Market Trends of Shipbuilding Industry

Increasing Trade and Naval Activities Between Countries to Drive the Market

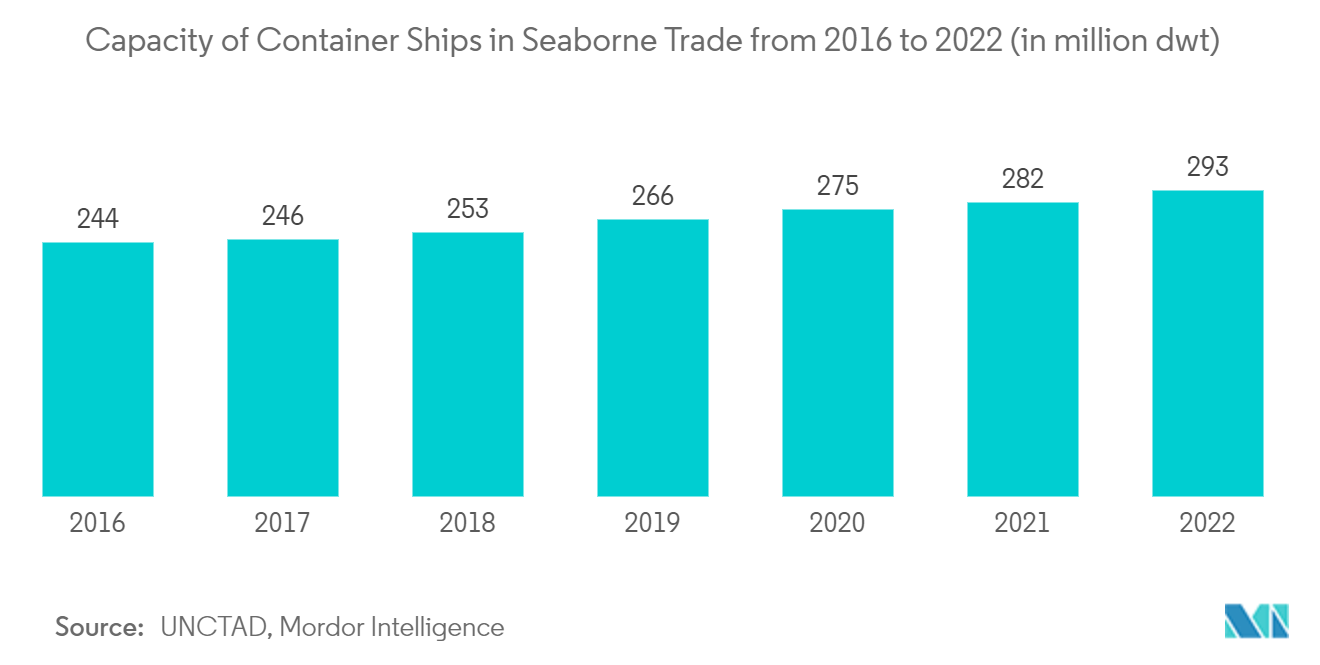

Trade growth is one of the hallmarks of the global economy in recent decades, and maritime transport is the backbone of global trade. Maritime trades primarily influence the shipbuilding market. With the extended supply chains and opened new markets, maritime transport is a catalyst for the economic development of nations worldwide. Almost 90% of global freight is seaborne. As a result, countries heavily rely on ships, which further accelerates the shipbuilding market.

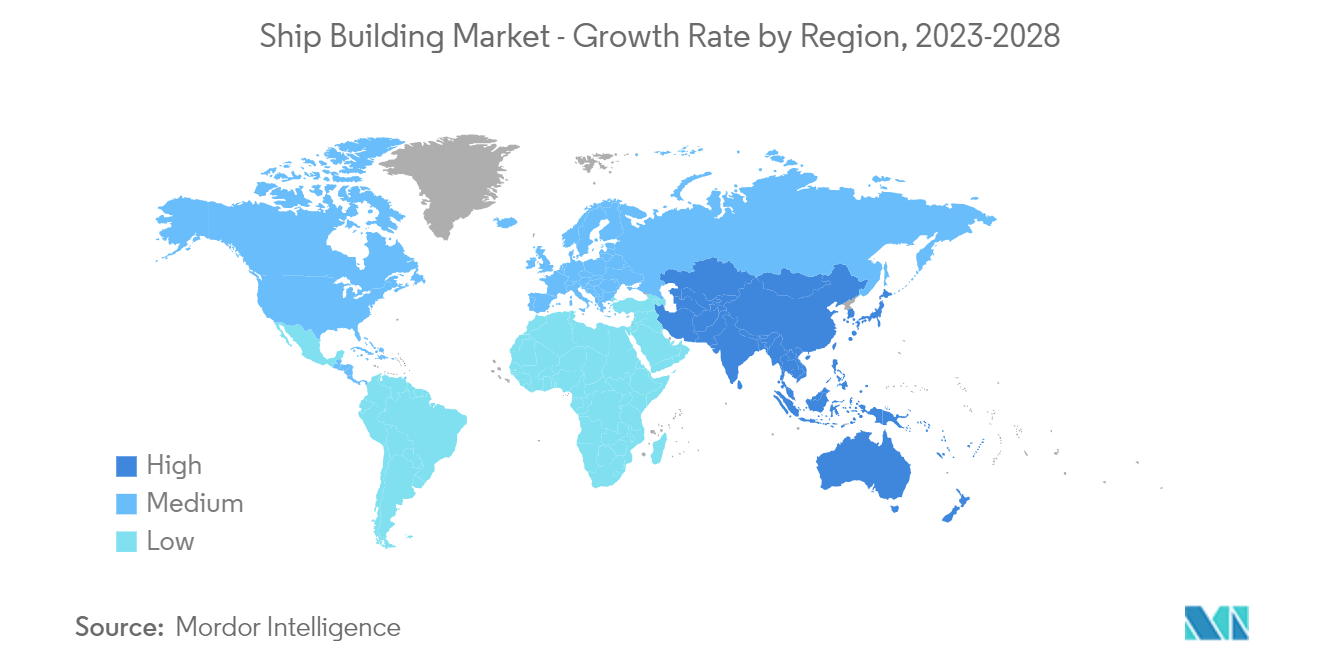

China, Japan, and South Korea represented approximately 85% of the shipbuilding activity. China, the Republic of Korea, and Japan continue to dominate maritime ship supply, accounting for 94% of the market in 2022. Shipbuilding increased by 15.5% in China and 8.3% in the Republic of Korea over the past year but declined by 16.4% in Japan. In June 2022, the Republic of Korea ordered 70% of the alternative fuel-capable ships, China ordered 26%, Europe ordered 58%, and Japan ordered 17%. South Korea accounted for 64% of gas carriers and 42% of oil tankers, and Japan accounted for 45% of chemical tankers. Cargos are the most preferred marine vessels used for trading activities.

There is an increase in demand for maritime transport over the years, which caused a subsequent rise in the number of imports and exports across the world. With globalization taking root in the heart of many economies, there are growing possibilities of internationally trading goods, providing a superior range of available products at different price points.

The top three ship-owning countries in terms of both dead-weight tonnage and commercial value as of 1 January 2022 included two Asian countries, namely China and Japan. China had the second-highest increase in tonnage (13%) among the top 25 ship-owning countries in the 12 months to 1 January 2022.

The Canadian government is introducing contracts for ships for the navy, which may generate the demand for defense ships in the country. To support the government's plans to build a large vessel fleet, the government signed a long-term strategic agreement with two Canadian shipyards, namely, Irving Shipbuilding Inc. (Halifax) and Seaspan's Vancouver Shipyards Co. Ltd (Vancouver), for the construction of combat and non-combat naval vessels for the Royal Canadian Navy and non-combat vessels for the Canadian Coast Guard.

In this regard, in January 2023, Irving Shipbuilding and the federal government agreed to a USD 1.6 billion contract to build two additional Arctic and offshore patrol ships for the Canadian Coast Guard.

Such instances are aiding the growth of the shipbuilding industry.

Asia-Pacific is Expected to Dominate the Market

The shipbuilding sector is one of the major contributors to the GDP of the countries in the manufacturing sector. India currently includes 28 shipyards, six of which are run by the Central Public Sector, two by state governments, and 20 by private companies. The Federation of Indian Export Organizations (FIEO) is also advocating for shipbuilding industry reforms.

China, Japan, and South Korea represented approximately 85% of the shipbuilding activity. China, the Republic of Korea, and Japan continue to dominate maritime ship supply, accounting for 94% of the market in 2022. In June 2022, the Republic of Korea ordered 70% of the alternative fuel-capable ships, China ordered 26%, Europe ordered 58%, and Japan ordered 17%. South Korea accounted for 64% of gas carriers and 42% of oil tankers, and Japan accounted for 45% of chemical tankers. Cargos are the most preferred marine vessels used for trading activities.

The shipbuilding industry in India holds the potential to strengthen the mission of an Atmanirbhar Bharat. It is due to its extensive direct and indirect links with most other leading industries such as steel, aluminum, electrical machinery and equipment, and so on, as well as its reliance on infrastructure and services sectors of the economy. The total traffic handled at JNPA in India during August 2023 is 7.34 million tonnes, which is 14.75% higher than 6.39 million tonnes in August 2022. August's traffic includes 6.64 million tonnes of container traffic and 0.69 million tonnes of bulk cargo as against 5.81 million tonnes of container traffic and 0.59 million tonnes of bulk traffic in the corresponding month of 2022.

In terms of commercial value, the ranking of fleet ownership and registration is more volatile than in terms of tonnage. China increased its share the most by 1.1% points, followed by Switzerland, Hong Kong, China, and the Republic of Korea, all of which contain a higher proportion of container ships in their fleets.

The Ministry of Industry and Trade in Vietnam proposed several measures aimed at easing supply chain issues along intra-Asian routes and reducing the burden on traders. These included tax breaks to encourage foreign investment in new ships and private-sector investment in critical infrastructure upgrades, as well as fleet renewal and the development of a coastal fleet management program.

Further, there are various developments in the country concerning the development of warships in the country. For instance,

- In May 2023, Mitsubishi Shipbuilding, a part of Mitsubishi Heavy Industries (MHI) Group and Nihon Shipyard Co., Ltd., a Tokyo-based joint venture for ship design and sales between Imabari Shipbuilding Co., Ltd., and Japan Marine United Corporation, started joint study for the development of an ocean-going liquified CO2 (LCO2) carrier. Nihon Shipyard is pursuing this project to complete the construction of the vessel from 2027 onwards.

Thus, the factors above are responsible for the growth of the Shipbuilding market in the region.