Market Size of Service Delivery Platform Industry

| Study Period | 2019 - 2029 |

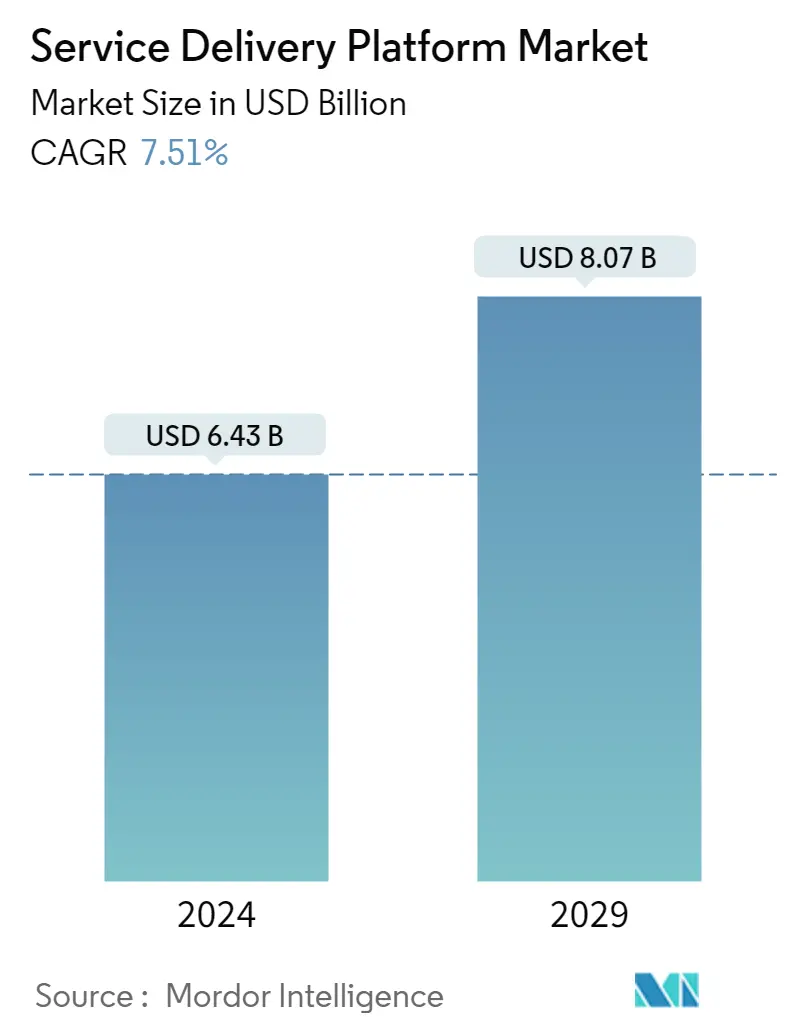

| Market Size (2024) | USD 6.43 Billion |

| Market Size (2029) | USD 8.07 Billion |

| CAGR (2024 - 2029) | 7.51 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Service Delivery Platform Market Analysis

The Service Delivery Platform Market size is estimated at USD 6.43 billion in 2024, and is expected to reach USD 8.07 billion by 2029, growing at a CAGR of 7.51% during the forecast period (2024-2029).

- To facilitate the exchange of optimized services among operators, service and content providers, and users, service delivery platforms (SDPs) - which are operator solutions - provide a unified middle ground. The rising trend of "health system strengthening" (HSS) has become influential in global health circles, boosting the service delivery platform market. SDPs are a framework that supports a wide range of applications, targets different networks, and offers users extensive services. To provide a platform for session control, service development, protocol execution, and technology and network boundary crossing, SDPs require the integration of IT capabilities.

- To establish more physical delivery platforms, companies are customizing services for different industries, upgrading the delivery dispatch system, and enhancing delivery infrastructure. In 2022, Intel maintained its position as the top network silicon vendor by introducing the Intel Network Platform, as well as new product enhancements for 5G and Edge.

- Companies are aiming to develop a service delivery platform that allows telecom operators to access convergent, multimedia, and "Web 2.0" services on their mobile devices

- Furthermore, In June 2023, CWT announced a strategic partnership to provide Spotnana's next-generation Travel-as-a-Service platform to the market. This collaboration is an important step in CWT's strategy to bring innovative solutions to customers looking to deploy pioneering technology, driven by the strength of CWT's people and holistic, global approach.

- Moreover, in November 2023, Indosat Ooredoo Hutchison (IOH) and TIMWETECH announced the successful deployment of TIMWETECH's Digital Service Delivery Platform. Integrating the DSDP platform is a significant step for Indosat's partner onboarding. This advanced platform facilitates integration processes, significantly reducing the time required to bring services to the market and fostering smooth collaboration with various partners. It is especially effective in engaging with OTT service providers, who dominate the telco industry's digital content and service sector.

Service Delivery Platform Industry Segmentation

The service delivery platform helps in creating a structure that enables the operators to create, deliver, and manage services. The report offers a comprehensive evaluation of the market. The market has been segmented by type and geography.

The service delivery platform market is segmented by type (software, services) and geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| By Type | |

| Software | |

| Services |

| Geography | ||||||

| ||||||

| ||||||

| ||||||

| Rest of the World |

Service Delivery Platform Market Size Summary

The service delivery platform market is poised for significant growth, driven by the increasing demand for optimized service exchange among operators, service providers, and users. These platforms serve as a unified framework, supporting a diverse range of applications and networks, and are essential for session control, service development, and protocol execution. The trend of health system strengthening has notably influenced the market, alongside advancements in cloud adoption and software-defined data centers. Companies are actively customizing services for various industries and enhancing delivery infrastructure to meet the evolving needs of telecom operators and other sectors. Strategic partnerships and technological innovations, such as Intel's Network Platform and CWT's collaboration with Spotnana, are further propelling the market forward.

The market landscape is characterized by the presence of major players like Huawei Technologies, HCL Technologies, and Fujitsu, who are leveraging research and development, strategic partnerships, and mergers to enhance their market share and profitability. The integration of service delivery platforms in sectors such as connected cars, data centers, and government services presents lucrative opportunities for growth. Notable developments include Fujitsu's EDI shared operating platform for the food distribution industry and Deloitte's expansion of its digital service delivery platform for government agencies. These initiatives, along with the introduction of platforms like Quantum's MyQuantum and Tech Mahindra's Cloud BlazeTech, underscore the market's dynamic nature and the continuous innovation driving its expansion.

Service Delivery Platform Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Introduction to Market Drivers and Restraints

-

1.3 Market Drivers

-

1.3.1 Rise in Demand for Data and Content-related Services

-

1.3.2 Rising Demand for High Performance Smartphones

-

1.3.3 Increasing Use of Platform-as-a-service (PaaS)

-

-

1.4 Market Restraints

-

1.4.1 High Initial Investments

-

-

-

2. MARKET SEGMENTATION

-

2.1 By Type

-

2.1.1 Software

-

2.1.2 Services

-

-

2.2 Geography

-

2.2.1 North America

-

2.2.1.1 United States

-

2.2.1.2 Canada

-

-

2.2.2 Europe

-

2.2.2.1 Germany

-

2.2.2.2 United Kingdom

-

2.2.2.3 France

-

2.2.2.4 Rest of the Europe

-

-

2.2.3 Asia-Pacific

-

2.2.3.1 China

-

2.2.3.2 Japan

-

2.2.3.3 India

-

2.2.3.4 Rest of Asia-Pacific

-

-

2.2.4 Rest of the World

-

-

Service Delivery Platform Market Size FAQs

How big is the Service Delivery Platform Market?

The Service Delivery Platform Market size is expected to reach USD 6.43 billion in 2024 and grow at a CAGR of 7.51% to reach USD 8.07 billion by 2029.

What is the current Service Delivery Platform Market size?

In 2024, the Service Delivery Platform Market size is expected to reach USD 6.43 billion.