Market Size of Global STD Diagnostics Industry

| Study Period | 2019 - 2029 |

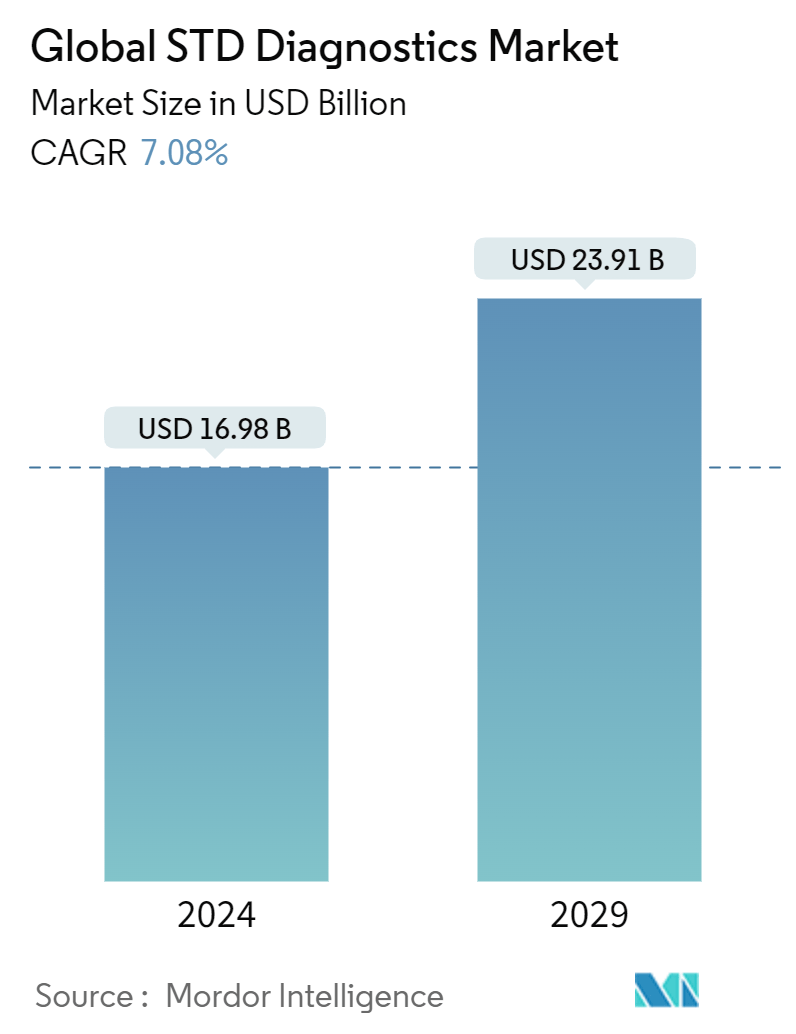

| Market Size (2024) | USD 16.98 Billion |

| Market Size (2029) | USD 23.91 Billion |

| CAGR (2024 - 2029) | 7.08 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

STD Diagnostics Market Analysis

The Global STD Diagnostics Market size is estimated at USD 16.98 billion in 2024, and is expected to reach USD 23.91 billion by 2029, growing at a CAGR of 7.08% during the forecast period (2024-2029).

Sexually transmitted diseases (STDs) are spread mainly by sexual contact. Sexually transmitted diseases (STIs) are caused by bacteria, viruses, or parasites. These STIs-causing microorganisms can be diagnosed by using STD diagnostics and help in receiving proper treatment. Factors such as the growing prevalence of STDs globally, growing government initiatives to create awareness about STDs, and increasing advancement in STD diagnostics are anticipated to drive the STD diagnostics market during the forecast period. The rising prevalence of STDs is expected to drive the market during the forecast period. For instance, the World Health Organization Report 2023 reported that more than 1.0 million sexually transmitted infections are acquired globally, and most of them are asymptomatic. It also reported that every year, there are an estimated 374.0 million new infections, with 1 out of 4 sexually transmitted infections: gonorrhea, chlamydia, trichomoniasis, and syphilis. Therefore, such an increasing prevalence and incidence rate of sexually transmitted diseases around the globe is expected to increase the demand for STD diagnostics, thereby propelling market growth during the forecast period. Also, the increasing government organizations' initiatives to create awareness about STDs are expected to increase the demand for STD diagnostics procedures for early detection of infections. For instance, in March 2022, the National Chlamydia Screening Program (NCSP) was organized in the United Kingdom. The major focus of this program was to reduce the harm of untreated chlamydia infection by primarily screening women and girls. In June 2022, the Centers for Disease Control and Prevention (CDC) recommended and issued guidelines for screening sexually transmitted diseases to create awareness toward screening programs for STDs and the increasing burden of STDs around the globe. Hence, such initiatives by government organizations are expected to drive the demand for the diagnosis of STDs, which is expected to drive the market during the forecast period. Also, advancements in STD diagnostics, research, and the development of new technologies are projected to fuel market growth. Also, the market is witnessing a major shift from conventional technologies to molecular diagnostics for the diagnosis of STDs, which is a breakthrough for the growth of the market. For instance, in May 2022, Medmira Inc. received a CE mark for its Multiplo complete syphilis (TP/nTP) antibody test (Multiplo TP/nTP). This approval enables the company to strengthen further its product offering in all markets that accept the CE mark. Hence, the rising prevalence of STDs, increasing government organizations' initiatives to increase awareness about STDs, and increasing product launches are expected to drive the STD diagnostic market. However, the social stigma associated with patients visiting specialized STD clinics and stringent regulatory scenarios for product approvals is expected to restrain the market during the forecast period.

STD Diagnostics Industry Segmentation

As per the scope of the report, STDs are infections that transmit from one person to another during oral, anal, and vaginal sex. Bacteria, parasites, yeast, and viruses are the main causes of STDs. Rapid and early diagnosis of STDs will limit the effects and progression of the disease. If the STDs are left untreated, they can lead to more serious and long-term health complications. The STD diagnostics market is segmented by type of disease, location of diagnostic test, device, and geography. By type, the market is segmented into chlamydia, gonorrhea, syphilis, genital herpes, hepatitis B, HIV/AIDS (human immunodeficiency virus and acquired immune deficiency syndrome), human papillomavirus, and other diseases. By devices, the market is segmented into laboratory devices (thermal cyclers - PCR, lateral flow readers immunochromatographic assays, flow cytometers, absorbance microplate reader - enzyme-linked immunosorbent assay (ELISA), and other laboratory devices) and point-of-care devices, phone chips (microfluidics + ICT), and portable/benchtop/rapid diagnostic kits). By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across significant global regions. The report offers the value (in USD) for the above segments.

| By Type of Disease | |

| Chlamydia | |

| Gonorrhea | |

| Syphilis | |

| Genital herpes | |

| Hepatitis B | |

| HIV/AIDS (Human immunodeficiency virus infection and acquired immune deficiency syndrome) | |

| Human papillomavirus (HPV) | |

| Other Diseases |

| By Location of Diagnostic Test | |

| Laboratory Testing | |

| Point-of-care (PoC) Testing |

| By Devices | |||||||

| |||||||

|

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Global STD Diagnostics Market Size Summary

The STD diagnostics market is poised for significant growth, driven by the increasing prevalence of sexually transmitted diseases worldwide and heightened awareness through educational campaigns and government initiatives. The market is experiencing a shift from conventional diagnostic methods to advanced molecular diagnostics, which is expected to enhance the accuracy and efficiency of STD detection. The COVID-19 pandemic initially disrupted screening rates, but the subsequent rise in awareness and the implementation of targeted screening programs have rekindled demand for diagnostic solutions. The market is characterized by continuous advancements in technology and product offerings, with key players like Abbott Laboratories and Qiagen Inc. leading the charge in developing innovative diagnostic tests.

North America dominates the global STD diagnostics market, largely due to the high prevalence of STDs and the presence of numerous diagnostic companies. The United States, in particular, is witnessing a surge in demand for diagnostic processes, fueled by the significant number of reported cases and government initiatives aimed at reducing the incidence of STDs. The market's competitive landscape is marked by strategic partnerships and product licensing agreements among major players, ensuring a steady influx of new technologies and solutions. As the market continues to evolve, the focus on early detection and intervention remains paramount, promising substantial growth opportunities in the coming years.

Global STD Diagnostics Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Growing Incidence and Prevalence Rates of STD

-

1.2.2 Implementation of National Screening Programs

-

1.2.3 Growing Innovations in the Development of STD Diagnostics

-

-

1.3 Market Restraints

-

1.3.1 Social Stigma Associated with Patients Visiting Specialized STD Clinics

-

1.3.2 Stringent Regulatory Scenario for Product Approvals

-

-

1.4 Porter's Five Force Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value - USD)

-

2.1 By Type of Disease

-

2.1.1 Chlamydia

-

2.1.2 Gonorrhea

-

2.1.3 Syphilis

-

2.1.4 Genital herpes

-

2.1.5 Hepatitis B

-

2.1.6 HIV/AIDS (Human immunodeficiency virus infection and acquired immune deficiency syndrome)

-

2.1.7 Human papillomavirus (HPV)

-

2.1.8 Other Diseases

-

-

2.2 By Location of Diagnostic Test

-

2.2.1 Laboratory Testing

-

2.2.2 Point-of-care (PoC) Testing

-

-

2.3 By Devices

-

2.3.1 Laboratory Devices

-

2.3.1.1 Thermal Cyclers - PCR

-

2.3.1.2 Lateral Flow Readers Immunochromatographic Assays

-

2.3.1.3 Flow Cytometers

-

2.3.1.4 Absorbance Microplate Reader - Enzyme Linked Immunosorbent Assay (ELISA)

-

2.3.1.5 Other Laboratory Devices

-

-

2.3.2 Point-of-care (PoC) Devices

-

2.3.2.1 Phone Chips (Microfluidics + ICT)

-

2.3.2.2 Portable/Bench Top/Rapid Diagnostic Kits

-

-

-

2.4 Geography

-

2.4.1 North America

-

2.4.1.1 United States

-

2.4.1.2 Canada

-

2.4.1.3 Mexico

-

-

2.4.2 Europe

-

2.4.2.1 Germany

-

2.4.2.2 United Kingdom

-

2.4.2.3 France

-

2.4.2.4 Italy

-

2.4.2.5 Spain

-

2.4.2.6 Rest of Europe

-

-

2.4.3 Asia-Pacific

-

2.4.3.1 China

-

2.4.3.2 Japan

-

2.4.3.3 India

-

2.4.3.4 Australia

-

2.4.3.5 South Korea

-

2.4.3.6 Rest of Asia-Pacific

-

-

2.4.4 Middle East and Africa

-

2.4.4.1 GCC

-

2.4.4.2 South Africa

-

2.4.4.3 Rest of Middle East and Africa

-

-

2.4.5 South America

-

2.4.5.1 Brazil

-

2.4.5.2 Argentina

-

2.4.5.3 Rest of South America

-

-

-

Global STD Diagnostics Market Size FAQs

How big is the Global STD Diagnostics Market?

The Global STD Diagnostics Market size is expected to reach USD 16.98 billion in 2024 and grow at a CAGR of 7.08% to reach USD 23.91 billion by 2029.

What is the current Global STD Diagnostics Market size?

In 2024, the Global STD Diagnostics Market size is expected to reach USD 16.98 billion.