Singapore Data Center Construction Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2031 |

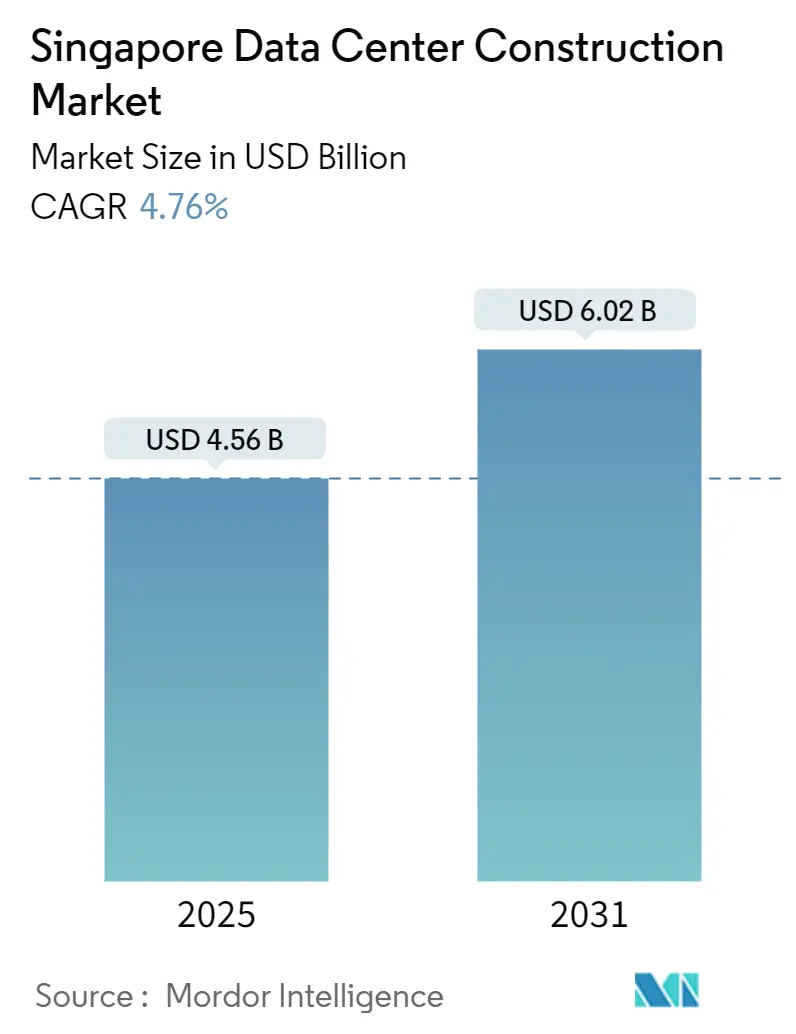

| Market Size (2025) | USD 4.56 Billion |

| Market Size (2031) | USD 6.02 Billion |

| Growth Rate (2025 - 2031) | 4.76% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Singapore Data Center Construction Market Analysis by Mordor Intelligence

The Singapore data center construction market size is valued at USD 4.56 billion in 2025 and is forecast to reach USD 6.02 billion by 2031, advancing at a 4.76% CAGR over the period. Singapore’s tightly managed power-allocation policy, robust subsea connectivity, and status as a financial hub anchor sustained investment even as operators confront land scarcity and high build costs. Regulatory momentum under the Green Data Centre Roadmap encourages designs that achieve Power Usage Effectiveness (PUE) of 1.3 or better, reshaping tender specifications and equipment choices. Hyperscalers continue to deploy GPU-dense infrastructure that pushes average rack power beyond 50 kW, accelerating demand for advanced switchgear, liquid cooling, and modular prefabrication. Meanwhile, the twin-hub strategy that links Singapore with Johor mitigates local constraints by allowing capacity spill-over while preserving sub-5 ms latency to core workloads. Investor appetite for data-center REITs supports a healthy project finance pipeline, helping developers offset the city-state’s premium land and labor costs.

Key Report Takeaways

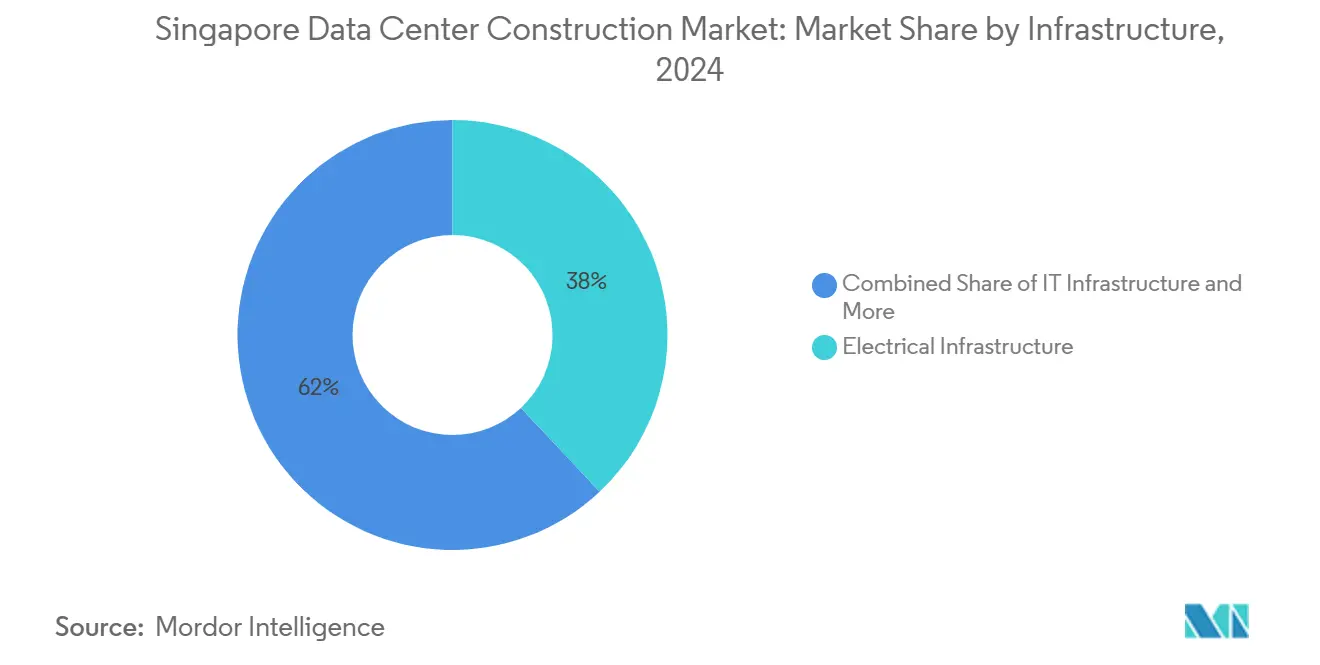

- By infrastructure, electrical systems captured 38% revenue share of the Singapore data center construction market in 2024, while liquid-based cooling is projected to expand at a 4.76% CAGR through 2031.

- By tier standard, Tier III facilities held 54% of the Singapore data center construction market share in 2024; Tier IV builds are forecast to grow at 5.16% CAGR to 2031.

- By end-user industry, IT and telecommunications accounted for 36% of the Singapore data center construction market size in 2024, whereas the AI/HPC segment is poised for 4.90% CAGR during the outlook period.

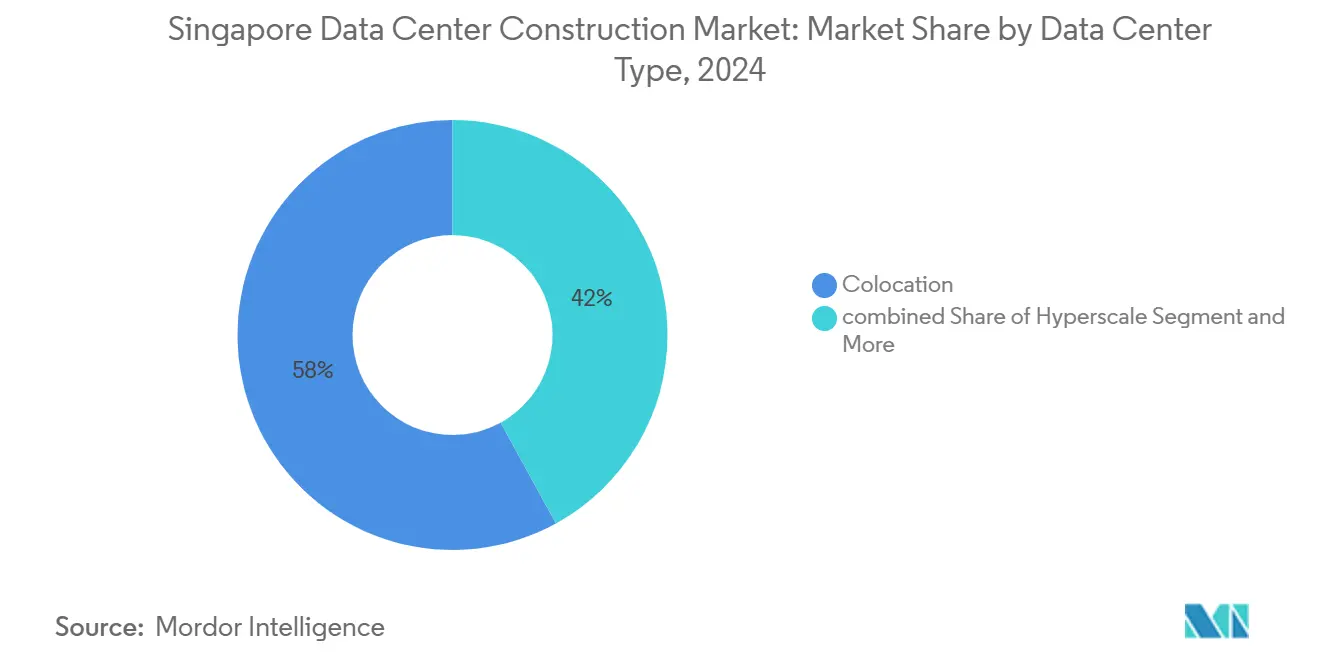

- By data center type, colocation maintained 58% share of the Singapore data center construction market size in 2024, yet hyperscale/self-build projects exhibit the fastest CAGR at 7.10% through 2031.

Singapore Data Center Construction Market Trends and Insights

Drivers Impact Analysis

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Power-allocation release under Green DC Roadmap | +1.2% | National (Jurong, Loyang) | Medium term (2–4 years) |

| Surge in AI/GPU-dense workloads | +1.8% | Global demand; Singapore hub | Short term (≤2 years) |

| Hyperscaler “Singapore-plus-Johor” twin-hub builds | +0.9% | Cross-border ASEAN | Long term (≥4 years) |

| Accelerating sovereign-cloud and MAS FSI localization | +0.6% | National | Medium term (2–4 years) |

| Investor appetite for DC-REIT conversions | +0.4% | Regional capital markets | Short term (≤2 years) |

| Modular prefabrication to compress build-times | +0.7% | National | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Power-Allocation Release Under Green DC Roadmap

Singapore’s revised Green Data Centre Roadmap commits at least 300 MW of new IT load on the condition that facilities demonstrate PUE of 1.3 or lower, pivoting the Singapore data center construction market toward highly efficient designs. Two-thirds of the quota rewards projects that integrate renewables or alternative backup fuels, prompting developers to specify hydrogen-ready generators and heat-recovery chillers. Early movers have implemented AI-driven cooling control to reduce energy use by up to 30%.[1]ST Telemedia Global Data Centres, “STT GDC Collaborates with Phaidra to Optimise Data Centre Cooling,” sttelemediagdc.com Competitive bidding for scarce megawatts intensifies, raising design consultancy demand and favoring firms with a proven sustainability track record. Over the medium term, the policy accelerates the market’s migration toward liquid cooling and on-site solar plus energy-storage hybrids. These elements together enlarge the addressable opportunity for specialist contractors and equipment vendors within the Singapore data center construction market.

Surge in AI/GPU-Dense Workloads Requiring New Build Specs

The generative-AI wave lifts rack densities above 50 kW, forcing mechanical and electrical packages in the Singapore data center construction market to pivot toward immersion and direct-to-chip cooling. A major campus upgrade showcases this shift, featuring chilled-water and liquid-cooling loops designed for 27 °C set-points.[2]Light Reading, “Google Invests USD 5B in Latest Infrastructure Expansion in Singapore,” lightreading.com High-density deployment elongates cable runs and upsizes busways, which increases bill-of-materials value yet lengthens commissioning time by 15–20%. Developers respond by adopting rear-door heat exchangers and medium-voltage (22 kV) power distribution to reduce copper usage. As AI inferencing proliferates across finance, healthcare, and public-sector workloads, construction pipelines increasingly bundle specialized white space for GPU pods, helping the Singapore data center construction market sustain double-digit project count growth despite the national power cap.

Hyperscaler “Singapore-plus-Johor” Twin-Hub Build Strategies

Land scarcity and power quotas propel operators to anchor core workloads in Singapore while situating scalable capacity in Johor, 35 km away across the Causeway. Johor approved 42 projects totaling more than 2,500 MW in Q2 2025, offering construction cost savings of 40–50% versus Singapore. A 150 MW, USD 280 million campus exemplifies this twin-hub blueprint, linking to Singapore via dual subsea fiber for sub-5 ms round-trip latency.[3]Princeton Digital Group, “PDG Secures USD 280 Million Green Loan for Johor Campus,” princetondg.com The model fosters standardized modular designs, enabling contractors to replicate fit-outs on both sides of the border and shortening learning curves. Over the long term, the cross-border ecosystem augments facility count without breaching Singapore’s environmental thresholds, entrenching the Singapore data center construction market as the command node for ASEAN workloads.

Accelerating Sovereign-Cloud and MAS FSI Localization Rules

The Monetary Authority of Singapore mandates local processing for critical financial data, spurring demand for Tier III and Tier IV builds with 2N redundancy, biometric access, and SEC-compliant audit trails. Government Cloud migration, which reached 80% of targeted systems by 2024, sets procurement precedents that influence private-sector specifications. Financial clients sign 10-year anchored leases, underpinning predictable cash flows that de-risk construction financing inside the Singapore data center construction market. Compliance features—including separated air-flows and raised-floor isolation—add 15–25% to build costs but enhance long-term occupancy rates. The rule set also stimulates advanced DDoS protection rooms, creating niche scope for specialists in cyber-resilient facility design.

Restraints Impact Analysis

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Tight 300 MW annual power quota and moratorium legacy | –1.4% | National | Long term (≥4 years) |

| Highest APAC construction cost (USD 11.7 m/MW) and 19 ¢/kWh tariffs | –0.8% | National | Medium term (2–4 years) |

| Scarce brown-field plots; feasibility of underground/high-rise unproven | –0.6% | Urban core | Long term (≥4 years) |

| Skilled MEP labor crunch inflating project timelines | –0.5% | National | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Tight 300 MW Annual Power Quota and Moratorium Legacy

Singapore’s power-allocation ceiling, reinstated in 2024 after a three-year moratorium, falls below regional demand growth, stalling many planned hyperscale builds. Developers must compete in a Call-for-Application process whose scoring heavily weights PUE and carbon intensity, inflating pre-construction consultancy fees. The scarcity of megawatts drove some operators to shift incremental capacity to Batam or Johor, dampening the full revenue potential of the Singapore data center construction market. Long-term uncertainty also complicates transformer and generator ordering cycles, with lead times already stretched by global supply constraints. Together, these factors shave an estimated 1.4 percentage points from forecast CAGR.

Highest APAC Construction Cost and Premium Power Tariffs

Decades of industrial expansion left few shovel-ready parcels zoned for high-density IT use inside Singapore’s urban core. Keppel and JTC Corporation are studying underground caverns and 20-story data-center towers, yet pilot economics remain inconclusive. Vertical stacking complicates fire-suppression design, while subterranean sites demand sophisticated venting and evacuation systems that push project costs higher. Zoning regulations also cap rooftop solar placement, limiting on-site renewables. Until novel formats reach commercial proof, land scarcity continues to constrain the Singapore data center construction market, encouraging outward migration of large-footprint builds.

Segment Analysis

By Infrastructure: AI-Ready Electrical Systems Lead Value Capture

The electrical package accounted for 38% of overall spend within the Singapore data center construction market in 2024, reflecting hyperscaler preference for 22 kV feeds, intelligent switchgear, and high-capacity busways designed for GPU racks running at 50 kW and above. Liquid-based cooling, though still a subset of mechanical infrastructure, is the fastest-growing line item and will contribute USD 635 million to the Singapore data center construction market size by 2031. Adoption of immersion tanks and rear-door heat exchangers reduces white-space real estate per rack, enabling higher revenue density for colocation operators. Services such as design-build integration and commissioning enjoy premium billing rates because owners demand turnkey validation of PUE targets. Over the forecast window, integration between electrics and controls will deepen as AI-driven optimization platforms require real-time telemetry from both power and cooling loops. This convergence elevates the strategic value of firms that can span electrical and mechanical scopes in a single contract, cementing their competitive position within the Singapore data center construction market.

The mechanical segment is evolving from traditional chillers toward pumped refrigerant and dielectric immersion systems capable of dissipating 1,200 W per chip. A joint program cut cooling energy by 29%, saving roughly USD 25,000 per rack annually and setting a cost-avoidance benchmark other operators now target. General construction remains a steady contributor driven by multi-story shells, seismic reinforcement, and blast-resistant façades required under Singapore’s stringent codes. IT infrastructure—racks, network fabric, and cable management—captures incremental spend as high-density layouts demand thicker fiber trunks and AI-optimized topologies. Collectively, these shifts underscore how rising workload complexity expands wallet share for specialized subcontractors in the Singapore data center construction market.

Note: Segment shares of all individual segments available upon report purchase

By Tier Standard: Tier III Holds Sway, Tier IV Accelerates

Tier III facilities delivered 54% of the Singapore data center construction market share in 2024 thanks to their balanced cost-reliability proposition and 99.982% uptime guarantee. Enterprises and cloud providers value concurrently maintainable infrastructure that supports live upgrades without the doubled capex of 2N systems. Nevertheless, Tier IV pipelines are expanding at 5.16% CAGR, fueled by fintech, trading desks, and sovereign-cloud workloads that demand 99.995% availability. These fault-tolerant sites typically deploy 2N UPS, dual fuel farms, and independent chilled-water plants, doubling MEP scope relative to Tier III and lifting the Singapore data center construction market size for high-tier builds.

Iron Mountain’s Singapore facility typifies Tier IV attributes with three geographically diverse meet-me-rooms and bio-protected access corridors. Although Tier I and II projects persist in edge or telco applications, their contribution to revenue remains marginal. Over time, regulatory and customer pressure for resilience is expected to pull Tier III specifications closer to Tier IV, blurring distinctions and increasing the baseline spend per megawatt across the Singapore data center construction market.

By Data Center Type: Colocation Stable, Hyperscale Accelerating

Colocation facilities composed 58% of total capacity in 2024, leveraging Singapore’s carrier-dense ecosystem at SG1, SG3, and Serangoon North to attract latency-sensitive workloads. Multi-tenant demand remains strong among SaaS providers and regional enterprises seeking cross-connect richness. Yet hyperscale/self-build projects represent the fastest-growing slice at 7.10% CAGR as cloud majors pursue dedicated campuses that optimize internal network architecture and security controls. Amazon’s USD 9 billion program illustrates this pivot, embedding proprietary hardware layouts and renewable-ready diesel generators into campus-wide master plans.

Enterprise/edge/modular builds address 5G MEC, content-delivery, and robotics workloads that require near-user processing in high-rent urban zones. StarHub and HPE’s 5G MEC pilot demonstrates how miniaturized nodes integrate with public cellular networks to sustain SLA-driven latency of 20 ms or lower. The interplay of colocation and hyperscale formats ensures balanced landlord risk and attracts a varied contractor ecosystem, collectively enlarging the Singapore data center construction market.

By End-User Industry: IT and Telecoms Dominate, AI/HPC Surges

IT and telecommunications retained 36% share of the Singapore data center construction market size in 2024, underpinned by multi-billion-dollar expansion from Amazon, Google, and Microsoft. Their self-builds emphasize GPU clusters, proprietary network fabrics, and highly automated operations that feed demand for advanced MEP solutions. The AI/HPC segment, though smaller, clocks the highest 4.90% CAGR as research institutes, drug-discovery firms, and quant trading shops request bespoke white space for liquid-cooled supercomputing. Each deployment often exceeds 100 kW per cabinet, requiring specialized floor loading and power distribution schemes within the Singapore data center construction industry.

Banking, financial services, and insurance continue to commission compliance-ready suites featuring biometric security and real-time transaction monitoring, ensuring a recurring retrofit stream for contractors. Government and defense procurements leverage commercial cloud under strict sovereignty constraints, broadening the colocation tenant-mix and raising the minimum security specification. Healthcare, manufacturing, and logistics verticals adopt edge nodes for telemedicine and IoT, respectively. This diversified demand profile inoculates the Singapore data center construction market against single-sector cyclicality and fosters a robust long-term pipeline.

Geography Analysis

Singapore packs more than 1.4 GW of installed IT load into just 728 km², making it one of the most density-optimized footprints globally. Active builds cluster in Jurong East, Loyang, and Serangoon because zoning permits high-floor loading and easier grid interconnects. New master-plan concepts explore subterranean caverns to unlock capacity without consuming scarce surface land, although ventilation and evacuation complexities continue to challenge feasibility. High-rise designs above 15 stories are also under study, promising better land efficiency yet demanding inventive seismic and smoke-extraction solutions that inflate capex.

The Johor-Singapore special economic corridor amplifies regional capacity. Malaysian regulators cleared 2,500 MW of projects in Q2 2025 alone, positioning Johor as a low-cost spill-over node tethered to Singapore by fiber paths delivering sub-5 ms latency. This twin-hub approach allows operators to house transactional workloads in Singapore while shifting batch processing across the Causeway, effectively extending the Singapore data center construction market without breaching local power caps.

Beyond immediate borders, Singapore-headquartered firms such as ST Telemedia Global Data Centres are scaling into India, Indonesia, and Thailand, capitalizing on brand credibility built at home to win land concessions overseas. The outbound push reinforces Singapore’s role as an engineering and financing command center even as physical builds disperse across ASEAN. For contractors and equipment suppliers, this pattern unlocks multi-country order streams anchored on Singapore-based decision making.

Competitive Landscape

The Singapore data center construction market is moderately concentrated: the top five operators collectively control roughly 45% of installed capacity. Market leaders ST Telemedia Global Data Centres, Equinix, and Digital Realty differentiate through technology partnerships that sharpen energy efficiency and speed-to-market. STT’s collaboration with Phaidra harnesses reinforcement learning to shave cooling energy, while Digital Realty’s pilot of liquid-cooled racks marks an industry first locally. No single player exceeds 20% share, creating entry lanes for specialist builders focusing on sovereign-cloud, healthcare, or edge form factors.

Strategic activity remained brisk in 2025. Keppel DC REIT recycled mature assets to release capital for green-field projects, and NTT DC REIT’s USD 773 million IPO opened an additional funding tap for new developments. Hyperscalers pursued self-build campuses to lock in bespoke electrical and network architectures, often contracting multi-year framework agreements with EPC consortia to secure pricing. Technology adoption serves as a competitive fulcrum: immersion cooling, AI-enabled building-management systems, and hydrogen-ready backup generators command premium tenancy and better power-allocation scores.

Niche players are carving out positions in modular prefabrication and underground construction studies, leveraging intellectual property to penetrate segments overlooked by incumbents. As power quotas persist, differentiation will hinge on Watts-per-hectare metrics and renewable-energy integration rather than raw floor space. Consequently, design-build firms that can guarantee sub-1.3 PUE and accelerated time-to-revenue look set to capture outsized value in the Singapore data center construction market.

Singapore Data Center Construction Industry Leaders

-

Boustead Projects

-

Dragages Singapore (Bouygues)

-

Takenaka Corp.

-

Gammon Pte Ltd (Balfour Beatty)

-

Kajima Overseas Asia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Johor state government approved 42 data-center construction projects in Q2 2025, totaling more than 2,500 MW of planned capacity to support the Singapore-Johor twin-hub strategy.

- July 2025: NTT DC REIT completed Singapore’s largest REIT IPO in a decade, raising USD 773 million with an initial portfolio that includes one Serangoon North facility.

- July 2025: Princeton Digital Group delivered phase one of its AI-ready JH1 campus in Johor as part of a USD 1.5 billion investment.

- June 2025: Google committed USD 5 billion to expand its Singapore cloud campus, embedding liquid-cooling systems tailored for AI workloads.

Singapore Data Center Construction Market Report Scope

A data center is a physical room, building, or facility that holds IT infrastructure used to construct, run, and provide applications and services and store and manage the data connected with them. Under data center construction, the capital expenditure incurred while building the existing data center facilities is tracked, and the future capex is estimated based on upcoming data center facilities.

The Singaporean data center construction market is segmented by infrastructure (electrical infrastructure (power distribution solution (PDU, transfer switches, switchgear, power panels, and components)), power backup solution (UPS and generators), service - design and consulting, integration, and support and maintenance)), (mechanical infrastructure (cooling systems (immersion cooling, direct-to-chip cooling, rear door heat exchanger, and in-row and in-rack cooling)), racks, and other mechanical infrastructure)), and general construction)), tier type (Tier 1 and 2, Tier 3, and Tier 4), and end user (banking, financial services and insurance, IT and telecommunications, government, defense, healthcare, and other end users). The market size and forecasts are provided in value (USD) for all the above segments.

| Electrical Infrastructure | Power Distribution Solutions | Power Distribution Units |

| Switchgears | ||

| Others | ||

| Power Backup Solutions | UPS | |

| Generators | ||

| Mechanical Infrastructure | Cooling Systems | Liquid-based Cooling |

| Air-based Cooling | ||

| Racks and Cabinets | ||

| Other Mechanical Infrastructure | ||

| IT Infrastructure | Servers | |

| Storage | ||

| Other IT Infrastructure | ||

| General Construction | ||

| Services | Design and Consulting | |

| Integration | ||

| Support and Maintenance | ||

| Tier I and II |

| Tier III |

| Tier IV |

| Banking, Financial Services and Insurance |

| IT and Telecommunications |

| Government and Defense |

| Healthcare |

| Other End Users |

| Colocation Facilities |

| Hyperscale / Self-built |

| Enterprise / Edge / Modular |

| By Infrastructure | Electrical Infrastructure | Power Distribution Solutions | Power Distribution Units |

| Switchgears | |||

| Others | |||

| Power Backup Solutions | UPS | ||

| Generators | |||

| Mechanical Infrastructure | Cooling Systems | Liquid-based Cooling | |

| Air-based Cooling | |||

| Racks and Cabinets | |||

| Other Mechanical Infrastructure | |||

| IT Infrastructure | Servers | ||

| Storage | |||

| Other IT Infrastructure | |||

| General Construction | |||

| Services | Design and Consulting | ||

| Integration | |||

| Support and Maintenance | |||

| By Tier Standard | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By End-User Industry | Banking, Financial Services and Insurance | ||

| IT and Telecommunications | |||

| Government and Defense | |||

| Healthcare | |||

| Other End Users | |||

| By Data Center Type | Colocation Facilities | ||

| Hyperscale / Self-built | |||

| Enterprise / Edge / Modular | |||

Key Questions Answered in the Report

What is the forecast value of the Singapore data center construction market in 2031?

The market is projected to reach USD 6.02 billion by 2031.

How fast is the Singapore data center construction market expected to grow?

It is forecast to expand at a 4.76% CAGR between 2025 and 2031.

Which infrastructure segment holds the largest share in recent builds?

Electrical systems lead with a 38% revenue share as of 2024.

Why are Tier IV facilities gaining momentum?

Financial and AI workloads require 99.995% uptime, driving Tier IV builds that grow at 5.16% CAGR.

How does the twin-hub strategy with Johor benefit operators?

It offers 40-50% cost savings and sub-5 ms latency while easing Singapores land and power constraints.

What constrains new capacity inside Singapore itself?

A 300 MW annual power quota, land scarcity, and high construction costs limit local expansion.

Page last updated on: