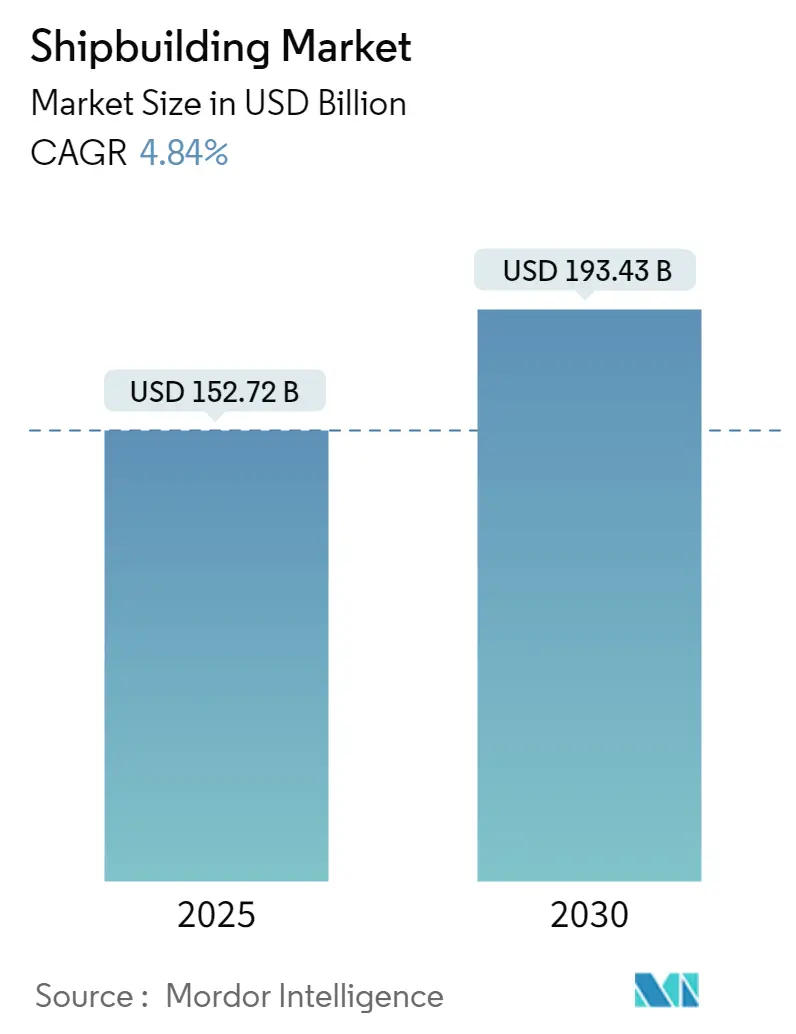

Shipbuilding Market Size

Market Overview

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 152.72 Billion |

| Market Size (2030) | USD 193.43 Billion |

| Growth Rate (2025 - 2030) | 4.84% CAGR |

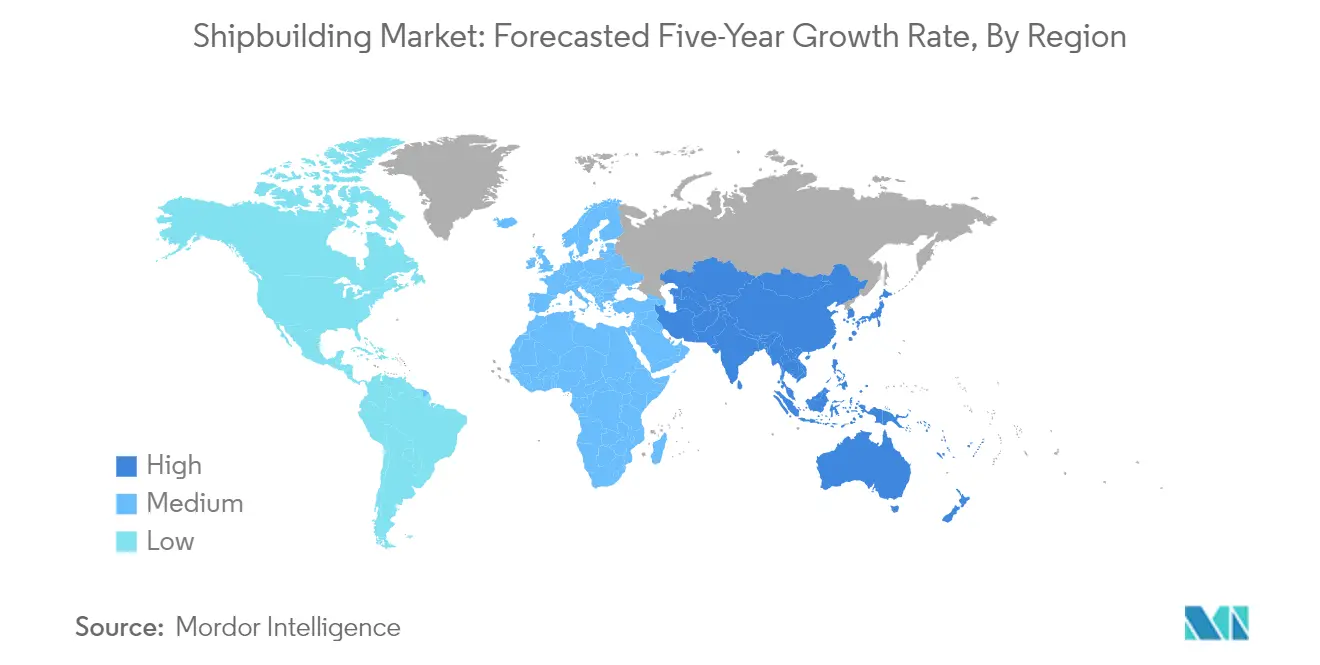

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Shipbuilding Market Analysis

The Shipbuilding Market size is estimated at USD 152.72 billion in 2025, and is expected to reach USD 193.43 billion by 2030, at a CAGR of 4.84% during the forecast period (2025-2030).

The global shipbuilding industry continues to undergo significant transformation driven by technological advancement and sustainability imperatives. The integration of robotics and automated systems in ship manufacturing industry processes has become increasingly prevalent, with major shipyards implementing smart manufacturing solutions to enhance efficiency and precision. This technological revolution extends to the adoption of 3D printing technologies, also known as additive manufacturing, which is revolutionizing the production of complex ship components and reducing manufacturing timeframes. Leading shipbuilders are forming strategic partnerships with technology providers to leverage these advanced manufacturing capabilities, marking a fundamental shift in traditional shipbuilding sector practices.

The industry landscape is characterized by strong regional concentration, particularly in East Asia, which maintains its position as the global shipbuilding hub. China has emerged as the dominant force in the sector, securing more than half of all global shipbuilding orders in 2022, while Japan and South Korea continue to maintain significant market presence through their technological expertise and specialized vessel construction capabilities. This regional consolidation extends to ship recycling activities, with Bangladesh, India, and Pakistan collectively accounting for approximately 90% of global ship scrapping operations, highlighting the industry's geographical specialization.

Environmental sustainability has become a cornerstone of modern shipbuilding trends, driving innovation in vessel design and construction methodologies. Shipyards are increasingly focusing on developing eco-friendly vessels equipped with alternative propulsion systems and energy-efficient technologies. The industry is witnessing a surge in orders for vessels powered by liquefied natural gas (LNG) and other clean fuels, as shipping companies aim to comply with stringent environmental regulations and reduce their carbon footprint. This shift towards sustainable shipbuilding is accompanied by investments in research and development of new materials and construction techniques that minimize environmental impact.

The digitalization of shipbuilding processes represents another pivotal trend shaping the industry's future. Advanced digital technologies, including artificial intelligence and digital twin solutions, are being integrated into design, construction, and testing phases. These digital tools enable more precise planning, reduce construction errors, and facilitate better collaboration between different stakeholders in the shipbuilding process. The industry is also seeing increased adoption of smart sensors and Internet of Things (IoT) technologies in newly built vessels, enhancing operational efficiency and enabling predictive maintenance capabilities. This digital transformation is fundamentally changing how ships are designed, built, and maintained, setting new standards for the industry.

Shipbuilding Market Trends

Increasing Containers and Dry Bulk Trade

Maritime transport continues to be the backbone of global trade, with approximately 90% of global freight being seaborne. This overwhelming dependence on maritime shipping has created a sustained demand for new vessels across various categories. The extended supply chains and opening of new markets have positioned maritime transport as a crucial catalyst for economic development worldwide, driving the need for modern and efficient ships to handle increasing cargo volumes.

The growing possibilities of international trade have led to significant developments in maritime infrastructure and vessel capabilities. This is evidenced by the increasing sophistication of cargo vessels and the rising port traffic volumes. For instance, the Jawaharlal Nehru Port Authority (JNPA) in India reported handling 7.34 million tonnes of traffic in August 2023, marking a substantial 14.75% increase compared to the previous year, with container traffic accounting for 6.64 million tonnes of the total volume. Such significant increases in port traffic volumes directly translate to higher demand for new vessels and shipbuilding activities.

Naval Fleet Modernization and Defense Contracts

The global focus on maritime security and defense capabilities has led to substantial investments in naval fleet modernization programs. This trend is exemplified by recent major defense contracts, such as the January 2023 agreement between Irving Shipbuilding and the Canadian federal government for a USD 1.6 billion contract to construct two additional Arctic and offshore patrol ships for the Canadian Coast Guard. These types of strategic investments in naval capabilities are driving significant growth in the military vessel segment of the shipbuilding market forecast.

The emphasis on developing advanced military vessels has also spurred technological innovations in shipbuilding. Countries are increasingly focusing on building specialized vessels with enhanced capabilities, leading to the development of more sophisticated shipbuilding techniques and technologies. This is evidenced by the strategic agreements between governments and shipyards, such as the long-term partnership between the Canadian government and shipyards like Irving Shipbuilding Inc. and Seaspan's Vancouver Shipyards Co. Ltd for the construction of both combat and non-combat naval vessels.

Environmental Regulations and Green Technology Integration

The shipbuilding industry is experiencing a significant shift toward environmental sustainability, driven by stringent regulations and increasing demand for eco-friendly vessels. This trend is reflected in the substantial orders for alternative fuel-capable ships, with significant developments in 2022 showing the Republic of Korea securing 70% of such orders, followed by China at 26%, and Japan at 17%. These statistics demonstrate the industry's rapid transition toward more sustainable shipbuilding trends and technologies.

Recent technological innovations in eco-friendly shipbuilding are reshaping the industry's future. A prime example is the May 2023 joint initiative between Mitsubishi Shipbuilding and Nihon Shipyard Co., Ltd. to develop an ocean-going liquified CO2 carrier, with construction planned from 2027 onwards. This type of innovative project represents the industry's commitment to developing new vessel types that support environmental sustainability while creating new market opportunities for shipbuilders.

Infrastructure Development and Manufacturing Capabilities

The global shipbuilding industry is witnessing substantial investments in infrastructure development and manufacturing capabilities enhancement. This is particularly evident in emerging markets where governments are implementing supportive policies and initiatives. For instance, Vietnam's Ministry of Industry and Trade has proposed comprehensive measures including tax breaks to encourage foreign investment in new ships and private-sector investment in critical infrastructure upgrades, alongside the development of a coastal fleet management program.

The focus on developing domestic shipbuilding capabilities has led to significant improvements in manufacturing infrastructure. India's strategic approach exemplifies this trend, with the country currently operating 28 shipyards, including six under Central Public Sector, two under state governments, and 20 under private companies. This infrastructure development is complemented by initiatives like the Federation of Indian Export Organizations' (FIEO) advocacy for industry reforms, demonstrating the growing emphasis on enhancing domestic shipbuilding capabilities and infrastructure, which is crucial for the shipbuilding market analysis.

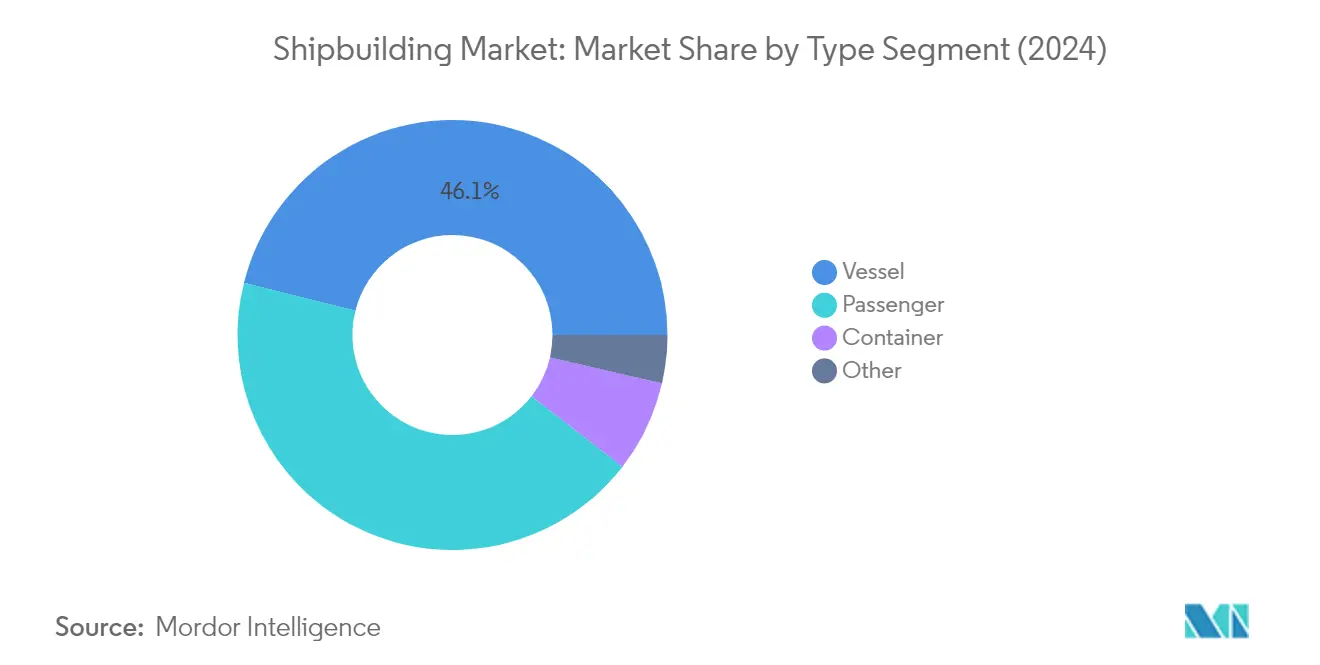

Segment Analysis: By Type

Vessel Segment in Global Shipbuilding Market

The vessel segment dominates the global shipyard market, commanding approximately 46% market share in 2024, while also demonstrating the strongest growth trajectory with a projected growth rate of around 5% during 2024-2029. This segment encompasses bulk carriers, general cargo vessels, and livestock vessels, with bulk carriers recording the highest level of ship deliveries. The segment's prominence is driven by the increasing demand for dry bulk market transportation, particularly for commodities like food grains, ores, coal, and cement. The adaptation of these vessels to handle diverse cargo types without specific packaging requirements has made them particularly attractive to major economies. Additionally, the growing focus on environmental sustainability has led to increased investments in eco-friendly vessel designs and propulsion systems, further strengthening this segment's market position.

Container Segment in Global Shipbuilding Market

The container segment in the shipyard industry has emerged as a significant growth area, driven by the expanding global trade and logistics sectors. The segment's growth is supported by increasing investments in port infrastructure development and the rising demand for larger container vessels to achieve economies of scale. Modern container ships are being designed with advanced technologies for improved fuel efficiency and reduced environmental impact, aligning with global sustainability goals. The development of smart container vessels with automated systems and digital capabilities is also contributing to the segment's evolution. Furthermore, the expansion of e-commerce and cross-border trade has created sustained demand for container ships, particularly in major maritime routes connecting Asia with Europe and North America.

Remaining Segments in Shipbuilding Market by Type

The passenger and other vessel segments complete the shipbuilding market landscape, each serving distinct maritime needs. The passenger segment includes cruise ships, ferries, and other passenger vessels, with a growing emphasis on luxury cruise liners and electric-powered passenger ferries. This segment has seen significant technological advancement in terms of comfort, safety features, and environmental compliance. The other vessel types category encompasses specialized vessels such as research vessels, fishing vessels, and offshore support vessels, each playing crucial roles in their respective industries. These segments are witnessing increased adoption of advanced propulsion systems and digital technologies to enhance operational efficiency and meet stringent environmental regulations.

Segment Analysis: By End User

Transport Companies Segment in Shipbuilding Market

The transport companies segment dominates the global shipbuilding market segmentation, accounting for approximately 85% of the market share in 2024. This significant market share is primarily driven by the increasing demand from the freight and logistics sector. The segment's growth is supported by the rising global commercial fleet expansion and the increasing carrying capacity of vessels. Transport companies are increasingly focusing on building specialized vessels like containers, gas carriers, and chemical tankers to meet diverse shipping requirements. The segment is also witnessing a transformation with the introduction of newer regulations mandating the creation of sulfur emission control areas (SECA), pushing companies to either install scrubber systems or switch to low-sulfur distillate fuel while transiting these areas.

Military Segment in Shipbuilding Market

The military segment is projected to be the fastest-growing segment in the shipbuilding market between 2024 and 2029, driven by rapid growth in defense spending and increasing geopolitical tensions worldwide. The segment's growth is particularly fueled by maritime disputes between several countries, leading to increased procurement of naval vessels. The demand for destroyers is currently higher than other naval vessels, as various nations are looking to acquire new destroyer ships. The segment is also witnessing significant technological advancements in naval vessel construction, including the integration of advanced combat suites and modernization of naval capabilities.

Remaining Segments in End User Segmentation

The other end users segment in the shipbuilding market encompasses various specialized vessels including weather forecasting ships, ocean station vessels, and offshore support vessels. This segment plays a crucial role in supporting activities such as weather monitoring, marine research, and offshore exploration. The segment is witnessing evolution with the increasing adoption of alternative fuel vessels and the rising demand for specialized offshore support vessels like anchor-handling tug supply (AHTS) ships. The segment is also adapting to changing market dynamics with increased focus on electric and renewable energy-powered vessels.

Shipbuilding Market Geography Segment Analysis

Shipbuilding Market in North America

The North American shipbuilding market demonstrates a robust infrastructure across its key countries, including the United States, Canada, and other territories. The region's shipbuilding capabilities are primarily driven by military vessel construction and commercial shipping requirements. The United States leads the regional market with its extensive network of shipyards and advanced manufacturing capabilities, while Canada maintains a strategic focus on specialized vessel construction and naval fleet modernization. The industry benefits from strong government support through various maritime policies and defense contracts, helping sustain long-term growth and technological advancement in shipbuilding capabilities.

Shipbuilding Market in United States

The United States dominates the North American shipbuilding landscape, accounting for approximately 78% of the regional shipbuilding market share in 2024. The country maintains around 120 shipyards engaged in various shipbuilding operations, with the government being the primary customer of the domestic shipbuilding industry. The U.S. shipbuilding sector is experiencing a transformation driven by increasing demand for eco-friendly vessels and LNG carriers. The Navy's ambitious fleet expansion plans and the government's focus on strengthening domestic shipbuilding capabilities continue to drive market growth. The industry is also witnessing significant investments in modernizing shipyard infrastructure and adopting advanced manufacturing technologies to enhance productivity and maintain a competitive advantage.

Shipbuilding Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 4% during 2024-2029. The country's shipbuilding sector is experiencing significant expansion through its National Shipbuilding Strategy, which has created a favorable environment for both military and commercial vessel construction. Canadian shipyards are increasingly focusing on specialized vessel construction and developing expertise in Arctic-capable ships. The government's long-term strategic agreements with major shipyards and continued investments in facility modernization are strengthening the country's shipbuilding capabilities. The industry is also witnessing increased participation from international shipbuilding companies, contributing to technology transfer and capability enhancement.

Shipbuilding Market in Europe

The European shipbuilding market showcases a diverse landscape with significant contributions from Germany, the United Kingdom, France, and other maritime nations. The region's shipbuilding industry is characterized by its focus on high-value, specialized vessels and advanced maritime technologies. European shipyards excel in producing sophisticated vessels such as cruise ships, specialized offshore vessels, and naval ships. The market benefits from strong research and development initiatives, particularly in developing environmentally friendly shipping solutions and autonomous vessel technologies. The region's shipbuilding sector is supported by well-established maritime clusters that provide crucial upstream and downstream services.

Shipbuilding Market in Germany

Germany stands as the largest shipbuilding market in Europe, representing approximately 17% of the regional market in 2024. The country's shipbuilding industry is supported by about 2,800 companies active in shipbuilding and ocean industries, with nine major shipyards specifically supporting the naval shipbuilding sector. German shipyards are renowned for their technical expertise and innovation in specialized vessel construction. The industry maintains a strong focus on research and development, particularly in environmental technologies and digital solutions for maritime applications. The sector benefits from high domestic value addition and strong integration with the broader maritime industry cluster.

Shipbuilding Market in France

France emerges as the fastest-growing shipbuilding market in Europe, with a projected growth rate of approximately 5% during 2024-2029. The country's shipbuilding industry excels in constructing sophisticated vessels, particularly cruise ships and naval vessels. French shipyards are increasingly focusing on developing environmentally friendly technologies and innovative maritime solutions. The industry benefits from strong government support and strategic partnerships with international maritime players. The country's commitment to reducing maritime emissions and developing next-generation naval capabilities continues to drive innovation and growth in the sector.

Shipbuilding Market in Asia-Pacific

The Asia-Pacific region represents the global powerhouse in shipbuilding, with significant contributions from China, Japan, South Korea, India, and other maritime nations. The region's dominance is supported by extensive shipbuilding infrastructure, cost-competitive manufacturing capabilities, and strong government support. Each country in the region has developed specialized capabilities, with China leading in commercial vessel construction, South Korea excelling in high-value ships, Japan focusing on technological innovation, and India emerging as a growing force in the industry. The region benefits from strong domestic demand, extensive port infrastructure, and well-developed maritime supply chains.

Shipbuilding Market in China

China maintains its position as the largest shipbuilding market in the Asia-Pacific region. The country's shipbuilding industry benefits from extensive infrastructure, including numerous major shipyards and a comprehensive maritime supply chain. Chinese shipbuilders have demonstrated significant capabilities in constructing various vessel types, from commercial carriers to specialized ships. The industry's competitiveness is enhanced by strong government support, continuous technological upgrades, and integration of advanced manufacturing processes. The country's shipbuilding sector continues to expand its global market presence through strategic partnerships and a focus on high-value vessel segments.

Shipbuilding Market in India

India emerges as the fastest-growing shipbuilding market in the Asia-Pacific region. The country's shipbuilding industry benefits from competitive labor costs and a strategic geographical location. Indian shipyards are increasingly focusing on both domestic and international markets, with capabilities spanning various vessel types. The government's supportive policies, including the Shipbuilding Financial Assistance Policy, are helping strengthen domestic shipbuilding capabilities. The industry is witnessing significant modernization efforts and increasing collaboration with international partners to enhance technological capabilities and market reach. The shipbuilding industry in India is poised for growth, driven by these strategic initiatives and expanding market opportunities.

Shipbuilding Market in Rest of the World

The Rest of the World region, encompassing Brazil, Mexico, the United Arab Emirates, and other countries, demonstrates growing capabilities in shipbuilding. Brazil emerges as both the largest and fastest-growing market in this region, supported by its extensive coastline and strategic focus on offshore vessel construction. The region's shipbuilding industry benefits from increasing investments in port infrastructure and maritime capabilities. Mexico's shipbuilding sector focuses on repair and maintenance services, while the UAE is developing its capabilities through strategic partnerships with global ship manufacturing companies in the UAE. These markets are characterized by growing domestic demand and an increasing focus on developing indigenous shipbuilding capabilities to reduce dependence on imports.

Shipbuilding Industry Overview

Top Companies in Shipbuilding Market

The global shipbuilding industry is characterized by continuous innovation and strategic developments among key players like Mitsubishi Heavy Industries, Hyundai Heavy Industries, China State Shipbuilding Corporation, and Samsung Heavy Industries. These leaders in the shipbuilding industry are increasingly focusing on developing eco-friendly vessels and implementing advanced technologies such as AI-driven operating systems and digital transformation initiatives in shipyards. The industry leaders emphasize operational excellence through automation and integrated product development environments to enhance efficiency and reduce human errors. Strategic partnerships and collaborations are being formed to strengthen capabilities in specialized vessel segments like LNG carriers and offshore vessels. Companies are also expanding their geographical presence and production capabilities through facility upgrades and modernization programs, while simultaneously investing in research and development to meet evolving environmental regulations and customer demands.

Asian Dominance Shapes Market Competition Dynamics

The shipbuilding market exhibits a moderately consolidated structure with Asian manufacturers, particularly from South Korea, China, and Japan, holding dominant positions. These major players operate as diversified industrial conglomerates with extensive capabilities across various vessel types and marine technologies. The market is characterized by high entry barriers due to substantial capital requirements, complex regulatory compliance needs, and the importance of long-term relationships with shipyards and component suppliers. Regional players often focus on specialized vessel segments or maintain strong positions in their domestic markets through government support and strategic partnerships.

The industry has witnessed significant consolidation activities, particularly in Asian markets, as companies seek to strengthen their competitive positions and achieve economies of scale. Market leaders are increasingly pursuing vertical integration strategies by developing in-house capabilities for critical components and systems. The competitive landscape is further shaped by government policies and support measures, especially in major shipbuilding nations, which influence market dynamics through subsidies, financing support, and regulatory frameworks. Companies are also forming strategic alliances and joint ventures to share technological expertise and market access.

Innovation and Sustainability Drive Future Success

Success in the shipbuilding market increasingly depends on companies' ability to adapt to environmental regulations and technological advancements. Leaders in the shipbuilding industry are investing heavily in developing green technologies and digital solutions, while smaller players are focusing on specialized market segments and regional strengths. The industry's future competitiveness will be determined by capabilities in areas such as autonomous shipping technology, alternative fuel systems, and smart shipyard operations. Companies are also strengthening their after-sales services and lifecycle support offerings to create additional revenue streams and maintain long-term customer relationships.

For new entrants and smaller players, success lies in identifying and serving niche markets while building strategic partnerships with established players. The increasing focus on environmental regulations and sustainability creates opportunities for companies specializing in eco-friendly technologies and retrofit solutions. Market participants must also consider the growing influence of end-users in vessel design and specification requirements, particularly in specialized segments like LNG carriers and cruise ships. The ability to offer flexible financing solutions and maintain strong relationships with financial institutions remains crucial for market success, given the capital-intensive nature of shipbuilding projects. The world's largest shipyards are continually adapting to these changes to maintain their competitive edge.

Shipbuilding Market Leaders

-

China State Shipbuilding Corporation

-

Mitsubishi Heavy Industries Ltd.

-

Samsung Heavy Industries

-

Daewoo Shipbuilding & Marine Engineering Co., Ltd

-

Hyundai Heavy Industries Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Shipbuilding Market News

- August 2023: The Canadian government announced that it would invest CAD 463 million (USD 345 million) in shipbuilding infrastructure to move forward with the Surface Combatant (CSC) program. It calls for the construction of 15 new warships that will be a key component of the future Royal Canadian Navy. The funds will be used to prepare the Irving Shipyard and adjacent facilities in Nova Scotia for construction, which is now slated to begin next year for the program.

- May 2023: Vard Marine Inc., in collaboration with Team Vigilance partner firms Heddle Shipyards, Thales Canada, SH Defence, and Fincantieri, unveiled the Vigilance Offshore Patrol Vessel at CANSEC 2023. Team Vigilance partner firms collectively bring extensive and significant capabilities and expertise to bear in naval ship design, Canadian and worldwide construction, combat and offboard system integration, modular payload systems, and life-cycle solutions.

- May 2023: Garden Reach Shipbuilders and Engineers Ltd established the GRSE Accelerated Innovation Nurturing Scheme to find and stimulate the creation of new solutions as part of the shipyard's technological development activities. GAINS intends to address current and emerging ship design and construction issues while simultaneously accomplishing the goals of Atmanirbhar Bharat.

- March 2023: The Ministry of Ports, Shipping, and Waterways (MoPSW) in India launched the 'Green Tug Transition Programme' (GTTP) to make India a global hub for building green ships. The GTTP will convert all tugboats operating in the country into 'Green Hybrid Tugs' that run on non-fossil fuels such as Methanol, Ammonia, and Hydrogen.

Shipbuilding Industry Segmentation

Shipbuilding is the construction of large seagoing vessels, primarily of steel, but other materials, such as wood and composites, can also be employed.

The shipbuilding market is segmented by type, by end-user, and by geography. By type, the market is segmented into vessel, container, passenger, and other types. By end user, the market is segmented into transport companies, military, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the rest of the World.

The report offers the market sizes and forecast in value in (USD ) for all the above segments.

| Type | Vessel | ||

| Container | |||

| Passenger | |||

| Other Types | |||

| End User | Transport Companies | ||

| Military | |||

| Other End Users | |||

| Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Rest of the World | Brazil | ||

| Mexico | |||

| United Arab Emirates | |||

| Other Countries | |||

| Vessel |

| Container |

| Passenger |

| Other Types |

| Transport Companies |

| Military |

| Other End Users |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Rest of the World | Brazil |

| Mexico | |

| United Arab Emirates | |

| Other Countries |

Shipbuilding Market Research FAQs

How big is the Shipbuilding Market?

The Shipbuilding Market size is expected to reach USD 152.72 billion in 2025 and grow at a CAGR of 4.84% to reach USD 193.43 billion by 2030.

What is the current Shipbuilding Market size?

In 2025, the Shipbuilding Market size is expected to reach USD 152.72 billion.

Who are the key players in Shipbuilding Market?

China State Shipbuilding Corporation, Mitsubishi Heavy Industries Ltd., Samsung Heavy Industries, Daewoo Shipbuilding & Marine Engineering Co., Ltd and Hyundai Heavy Industries Co. Ltd. are the major companies operating in the Shipbuilding Market.

Which is the fastest growing region in Shipbuilding Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Shipbuilding Market?

In 2025, the Asia Pacific accounts for the largest market share in Shipbuilding Market.

What years does this Shipbuilding Market cover, and what was the market size in 2024?

In 2024, the Shipbuilding Market size was estimated at USD 145.33 billion. The report covers the Shipbuilding Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Shipbuilding Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.