| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 1.01 Billion |

| Market Size (2030) | USD 3.05 Billion |

| CAGR (2025 - 2030) | 24.70 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

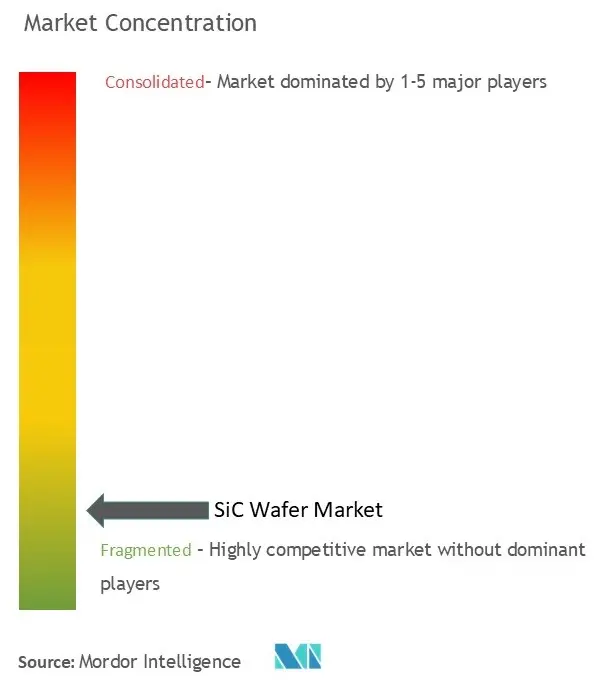

| Market Concentration | Low |

Major Players Wafer Market Major Players")

*Disclaimer: Major Players sorted in no particular order |

Wafer Market Size")

Silicon Carbide (SiC) Wafer Market Analysis

The Silicon Carbide Wafer Market size is estimated at USD 1.01 billion in 2025, and is expected to reach USD 3.05 billion by 2030, at a CAGR of 24.7% during the forecast period (2025-2030).

The silicon carbide wafer industry is experiencing significant transformation amid evolving geopolitical dynamics, particularly the US-China tech war, which has reshaped global supply chains and manufacturing strategies. This has led to increased regional manufacturing initiatives and technological sovereignty efforts across major economies. The semiconductor industry's structural changes have prompted companies to diversify their supply chains and establish new manufacturing facilities in different regions, creating a more distributed global production network. These developments have particularly impacted the SiC wafer market, as manufacturers seek to ensure stable supply chains and reduce dependencies on single geographic regions.

The advancement in semiconductor technology has positioned silicon carbide semiconductors as a superior alternative to traditional silicon semiconductors, with SiC devices capable of operating at temperatures up to 400°C compared to silicon's 175°C ceiling. This technological superiority has enabled the development of more compact, efficient, and powerful electronic devices across various applications. The material's exceptional thermal and electrical properties have made it particularly valuable in high-power and high-frequency applications, where traditional semiconductors face significant limitations.

The telecommunications sector's evolution, particularly the rollout of 5G infrastructure, has emerged as a significant market catalyst. According to 5G Americas, 5G connections are projected to reach 5.9 million by 2027, driving demand for high-performance RF power amplifiers that can operate efficiently in new high-frequency bands. This growth in telecommunications infrastructure has created substantial opportunities for silicon carbide wafer manufacturers, as these components are essential for developing advanced 5G base stations and communication equipment.

The renewable energy sector has become a major growth driver for SiC wafer applications, particularly in power electronics and energy conversion systems. India's ambitious target of achieving 500 GW of non-fossil fuel energy capacity by 2030, coupled with its current installed solar energy capacity of 72.31 GW as of November 2023, exemplifies the global push toward renewable energy adoption. SiC-based power electronics are playing a crucial role in this transition, offering higher efficiency and better performance in solar inverters, wind energy systems, and power distribution networks.

Silicon Carbide (SiC) Wafer Market Trends

RISING PENETRATION OF EV AND THE INCLINATION TOWARD HIGH-VOLTAGE 800V EV ARCHITECTURES PROPELLING THE DEMAND FOR SIC WAFERS

The automotive industry is witnessing a revolutionary shift toward electric vehicles (EVs), with major automakers increasingly adopting high-voltage 800V architectures to meet demands for faster charging times and extended driving ranges. This transition has created substantial demand for silicon carbide wafer, as they enable the development of more efficient and compact power electronic systems essential for EV operations. Notable automotive manufacturers, including Audi with its Q6 e-tron, Porsche Taycan, and Hyundai Ioniq 5, have already implemented 800V charging architectures, demonstrating the industry's commitment to this technology.

The adoption of SiC in electric vehicles extends beyond just power electronics, impacting multiple vehicle systems including traction inverters, DC-DC converters, and onboard chargers. Major automotive manufacturers are making significant investments in this technology, as evidenced by Ford's substantial investment in electric vehicle production facilities in Tennessee and Kentucky, focusing on battery parks and manufacturing capabilities. Additionally, General Motors has increased its EV and AV investments to USD 35 billion through 2025, representing a 75% increase from its initial commitment, further driving the demand for SiC wafers in the automotive sector.

Understand The Key Trends Shaping This Market

Download PDF

INCREASING DEMAND FOR SIC WAFERS IN POWER ELECTRONICS SWITCHES AND LED LIGHTING DEVICES DUE TO ITS HIGH THERMAL CONDUCTIVITY

The superior thermal conductivity of silicon carbide wafer has revolutionized power electronics and LED lighting applications, enabling the development of more efficient and compact devices. In power electronics, SiC's ability to operate at higher temperatures and voltages while maintaining excellent thermal management has made it invaluable for applications ranging from industrial motor drives to renewable energy systems. The material's wide bandgap semiconductor properties allow for faster switching speeds and reduced energy losses, resulting in smaller, more efficient power electronic devices.

The LED lighting industry has particularly benefited from SiC wafer technology, as the material's high thermal conductivity enables better heat dissipation in high-power LED applications. This characteristic is crucial for maintaining LED performance and longevity, especially in demanding applications such as automotive lighting and industrial illumination. The technology's adoption in power electronics has also expanded into data center applications, where efficiency and power density are critical factors. Companies like Wolfspeed have noted that data centers currently consume approximately 3% of all electricity in the United States, with projections indicating an increase to 15% over the next seven years, highlighting the growing importance of efficient power electronics in this sector.

Segment Analysis: By Wafer Size

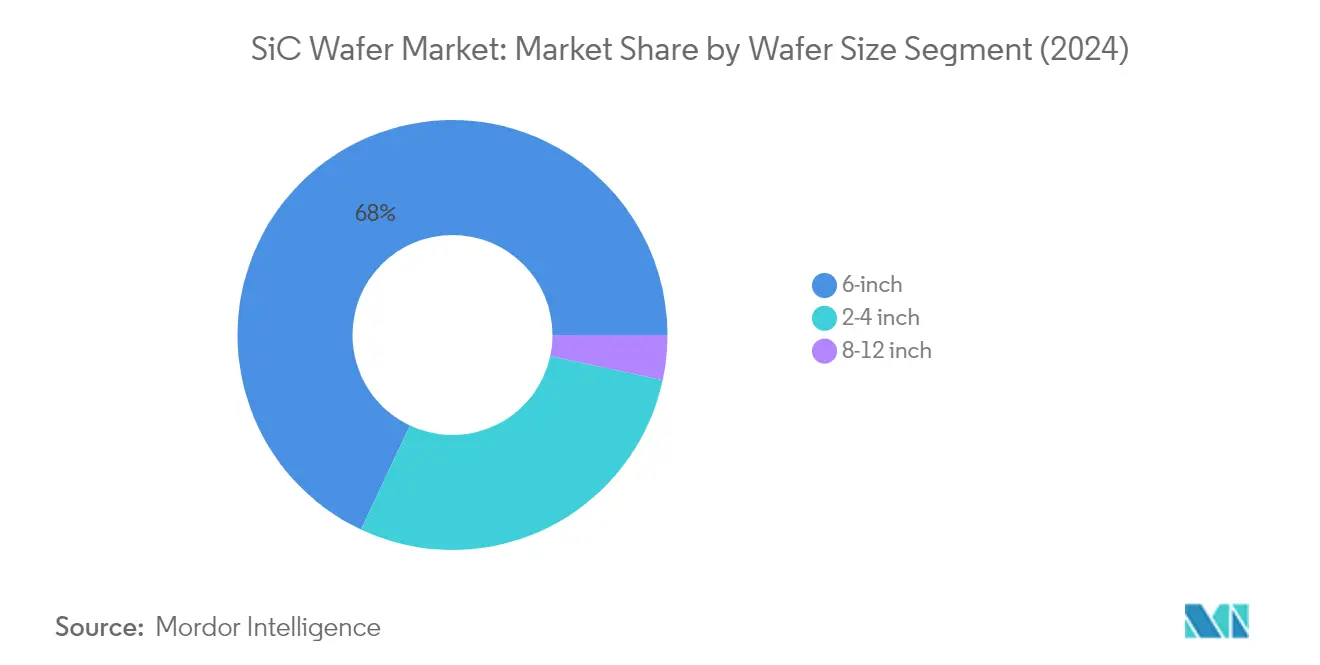

6-inch Segment in SiC Wafer Market

The 6-inch wafer segment continues to dominate the global SiC wafer market, holding approximately 68% market share in 2024. This significant market position is primarily driven by the emergence of 150mm/6-inch silicon carbide wafers as a critical component in enabling economies of scale from the manufacturing standpoint. The segment's dominance is further strengthened by the ability to utilize depreciated 150mm silicon production lines that can be converted to produce silicon carbide wafers as per desired specifications. The 6-inch technology has successfully surpassed the traditional 100mm technology, maintaining consistent shape and thickness parameters that enable seamless manufacturing process transfers. Major semiconductor wafer manufacturers have optimized their production processes around 6-inch wafers, particularly for diode manufacturing, due to their balanced cost-effectiveness and quality characteristics.

8-12 inch Segment in SiC Wafer Market

The 8-12 inch wafer segment is experiencing remarkable growth momentum, projected to expand at approximately 48% CAGR from 2024 to 2029. This exceptional growth trajectory is driven by the increasing demand for improved and enhanced SiC wafers from semiconductor wafer industries and electric vehicle manufacturers. The segment's rapid expansion is supported by companies migrating from smaller dice to larger dice per wafer configurations, capitalizing on overall cost benefits derived from higher production efficiency. The transition to larger wafer sizes is particularly crucial for high-power applications, with 300mm wafers capable of accommodating twice as many dice per wafer compared to 200mm alternatives. This shift is fundamentally transforming the industry's manufacturing capabilities and cost structures.

Remaining Segments in SiC Wafer Market by Size

The 2-4 inch segment continues to maintain its relevance in specific applications despite the industry's shift toward larger wafer sizes. These smaller wafers are particularly valuable in specialized applications where precision and specific technical requirements take precedence over production volume efficiency. While the segment faces challenges from the industry's transition to larger wafer sizes, it maintains its importance in research and development activities, specialized semiconductor devices, and specific high-precision applications. The manufacturing processes for these smaller wafers have been well-established, offering reliable performance characteristics that continue to serve certain niche market requirements.

Segment Analysis: By Application

Power Segment in SiC Wafer Market

The Power segment dominates the global SiC wafer market, commanding approximately 66% market share in 2024. This significant market position is driven by the extensive use of SiC wafers in power electronic switches, which are critical components carrying heavy currents in various applications. The segment's dominance is primarily attributed to the material's excellent thermal conductivity and low electrical resistance properties, enabling a reduction in the size and weight of power switches. The optimization of SiC production processes by companies has been crucial in meeting the strong market demand, particularly in applications such as electric vehicles, industrial markets, and mobile telecommunications. The segment's growth is further supported by the material's ability to handle higher power density and improved efficiency, making it particularly valuable in switching power supplies, inverters for solar and windmill energy generation, industrial motor drives, and smart-grid power switching applications.

Radio Frequency (RF) Segment in SiC Wafer Market

The Radio Frequency (RF) segment is projected to exhibit the highest growth rate of approximately 20% during the forecast period 2024-2029. This accelerated growth is driven by the increasing adoption of SiC devices in cellular base stations and radio-frequency operations, coupled with supportive government regulations promoting renewable energy resources. The segment's growth is further bolstered by the expanding applications in 5G and smartphone equipment, aerospace and defense, automotive, and other industries. The RF industry's requirements for direct wireless communication devices and the rising popularity of consumer electronics continue to fuel the growth of RF technology applications. The development of new technologies and innovations in RF applications, particularly in 5G wireless deployment, is creating substantial opportunities for SiC wafers in RF power amplifiers that can function efficiently in new high-frequency bands.

Remaining Segments in SiC Wafer Market by Application

The Other Applications segment encompasses various important applications including electronic power, photoelectric fields, and specialized applications in MEMS technology. This segment plays a crucial role in addressing emerging applications in adverse environments and specialized industrial needs. The segment's impact is particularly notable in the development of unique MEMS-based sensors for various applications, contributing to market diversification. The applications extend to photoelectric sensors widely used in automotive, healthcare, and food and beverage industries, demonstrating the versatility of SiC wafers across different industrial applications. The segment also supports GaN epitaxy devices, power devices, high-temperature devices, and optoelectronic devices, showcasing the broad spectrum of applications that SiC wafers serve beyond the primary power and RF segments.

Segment Analysis: By End-User Industry

Automotive & Electric Vehicles Segment in SiC Wafer Market

The Automotive & Electric Vehicles segment has emerged as the dominant force in the global SiC wafer market, commanding approximately 38% of the total market share in 2024. This segment's leadership position is primarily driven by the increasing adoption of SiC-based power semiconductors in electric vehicles, particularly in applications such as power modules, traction inverters, and onboard charging systems. The segment's growth is further bolstered by the automotive industry's rapid transition toward high-voltage 800V EV architectures, where SiC technology plays a crucial role in improving power density and efficiency. Additionally, the segment is experiencing the fastest growth trajectory in the market, as automotive manufacturers worldwide continue to expand their electric vehicle portfolios and invest in SiC-based power electronics solutions. The superior properties of SiC wafers, including higher thermal conductivity and breakdown voltage capabilities, make them particularly suitable for EV applications, enabling increased driving range and faster charging capabilities.

Remaining Segments in End-User Industry

The SiC wafer market encompasses several other significant segments including Telecom and Communications, Photovoltaic/Power Supply/Energy Storage, and Industrial applications. The Telecom and Communications segment is driven by the ongoing deployment of 5G infrastructure and the need for high-performance RF devices. The Photovoltaic/Power Supply/Energy Storage segment leverages SiC wafers capabilities in renewable energy applications, particularly in solar inverters and energy storage systems. The Industrial segment, which includes applications in UPS systems and motor drives, benefits from SiC wafers ability to operate at higher temperatures and voltages, enabling more efficient power conversion in industrial equipment. Each of these segments contributes uniquely to the market's growth, with varying requirements for wafer specifications and performance characteristics that continue to drive innovation in SiC wafer technology.

SiC Wafer Market Geography Segment Analysis

SiC Wafer Market in North America

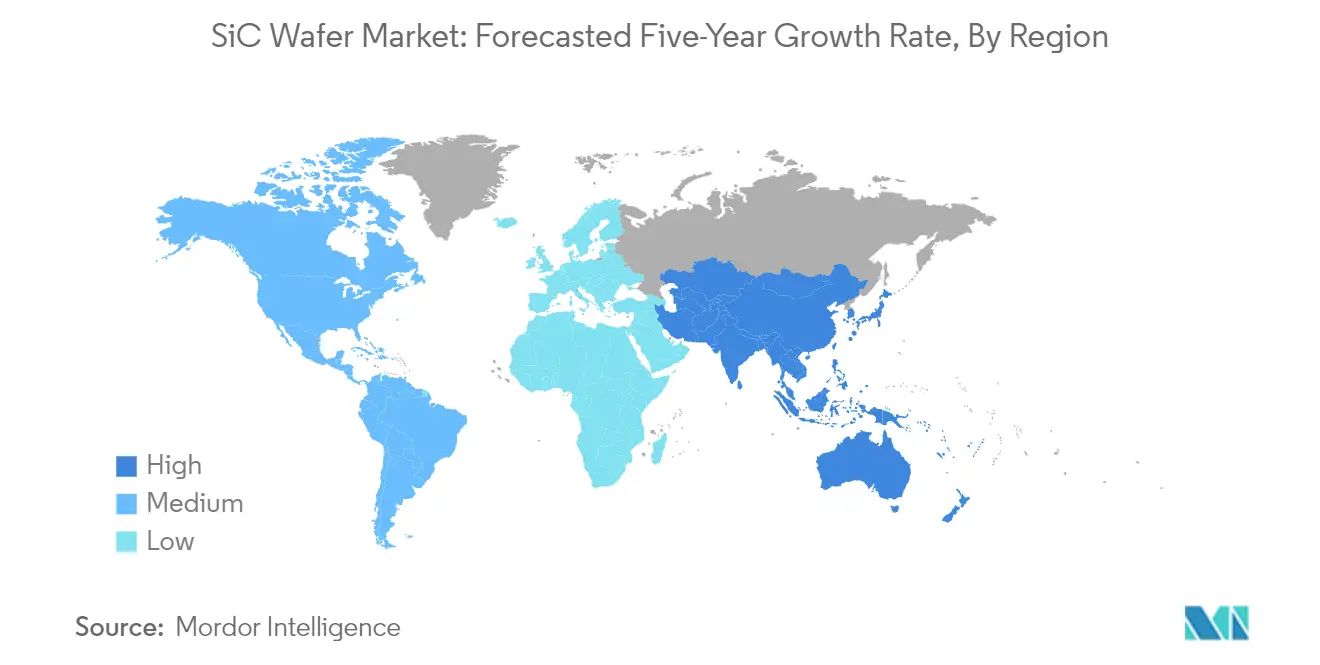

North America represents a dominant force in the global SiC wafer market, holding approximately 33% of the SiC market share in 2024. The region's leadership position is primarily driven by its early adoption of new technologies in semiconductor manufacturing, design, and research. The growth in the North American SiC wafer market strongly correlates with the development of various end-user industries, including automotive, energy, IT and telecommunications, military and aerospace, and consumer electronics. The region's semiconductor industry continues to demonstrate robust growth through substantial investments in research and development activities. Various organizations, including government entities, are actively engaged in advanced manufacturing research for silicon carbide wafer manufacturing. The presence of leading market players and their continuous focus on expanding production capabilities has further strengthened the region's position in the global market. The region's strong focus on electric vehicle adoption and the growing demand for high-power applications in various industries continue to drive market growth.

SiC Wafer Market in Europe

Europe has established itself as a crucial hub in the global SiC wafer market, demonstrating a steady growth rate of approximately 17% from 2019 to 2024. The region houses some of the most vital tech hubs globally and serves as a significant driver and adopter of modern technology. The European market's growth is primarily fueled by the increasing penetration of advanced technologies and the rising adoption of semiconductors across various industries. The region's automotive sector plays a pivotal role in market development, with numerous vehicle assembly and production plants operating across multiple countries. Being home to some of the largest semiconductor manufacturing companies globally, Germany leads the regional market with significant investments in silicon carbide wafer production. The region's strong focus on electric vehicle manufacturing and renewable energy applications continues to drive the demand for SiC wafers. The presence of robust research and development facilities and technological expertise further strengthens Europe's position in the global market.

SiC Wafer Market in Asia-Pacific

The Asia-Pacific region stands as a powerhouse in the global SiC wafer market, with projections indicating a robust growth rate of approximately 21% from 2024 to 2029. The region's dominance is supported by strong government policies and the presence of major semiconductor manufacturing countries like Taiwan, China, Japan, and South Korea. The region's semiconductor ecosystem is further complemented by contributions from emerging markets such as Thailand, Vietnam, Singapore, and Malaysia. The market growth is driven by the rapid expansion of electric vehicle manufacturing, increasing adoption of 5G technology, and growing investments in renewable energy infrastructure. The presence of major semiconductor fabrication facilities and the continuous focus on technological advancement has positioned Asia-Pacific as a critical hub for SiC wafer production. The region's strong supply chain network, coupled with increasing investments in research and development activities, continues to attract global players looking to expand their manufacturing capabilities.

SiC Wafer Market in Rest of the World

The Rest of the World region, encompassing Latin America, the Middle East, and Africa, represents an emerging market in the global compound semiconductor market. The region is witnessing increasing demand for compound semiconductors, particularly driven by the growing automotive sector and renewable energy initiatives. Latin America, specifically Mexico and Brazil, shows promising growth potential due to the expanding electric vehicle manufacturing sector and increasing semiconductor applications. The Middle East and Africa region is gradually developing its semiconductor capabilities through various government initiatives and investments in technology parks. The region's focus on renewable energy projects and the growing adoption of electric vehicles create significant opportunities for SiC wafer applications. The increasing initiatives taken to boost the overall semiconductor industry in these regions, coupled with rising investments in manufacturing capabilities, create a positive outlook for market growth.

Get Analysis on Important Geographic Markets

Download PDF

Silicon Carbide (SiC) Wafer Market Overview

Top Companies in SiC Wafer Market

The SiC wafer market is characterized by intense innovation and strategic developments among key players, including Wolfspeed, II-VI Incorporated, STMicroelectronics, Showa Denko, and SK Siltron. Companies are heavily investing in research and development to enhance existing product offerings and develop next-generation technologies, particularly focusing on larger diameter wafers and improved manufacturing processes. Operational agility is demonstrated through the establishment of new fabrication facilities and production capacity expansions to meet growing demand, especially in the automotive and power electronics sectors. Strategic partnerships and long-term supply agreements with major semiconductor manufacturers have become increasingly common to secure market position and ensure stable supply chains. Geographic expansion is primarily focused on Asia-Pacific and North America, with companies establishing new manufacturing facilities and research centers to capitalize on regional growth opportunities and strengthen their global presence.

Market Dominated by Global Technology Conglomerates

The competitive landscape is characterized by a mix of established global technology conglomerates and specialized silicon carbide wafer manufacturers, with market leadership concentrated among a few key players. Major companies leverage their extensive research capabilities, established distribution networks, and strong financial positions to maintain market dominance, while regional players focus on serving specific geographic markets or specialized applications. The market structure shows moderate consolidation, with larger players continuously expanding their market presence through strategic acquisitions and partnerships.

The industry has witnessed significant merger and acquisition activity, particularly focused on securing raw material supply chains and expanding technological capabilities. Companies are actively pursuing vertical integration strategies, with many major players acquiring smaller specialized firms to enhance their manufacturing capabilities and secure critical supply chain components. This consolidation trend is particularly evident in regions with strong semiconductor manufacturing bases, such as North America, Europe, and Asia-Pacific, where companies are seeking to establish complete end-to-end solutions for SiC wafer manufacturing and processing.

Innovation and Supply Chain Control Drive Success

Success in the SiC wafer market increasingly depends on technological innovation, manufacturing scale, and supply chain control. Incumbent players are focusing on expanding their production capacities, investing in advanced manufacturing technologies, and developing larger diameter wafers to maintain their competitive advantage. Companies are also strengthening their relationships with end-users through long-term supply agreements and collaborative development projects, particularly in the automotive and industrial sectors where demand for SiC-based devices is growing rapidly. The ability to provide consistent quality, manage production costs, and maintain reliable supply chains has become crucial for maintaining market position.

For contenders looking to gain SiC market share, success factors include developing specialized expertise in specific applications or regions, forming strategic partnerships with established players, and investing in innovative manufacturing processes. The market presents moderate substitution risk from competing technologies, though SiC wafers maintain significant advantages in high-power applications. The regulatory environment, particularly regarding environmental standards and manufacturing processes, plays an increasingly important role in shaping competitive strategies. Companies must also consider the high concentration of end-users in specific industries, such as automotive and power electronics, when developing their market approach and customer relationship strategies. Notably, Wolfspeed market share continues to be a focal point for industry analysis, given its significant role in the semiconductor substrate sector.

Silicon Carbide (SiC) Wafer Market Leaders

-

Wolfspeed Inc.

-

Coherent Corp. (II-VI Incorporated)

-

Xiamen Powerway Advanced Material Co.

-

STMicroelectronics (Norstel AB)

-

Resonac Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Silicon Carbide (SiC) Wafer Market News

- July 2024 - SiCrystal GmbH, a subsidiary of the ROHM Group based in Erlangen, Germany, announced its plans to expand its production capacity for monocrystalline silicon carbide (SiC) wafers. The company is constructing a new 6000 m2 facility directly across from its current location in northeast Nuremberg. Collaborating with the general contractor Systeambau from Hilpoltstein, the construction is slated for completion by early 2026.

- February 2024 - SK Siltron CSS obtained a conditional commitment for a loan of up to USD 544 million from the US Department of Energy (DOE). This loan, part of the Advanced Technology Vehicles Manufacturing (ATVM) Loan Program and overseen by the DOE’s Loan Programs Office (LPO), aims to bolster American production of high-quality SiC wafers. These wafers are essential for the power electronics in electric vehicles (EVs). The funding is expected to enhance the manufacturing capacity at SK Siltron CSS’ facility located in Bay City, Michigan.

Silicon Carbide (SiC) Wafer Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Insights

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Rising Penetration of EV and the Inclination Toward High-voltage 800V EV Architectures Propelling the Demand for SIC Wafers

- 5.1.2 Increasing Demand for SiC Wafers in Power Electronic Switches and LED Lighting Devices due to its High Thermal Conductivity

-

5.2 Market Restraints

- 5.2.1 Limiting Constraints Such as Scalability, Heat Dissipation, and Packaging-related Pressure on the Die and Substrate Supply

6. MARKET SEGMENTATION

-

6.1 By Wafer Size

- 6.1.1 2-, 3-, and 4-inch

- 6.1.2 6-inch

- 6.1.3 8- and 12-inch

-

6.2 By Application

- 6.2.1 Power

- 6.2.2 Radio Frequency (RF)

- 6.2.3 Other Applications

-

6.3 By End-user Industry

- 6.3.1 Telecom and Communications

- 6.3.2 Automotive and Electric Vehicles (EVs)

- 6.3.3 Photovoltaic/Power Supply/Energy Storage

- 6.3.4 Industrial (UPS and Motor Drives, etc.)

- 6.3.5 Other End-user Industries

-

6.4 By Geography***

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Wolfspeed Inc.

- 7.1.2 Coherent Corp. (II-VI Incorporated)

- 7.1.3 Xiamen Powerway Advanced Material Co.

- 7.1.4 STMicroelectronics (Norstel AB)

- 7.1.5 Resonac Holdings Corporation

- 7.1.6 Atecom Technology Co. Ltd

- 7.1.7 SK Siltron Co. Ltd

- 7.1.8 SiCrystal GmbH

- 7.1.9 TankeBlue Co. Ltd

- 7.1.10 Semiconductor Wafer Inc.

8. MARKET SHARE ANALYSIS

9. INVESTMENT ANALYSIS

10. FUTURE OF THE MARKET

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific' and Latin America and Middle East and Africa will be considered together as 'Rest of the World'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Silicon Carbide (SiC) Wafer Market Industry Segmentation

SiC is a silicon-carbon semiconductor compound that belongs to the wide-bandgap class of materials. The semiconductor's strong physical bond provides excellent mechanical, chemical, and thermal stability. The wafering process involves converting a solid SiC puck into an epi- or device-ready prime wafer.

The SiC wafer market is segmented by wafer size (2-, 3-, and 4-inch, 6-inch, and 8- and 12-inch), by application (power, radio frequency (RF) and other applications), by end-user industry (telecom and communications, automotive and electric vehicles (EVs), photovoltaic/power supply/energy storage, industrial [UPS and motor drives], other end-user industries), and by geography (North America, Europe, Asia-Pacific, and Rest of the World). The market sizes and forecasts for value (USD) for all the segments mentioned above have been provided.

| By Wafer Size | 2-, 3-, and 4-inch |

| 6-inch | |

| 8- and 12-inch | |

| By Application | Power |

| Radio Frequency (RF) | |

| Other Applications | |

| By End-user Industry | Telecom and Communications |

| Automotive and Electric Vehicles (EVs) | |

| Photovoltaic/Power Supply/Energy Storage | |

| Industrial (UPS and Motor Drives, etc.) | |

| Other End-user Industries | |

| By Geography*** | North America |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Silicon Carbide (SiC) Wafer Market Research FAQs

How big is the SiC Wafer Market?

The SiC Wafer Market size is expected to reach USD 1.01 billion in 2025 and grow at a CAGR of 24.70% to reach USD 3.05 billion by 2030.

What is the current SiC Wafer Market size?

In 2025, the SiC Wafer Market size is expected to reach USD 1.01 billion.

Who are the key players in SiC Wafer Market?

Wolfspeed Inc., Coherent Corp. (II-VI Incorporated), Xiamen Powerway Advanced Material Co., STMicroelectronics (Norstel AB) and Resonac Holdings Corporation are the major companies operating in the SiC Wafer Market.

Which is the fastest growing region in SiC Wafer Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in SiC Wafer Market?

In 2025, the Asia Pacific accounts for the largest market share in SiC Wafer Market.

What years does this SiC Wafer Market cover, and what was the market size in 2024?

In 2024, the SiC Wafer Market size was estimated at USD 0.76 billion. The report covers the SiC Wafer Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the SiC Wafer Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Silicon Carbide (SiC) Wafer Market Research

Mordor Intelligence provides comprehensive industry analysis and market insights for the silicon carbide wafer market through detailed market data, industry statistics, and future forecasts. Our research covers the entire spectrum of the semiconductor wafer ecosystem, including power semiconductor applications, wide bandgap semiconductor technologies, and emerging trends in silicon carbide semiconductor development. The report pdf delivers actionable insights on market segmentation, competitive landscape analysis, and growth projections, helping stakeholders make informed decisions in this rapidly evolving industry.

Our consulting expertise extends beyond traditional market research to provide strategic support in technology scouting, particularly for emerging compound semiconductor applications and silicon carbide device innovations. We assist clients with R&D and patent analysis support, helping them navigate the complex landscape of silicon carbide material development and manufacturing processes. Our team specializes in competition assessment, product pricing strategies, and new product launch tracking, particularly valuable for companies involved in sic wafer manufacturing and development of wide bandgap material solutions. Through comprehensive B2B surveys and advanced data analytics, we help clients identify market opportunities, assess technological feasibility, and develop robust go-to-market strategies in the evolving semiconductor substrate industry.