Singapore Chemical Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

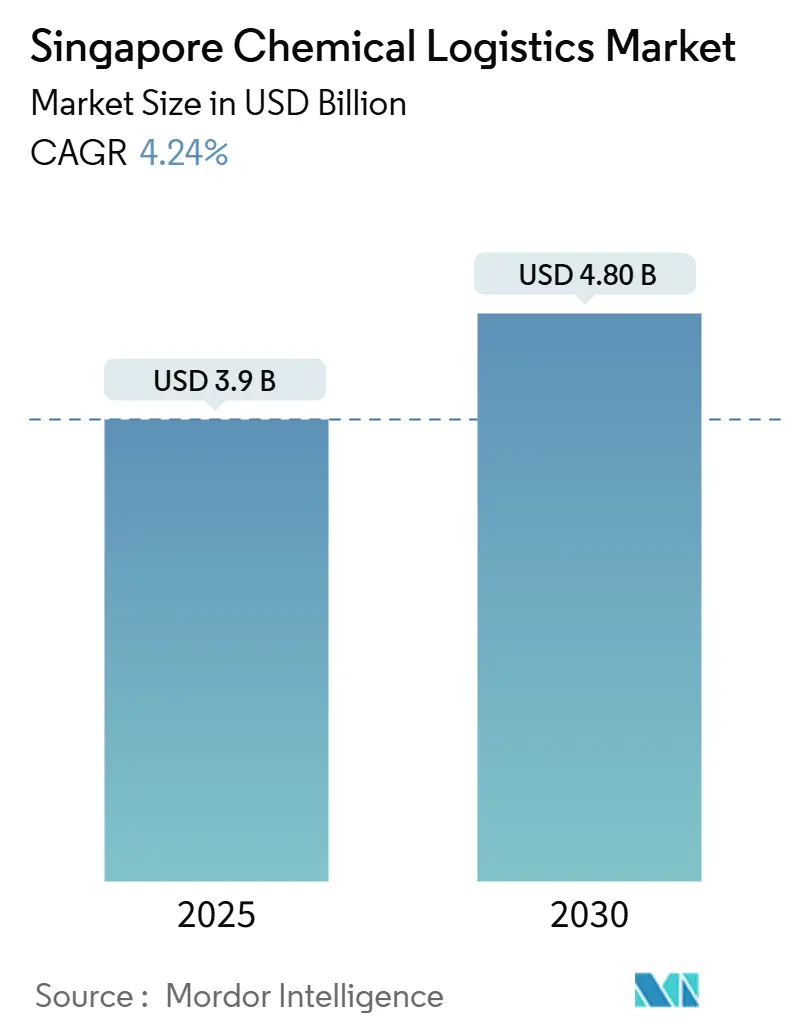

| Market Size (2025) | USD 3.9 Billion |

| Market Size (2030) | USD 4.80 Billion |

| Growth Rate (2025 - 2030) | 4.24% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Singapore Chemical Logistics Market Analysis by Mordor Intelligence

The Singapore Chemical Logistics Market size is estimated at USD 3.9 billion in 2025, and is expected to reach USD 4.80 billion by 2030, at a CAGR of 4.24% during the forecast period (2025-2030).

Strong throughput at Tuas Port, Jurong Island’s USD 50 billion petrochemical cluster, and continued life-science investments underpin steady demand for specialized transportation, warehousing, and compliance services. Growing volumes of hazardous and temperature-sensitive chemicals are pushing providers to adopt advanced automation, cold-chain technology, and digital control towers. At the same time, government-backed port modernization, stable regulatory oversight, and ASEAN trade harmonization reinforce Singapore’s gateway role even as land scarcity and rising costs temper expansion plans. The Singapore chemical logistics market continues to benefit from these structural advantages while facing intensifying regional competition for transshipment flows.

Key Report Takeaways

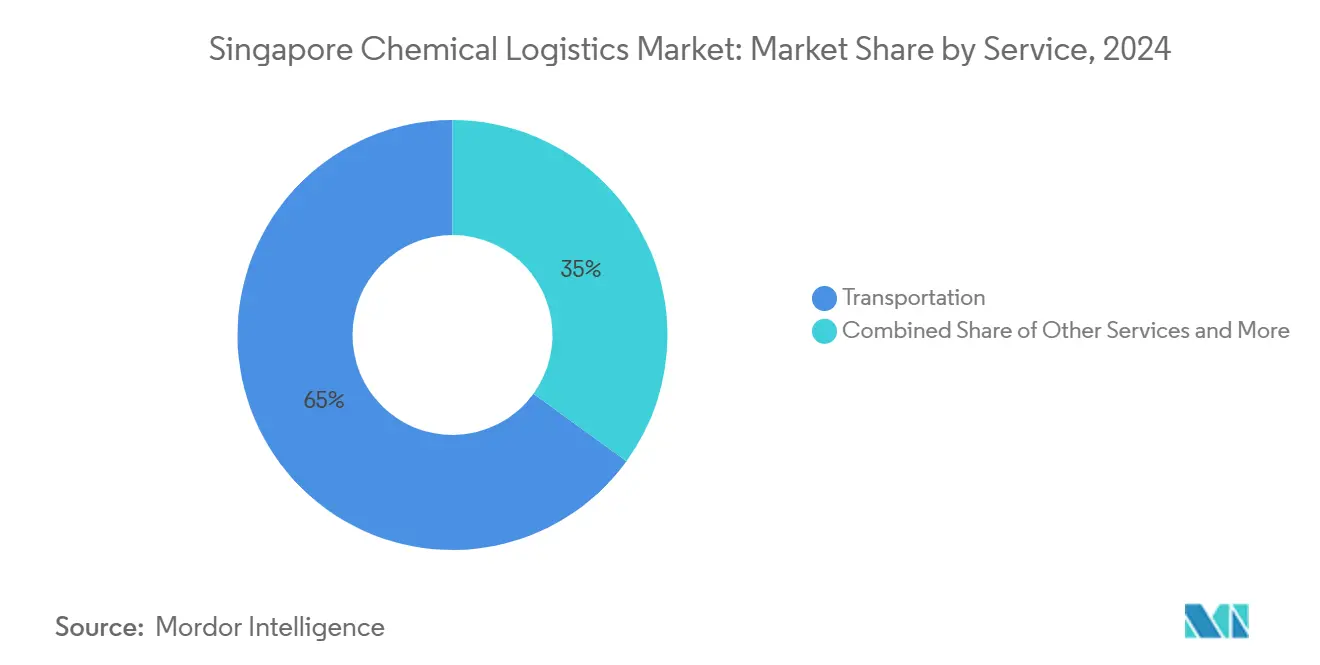

- By service, transportation commanded a 65% revenue share in 2024, while warehousing, distribution & inventory management are expanding at a 3.60% CAGR through 2030.

- By end-user industry, oil & gas held 24% of Singapore chemical logistics market share in 2024; pharmaceuticals are forecast to grow at a 4.10% CAGR through 2030.

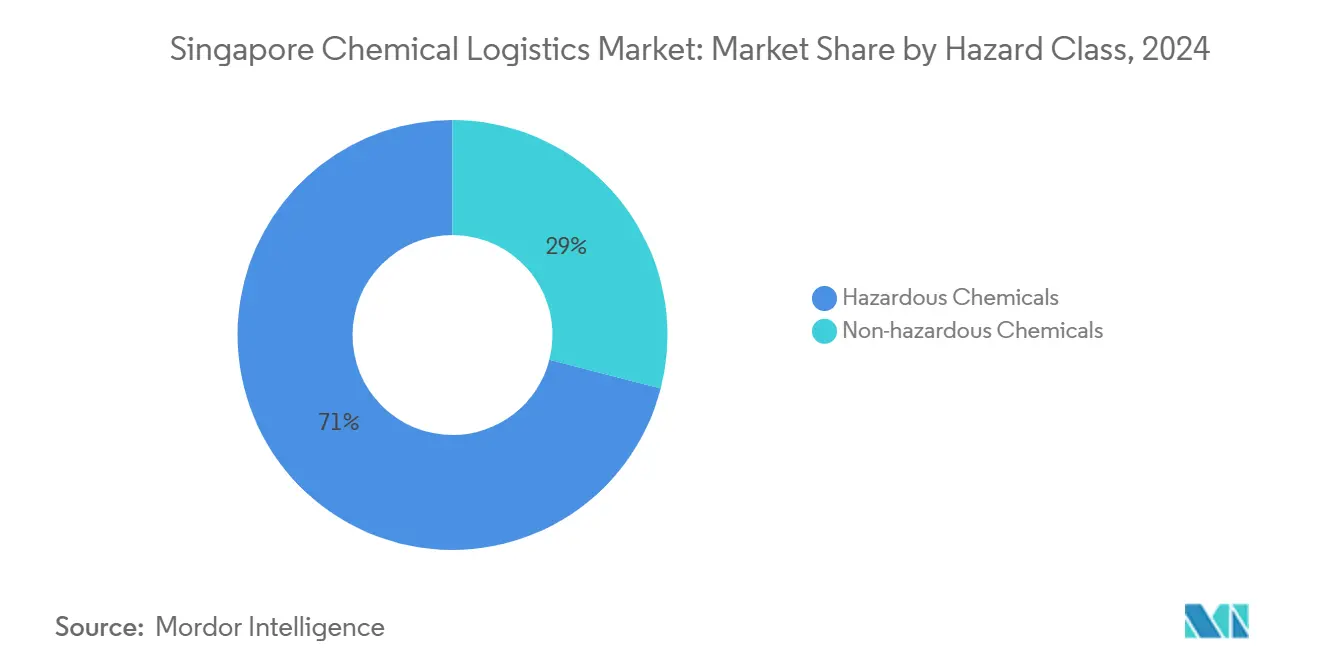

- By hazard class, hazardous chemicals accounted for 71% of Singapore chemical logistics market size in 2024 and are advancing at a 4.60% CAGR to 2030.

- By temperature control, non-temperature-controlled cargo dominated with 69% share in 2024, whereas temperature-controlled logistics is projected to expand at a 4.20% CAGR.

Singapore Chemical Logistics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding petrochemical production on Jurong Island | +1.2% | Singapore, with spillover to ASEAN | Medium term (2-4 years) |

| Government investment in Tuas Mega-Port infrastructure | +0.9% | Singapore, regional transshipment benefits | Long term (≥ 4 years) |

| Rising demand for temperature-controlled & specialty chemical storage | +0.7% | Singapore, regional pharmaceutical hub | Short term (≤ 2 years) |

| Digitalisation of supply chains (IoT, blockchain, control-tower platforms) | +0.5% | Singapore, with technology export potential | Medium term (2-4 years) |

| Growth of sustainable bio-based chemical clusters needing 'green' logistics | +0.4% | Singapore, ASEAN sustainable chemicals | Long term (≥ 4 years) |

| ASEAN regulatory harmonisation boosting Singapore's trans-shipment hub role | +0.3% | ASEAN-wide, Singapore as primary beneficiary | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Petrochemical Production on Jurong Island

Evonik’s SGD 1.5 billion (USD 1.1 billion) capacity expansion, completed in 2024, cements Jurong Island as the world’s largest methionine producer with more than 40% global share[1]Sue-Ann Tan, “Speciality Chemicals Giant Evonik Expands Facility on Jurong Island,” The Straits Times, straitstimes.com. Large-scale investments are shifting the product mix toward higher-value specialty and bio-based chemicals that require stringent handling, tank-farm connectivity, and multimodal dispatch. The integrated pipeline grid reduces truck movements but increases demand for on-island intermediate storage and just-in-time shuttle services. Cosco Shipping’s plan to double its Jurong Island Logistics Hub to 200,000 TEU by 2026 illustrates the direct relationship between manufacturing scale-up and logistics infrastructure. These developments enlarge the Singapore chemical logistics market by creating premium, specialized flows that few regional hubs can match.

Government Investment in Tuas Mega-Port Infrastructure

Singapore’s USD 20 billion Tuas Mega-Port is deploying over 200 automated guided vehicles, remote crane operations, and real-time orchestration platforms that slash berth times and improve hazardous-cargo segregation. The adjoining PSA Supply Chain Hub @ Tuas, a SGD 647.5 million (USD 476.6 million) facility with automated storage and retrieval systems, offers value-added consolidation tailored to chemical cargo. Automation lowers per-container handling cost even as Singapore’s labor rates rise, sustaining the Singapore chemical logistics market’s cost competitiveness relative to regional peers. As more petrochemical and pharmaceutical producers direct exports through Tuas, end-to-end visibility and risk control improve, reinforcing shipper confidence in Singapore.

Rising Demand for Temperature-Controlled & Specialty Chemical Storage

GDP-compliant cold rooms, 2-8°C chambers, and 15-25°C ambient zones are now standard at new multi-tenant facilities such as DHL’s EUR 10 million (USD 10.4 million) Jurong Pier pharma hub. Rental premiums for cold storage units exceed standard chemical warehouses by a double-digit margin due to continuous monitoring, backup power, and validated processes. Automated storage and retrieval systems reduce worker exposure to sub-zero environments while cutting energy consumption, addressing both cost and sustainability mandates. As biologics and advanced materials proliferate, cold-chain reliability becomes a decisive differentiator within the Singapore chemical logistics market.

Digitalisation of Supply Chains

The Maritime and Port Authority’s digitalPORT@SG platform consolidates 16 forms into one electronic clearance, saving 100,000 man-hours every year[2]Maritime and Port Authority of Singapore, “Port of the Future,” mpa.gov.sg. PSA’s CALISTA, integrated with the NEO operating platform, provides real-time traceability across 100 routes and automates dangerous-goods documentation. IoT sensors monitor temperature, vibration, and location, feeding blockchain-secured ledgers that regulators and shippers alike can audit instantly. These capabilities increase compliance confidence and lower administrative overhead, enhancing the overall value proposition of the Singapore chemical logistics market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High operating costs (land, labour, utilities) | -0.8% | Singapore, competitive pressure from regional hubs | Short term (≤ 2 years) |

| Scarcity of industrial land for new hazmat warehouses | -0.6% | Singapore, affecting capacity expansion | Medium term (2-4 years) |

| Decarbonisation mandates requiring high CAPEX for fleet & fuel transition | -0.4% | Singapore, with regulatory compliance requirements | Long term (≥ 4 years) |

| Manpower bottlenecks for licensed hazmat drivers & technicians | -0.3% | Singapore, skilled labor constraints | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Operating Costs (Land, Labor, Utilities)

SI Group closed its Jurong Island alkylphenol facility in 2025, citing elevated costs, underscoring the squeeze on service providers that depend on throughput volume to amortize fixed expenses. Warehouse supply trails demand by roughly 600,000 sq ft annually, pushing rents higher than regional averages. Wage inflation compounds the challenge; semiconductor engineering roles were added to Singapore’s shortage occupation list in late 2024[3]Goh Ruoxue, “SI Group Closure,” The Business Times, businesstimes.com. The Refundable Investment Credit and green-logistics grants soften the impact, yet smaller operators still struggle to maintain margins within the Singapore chemical logistics market.

Scarcity of Industrial Land for New Hazmat Warehouses

The Industrial Government Land Sales program released only 14.07 ha for logistics in H1 2025, and forecast single-user factory supply drops to 2.2 million sq ft post-2027. Mandatory solar-panel installation and strict building-height limits add cost and complexity for hazardous-material projects. Consequently, many operators retrofit aging stock rather than develop greenfield sites, driving consolidation as firms with existing footprints gain pricing power. Land scarcity thus curbs short-term capacity expansion in the Singapore chemical logistics market.

Segment Analysis

By Service: Transportation Dominance Amid Warehousing Acceleration

Transportation accounted for 65% of the Singapore chemical logistics market size in 2024, anchored by high container throughput and continuous barge and tanker shuttle runs between Jurong Island terminals. Automated guided vehicles and predictive berth scheduling at Tuas lower operating cost per move, allowing carriers to sustain service levels even with tight vessel windows. Road haulage remains primary for inland moves; rail use is negligible, while air handles niche ADR-class cargos.

Warehousing, distribution & inventory management services, though smaller, are forecast to log a 3.60% CAGR to 2030 as shippers seek single-site inventory and value-added packaging. Sankyu Singapore’s 38,380 m² automated hub exemplifies next-generation facilities combining hazmat segregation, temperature zoning, and robotics. Integrated service contracts covering inbound clearance, storage, and on-demand delivery are becoming the norm, expanding the addressable share of the Singapore chemical logistics market. Consultancy and compliance services form the smallest slice but command premium unit margins due to specialized licensing requirements.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Oil & Gas Leadership with Pharmaceutical Momentum

Oil & gas retained 24% of Singapore chemical logistics market share in 2024, leveraging the city-state’s role as the world’s third-largest oil trading center and its 1.5 million bpd refining complex. Bulk liquid handling dominates, supported by tank-farm cross-pumping and dedicated berths.

Pharmaceutical logistics grows fastest at a 4.10% CAGR to 2030, driven by life-science manufacturing incentives and GDP-compliant infrastructure like DHL’s new hub. Cold-chain protocols, validated packaging, and traceability requirements boost revenue per tonne, tilting the Singapore chemical logistics industry toward higher-value services. Specialty chemicals also gain share as Jurong Island pivots toward sustainable and higher-margin products, reinforcing the market’s complexity and regulatory intensity.

By Hazard Class: Hazardous Chemicals Drive Growth and Complexity

Hazardous cargos represented 71% of the Singapore chemical logistics market size in 2024 and are expanding at a 4.60% CAGR (2025-2030) on the back of more intricate upstream and specialty chemical flows. Stringent route restrictions, licensed drivers, and mandatory vehicle inspections restrict supply, supporting stable pricing for qualified carriers.

Non-hazardous chemicals, at 29%, face stiffer regional competition and lower service differentiation. Regulatory overlap among the National Environment Agency, Singapore Civil Defence Force, and Maritime and Port Authority adds compliance cost that only experienced players can absorb, concentrating value capture within the hazardous segment of the Singapore chemical logistics market.

By Temperature Control: Ambient Majority with Cold-Chain Acceleration

Non-temperature-controlled cargo held a 69% share in 2024, reflecting the continued dominance of petrochemical and commodity flows that do not require controlled environments. Standard warehouses and ISO tanks suffice, keeping operating costs in check.

Conversely, temperature-controlled logistics is projected to grow at a 4.20% CAGR (2025-2030), catalyzed by biologics and advanced materials needing 2-8°C or minus-20°C stability. Continuous monitoring, backup power, and GDP certification raise entry barriers yet yield rental premiums. New projects like DSV Pearl’s LEED Gold facility with multi-zone climate control illustrate future investment direction. Cold-chain sophistication bolsters the long-run value of the Singapore chemical logistics market.

Geography Analysis

Jurong Island anchors chemical manufacturing with over 100 global companies across 3,000 ha and integrated pipeline networks that minimize road haulage and expedite bulk liquids transfer. This concentration creates dense intra-island logistics activity, encouraging investment in specialized barges and on-island shuttle fleets.

Tuas in the western region is the epicenter of maritime throughput; Tuas Port handled 41.12 million TEU in 2024, second only to Shanghai, and its automation edge enhances berth utilization while preserving hazardous-goods segregation. The area, however, faces a 600,000 sq ft annual warehouse shortfall, pressuring rents and nudging operators toward multi-story facilities.

Competitive Landscape

Global terminal operator PSA dominates sea throughput and is spending millions on robotics and ASRS systems to support value-added chemical consolidation. DHL, DSV, and Yusen are expanding cold-chain and sustainable-transport offerings, while local specialists such as Sankyu leverage decades-old hazmat licenses and land banks.

Technology integration differentiates leaders within the Singapore chemical logistics market. PSA’s CALISTA offers blockchain-secured documentation and AI ETA predictions; DHL deploys IoT sensors for end-to-end temperature monitoring, and Yusen leverages ONE LEAF+ carbon-reduced shipping services. Investment in fleet electrification—exemplified by DSV’s Volvo electric trucks—indicates the sector’s response to Singapore’s planned SGD 80 per-ton (USD 58.9 per-ton) carbon tax by 2030.

Barriers to entry remain moderate. Licensing for hazardous-substance storage, multilevel driver training, and land scarcity deter new entrants yet allow regional 3PLs to acquire stakes or form joint ventures with incumbents. Overall, the Singapore chemical logistics market exhibits a balanced mix of global scale and local specialization.

Singapore Chemical Logistics Industry Leaders

-

ALPS Global Logistics

-

Bertschi Singapore Pte Ltd

-

DHL

-

Kuehne + Nagel

-

PSA Chemical Logistics (PSA Corp)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DHL Supply Chain opened an EUR 10 million (USD 10.4 million), 8,200 m² pharma hub at Jurong Pier with GDP-compliant zones and airtight docks.

- February 2025: PSA International rebranded its venture arm to PSA Ventures to fund renewable energy and automation projects.

- February 2025: Yusen Logistics partnered with Ocean Network Express to adopt the ONE LEAF+ green-shipping service.

- November 2024: DSV Air & Sea rolled out Singapore’s first electric truck fleet with Volvo models customized for local ADR operations.

Singapore Chemical Logistics Market Report Scope

The process of organizing and controlling the movement of chemicals and related materials from suppliers to manufacturers and consumers is known as chemical logistics. This procedure guarantees that the appropriate chemicals are delivered to the appropriate locations at the appropriate times. Transportation, storage, inventory management, and security can all be part of chemical logistics. A complete background analysis of the Singaporean chemical logistics market, including the assessment of the economy and contribution of sectors in the economy, a market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics and geographical trends, and COVID-19 impact, is covered in the report.

Singapore's chemical logistics market is segmented by service (transportation, warehousing, and other services), by mode of transportation (roadways, railways, airways, waterways, and other modes of transportation), and by end-user (pharmaceutical industry, cosmetic industry, oil and gas industry, specialty chemicals industry, and other end-users).

The report offers market size and forecast values (USD) for all the above segments.

| Transportation | Road |

| Rail | |

| Air | |

| Sea | |

| Warehousing, Distribution & Inventory Management | |

| Other Services |

| Pharmaceutical |

| Cosmetic |

| Oil & Gas |

| Specialty Chemicals |

| Other End-Users |

| Hazardous Chemicals |

| Non-hazardous Chemicals |

| Temperature-Controlled (Refrigerated/Heated) |

| Non-Temperature-Controlled |

| By Service | Transportation | Road |

| Rail | ||

| Air | ||

| Sea | ||

| Warehousing, Distribution & Inventory Management | ||

| Other Services | ||

| By End-User Industry | Pharmaceutical | |

| Cosmetic | ||

| Oil & Gas | ||

| Specialty Chemicals | ||

| Other End-Users | ||

| By Hazard Class | Hazardous Chemicals | |

| Non-hazardous Chemicals | ||

| By Temperature Control | Temperature-Controlled (Refrigerated/Heated) | |

| Non-Temperature-Controlled |

Key Questions Answered in the Report

What is the current value of the Singapore chemical logistics market?

The market stands at USD 3.90 billion in 2025 and is projected to grow to USD 4.80 billion by 2030.

Which segment is expanding fastest?

Temperature-controlled logistics is advancing at a 4.20% CAGR as pharmaceuticals and specialty chemicals grow.

Why do hazardous cargos dominate volumes?

Jurong Island’s petrochemical output requires advanced safety protocols, giving hazardous chemicals 71% share in 2024.

How is Tuas Mega-Port shaping future capacity?

Automation, real-time control systems, and an integrated supply-chain hub lower turnaround times and support larger chemical volumes.

What challenges do providers face most acutely?

High land and labor costs plus scarce hazmat-zoned sites constrain rapid capacity expansion despite strong demand.

Page last updated on: