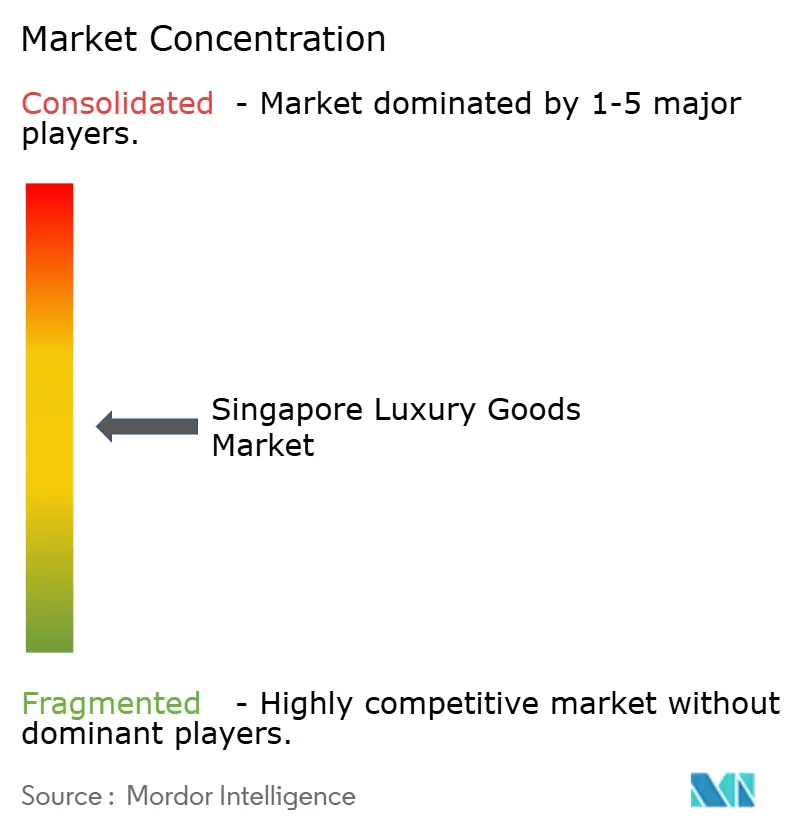

In Singapore's luxury goods market, a score of 5 indicates a moderate concentration. This score reflects a competitive landscape where global giants, regional players, and local luxury brands actively compete for market share. The market's competitive nature is driven by the presence of well-established global conglomerates such as LVMH, Kering, and Richemont, which dominate through their extensive portfolios, strong brand equity, and significant financial resources. These companies leverage their scale advantages to maintain a robust presence in the market, offering a wide range of luxury products that cater to diverse consumer preferences. Their ability to invest heavily in marketing, innovation, and distribution networks further strengthens their competitive positioning, allowing them to consistently attract high-net-worth individuals and affluent consumers in Singapore.

At the same time, the market structure creates ample opportunities for emerging regional players and local luxury brands to carve out their niche. These smaller players often focus on specialized offerings, such as bespoke services, unique craftsmanship, or culturally resonant designs, which appeal to specific customer segments. By targeting these distinct niches, they can differentiate themselves from larger competitors and build a loyal customer base. Additionally, the growing demand for personalized and exclusive luxury experiences in Singapore further supports the growth of these niche brands and specialized retailers. Local brands, in particular, are leveraging Singapore's rich cultural heritage and blending it with modern luxury trends to create products that resonate deeply with both domestic and international consumers.

The competitive environment in Singapore's luxury goods market is also shaped by evolving consumer preferences and trends. Increasingly, consumers are seeking sustainable and ethically produced luxury goods, prompting both global and local players to adapt their strategies. This shift has led to the introduction of eco-friendly product lines, transparent supply chains, and initiatives aimed at reducing environmental impact. As a result, the market not only fosters competition among established and emerging players but also drives innovation and sustainability within the luxury goods sector. Furthermore, the rise of digitalization and e-commerce platforms has intensified competition, as brands now compete not only in physical retail spaces but also in the online domain.

Singapore Luxury Goods Industry Leaders

-

The Swatch Group Ltd

-

Rolex SA

-

Richemont SA

-

Kering SA

-

LVMH Moët Hennessy Louis Vuitton

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Bvlgari unveiled a trunk show dedicated to its high jewellery and luxury watches at Singapore's heritage House of Tan Yeok Nee. Set against the backdrop of the elegantly restored Teochew mansion, the event highlighted 145 exquisite Bvlgari pieces. Dubbed 'Turmali', the showcase placed a special emphasis on tourmalines, featuring a stunning array from Paraiba tourmalines to rubellites, and showcasing vibrant hues of lagoon, mint, pink, and green.

- August 2024: Italian luxury fashion brand Marni opened its first Singapore boutique at The Shoppes at Marina Bay Sands, with additional VIP retail experiences and private salons for exclusive product previews also scheduled at this mall. The 100 sqm space at Marina Bay Sands showcases the Milan fashion brand’s latest women’s ready-to-wear and accessories collections.

- February 2024: Cartier expanded into Singapore Changi Airport Terminal 3 with a new boutique featuring designs inspired by local landmarks including the Merlion and Gardens by the Bay. The expansion reflects Cartier's strategy to connect with travelers across major global hubs while incorporating local cultural elements.

- February 2024: Louis Vuitton opened its first ultra-exclusive Singapore boutique at Ngee Ann City, designed specifically for Very Important Clients (VICs). The 690 square meter space features private salons, heritage exhibitions, and local design elements including frangipani trees, demonstrating luxury brands' focus on personalized experiences.

Singapore Luxury Goods Market Report Scope

A luxury good is a premium/high-end product available in the market landscape. Singapore luxury goods market is segmented by type into clothing and apparel, footwear, bags, jewelry, watches, and other accessories. By distribution channel, the market is segmented into single-branded stores, multi-brand stores, online retail stores, and other distribution channels.. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Clothing and Apparel |

| Footwear |

| Eyewear |

| Jewelry |

| Leather Goods |

| Watches |

| Other Types |

By End User

| Men |

| Women |

| Unisex |

By Distribution Channel

| Single Brand Stores |

| Multi Brand Stores |

| Online Stores |

| Other Distribution Channels |

| By Product Type | Clothing and Apparel |

| Footwear | |

| Eyewear | |

| Jewelry | |

| Leather Goods | |

| Watches | |

| Other Types | |

| By End User | Men |

| Women | |

| Unisex | |

| By Distribution Channel | Single Brand Stores |

| Multi Brand Stores | |

| Online Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the value of luxury goods sales in Singapore in 2025?

Sales total USD 10.45 billion, and they are projected to reach USD 14.26 billion by 2030.

Which product category currently generates the highest revenue?

Jewelry leads with 26.72% share of 2024 sales.

How fast is the watches segment expected to expand?

Watches are forecast to advance at a 7.18% CAGR during 2025-2030.

What rental trend affects Orchard Road boutiques?

Prime-retail rents climbed 4.1% in 2023 while vacancies fell to a decade-low 6.6%, pushing brands to optimize store productivity.

Page last updated on: