| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 13.58 Billion |

| Market Size (2030) | USD 24.00 Billion |

| CAGR (2025 - 2030) | 12.06 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

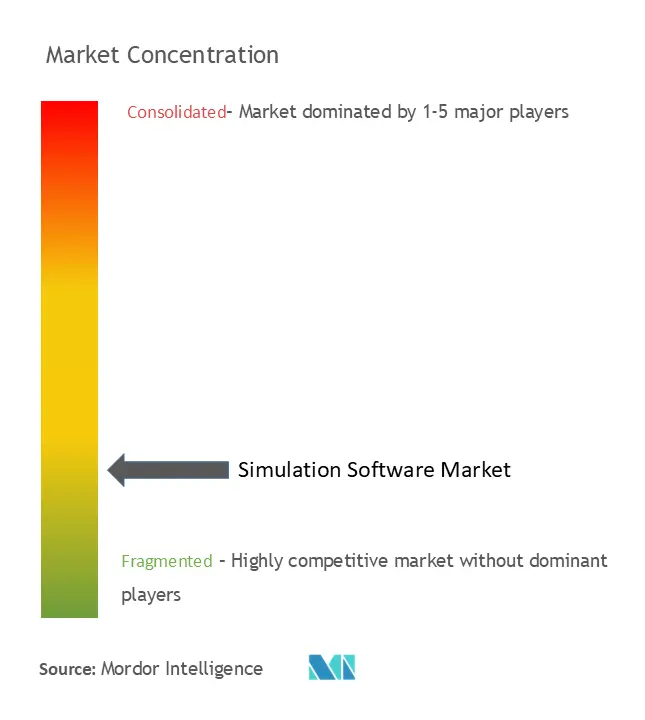

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Simulation Software Market Analysis

The Simulation Software Market size is estimated at USD 13.58 billion in 2025, and is expected to reach USD 24.00 billion by 2030, at a CAGR of 12.06% during the forecast period (2025-2030).

The simulation software industry has undergone a significant transformation from its initial role in production line optimization to becoming an integral part of product development and regulatory compliance across multiple sectors. Manufacturing companies are increasingly leveraging engineering simulation software to address uncertainties in production line modifications and new line construction, primarily driven by the critical need to minimize operational downtime and maintain customer delivery schedules. The technology's evolution has enabled manufacturers to conduct comprehensive pre-implementation testing, resulting in substantial cost savings and improved operational efficiency. This shift has been particularly evident in the automotive sector, where manufacturers are increasing their R&D investments to accommodate advanced manufacturing processes and intricate designs while simultaneously reducing component sizes and enhancing performance metrics.

The integration of simulation software with emerging technologies has created new opportunities across various industries, from manufacturing to engineering services. Major industry players are developing increasingly sophisticated solutions that combine traditional simulation capabilities with advanced analytics and cloud computing. For instance, Siemens' recent modeling of Electrolux's factories demonstrates the software's capability to identify and implement operational efficiencies at scale. Similarly, AnyLogic's collaboration with General Dynamics (NASSCO) has revolutionized the management of complex supply chain operations, handling thousands of parts flowing through shipyards with unprecedented precision and efficiency.

Cloud-based simulation software solutions are gaining significant traction, transforming how organizations approach design and testing processes. According to recent industry surveys, approximately 94% of enterprises are now utilizing cloud technologies, with 91% specifically employing public cloud services for their simulation needs. This shift towards cloud-based solutions has particularly benefited small and medium-sized enterprises (SMEs) by providing access to sophisticated modeling and simulation capabilities without requiring substantial infrastructure investments. The trend is especially pronounced in emerging markets, where SMEs account for a significant portion of economic activity, such as in Brazil, where small businesses contribute 27% to the national GDP.

The educational and research sectors have emerged as significant adopters of simulation software, driving innovation in teaching methodologies and research applications. Academic institutions are increasingly incorporating computer-aided engineering tools into their curriculum to provide hands-on experience in various fields, from engineering to medical training. The software's ability to create realistic scenarios while reducing costs and implementation time has made it particularly valuable in educational settings. This trend is supported by the growing number of partnerships between software providers and educational institutions, leading to the development of specialized digital simulation platforms for academic and research purposes. The integration of simulation software in education has demonstrated measurable improvements in learning outcomes and research capabilities, while simultaneously preparing students for real-world applications in their respective fields.

Simulation Software Market Trends

Increasing Demand for Real-Time Training

The growth of simulation software is intrinsically linked to the escalating demand for real-time training across multiple industries, driven by its ability to provide immediate, practical experience without operational risks. Real-time training simulation enables organizations to observe processes by running replicated scenarios based on real-life situations, incorporating specific mathematical formulas that allow for precise outcome prediction and analysis. This approach has proven particularly valuable in the aviation sector, where the increasing complexity and cost of advanced aircraft development, coupled with rising pilot training expenses, have made simulation-based training an essential tool. The technology allows pilots and operators to gain comprehensive experience in handling various scenarios and emergency situations without risking valuable equipment or human life.

The adoption of real-time training simulation has expanded significantly across diverse sectors, with law enforcement agencies emerging as major beneficiaries of this technology. For instance, the Orlando Police Department has implemented new simulator software that enables officers to undergo real-time training for different scenarios virtually, with automatic feedback mechanisms helping them prepare for real-world situations. In the education sector, institutions like the Dubai College of Tourism have pioneered virtual internship programs featuring real-time training and mentoring by industry experts, demonstrating the technology's versatility in preparing students for professional environments. These implementations highlight the key advantages of simulation-based training, including enhanced knowledge retention, zero operational risk, quantifiable training outcomes, and cost-effectiveness, making it an increasingly attractive option for organizations looking to improve their training methodologies while optimizing resource utilization.

Understand The Key Trends Shaping This Market

Download PDF

Segment Analysis: By Deployment Type

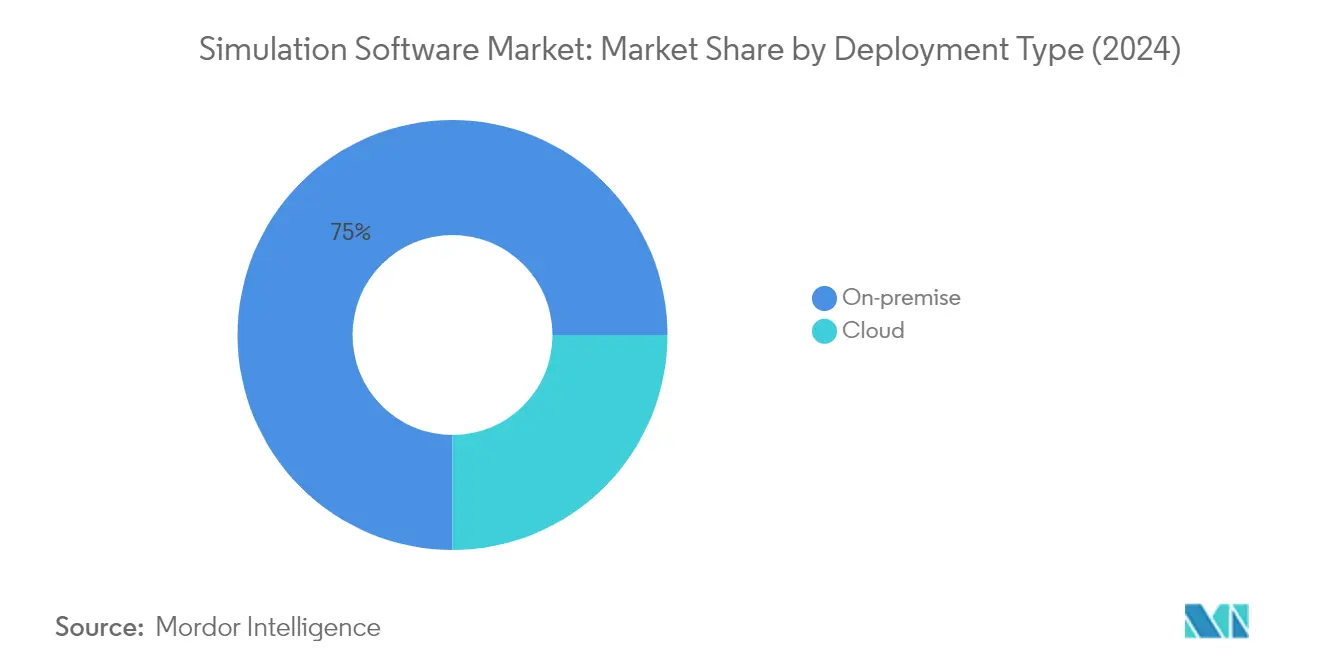

On-Premise Segment in Simulation Software Market

The on-premise deployment segment continues to dominate the simulation software market, holding approximately 75% of the market share in 2024. This significant market position is primarily driven by large organizations from conventional industries that prefer on-premise solutions for their enhanced security features and greater control over data. On-premise systems are loaded with extensive features and offer more flexibility and configurability compared to cloud-based alternatives. Organizations whose operations are performed on-site or in-network particularly favor this deployment model due to its ability to handle complex operations and provide better control over sensitive data. The segment's strength is further reinforced by continuous innovations from major vendors to enhance the effectiveness of their on-premise solutions, particularly in areas such as elastic licensing and optimization of both software and high-performance computing utilization. The integration of computer-aided engineering (CAE) software within on-premise systems is also notable for its role in enhancing engineering simulation capabilities.

Cloud Segment in Simulation Software Market

The cloud deployment segment is experiencing remarkable growth in the simulation software market, projected to grow at approximately 12% during 2024-2029. This growth trajectory is primarily driven by the increasing adoption of cloud-based solutions among small and medium enterprises (SMEs) due to their cost-efficiency and operational flexibility. Cloud deployment facilitates easy operability across various locations without concerns about installing software and maintaining supportive hardware. The segment's growth is further accelerated by the rising trend of remote work and the need for collaborative environments, enabling organizations to process increasing volumes of data at lower costs. Cloud-based simulation solutions are particularly gaining traction in industries requiring complex simulations and analysis, offering scalability and accessibility advantages that traditional deployment methods cannot match. The adoption of process simulation in cloud environments is also a key factor driving growth.

Segment Analysis: By End-User Industry

Electrical and Electronics Segment in Simulation Software Market

The electrical and electronics segment dominates the simulation software market, commanding approximately 22% market share in 2024. This significant market position is driven by the increasing complexity of electronic systems development and the growing need for integrated electrical and mechanical design tools. The segment's strength is particularly evident in applications such as circuit simulation, thermal analysis, and electromagnetic compatibility testing. Major manufacturers are leveraging simulation software to optimize their product development cycles, reduce physical prototyping costs, and ensure compliance with regulatory standards. The adoption of simulation tools in this segment is further accelerated by the rising demand for electronic design automation (EDA) software and the growing trend toward miniaturization in electronics manufacturing. The use of computational fluid dynamics in this sector is crucial for enhancing product design and performance.

Education and Research Segment in Simulation Software Market

The education and research segment is emerging as the fastest-growing sector in the simulation software market, projected to maintain robust growth from 2024 to 2029. This exceptional growth is primarily driven by the increasing adoption of simulation-based learning in educational institutions and research facilities worldwide. The segment's expansion is fueled by the rising demand for virtual learning environments, particularly in medical education, engineering studies, and scientific research. Educational institutions are increasingly incorporating simulation software into their curriculum to provide hands-on training experiences without the associated risks and costs of physical equipment. The growth is further supported by the increasing focus on STEM education and the rising investments in research and development activities across various scientific disciplines. The integration of system simulation tools in educational settings enhances the learning experience by providing realistic and interactive environments.

Remaining Segments in End-User Industry

The simulation software market encompasses several other significant segments, including automotive, aerospace and defense, IT and telecommunication, and energy and mining sectors. The automotive sector utilizes simulation software for vehicle design, testing, and autonomous vehicle development. The aerospace and defense segment employs these tools for aircraft design, mission planning, and training simulations. In the IT and telecommunication sector, simulation software is crucial for network planning and optimization. The energy and mining segment leverages these tools for resource exploration, plant operations, and safety training. Each of these segments contributes uniquely to the market's dynamics, driven by their specific industry requirements and technological advancements. The role of industrial simulation in these sectors is pivotal for optimizing processes and enhancing operational efficiency.

Simulation Software Market Geography Segment Analysis

Simulation Software Market in North America

North America continues to maintain its dominant position in the global simulation software market, commanding approximately 38% of the simulation software market share in 2024. The region's leadership is primarily driven by the strong foothold of major simulation software industry vendors, including Autodesk Inc., ANSYS, The MathWorks Inc., and Synopsys Inc. The presence of a robust technological infrastructure, coupled with high adoption rates of advanced technologies across various industries, particularly in the automotive, aerospace, and defense sectors, continues to fuel simulation software market growth. The region's emphasis on research and development activities, particularly in emerging technologies like autonomous vehicles and digital twins, has created substantial opportunities for simulation software providers. Additionally, the increasing focus on cloud-based simulation solutions, especially among small and medium enterprises, has opened new avenues for market expansion. The U.S. government's smart city initiatives and stringent regulations promoting eco-friendly work environments have further accelerated the adoption of simulation technologies for testing product viability before manufacturing.

Simulation Software Market in Europe

Europe has established itself as a crucial market for the simulation software industry, demonstrating robust growth with an impressive compound annual growth rate of approximately 12% from 2019 to 2024. The region's market dynamics are shaped by the presence of industry giants like Dassault Systèmes and Siemens AG, who continue to drive innovation in simulation technologies. The European market's growth is particularly notable in the automotive and aerospace sectors, where simulation software plays a crucial role in product development and testing. The region's strong focus on digital transformation initiatives, particularly in manufacturing and industrial automation, has created a fertile ground for simulation software adoption. The emergence of innovative startups in the simulation space, coupled with increasing investments in cloud-based services, has further enriched the market ecosystem. The region's commitment to sustainable development and energy efficiency has also driven the adoption of simulation tools for optimizing industrial processes and reducing environmental impact.

Simulation Software Market in Asia-Pacific

The Asia-Pacific simulation software market is positioned for substantial growth, with projections indicating a robust growth rate of approximately 12% during the 2024-2029 period. The region's market is characterized by rapid digital transformation across industries, particularly in the manufacturing and automotive sectors. The increasing adoption of cloud-based solutions among small and medium-sized enterprises has created new opportunities for market expansion. Countries like China, Japan, and South Korea are leading the charge in implementing advanced simulation technologies, particularly in electronics manufacturing and automotive design. The region's growing focus on industrial automation and smart manufacturing initiatives has created a strong demand for simulation software solutions. The presence of a large manufacturing base, coupled with increasing investments in research and development activities, continues to drive market growth. Furthermore, government initiatives promoting digital transformation and Industry 4.0 adoption have created a favorable environment for simulation software providers.

Simulation Software Market in Latin America

The Latin American simulation software market is experiencing steady growth, primarily driven by the increasing digitalization of industries across Brazil and Mexico. The region's market is characterized by growing adoption among small and medium-sized enterprises, particularly in the manufacturing and automotive sectors. The rise of software-as-a-service (SaaS) solutions has created new opportunities for market expansion, especially in emerging economies. The region's focus on industrial modernization and automation has spurred the demand for simulation software across various applications. The growing emphasis on cost-effective manufacturing solutions and process optimization has made simulation software an attractive option for businesses in the region. Additionally, the increasing presence of global simulation software providers and their partnerships with local enterprises has enhanced market accessibility and technical support infrastructure. The region's ongoing digital transformation initiatives and growing investment in technological infrastructure continue to create favorable conditions for market growth.

Simulation Software Market in Middle East & Africa

The Middle East & Africa region represents an emerging market for simulation software, with significant growth potential driven by increasing industrial automation and digital transformation initiatives. The region's market is characterized by growing adoption across various sectors, particularly in the oil and gas, manufacturing, and construction industries. Countries in the Middle East are actively implementing innovative technologies as part of their economic diversification strategies, creating new opportunities for simulation software providers. The region's focus on smart city initiatives and infrastructure development has increased the demand for simulation tools in urban planning and construction projects. Educational institutions and research centers are increasingly incorporating simulation software into their programs, fostering a new generation of skilled professionals. The growing emphasis on local manufacturing capabilities and industrial development has created a strong demand for simulation solutions that can optimize production processes and reduce operational costs. Furthermore, the region's investment in renewable energy projects has opened new avenues for simulation software applications in energy system design and optimization.

Get Analysis on Important Geographic Markets

Download PDF

Simulation Software Industry Overview

Top Companies in Simulation Software Market

The simulation software market features established players like ANSYS, Autodesk, Siemens, PTC, and Dassault Systèmes, leading innovation through continuous R&D investments and product development. These companies are focusing on expanding their portfolios through cloud-based solutions, real-time simulation tools capabilities, and integration of advanced technologies like artificial intelligence and machine learning. Strategic partnerships with technology providers and academic institutions have become crucial for developing next-generation simulation tools. Companies are emphasizing the development of industry-specific solutions while simultaneously working on improving interoperability between different simulation platforms. The market leaders are also actively pursuing geographical expansion through both direct presence and partner networks, while maintaining a strong focus on customer support and training services.

Market Consolidation Drives Competitive Dynamics Forward

The simulation software market exhibits a mix of large multinational technology conglomerates and specialized simulation software providers competing across various industry verticals. The larger players leverage their extensive resources, established customer relationships, and comprehensive product portfolios to maintain market leadership, while specialized providers focus on developing niche solutions for specific industries or applications. The market is experiencing significant consolidation through mergers and acquisitions, as larger companies seek to acquire innovative technologies and expand their capabilities in emerging areas like digital twin software and cloud-based simulation.

The competitive landscape is characterized by intense rivalry among established players and emerging contenders, with companies differentiating themselves through technological innovation, industry expertise, and service quality. Market participants are increasingly focusing on developing end-to-end solutions that combine simulation capabilities with other digital tools like PLM, CAD, and IoT platforms. Strategic partnerships and collaborations have become essential for addressing complex customer requirements and expanding market reach, particularly in emerging economies where local knowledge and presence are crucial for success.

Innovation and Adaptability Drive Future Success

Success in the simulation software market increasingly depends on vendors' ability to provide scalable, flexible solutions that can adapt to evolving customer needs and technological advancements. Companies must focus on developing user-friendly interfaces while maintaining advanced capabilities to address both expert and novice users' requirements. The integration of cloud computing, artificial intelligence, and real-time simulation capabilities has become crucial for maintaining competitive advantage. Vendors need to establish strong partnerships with industry leaders, technology providers, and academic institutions to enhance their innovation capabilities and market presence.

Market players must address the growing demand for industry-specific solutions while maintaining the flexibility to serve diverse customer segments. The ability to provide comprehensive training, support services, and consulting expertise has become increasingly important for building long-term customer relationships. Companies need to carefully balance their investment in new technology development with maintaining competitive pricing structures, particularly as cloud-based solutions and new delivery models emerge. The market's future success factors also include the ability to address cybersecurity concerns, ensure regulatory compliance across different regions, and provide solutions that can integrate seamlessly with existing enterprise systems. The adoption of virtual prototyping and predictive simulation techniques is also anticipated to play a pivotal role in shaping the future landscape of the industry.

Simulation Software Market Leaders

-

Siemens AG

-

Rockwell Automation Inc.

-

Schneider Electric SE

-

Autodesk Inc.

-

Ansys Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Simulation Software Market News

- March 2023 - Simulations Plus, Inc., which offers modeling and simulation software for pharmaceutical development, revealed a partnership with the Institute of Medical Biology of the Polish Academy of Sciences to create novel compounds for RORγ/RORγT nuclear receptors using artificial intelligence in the ADMET Predictor software.

- January 2023 - Real-Time Innovations (RTI), the software framework organization for autonomous systems, reported its association with Ansys, a player in simulation software. This partnership accelerates developing, testing, and deploying high-performance and high-reliability distributed procedures by authorizing them to be simulated without their underlying hardware, which may have restricted availability or be cost-prohibitive.

Simulation Software Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of the COVID-19 on the Market

-

4.4 Market Drivers

- 4.4.1 Rising Demand from the Automotive Sector

- 4.4.2 The Growing Shift to Cloud-Based Simulation Solutions

- 4.5 Market Restraints

5. MARKET SEGMENTATION

-

5.1 Deployment Type

- 5.1.1 On-premise

- 5.1.2 Cloud

-

5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 IT and Telecommunication

- 5.2.3 Aerospace and Defense

- 5.2.4 Energy and Mining

- 5.2.5 Education and Research

- 5.2.6 Electrical and Electronics

- 5.2.7 Other End-user Industries

-

5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia

- 5.3.4 Australia and New Zealand

- 5.3.5 Latin America

- 5.3.6 Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles*

- 6.2.1 Altair Engineering Inc.

- 6.2.2 The MathWorks Inc.

- 6.2.3 Autodesk Inc.

- 6.2.4 Cybernet Systems Corp.

- 6.2.5 Bentley Systems Incorporated

- 6.2.6 PTC Inc.

- 6.2.7 CPFD Software LLC

- 6.2.8 Design Simulation Technologies Inc.

- 6.2.9 Synopsys Inc.

- 6.2.10 Siemens AG

- 6.2.11 Ansys Inc.

- 6.2.12 Dassault Systèmes SE

- 6.2.13 Simio LLC

- 6.2.14 Lanner Group Ltd

- 6.2.15 SIMUL8 Corporation

- 6.2.16 CONSELF Srl

- 6.2.17 SolidWorks Corporation

- 6.2.18 Rockwell Automation Inc.

- 6.2.19 The COMSOL Group

- 6.2.20 Schneider Electric SE

7. MARKET INVESTMENT ANALYSIS

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Simulation Software Industry Segmentation

Simulation is the imitation of the operation of a real-world process or system. The act of simulating something first requires a mathematical model to be developed. This replicated model represents the key characteristics of the physical process. The model basically represents the system itself, whereas the simulation software runs the operation of the system over time.

The simulation software market is segmented by deployment (on-premise, cloud), end-user industry (automotive, IT and telecommunication, aerospace and defense, energy and mining, education and research), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Deployment Type | On-premise |

| Cloud | |

| End-user Industry | Automotive |

| IT and Telecommunication | |

| Aerospace and Defense | |

| Energy and Mining | |

| Education and Research | |

| Electrical and Electronics | |

| Other End-user Industries | |

| Geography | North America |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Simulation Software Market Research FAQs

How big is the Simulation Software Market?

The Simulation Software Market size is expected to reach USD 13.58 billion in 2025 and grow at a CAGR of 12.06% to reach USD 24.00 billion by 2030.

What is the current Simulation Software Market size?

In 2025, the Simulation Software Market size is expected to reach USD 13.58 billion.

Who are the key players in Simulation Software Market?

Siemens AG, Rockwell Automation Inc., Schneider Electric SE, Autodesk Inc. and Ansys Inc. are the major companies operating in the Simulation Software Market.

Which is the fastest growing region in Simulation Software Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Simulation Software Market?

In 2025, the North America accounts for the largest market share in Simulation Software Market.

What years does this Simulation Software Market cover, and what was the market size in 2024?

In 2024, the Simulation Software Market size was estimated at USD 11.94 billion. The report covers the Simulation Software Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Simulation Software Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Simulation Software Market Research

Mordor Intelligence brings extensive expertise in analyzing the simulation software industry. We offer comprehensive insights into computational fluid dynamics, finite element analysis, and computer aided engineering solutions. Our research thoroughly examines various segments, including physics simulation, 3D simulation, and digital twin software applications. The report provides a detailed analysis of virtual engineering practices and process simulation methodologies. It also explores emerging trends in virtual testing and virtual prototyping, all available in an easy-to-download report PDF format.

Stakeholders across industries benefit from our in-depth coverage of engineering simulation technologies, manufacturing simulation applications, and industrial simulation solutions. The report delves into advanced applications in discrete event simulation, system simulation, and predictive simulation. We analyze developments in virtual simulation and digital simulation technologies. Our analysis encompasses scientific simulation methodologies, training simulation platforms, and CAE software implementations. This provides valuable insights for businesses leveraging modeling and simulation capabilities in their operations.